Heychli

Introduction

It’s time to talk about one of my favorite stocks in the aerospace industry. Pittsburgh, Pennsylvania, based Howmet Aerospace (NYSE:HWM) is not only one of the most interesting suppliers of high-quality aerospace parts, but it is also one of the best performers in the industry this year. The company is seeing higher margins, a strong rebound in orders, and a wave of free cash flow used to reduce debt and reward shareholders. All of this is happening while long-haul air traffic is still suffering. While ongoing economic difficulties are preventing the stock from breaking out, I remain extremely bullish on the company’s long-term prospects as outperformance is the base case in my book.

So, without further ado, let’s look at the details!

What’s Howmet Aerospace?

On one hand, Howmet Aerospace is a very old company. It dates back to 1926 with the founding of Austenal, a company focused on manufactured materials for dental appliances. On the other hand, the company is relatively young as it is a product of two major spin-offs that happened rather “recently”.

In 2016, aluminum giant Alcoa (AA) spun off its bauxite, alumina, and aluminum operations to a new company, which got the name Alcoa – that’s Alcoa the way it’s known today.

The remaining company was named Arconic (ARNC), which split again into two separate businesses. Arconic was renamed Howmet Aerospace. The spin-off was named Arconic. The separation became effective on April 1, 2020, roughly two months after the COVID-19 news broke.

I believe that all of these spin-offs were great decisions as they basically ended up providing investors with the opportunity to own three companies, each at a different stage of the aluminum supply chain.

In the case of this article’s star, Howmet, the company has a $14.9 billion market cap, which makes it one of the world’s largest suppliers in the aerospace industry.

The company is a global leader in lightweight metals engineering and manufacturing.

What’s interesting is that the company is not officially an aerospace and defense company – although I call it that, and will continue to do so. The company is operating in the specialty industrial machinery industry as it has high non-aerospace exposure.

However, aerospace is the company’s bread and butter. Using pre-pandemic numbers, the company generated close to 80% of its sales from aerospace operations – both commercial and defense.

