Marti157900

Thesis

I would like to like AMC Entertainment Holdings (NYSE:AMC). But the company’s financials are a mess. For the trailing twelve months, AMC generated a loss from continuing operations of $820 million. Moreover, with a net debt position of approximately $9.5 billion, AMC does not have a strong enough balance sheet to continue absorbing such enormous losses.

However, I argue that it is too early to write off any value for the world’s largest movie theater chain, as 2023 might offer some upside on the backdrop of a strong movie release pipeline. Personally, I value AMC at $4.07/share, assuming a successful turnaround for the movie theater industry. But given the risks and uncertainty, the stock is a ‘Hold’ for now.

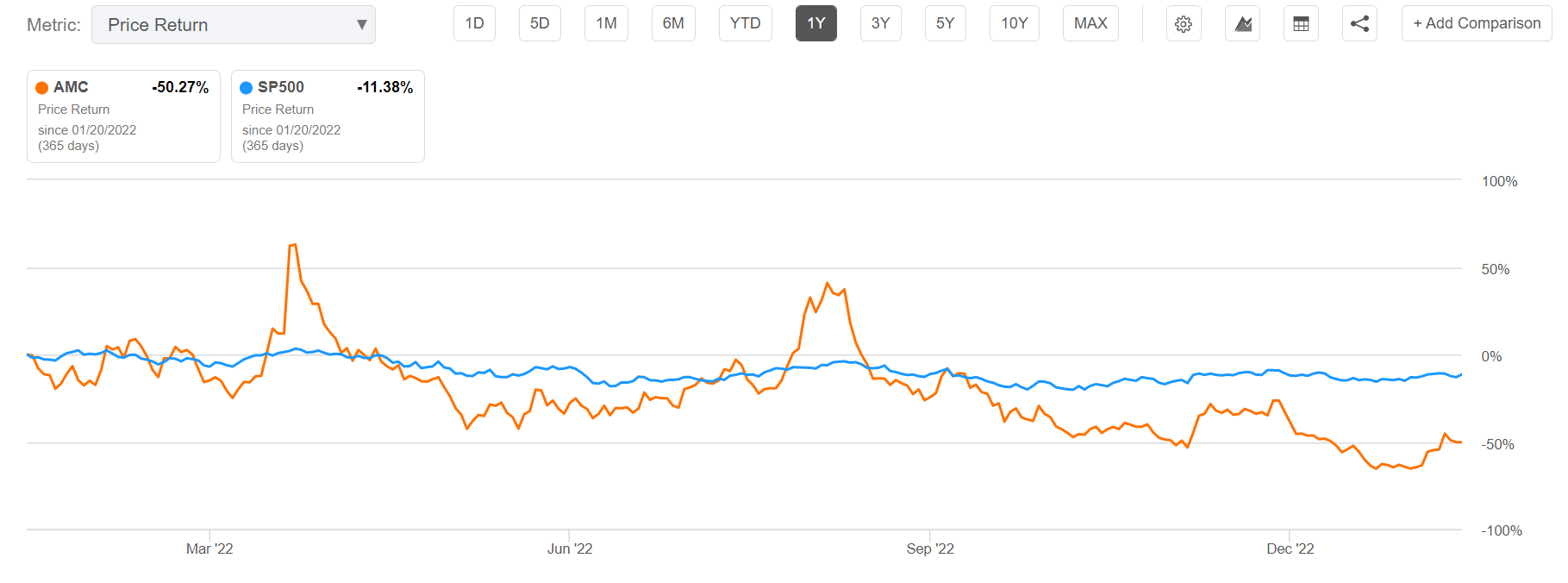

For reference, AMC stock is down approximately 504% for the past twelve months, as compared to a loss of about 11.5% for the S&P 500 (SPY).

