David Silverman

Introduction

It’s time to talk about one of my all-time favorite dividend growth stocks: Raytheon Technologies (NYSE:RTX). A lot has happened since I wrote my most recent article in October 2022, when I expanded my position by 8%. The company has reported fantastic fourth-quarter earnings, the (related) war in Ukraine is still ongoing, budget talks in Washington have taken an unexpected turn, and so much more. In this article, I will walk you through these things as we assess where Raytheon might be five years from now. This includes assessing the current risk/reward for investors looking to initiate a position or add to an existing one.

In other words, we’ll look for catalysts and everything investors should consider before buying RTX.

So, without further ado, let’s dive straight in!

Two Big Reasons To Buy Raytheon Stock

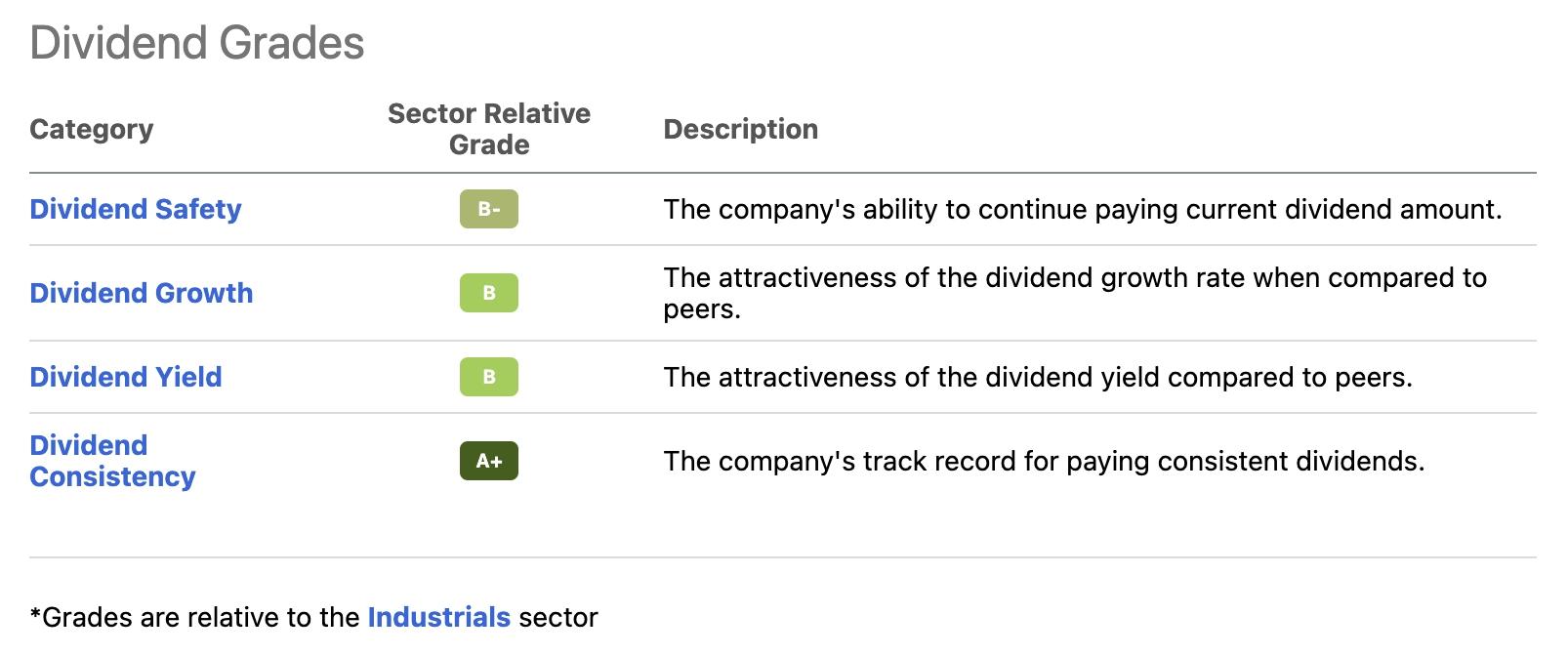

While opinions, investment goals, and preferences vary, I think I have a good understanding of the reasons why people buy Raytheon stock. The most obvious answer is its dividend, as the stock has a 2.2% yield, consistent dividend growth, and stellar dividend safety. Moreover, while the average dividend growth of the past three years is just 5.3%, we’re likely moving close to 10% again after 2023 due to accelerating free cash flow. This will also fuel RTX’s ability to buy back shares.

Seeking Alpha

However, reason one does not really narrow it down as it is somewhat obvious. Hence, reason two is what makes Raytheon special: its position in the aerospace & defense industry.