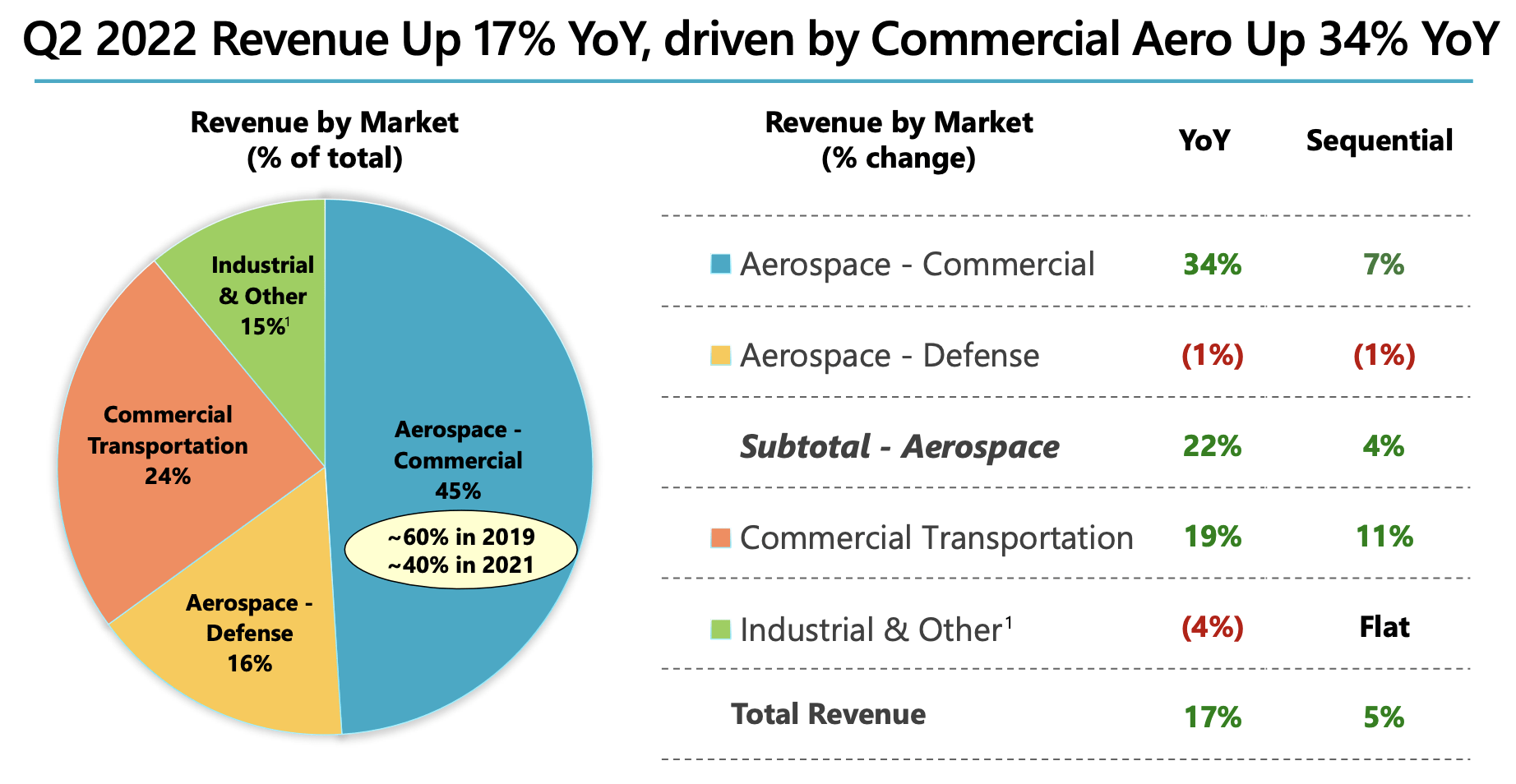

Howmet Aerospace 2Q22 Earnings Presentation

On top of that, the company produces products for industrial and commercial transportation customers.

Based on that context, the company operates four business segments. The first three are completely dominated by aerospace operations.

Engine Products utilizes advanced designs and techniques to support next-generation engine programs and produces components primarily for aircraft engines and industrial gas turbines, including airfoils and seamless rolled rings. Engine Products produces rotating parts as well as structural parts.

Fastening Systems produces aerospace and industrial fasteners, latches, bearings, fluid fittings and installation tools. In addition to highly engineered aerospace fasteners with a broad range of fastening systems, the segment also supplies the commercial transportation, renewable, and material handling industries.

Engineered Structures produces titanium ingots and mill products for aerospace and defense applications and is vertically integrated to produce titanium forgings, extrusions, forming and machining services for airframe, wing, aero-engine, and landing gear components.

Forged Wheels manufactures forged aluminum wheels for trucks, buses, and trailers and related products for the global commercial transportation market.

While the company believes that competitors can produce competing products with similar production techniques, the company continues to be a leader in its industries thanks to its production capabilities and expertise in what are often true niche segments.

The company’s largest competitor is Warren Buffett’s Berkshire Hathaway, which owns the Precision Castparts Corporation.