Seeking Alpha

AMC’s Financials Are A Mess

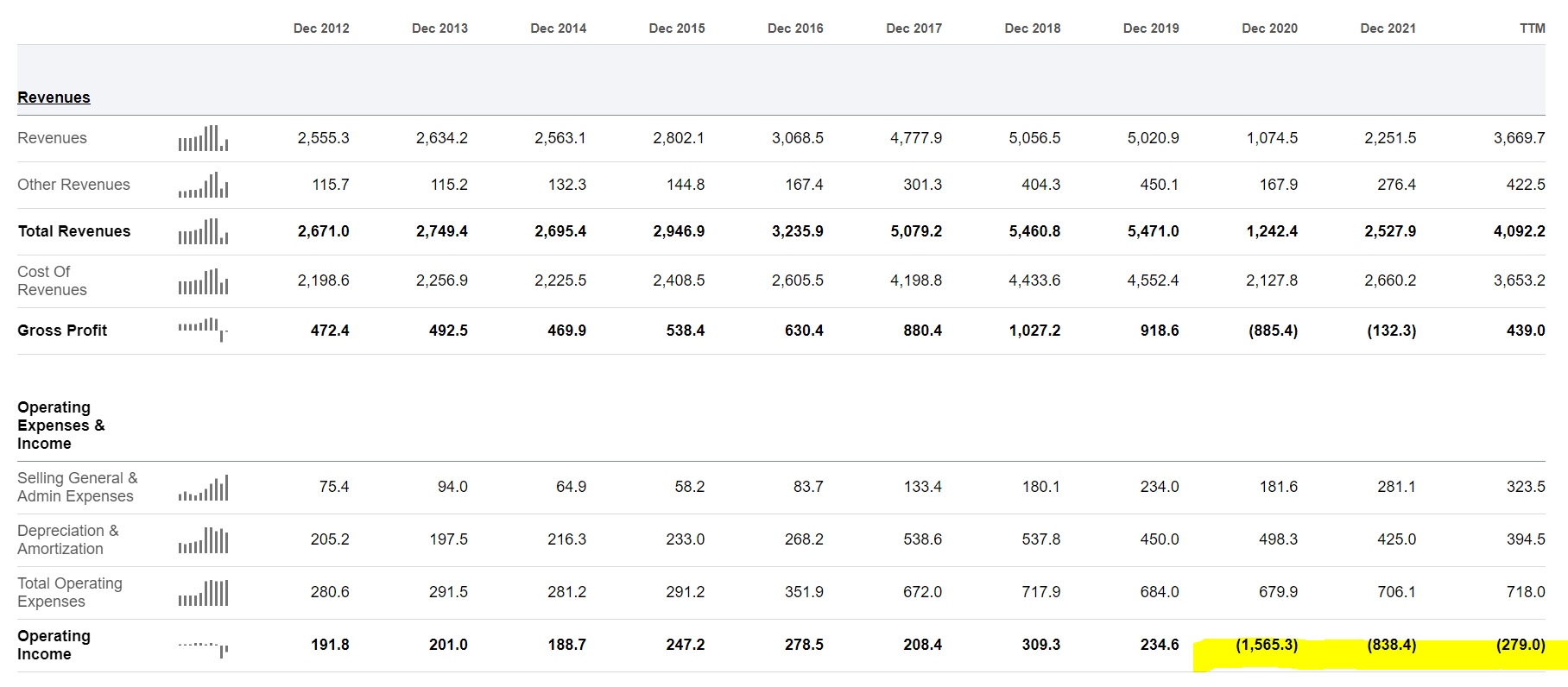

Although AMC stock is down more than 90% from all-time highs, it is hard to argue that the company offers value to investors. Looking at AMC’s income statement for the trailing twelve months, I would like to point out that AMC generated an operating loss of $279 million, on revenues equal to approximately $3.7 billion.

