Richard Drury

Written by Nick Ackerman, co-produced by Stanford Chemist.

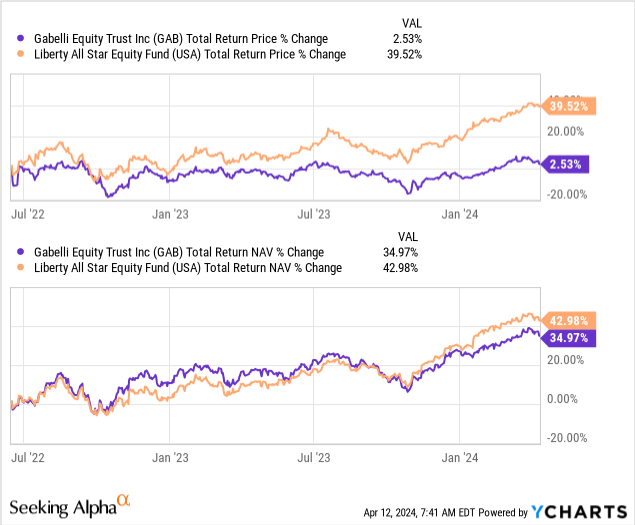

We had previously touched on Gabelli Equity Trust (NYSE:GAB) last year; at that time, we also discussed Liberty All-Star Equity (USA). We were recapping how our previous swap idea trade we highlighted worked out successfully. Since then, GAB has not done too much in terms of total returns during that period.

GAB Performance Since Prior Update (Seeking Alpha)

This was largely due to the fund’s premium coming down even further. In that update, GAB was still sporting around a 7% premium, and today, it’s now at a very narrow discount. For that reason, it’s looking like a much better opportunity today.

Ultimately, though, I’d really want to see a larger discount before getting too excited and adding this position to my portfolio. That is despite the fact that this fund actually trades at a premium pretty regularly. Discounts aren’t unheard of for this fund either, but it can require a bit of patience as it is fairly rare.

GAB Basics

- 1-Year Z-score: -1.20

- Discount: 0.56%

- Distribution Yield: 11.28%

- Expense Ratio: 1.62%

- Leverage: 21.16%

- Managed Assets: $2.05 billion

- Structure: Perpetual

GAB’s investment objective is “long-term growth of capital, with income as a secondary objective.” Generally, we see that the investment objective for closed-end funds is often income or high income. In this case, GAB is looking for long-term growth of capital, which it technically hasn’t been successful with. There has been very limited appreciation, and returns have only come from the distributions.

The fund is leveraged, which will add greater volatility and risks to investing in this fund. One of the moving parts here is also the costs of the borrowings, which most closed-end funds saw skyrocket in the higher rate environment.

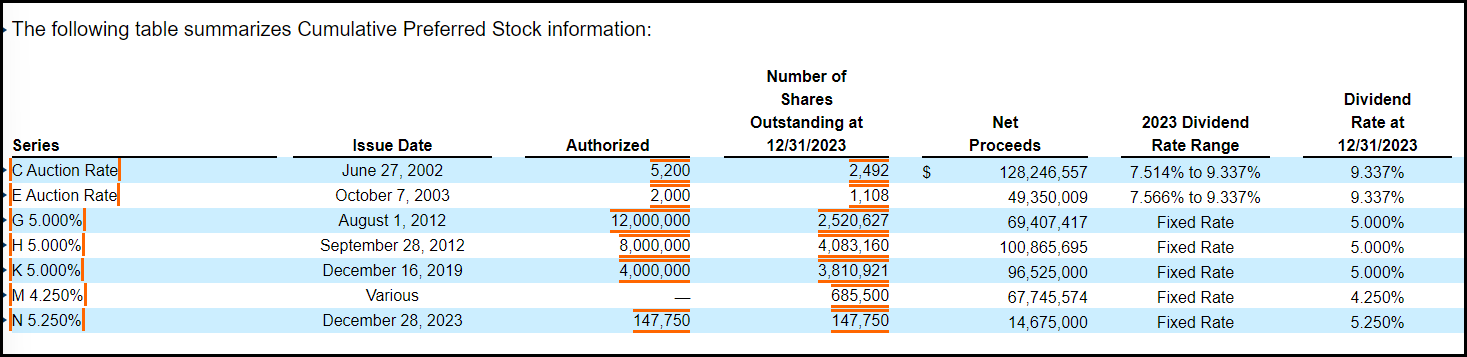

For GAB, they are fortunately much more protected thanks to a large portion of their borrowings being fixed-rate preferred. Only a minor sleeve of their borrowings is based on the auction rate preferred. That helped with some predictability of the fund with fewer moving parts, relatively speaking.