Improving Results, Outperforming Capital Gains

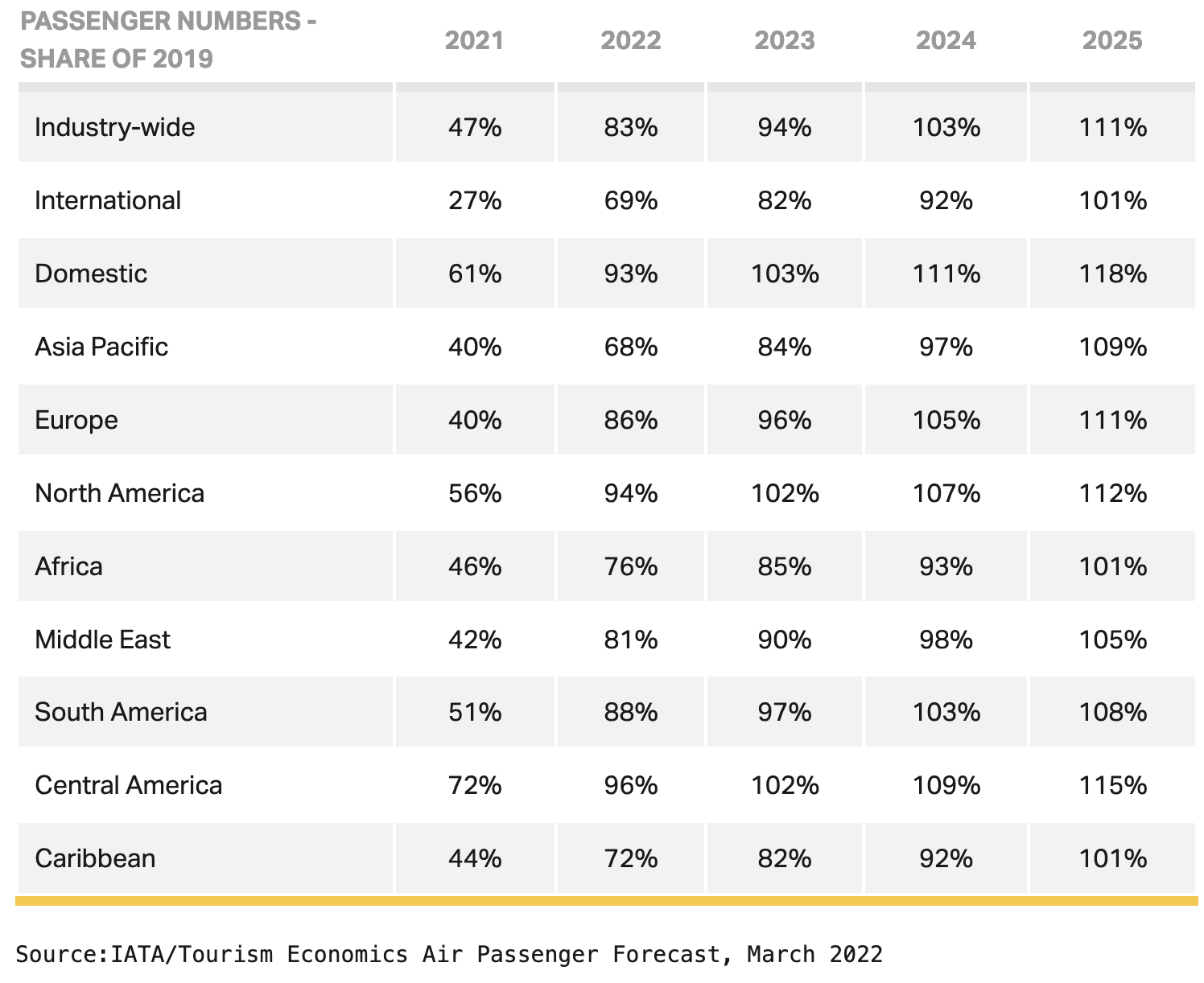

Earlier this year, the IATA released its commercial aerospace outlook. What we’re looking at below is a study that shows that 2024 will see a return to pre-pandemic levels (slightly better). This will be driven by domestic flights that are set to recover in 2023. Asia is not expected to recover until 2025. The same goes for international flights.

IATA

That’s a huge deal for a number of reasons. First, aerospace was one of the best places to be prior to the pandemic. Demand growth was strong as global population growth and an expanding middle class in Asia caused demand for air travel to rise consistently. The pandemic ended that trend – or at least it caused a significant setback.