Seeking Alpha

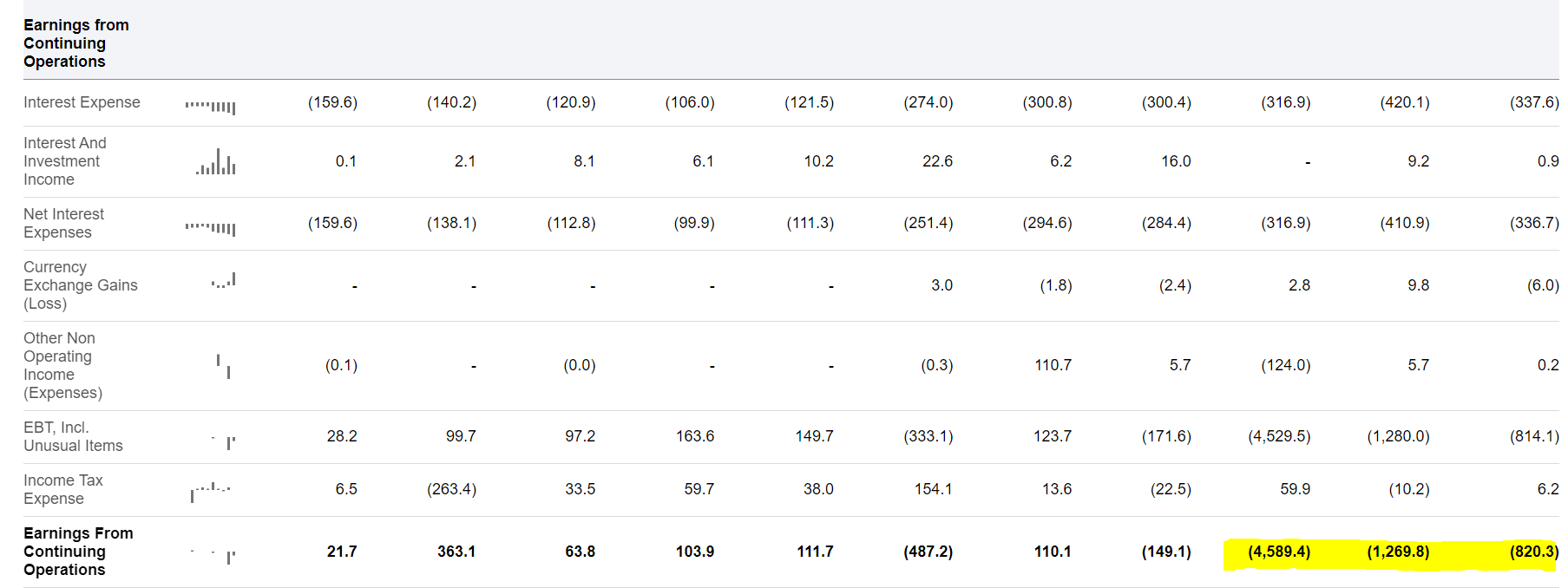

Notably, if an analyst also accounts for AMC’s interest payments – which are most certainly real costs to the firm and shareholders – then AMC’s losses expand to $820 million. It is worth highlighting, however, that the trend is showing a positive traction: AMC’s losses from continuing operations have narrowed as compared to 2021 (- $1.3 billion). And 2021’s losses have already narrowed significantly versus 2020’s (-$4.6 billion).

Seeking Alpha

However, if AMC is hoping to survive, financially, the company needs to write black numbers as soon as possible, because AMC’s balance sheet is not strong enough to continue absorbing losses. As of late September 2022, AMC recorded ‘only’ $684 million of cash and cash equivalents on the balance sheet, as compared to total financial debt of $10.2 billion (net debt equal to approximately $9.5 billion).

With that frame of reference, investors should also consider that financing options for the firm are limited, given that loss-making history of the firm paired with frozen capital markets. And even if AMC would be able to finance through equity underwriting, shareholders would face significant dilution, referencing a market capitalization of about $2.8 billion.