For those auction rates preferred, we can see just how much the costs exploded in their last annual report, with rates now up to over 9%. These were paying rates at 0.123% and 0.14% at the end of 2021.

GAB Leverage Info (Gabelli)

Performance – A Better Looking Candidate Today

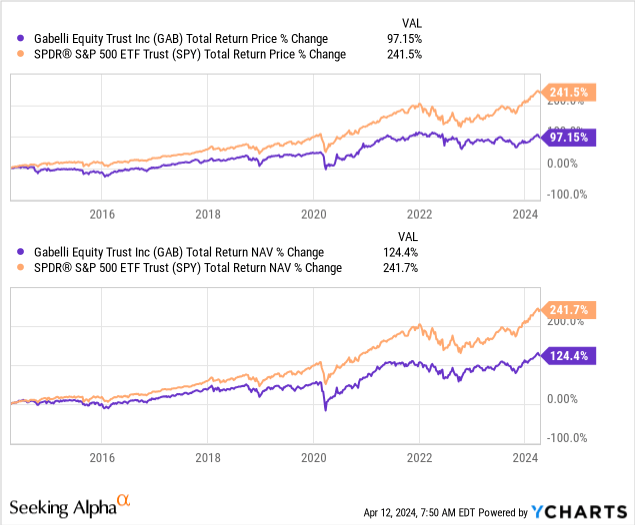

As an equity fund, it has historically been able to deliver some solid annualized performance. We experienced the Covid crash and 2022’s bear market, but those were relatively short-lived market sell-offs where most of the last decade now has been seeing equities rally massively. The fund comes with a more value-oriented approach, and that has been getting stomped by investments that have more of a growth focus.

In particular, that includes the S&P 500 Index. That broader market index has become increasingly heavy in tech weighting as mega-cap tech names drive most of the index results. The weightings in names such as Microsoft (MSFT) and Apple (AAPL) continue to push higher. If we compare GAB to something like (SPY), the results are pretty much to be anticipated. The higher expense ratio for GAB as an actively managed fund is also going to play a role, too.

Ycharts

That’s why it can be important to get these straightforward, plain vanilla equity funds at a ‘good deal.’

Our original swap idea from GAB to the USA was when GAB was sporting a nearly 29% premium. At that time, the USA was trading at a richer valuation, too, at a 5% premium. This, once again, really highlights the opportunity there is when making swaps between similar funds. During this time, the USA was also able to outperform on a total NAV return basis, so that certainty helped, too.

Ycharts

Fortunately, investors that remained in GAB got to collect their distributions—which is probably the main thing they are most worried about anyway. Plus, returns weren’t negative for the fund during this period, just flat essentially.

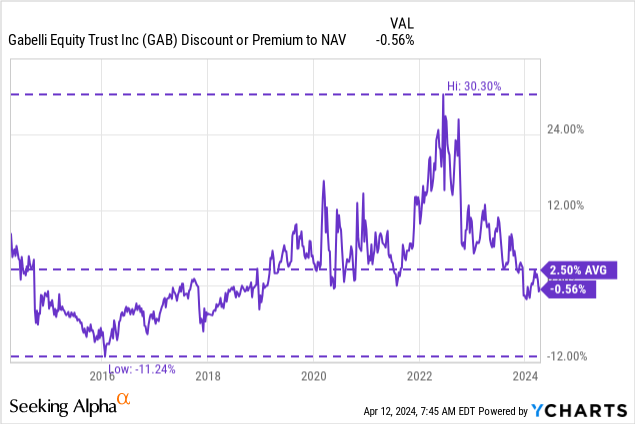

Today, at a slight discount, GAB looks like a much more interesting candidate. This is because the fund’s current valuation relative to its historical level is finally back in line.

Ycharts

The last several years were more of an outlier, which really brought up the fund’s average premium during this period. The last three years show an average premium of ~9%, and the last five years show an average premium of ~8%.

I would feel more comfortable picking up a position if we hit the 5% to 10% discount area. That hasn’t happened since around 2018, so it isn’t a frequent occurrence—at least not in the last decade—but it has happened.