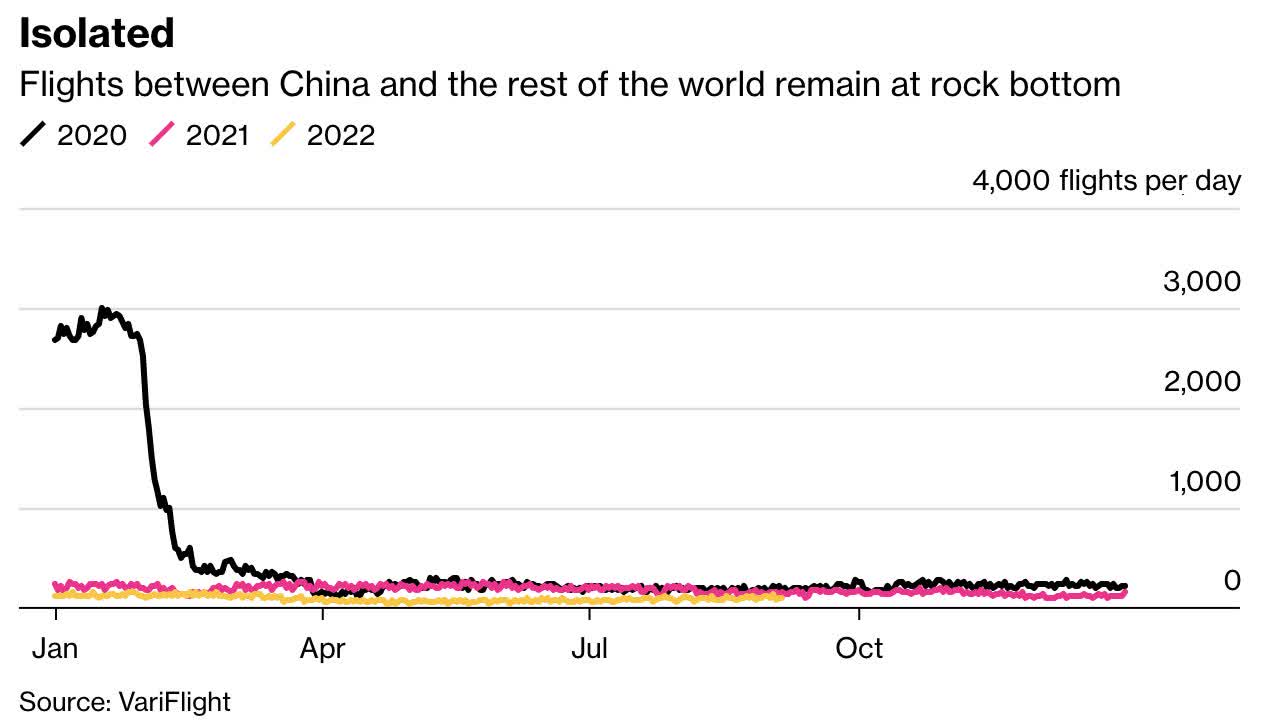

While demand is almost back to normal in the US, China continues to be an outlier. According to recent numbers, flights from and to China are below 2021 and 2020 levels as the government continues to use harsh lockdowns as a way to fight the pandemic.

VariFlight, Via Bloomberg

Howmet also commented on these developments as it sees strong growth in narrow-body (domestic, short flights) with Airbus leading with the A320 production.

With regard to long-haul/wide-body demand, the company commented:

Wide-body aircraft production is viewed as stable in the second half, and we are beginning to see spares demand increase due to improvements in international travel.

Our view is that the build of wide-body aircraft improves as we move through into 2023, especially with the production of the Boeing 787 restarting and combine that with the increases at Airbus of the A330 and A350.

The forecast for 787 production in 2022 is cut again from 25 aircraft I talked about in the last quarter’s earnings call to 15 as our best estimate, although we are now optimistic about the future, given the clearance by the FAA to restart deliveries.