2023 Could Deliver Upside

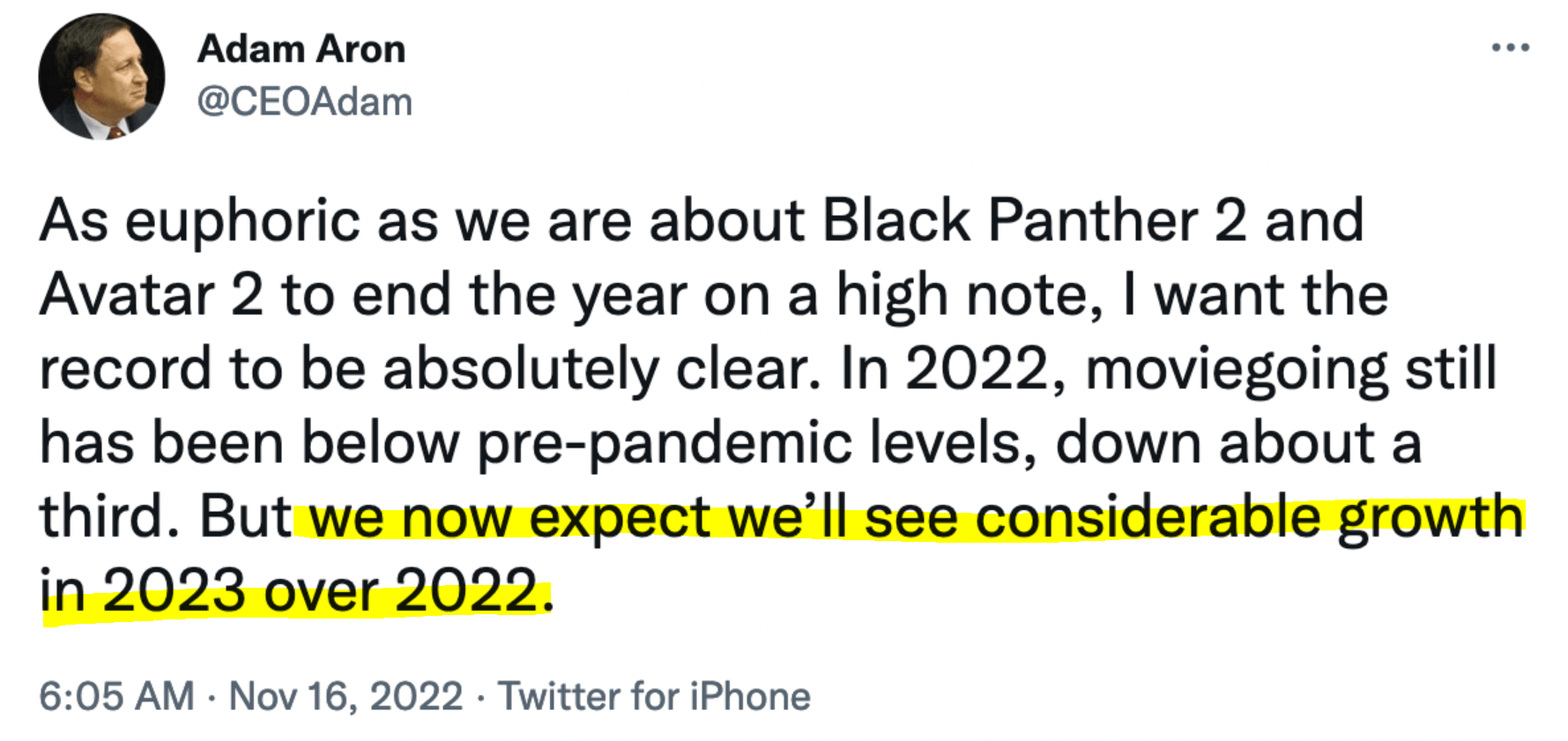

AMC’s hope for a turnaround is firmly anchored on an improving 2023. The company’s CEO has already voiced confidence going into the new year, on the backdrop of a strong movie release pipeline.