I currently have 24% aerospace & defense exposure in my dividend portfolio. It consists of the following companies:

Owning four defense stocks in a 21-stock portfolio is a lot, let alone giving these stocks 24% exposure. Hence, I made sure that all of them had specific characteristics.

Here’s the very short version of what went on in my mind when I made this decision:

- Lockheed Martin is highly dependent on the F-35 and the backbone of NATO defense hardware.

- Northrop Grumman is ultra high-tech, focused on supplying key technologies in all major defense projects. It is also the home of the next strategic bomber (B-21 Raider).

- L3Harris Technologies is a fast-evolving supplier without major defense programs. It is a first-tier supplier of all major contractors and expanding into new areas like hypersonics through the (expected) acquisition of Rocketdyne Aerojet (AJRD).

And then there’s Raytheon. The company is a major supplier as well, as it produces the F-135 engine for the F-35 in its Pratt & Whitney segment, it produces an almost countless number of commercial and military supplies in its Collins segment, and it is a producer of hypersonic applications, everything related to missiles, and space hardware.

However, the company also has a lot of commercial exposure. The companies I just listed have close to zero commercial exposure. As commercial aviation is a fast-growing industry, I wanted exposure in that area as well.

In 2021, Raytheon had roughly 48% government exposure. I don’t have the exact numbers for 2022 yet, but I assume that this breakdown will remain somewhere close to 50%. In 2021, commercial demand was weak. Now, commercial demand is rebounding. However, as defense demand is rising as well, I think that number will remain close to 50%.

| $ in millions | 2021 | 2020 | 2019* |

| Sales to the US Government | $31,177 | $25,962 | $9,094 |

| % of total sales | 48% | 46% | 20% |

*= pre-merger

I believe that the mix between high commercial exposure and a decent dividend is what attracts a lot of investors – especially after Boeing (BA) ran into trouble years ago, which resulted in Boeing stopping shareholder distributions.

With that said, let’s talk about Raytheon’s business improvements.

4Q22: Raytheon Is Firing On All Cylinders

The past two post-merger years were a bit unusual. Commercial demand suffered from the pandemic, which meant lower orders and a highly uncertain outlook. Defense demand did not suffer from that. However, defense segments were prone to supply issues, which included labor and material shortages, making it hard for high-tech companies like RTX to turn backlog into finished products.

As I own multiple defense stocks, I cannot tell you how many downgrades related to these issues I’ve seen since 2020.

Now, things are looking up again, as confirmed by 4Q22 earnings.

As reported by Seeking Alpha, Raytheon generated the following results:

- Q4 Non-GAAP EPS of $1.27 beats by $0.02.

- Revenue of $18.09B (+6.2% Y/Y) misses by $70M.

Both Commercial & Defense Segments Are Thriving

The company, which mentioned challenges like its move out of Russia (sanctions), record inflation, and supply chain/labor constraints, reported $86 billion in new bookings in 2022, resulting in a 12% higher backlog and a book-to-bill ratio of 1.28. Raytheon is now sitting on a backlog value of $175 billion.

This 1.28 number means that the company’s orders are coming in much faster than they can turn backlog into sales. It’s indicative of higher future growth. If the book-to-bill ratio were way below 1.0 consistently, it would mean the opposite.

Before we discuss the details behind the company’s progress, let’s quickly break down the performance per segment.