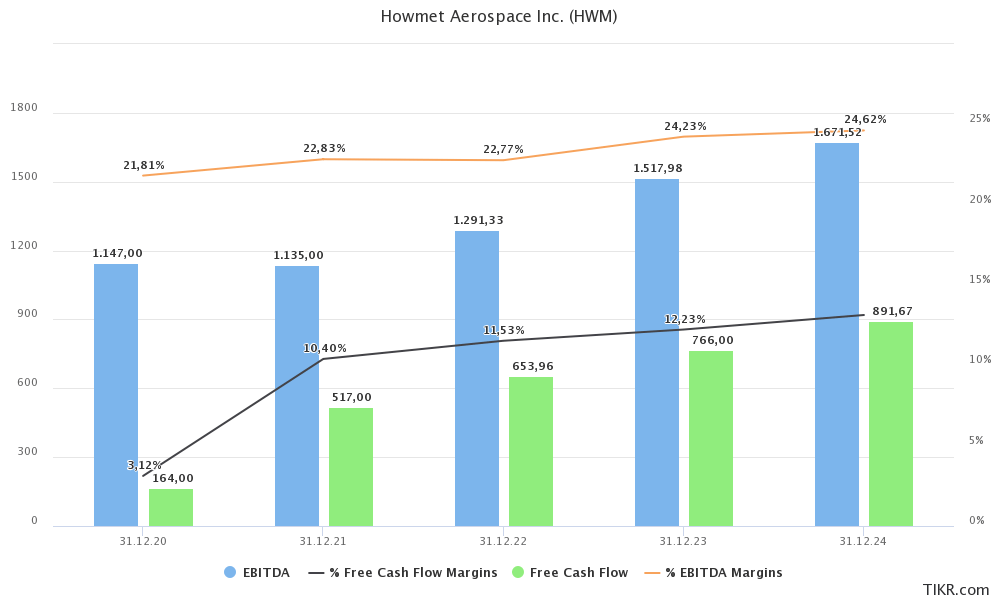

While we don’t have pre-pandemic numbers for Howmet as it was still attached to Arconic in 2019, we know that the company is starting to gain momentum this year as sell-side analysts expect close to $1.3 billion in EBITDA with free cash flow exceeding $650 million. This implies an FCF yield of 4.4%, which is impressive for two reasons. First, the market cap is close to its all-time high as investors have priced in a big part of the aerospace recovery, this pressures the FCF yield. Also, I’m using 2022 expectations, which will be exceeded in the years ahead as long-haul demand improves. The takeaway here is that HWM is truly in a great spot to generate long-term shareholder value.

TIKR.com

In 2Q22, for example, engine products saw 20% revenue growth with adjusted EBITDA rising by 38% thanks to an 80 basis points margin expansion. The narrow-body (short-haul travel) recovery is in full swing, oil and gas customers are causing higher demand, and productivity gains more than offset inflationary headwinds.

Fastening systems saw 6% growth, which was somewhat underwhelming due to the decline in industrial growth (in general), lower Boeing 787 production rates, and higher inflationary costs, which caused adjusted EBITDA to fall by 11% as margins fell from 21.0% to 20.2%.

Forged wheels also saw significant inflationary pressure. Sales grew 22% thanks to 7% higher volumes and high commercial transportation demand. Also, manufacturers are now seeing easing supply chains, which allows them to work on backlog. Hence, higher orders for suppliers like HWM.

However, due to higher inflation and what seems to be persisting supply chain issues, 22% sales growth ended up pushing adjusted EBITDA up only 7%.

Moreover, thanks to these numbers, the company lowered the net debt ratio to 3.0x EBITDA. This number is expected to end the year at 2.5x, and 1.6x in 2024.

Hence, management is now looking to use free cash flow for shareholders. The company has committed $343 million for buybacks and dividends in the first half of this year, including July. That’s 2.3% of the market cap, and it mainly consists of buybacks. The current dividend yield is 0.2% based on an $0.08 annual dividend payment per share. This dividend is expected to double in 4Q22. It will still only give investors a 0.44% yield, but it’s a good start as management is on its way to generating a lot of cash, as I briefly mentioned.