Twitter

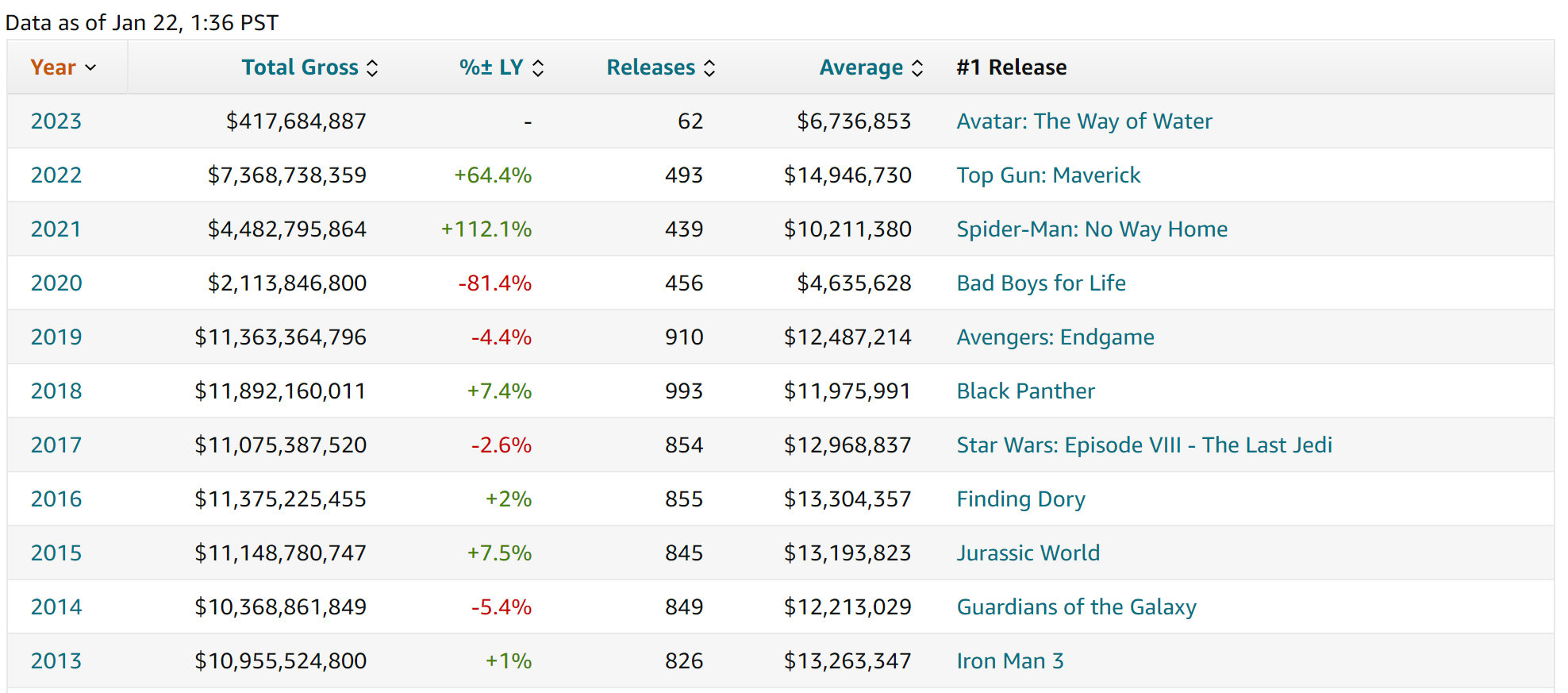

Reflecting on CEO Aron’s statement, it is true that ‘moviegoing’ is still about one third below pre-pandemic levels. In fact, cumulative global box-office spending in 2022 was about $7.4 billion, as compared to $11.4 billion in 2019 (38% difference). However, with $2.1 billion in 2020, $4.5 billion in 2021, and $7.4 billion in 2022, the trend is clearly pointing upwards.