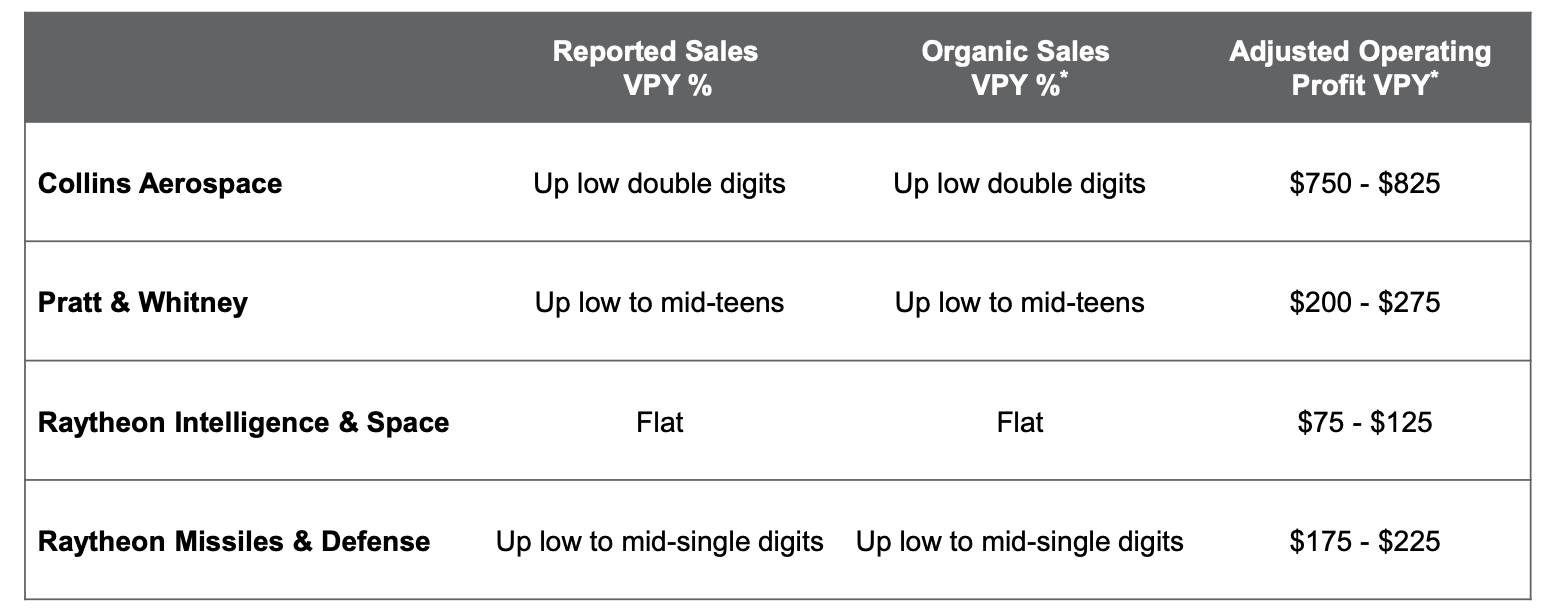

Collins reported 16% higher organic sales. Commercial aftermarket sales were up 21%. Commercial OE was up 20%. Defense revenue was up 5%. This segment benefited from higher commercial aftermarket demand and lower R&D expenses, which were partially offset by higher SG&A expenses. Operating margins improved by 360 basis points to 13.1%.

Like Collins, P&W also benefited from higher commercial aftermarket demand and more shop visits (maintenance). Organic sales improved by 11%. Commercial OE sales were up 37%. Commercial aftermarket sales were up 11%. Defense sales declined by 2%. Operating margins improved by 250 basis points to 5.4%, as higher demand more than offset growth in SG&A and R&D spending.

- Raytheon Intelligence & Space (“RIS”)

This defense segment saw a 5% decline in organic revenue. Adjusted profit fell 31% due to global training and services divestitures. Moreover, an unfavorable mix and lower net program efficiencies reduced the operating margin by 250 basis points to 7.8%.

The 4Q book-to-bill ratio was 0.92. On a full-year basis, that number was 0.96.

- Raytheon Missiles & Defense (“RMD”)

This segment was doing better than RIS. Organic sales improved by 7% thanks to higher volume in Naval Power, including SPY-6 (a radar system), Strategic Missile Defense, NGI development, and Advanced Technology Programs. In this case, NGI stands for Next Generation Interceptor. This is a program to intercept missiles together with its peer Northrop Grumman (NOC).

Unfortunately, an unfavorable mix more than offset higher volumes when it comes to margins. Operating margins were down 240 basis points to 9.2% (10.2% adjusted).

However, the book-to-bill ratio rose to 1.48 in the fourth quarter. On a full-year basis, that number is 1.37. This includes billions for Patriot missiles, NASAM air defense, and more.

The RMD segment alone has a $34 billion backlog value.

These backlog numbers are truly stunning and much higher than anyone could have guessed before the Ukraine war.

“Raytheon” Is Back – Literally

A big part of the fourth-quarter earnings call was about structural changes. For the first time since the 2020 merger, Raytheon Technologies is making a major change in its business. It’s bringing back the “Raytheon” name.

In 2020, Raytheon Technologies became the result of the merger between United Technologies’ aerospace businesses (Collins and P&W) and Raytheon. That merger was genius as it combined some of the most advanced aerospace businesses in the world.

After generating $1.4 billion in merger synergies so far, RTX is taking things to the next level by going from four to three business segments. All of them will now have an iconic name.

- Collins Aerospace

- Pratt & Whitney

- Raytheon (a merger between RIS & RMD)

Essentially, the plan is to allow for much more efficient business processes. This is based on customer feedback, demand trends, and the company’s assessment of collaboration possibilities.

[…] this realignment will allow us to better leverage our scale so we can optimize our footprint, improve resource allocation and reduce costs for both RTX and our customers.