Valuation

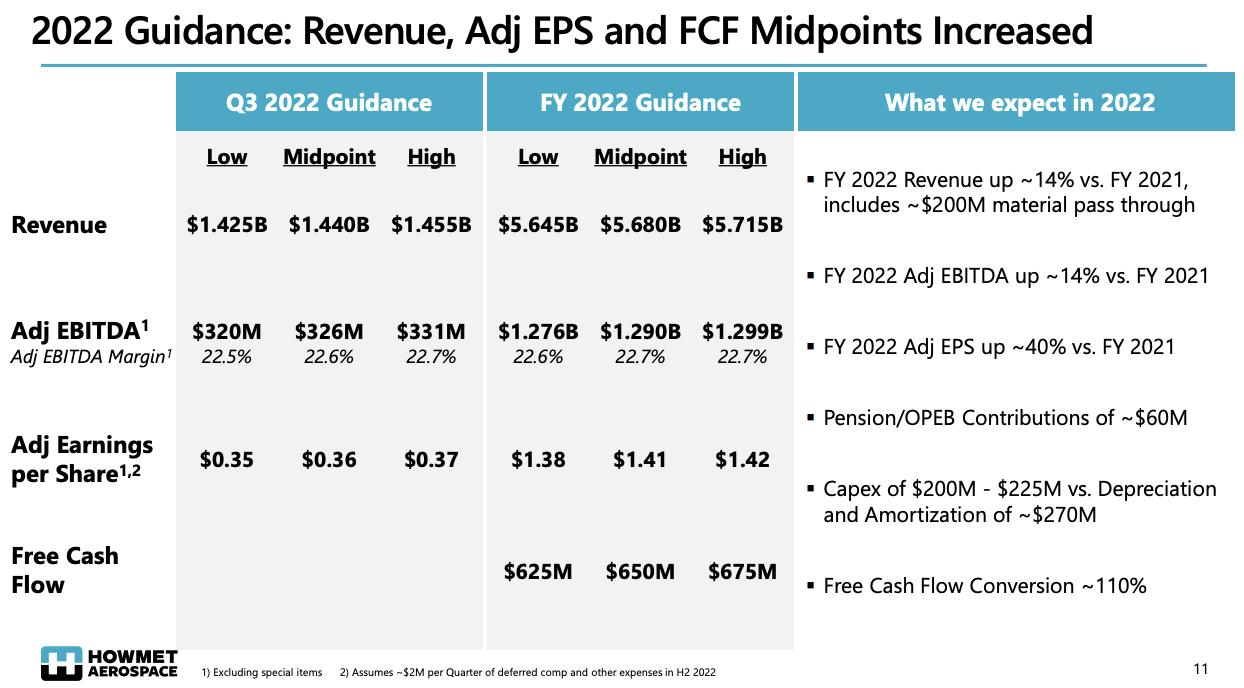

The slide below shows the company’s 2022 guidance. The midpoint is basically what analysts expect as well, according to the TIKR chart I showed earlier in this article.

Howmet Aerospace 2Q22 Earnings Presentation

However, for the company’s valuation, I like to look beyond 2022 as I use 2023 numbers. Right now, the company has an implied enterprise value of $18.7 billion consisting of its $14.9 billion market cap, $2.9 billion in 2023E net debt, and $860 million in pension-related liabilities. That’s roughly 12.3x 2023E EBITDA of $1.5 billion.

This valuation is fair, in general. However, it gets better as the upswing in aerospace demand is now finally translating to lasting orders growth. Moreover, HWM has great pricing power, which helps to offset inflation. Between 2023 and 2024, EBITDA is expected to grow by another 10.1% with margins reaching 24.6%. This could end up pushing free cash flow to $900 million, or 6% of the company’s market cap. We’re talking 2024, but that’s still an absolutely impressive number.