IMDB IMDB

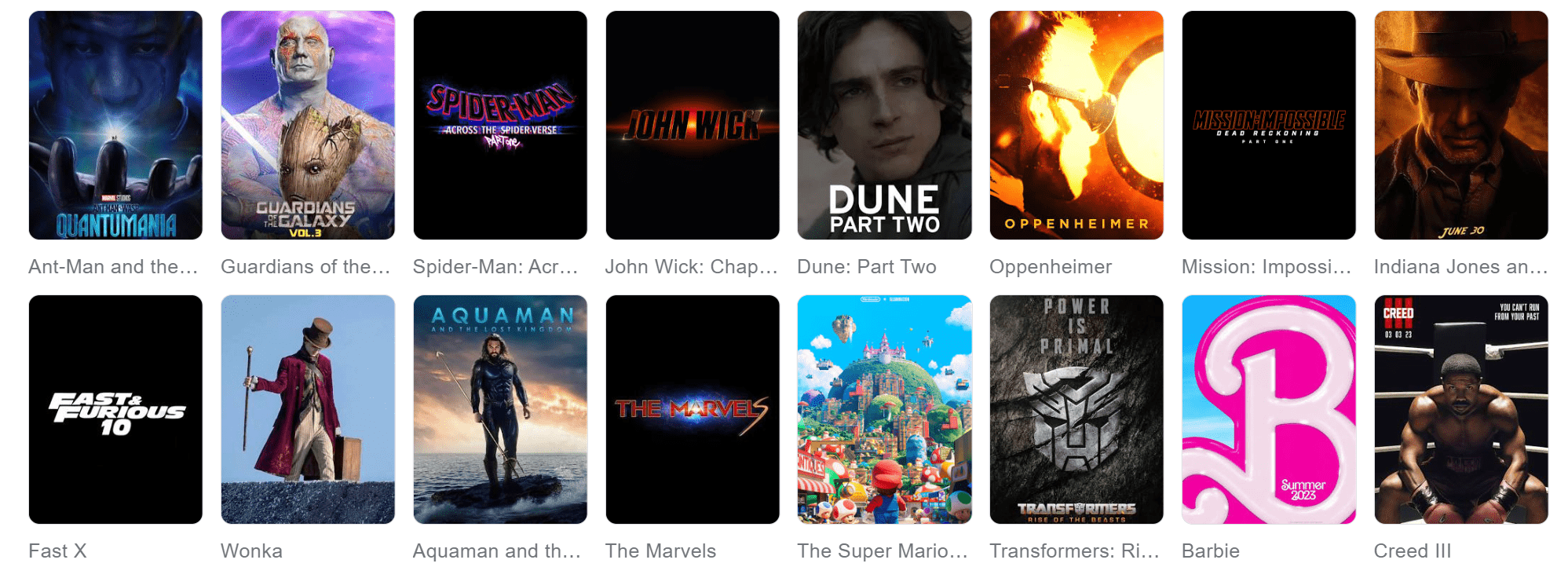

Investors should also consider that 2023 offers an exceptionally strong movie blockbuster pipeline. Among the key releases are:

- Ant-Man and The Wasp: Quantumania (2022)

- Creed III (2023)

- Scream VI (2023)

- Indiana Jones and the Dial of Destiny (2023)

- Dune: Part Two (2023)

- The Hunger Games: The Ballad of Songbirds & Snakes (2023)

- Dungeons & Dragons: Honor Among Thieves (2023)

- John Wick: Chapter 4 (2023)

- Guardians of the Galaxy Vol. 3 (2023)

- Fast X (2023)

- Spider-Man: Across the Spider-Verse (2023)

- Transformers: Rise of the Beasts (2023)

- Mission: Impossible – Dead Reckoning, Part One (2023)

Thus, in my opinion, it is not totally unreasonable that in 2023, box office sales will climb back to pre-pandemic levels, to more than $11 billion.

Google Search

Residual Earnings Model

Valuing AMC is most certainly difficult, given the financial risk considerations and the still weak market for movie theater spending. But assuming AMC would turn around the ship, here is how I would value AMC stock.

To estimate a company’s fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after a capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