Managed Minimum 10% Distribution

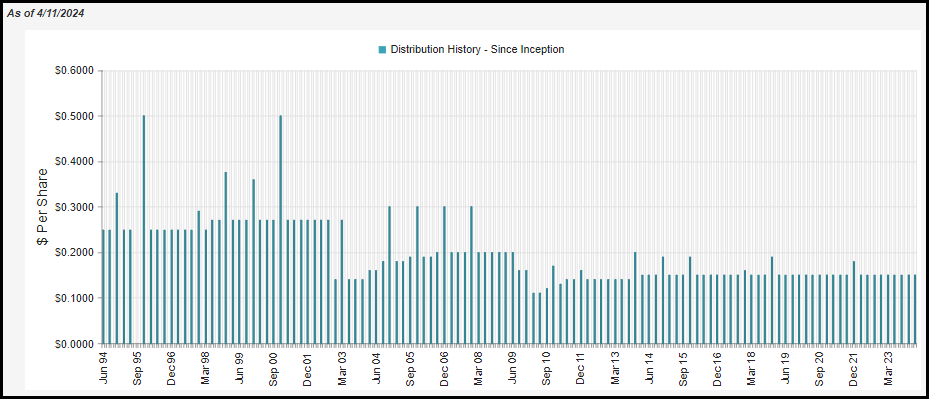

For those who are already holding GAB, the area that most investors are probably concerned about is the distribution. This fund has a minimum 10% managed distribution policy. This is a bit different from other managed distributions in that they don’t have a reset period. Often, funds will pay a certain rate based on NAV, and that gets adjusted monthly, quarterly, semi-annually or annually.

An example of that is USA, which adjusted its payout each quarter based on what 2.5% of the fund’s NAV is on the “Friday prior to each quarterly declaration date.” In effect, that’s how they achieve their 10% distribution policy.

For GAB, instead, since it is merely a minimum, anytime the fund has a “shortfall” below the 10% policy, it will pay out a year-end special. In this way, there is a more level distribution for what can be years at a time, as we saw in the last stretch since the GFC.

GAB Distribution History (CEFConnect)

If the regular quarterly distribution paid hits this minimum level, then no year-end special will be issued unless for IRS tax purposes. As a regulated investment company, if they realize too much in gains or income, they have to pay out extra or pay an excise tax.

Based on the fund’s current NAV distribution rate of 11.21%, the chances of a year-end in 2024 diminish with each passing month.

Like any equity fund, especially one that tries to pay out a double-digit rate every year, it will rely massively on capital gains from the underlying portfolio to cover the payout. However, some income is generated here thanks to the fund’s more value-oriented portfolio, which generally pays more generous dividends.

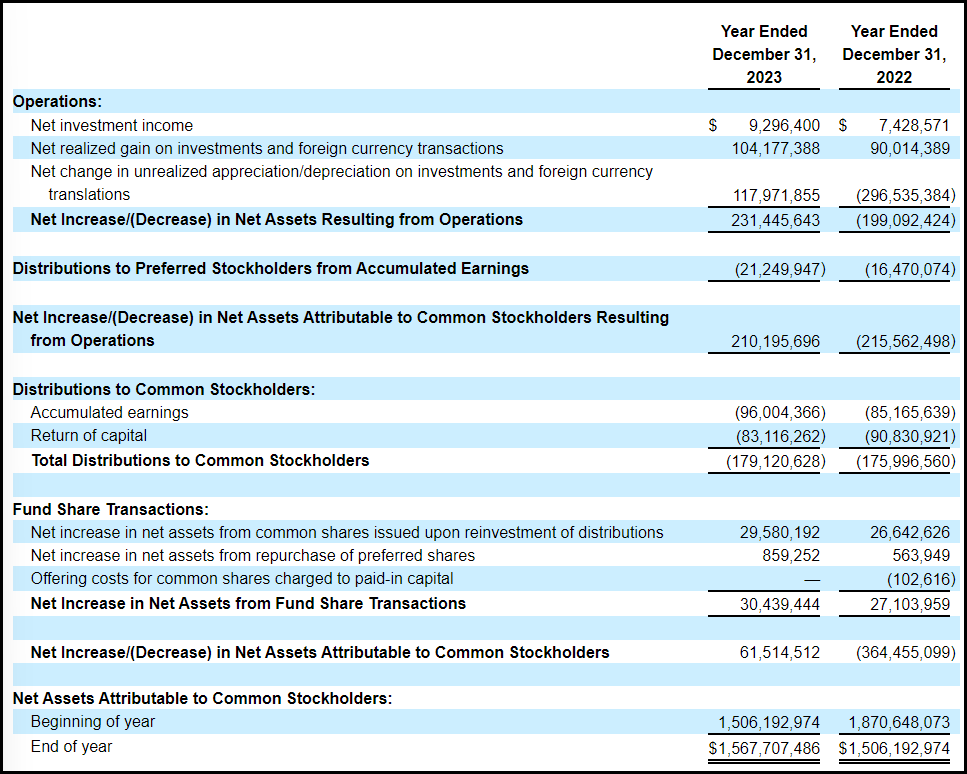

GAB Annual Report (Gabelli)

One area that could help the fund with its high premium in the last few years was the fact that it could issue new shares. This was through the reinvestment or at-the-market offering from the fund. Since the shares were being issued at a premium to the NAV, that meant it was accretive for the fund’s NAV.