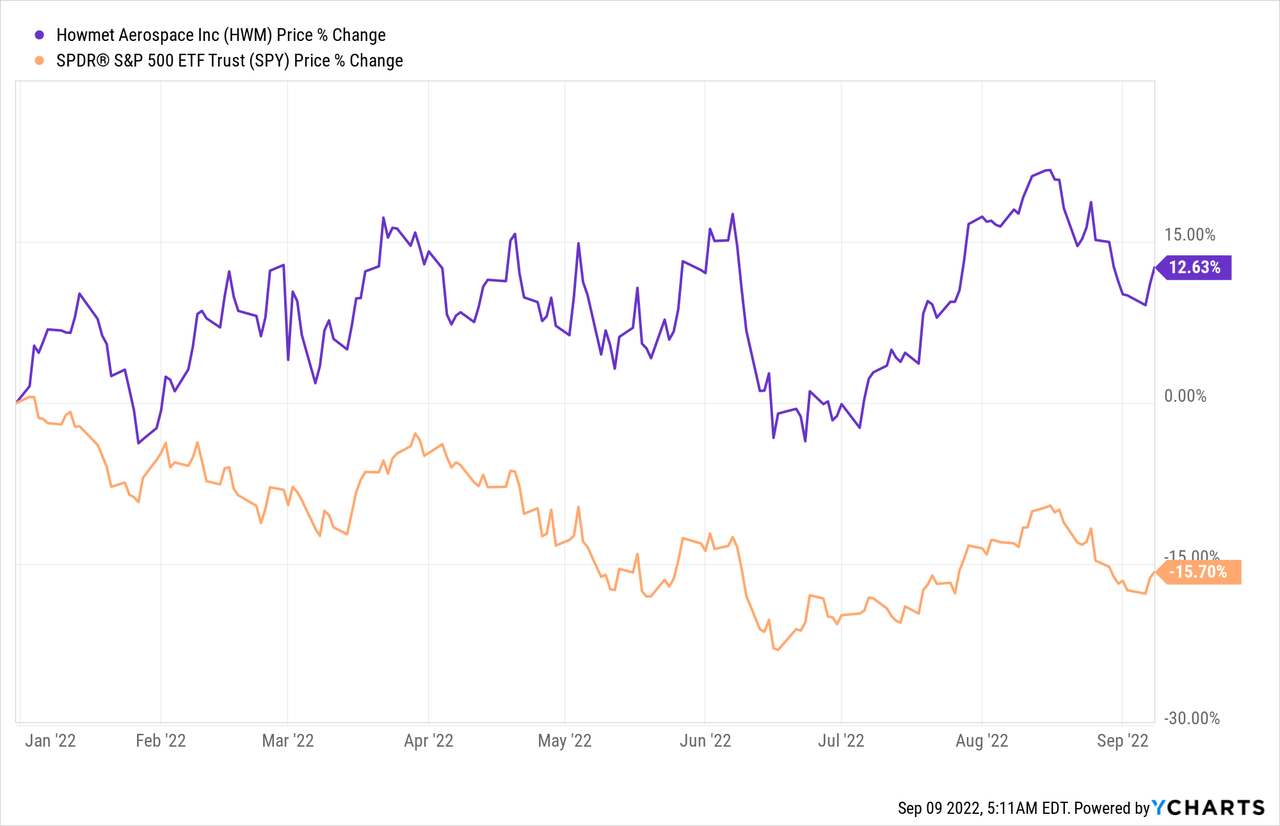

Hence, HWM is trading close to its all-time high, adding 12.6% to its market cap year to date, while the S&P 500 is 15.7% below its all-time high.

Takeaway

The only reason why I don’t own HWM is that I’m massively overweight industrials and aerospace stocks already. Close to 22% of my entire net worth is invested in aerospace & defense companies.

Yet, that doesn’t make HWM a less-quality stock. If anything, I think HWM is one of the best aerospace suppliers in the world. The company offers a range of highly-competitive products that go far up the value chain. The company has great pricing power and customers that are starting to boost production rates again, which includes replenishing depleted inventories.

HWM is in a good spot to generate double-digit EBITDA growth for years to come, which brings a wave of free cash flow used to reduce debt and accelerate shareholder distributions.

Moreover, the company is very attractively valued and outperforming the S&P 500 despite economic challenges and an aggressive Fed.

While I do not believe that HWM will suddenly explode to the upside due to the aforementioned economic challenges, I have little doubt that HWM is in a terrific spot to outperform the market on a long-term basis, generating high total returns for investors.

(Dis)agree? Let me know in the comments!

Be the first to comment