The change is expected to finish in the second half of this year. Raytheon does not yet have a synergy target. I am sure management will shed more light on that in the months ahead.

With all of this in mind, it’s time to dive into the outlook.

Outlook: Defense & Commercial Strength

If there’s one thing that has become mainstream in 2022, it’s the return of defense demand. The war in Ukraine triggered a wake-up moment for NATO partners (including the United States). When adding China’s hostility toward Taiwan and the high risks of escalations in the Middle East and Africa, we get an environment that calls for higher defense spending.

Raytheon is well-positioned when it comes to satisfying advanced defense needs. In Ukraine, for example, Raytheon is a key supplier of defense weapons like Stingers, Javelins, and Excaliburs. Now, the focus is on bigger equipment like NASAM and Patriot air defense systems.

To give you a few numbers, in the US, the Defense Authorization Bill and the Omnibus Appropriations Bill provide the defense industry with an $858 billion budget. That’s a 10% increase from 2022.

Overseas, the EU is targeting a EUR 70 billion increase in defense spending over the next three years. Japan is increasing its defense budget by 26% this year.

Given our current backlog and this continued strength in demand, we remain extremely focused on execution, and I see four key actions that will position us to be successful on this front.

To deal with its high backlog through 2023 and 2024, Raytheon is making new strategic investments in North Caroline, Texas, and India, to produce key parts and applications. Unfortunately, labor availability remains an issue.

While the company did not comment on it, I expect 2023 to be a great year for labor availability as a result of general economic weakness. Defense companies with steady and predictable income will be major winners in a situation where other high-tech companies reduce procurement volumes to deal with slower orders.

What’s also interesting is that Raytheon commented on the expected recovery in its supply chain. The company is now seeing a recovery in the second half of this year, three years after the start of the pandemic.

[…] we need to continue restoring health within our supply chain. We’ve actively maintained a physical presence at close to 400 supplier sites. We continue to qualify additional suppliers on key programs. We secured sources of supply for critical commodities. While we are broadly beginning to see our supply chain improve, it is not yet at the levels we need, we are assuming a recovery as we move into the back half of the year.

When it comes to inflation, the company sees $2 billion in labor and material headwinds in 2023. Raytheon expects to tackle these costs using pricing and cost-saving initiatives.

Moving over to commercial demand, the one thing on everyone’s mind is COVID, which did a number on the steady uptrend in global passengers before the 2020 lockdowns.

In light of fading COVID cases and the reopening of the Chinese economy, Raytheon sees normalization in demand. At the end of 2023, it expects a full normalization in global demand, which is better than I expected (I was looking for 2024).

[…] we expect global air traffic to fully recover to 2019 levels as we exit 2023 with continued strength in the U.S. and Europe. This is pretty consistent from what we’re all hearing from the airlines. And like everyone else, we’re keeping a close eye on China, which historically has represented about 14% of global air traffic.