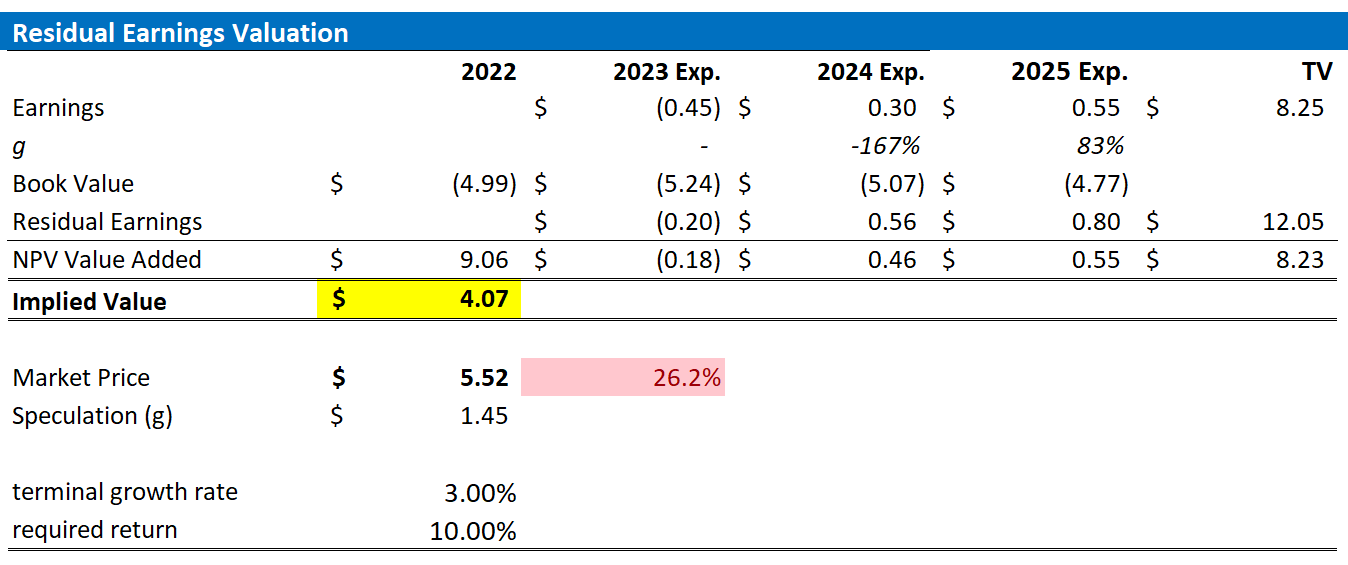

With regard to my AMC stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor AMC’s cost of equity at 10%.

- For the terminal growth rate after 2025, I apply a proud 3%, which is approximately double the estimated long-term nominal GDP growth (to reflect a strong growth tailwind until at least 2030).

Given these assumptions, I calculate a base-case target price for AMC of about $4.07/share.

Author’s Assumptions and Calculations

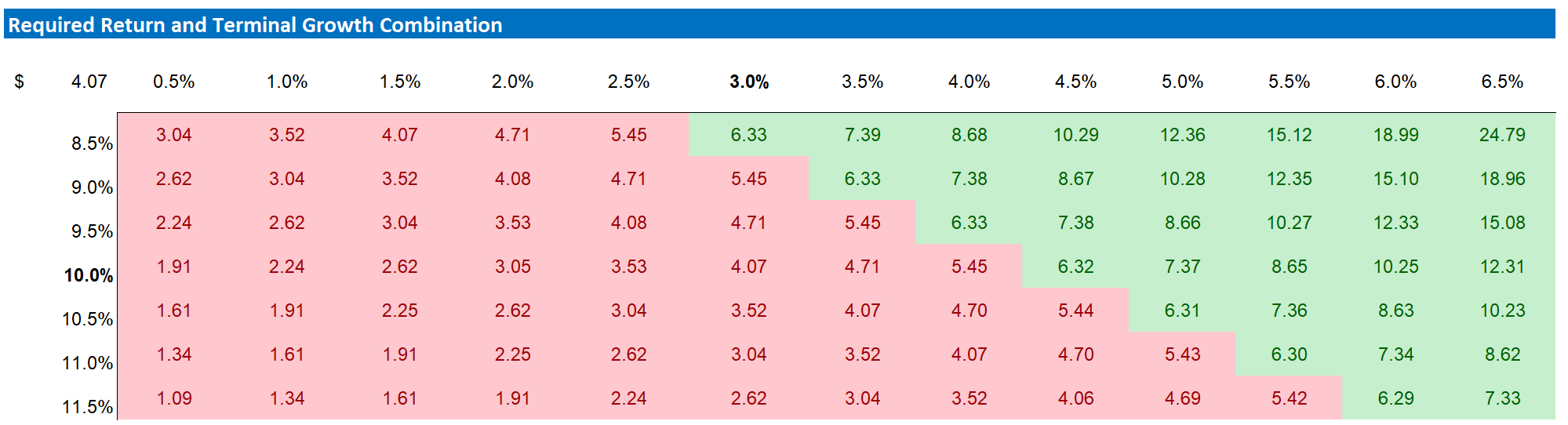

So, AMC is not undervalued. However, my model shows that AMC’s fair implied share price is very sensitive to variations in discount and terminal growth rate. To test various assumptions of AMC’s cost of equity and terminal growth rate, I have constructed a sensitivity table.

Author’s Assumptions and Calculations

Conclusion

AMC has been struggling financially and has generated a loss from continuing operations of $820 million for the trailing twelve months. This is concerning, because AMC does not have a strong enough balance sheet to continue absorbing such enormous losses, given a net debt position of approximately $9.5 billion. I argue, however, that it is too early to write off any value for AMC, as 2023 might offer some upside on the backdrop of a strong movie release pipeline.

Be the first to comment