Unfortunately, this fund is quite large, and there actually wasn’t too much accretion in the last couple of years. It was so small for 2023 that it just showed $0.00, and 2022 was good for a $0.01 bump. In 2021, the fund had a rights offering, and that saw a negative impact of $0.10, offsetting the even small gains they had seen from issuing shares accretively.

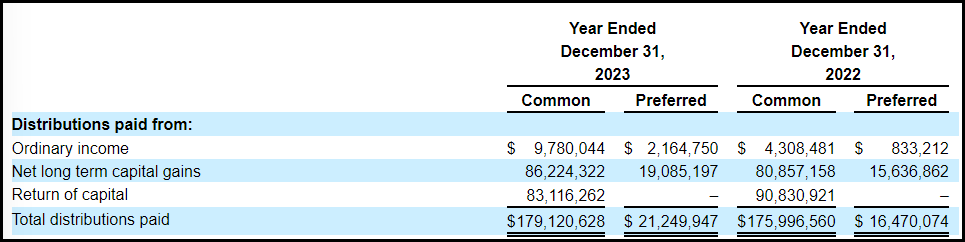

For tax purposes, a large portion of the distribution should generally be classified as long-term capital gains. However, in both 2023 and 2022, we saw a significant allocation characterized as return of capital as well.

GAB Distribution Tax Character (Gabelli)

In 2023, the NAV rose, so this wouldn’t have been considered destructive ROC, but in 2022, it would have been as the NAV declined.

GAB’s Portfolio

The portfolio turnover rate for this fund is generally pretty low. Last year, it was listed at 17.1%, and that was actually the highest in the last five years. Their latest fact sheet lists the turnover at just 3%. So, generally, the managers here aren’t making massive changes to the portfolio.

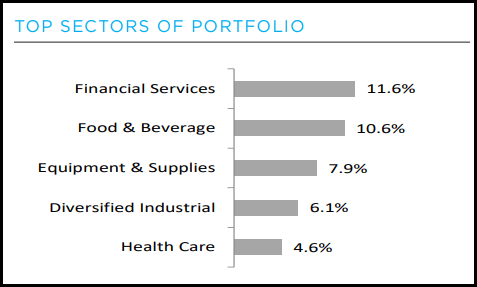

This fund has the largest exposure to sectors in the financial services sector and the “food & beverage” industry.

GAB Top Sectors (Gabelli)

The weightings here were as of December 31, 2023. That might be quite a lengthy period of time, but it actually had similar weightings to what we saw when we showed the breakdown in our June 2022 article on the fund. That really reflects the fairly low amount of changes that we would expect to see with such a low turnover.

These allocations are also a reflection of the fund’s more value-oriented approach relative to something like the S&P 500 Index, which has now seen its tech weighting climb to just over 30% of the index.

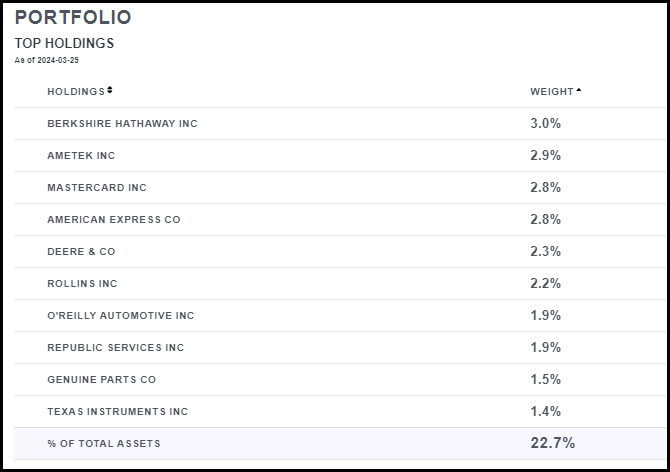

In looking at the top ten holdings, we also get even more confirmation of how much different this fund is invested relative to the broader market. We don’t see any of the magnificent 7 names as top ten holdings for this fund.

GAB Top Ten Holdings (Gabelli)

Conclusion

GAB has come down from its massive premium a couple of years ago, and that trend continued over the last ~6 months since we last touched on the fund. As a plain equity fund, I think it’s even more important to be selective on what valuation you are picking shares up of this CEF. For me, we still aren’t at that level, but we are getting much closer, and the fund’s future prospects from here do seem a bit more promising. At the same time, investors holding this fund are probably more focused on that 10% minimum distribution policy, which was reaffirmed earlier this year.

Be the first to comment