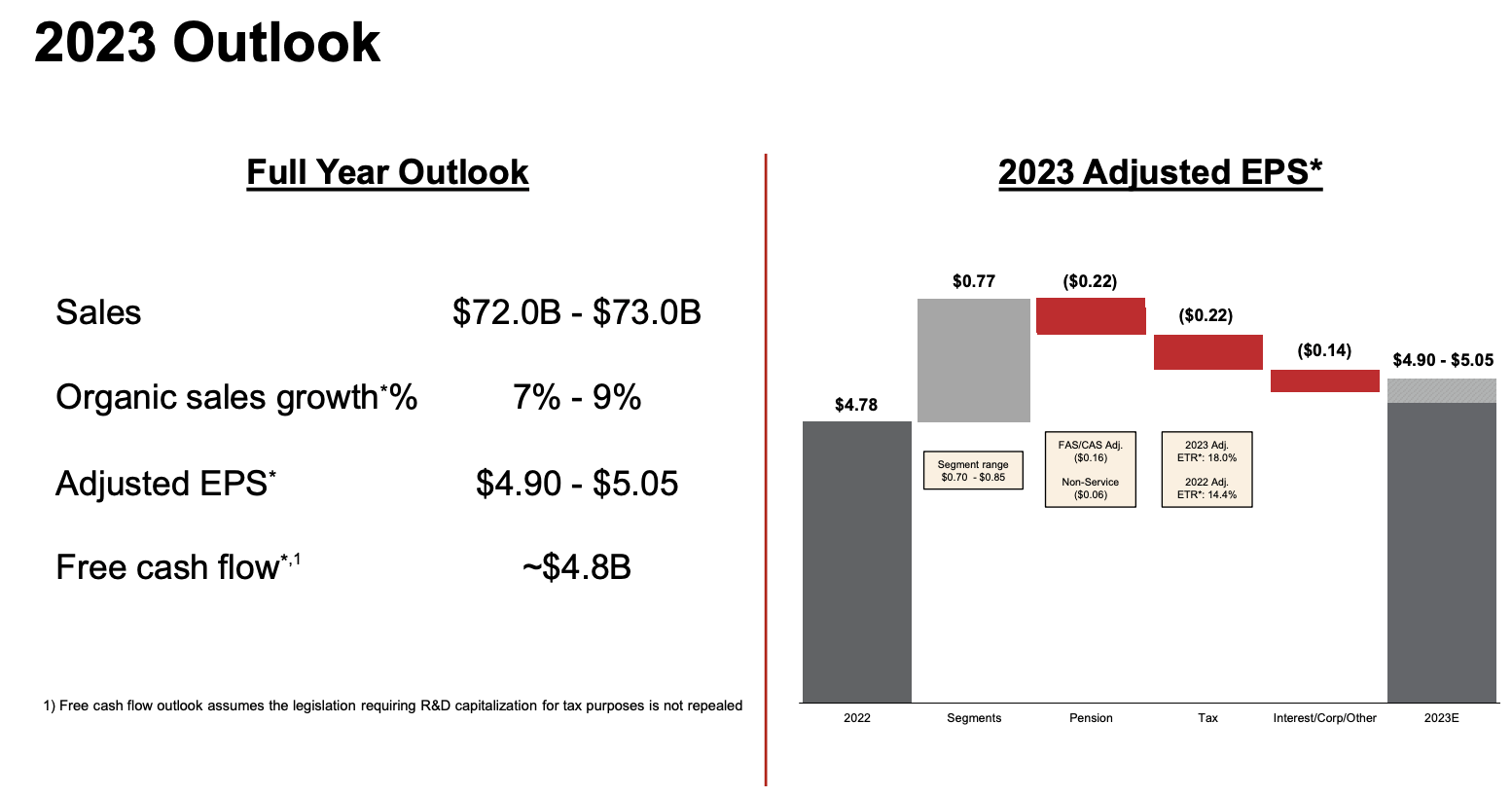

Hence, on a full-year basis, Raytheon is looking to grow organic sales by at least 7%. Adjusted EPS is expected to be at least 4.9%, which would imply a 3% to 6% growth rate.

Raytheon Technologies

RTX is also expecting to do $4.8 billion in free cash flow. This includes changed legislation requiring R&D expense capitalization for tax purposes. Under this law, RTX will have a $1.4 billion cash payment.

[…] we hope that people in Washington will understand that they’re making a very, very bad tactical decision here and not allowing us to deduct R&D, but it is the reality that we face today.

Moreover, pensions are expected to be a significant headwind.

[…] with respect to pension, although markets have improved since we spoke in October, pension will still be a substantial year-over-year headwind. Based on actual 2022 asset returns and where discount rates ended the year, that headwind will be about $0.22.

The overview below shows the segment breakdown, which displays increasing sales in all segments but RIS, with outperforming growth in Collins Aerospace. This outperformance is the result of subdued military exposure and high growth in commercial demand.

Raytheon Technologies

The good news is that the years after 2023 are expected to be even better.

After 2023, Growth Is Back In Full Force

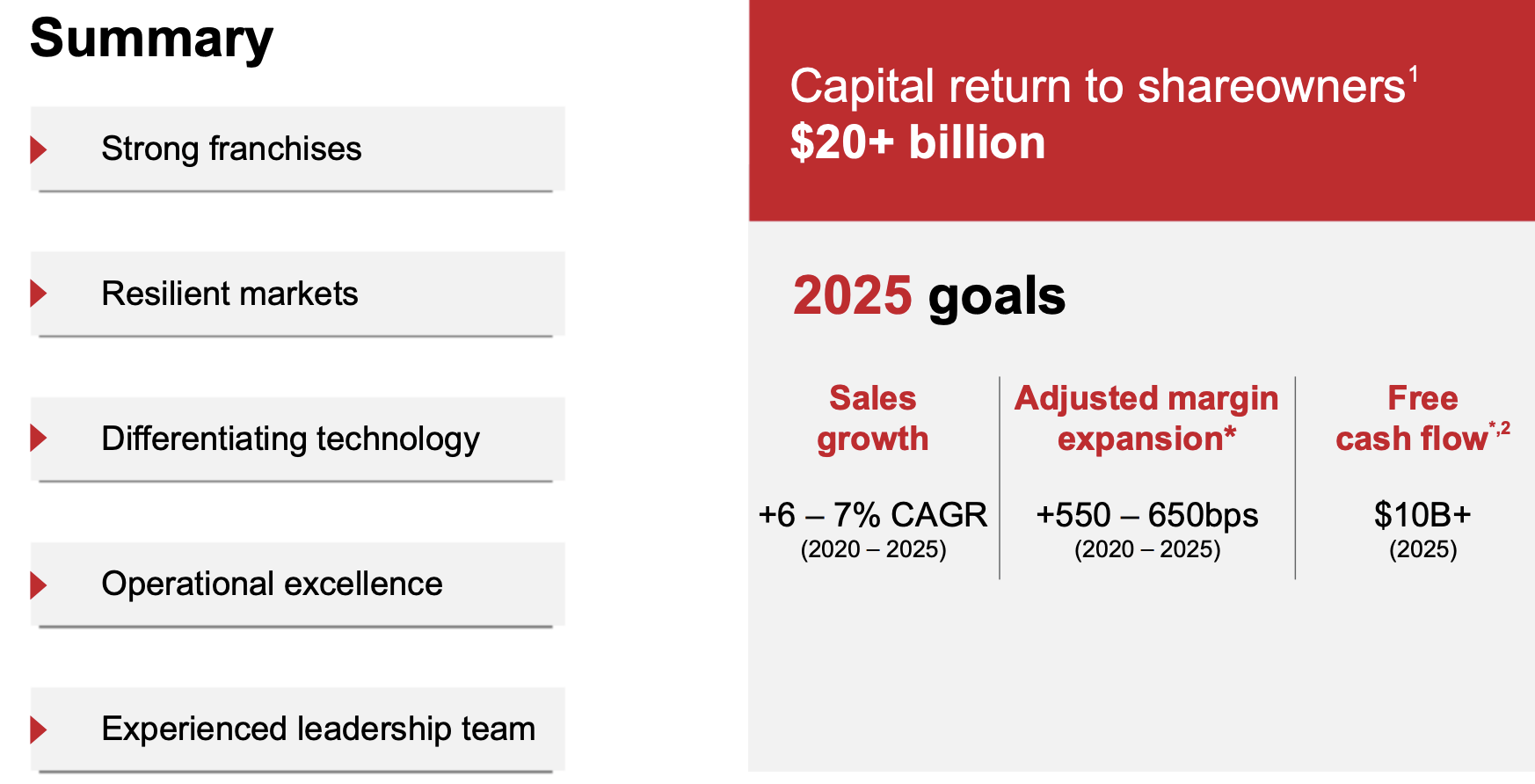

In 2021, Raytheon presented its 2025 targets. The company saw a path to $10 billion in free cash flow in 2025 based on 6% to 7% annual organic sales growth between 2020 and 2025.

Raytheon Technologies

Now, the FCF target is being lowered to $9 billion. CEO Greg Hayes does not see a path to $10 billion anymore, due to a $1 billion drag. $800 million of this is actual net R&D deferral. On top of that, there are slightly higher interest payments.

With that said, it’s not a surprise that $10 billion in 2025 FCF won’t be achieved. Analysts have adjusted their target to $8.7 billion as the overview below shows. This was due to an earlier announcement of R&D-related tax changes.

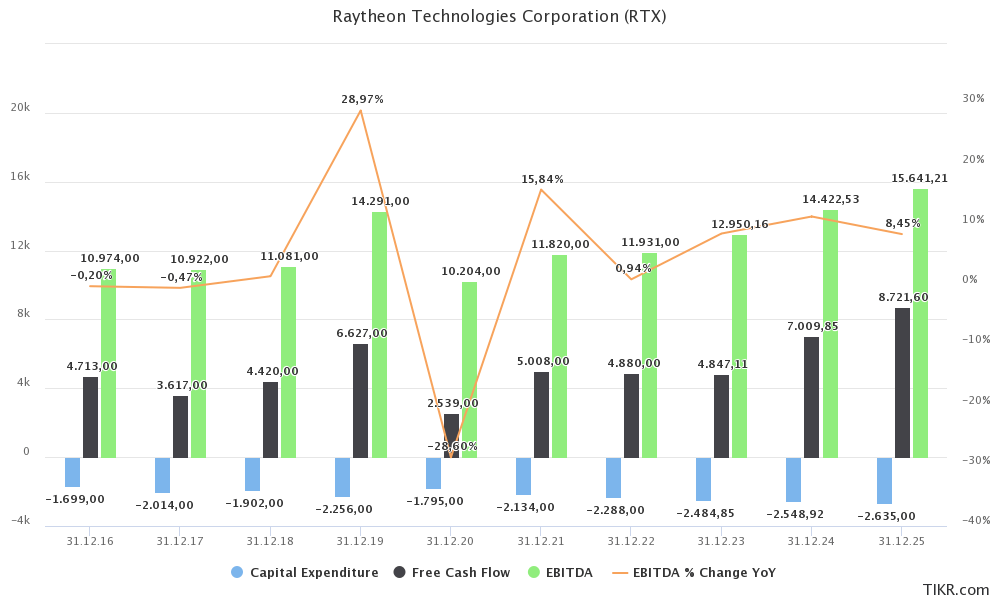

However, what we see below is that after 2023, RTX’s financials are about to take off. 2023 will likely see unchanged FCF and slightly higher CapEx. In 2024, the company will be able to benefit from its massive backlog, normalized supply chains, and much lower inflationary pressures.

TIKR.com

What is really important to mention here is that unforeseen issues like high inflation and supply chain bottlenecks in 2021 and 2022 will be offset by much higher defense demand and a strong commercial rebound.

[…] as I step back and look at the totality of RTX and where we projected to be and where we’re aiming to go and with that backlog, we feel confident that we can get there. We can get the sales growth, get the earnings growth and Greg already hit on the cash flow pieces there. So some things have changed since we’ve talked in 2021. We’re certainly dealing with a lot more inflation, but we’ve also got the situation in Ukraine that has given R&D some tailwinds.

Unless unforeseen things happen, like a new pandemic or a massive global recession, we are likely to see the return of pre-pandemic conditions for aerospace companies.

- Consistently rising demand.

- Improving pricing power.

- No major supply chain issues.

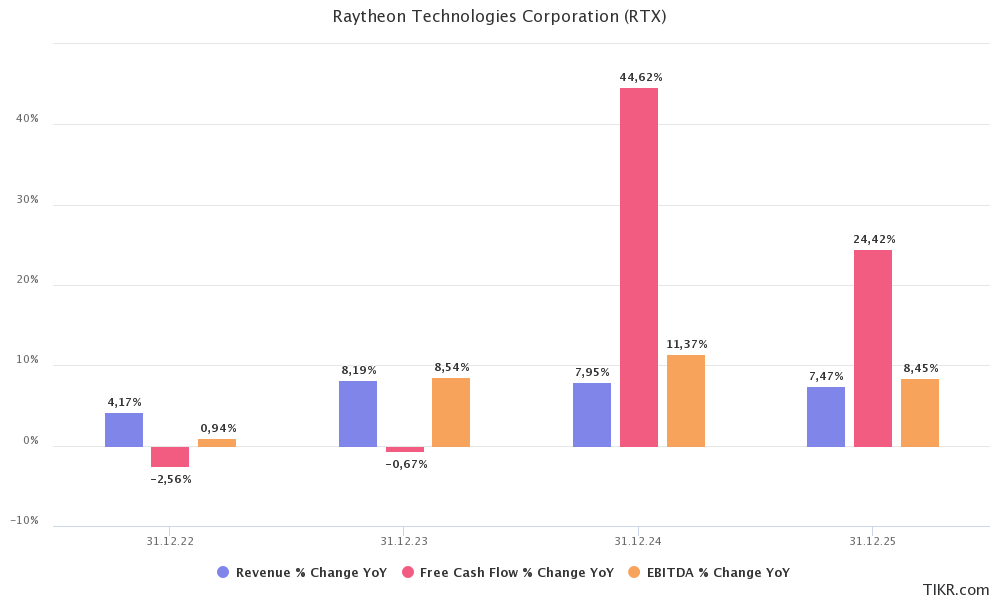

In the next few years, EBITDA growth rates could likely average 9%, with sales growth coming in roughly 200 basis points lower. The difference is caused by improving margins.

TIKR.com

This makes RTX shares attractive.

How High Can Raytheon Shares Go?

Where Will Raytheon Be In Five Years?

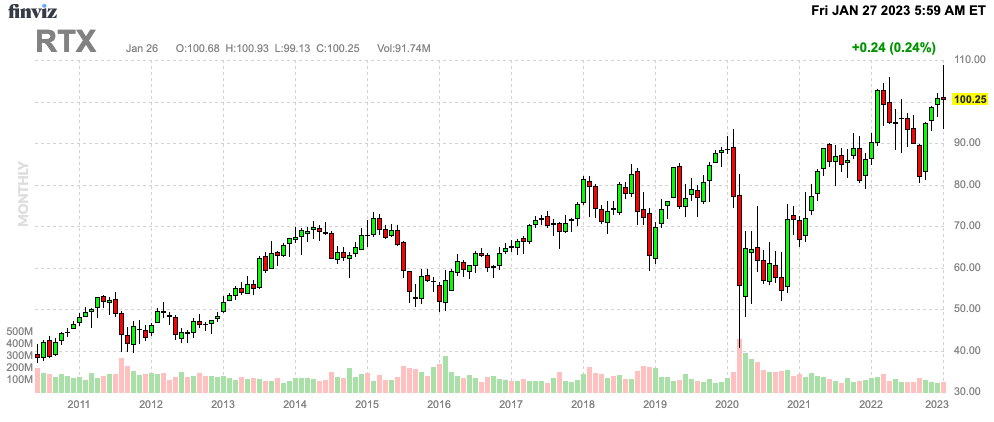

Raytheon shares are up 11% over the past 12 months. With a market cap of $147.4 billion, it continues to be the largest defense company in the world.

FINVIZ

While 2022 wasn’t bad, I am convinced that the best years are ahead. The past two years were somewhat of a mess, as supply chain and related issues kept Raytheon from showing its full potential.

That is now about to change.

RTX shares are trading at 12.6x 2024E EBITDA of $14.4 billion. This is based on its $180.8 billion enterprise value, consisting of its $147.4 billion market cap, $27.0 billion in net debt, $4.8 billion in pension liabilities, and $1.6 billion in minority interest.

Conservatively speaking, I believe that RTX should be trading close to 12-13x EBITDA, which would imply that RTX is now fairly valued. The current RTX share price target is $106, which implies roughly 6% upside potential. I think that’s fair.

The same goes for its implied FCF yield of 4.7% ($7.0 billion in 2024E FCF).

In 2027 (five years from now), the company should be able to do close to $18.5 billion in EBITDA (unadjusted for inflation).

So, conservatively speaking, I think we’re looking at capital gains of 7-8% per year over the next five years. When adding dividends, I think investors are looking at a very high likelihood of 10% total returns per year until at least 2027.

Risks To Consider

Let’s say my five-year prediction is spot on. Even if that were the case, returns would not be evenly distributed. I believe that the first half of 2023 might be tricky. The stock is fairly valued on a short-term basis and facing new headwinds.

While the 2023 defense budget is 10% higher, new policy risks have emerged.

Defense One

(Some) Republicans, led by Speaker Kevin McCarthy, call for defense spending cuts. McCarthy wants defense spending back at 2022 levels, implying a $75 billion cut from current levels.

After having spent way too much time watching political shows, I believe that he is mainly looking for cuts that are not related to hardware and next-gen technologies. He’s combatting “woke” spending, which is mainly used for political reasons.

While I do not disagree with more targeted funding, there are now high risks that defense spending growth could be subdued in the years ahead. I believe that he won’t achieve any cuts, but it’s a risk to keep in mind. After all, the defense supply chain is in desperate need of funding.

Despite a stabilization of late, the effects of the pandemic are still being felt three years later: high inflation, supply-chain disruptions, and worker shortages, executives say.

“American families and businesses continue to struggle under very real and serious economic conditions like inflation, workforce difficulties, and ongoing supply chain disruptions,” wrote Fanning, a former Army secretary during the Obama administration. “Uncertainty emanating from Washington would exacerbate these already serious challenges.” – Defense One

We also need to keep in mind that the US is dealing with another debt ceiling debate. For now, it looks like the Treasury has liquidity until August/September. However, the risks of a shutdown and new funding issues are rising.

I expect this to be resolved, but it won’t do defense stocks any favor, which is why some had a terrible start to the year.

Other risks are prolonged supply chain issues, which I do not expect. I think a normalization at the end of 2023 is a safe call.

The Bottom Line

Raytheon remains in a terrific place to generate consistently rising value for its shareholders on a long-term basis. Fourth-quarter earnings confirmed that commercial demand is back, while defense segments continue to benefit from accelerating orders. While supply chain issues are still a headwind, we can expect a healthy mix of fading supply chains, accelerating commercial demand, improving defense revenue growth, and high free cash flow in the quarters ahead.

Especially after 2023, we will see the first significant boost in EBITDA and free cash flow growth since the merger, allowing the company to do close to $9 billion in free cash flow in 2025.

Moreover, given industry dynamics, I expect this to continue, implying that RTX could deliver double-digit annual total returns for many years.

My advice remains simple. Buy RTX on dips, which is what I have been doing since 2020. Not only do I own RTX in my dividend portfolio, but it’s also a core holding of portfolios that I advise.

There really isn’t a company that provides a better mix of defense and commercial exposure with a decent dividend yield and accelerating long-term growth.

(Dis)agree? Let me know in the comments!

Be the first to comment