Editor’s note: Seeking Alpha is proud to welcome CDI Research as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Trucks at an XPO Logistics distribution point in San Jose, California Sundry Photography

Industry commentary says that activity levels in the U.S. trucking industry are strong and healthy. In trucking, we believe XPO (NYSE:XPO) – a pure-play less than truckload (LTL) specialist – has great potential for 75% upside.

XPO is attractive, both from an industry trends and business model point of view. There are ample LTL industry tailwinds for growth, which XPO is well equipped to capitalize on with its capacity additions to gain market share. We expect the company’s strong sales momentum to continue as it returns to a golden age of industry outperformance.

Thesis Summary

There are five elements that make up our investment thesis on XPO:

- The U.S. LTL industry is structurally attractive.

- The U.S. LTL industry has a long growth runway.

- The spinoff leaves XPO with a better business.

- XPO’s capacity additions will lead to market share gains and margin expansion.

- Momentum is strong with a healthy demand outlook.

U.S. LTL industry is structurally attractive; the business requires more capex to scale up

LTL shipping operates under a hub and spoke model because the shipped goods tend to be heterogenous and destinations may also be distributed across an area. For an LTL operator, adding more regional terminals and coordinating efficient logistical flows are critical requirements for success. This requires more capital, which creates barriers to entry and scale, which is why the LTL market is more consolidated than the full truckload market:

LTL vs Full Truckload Market Comparison (Coyote Logistics, CDI Research)

The top 10 carriers in the LTL market make up 76% of revenue share, compared to only 5% for full truckload, proving a more consolidated industry structure.

Limited capacity addition supports prices

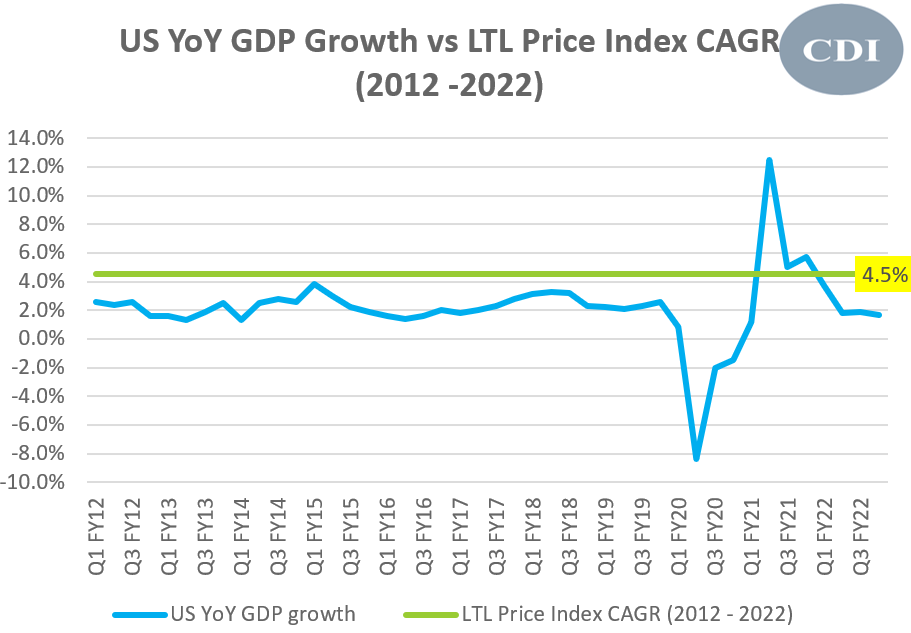

XPO’s CEO Mario Harik noted during a Q3 FY22 earnings call that the LTL industry today has less volume capacity than 10 years ago. This has supported healthy pricing growth in the market:

US GDP Growth vs LTL Price Index (Fred Economic Data, CDI Research)

The LTL industry’s price CAGR over the past 10 years has been 4.5%, outpacing nominal U.S. YoY GDP growth.

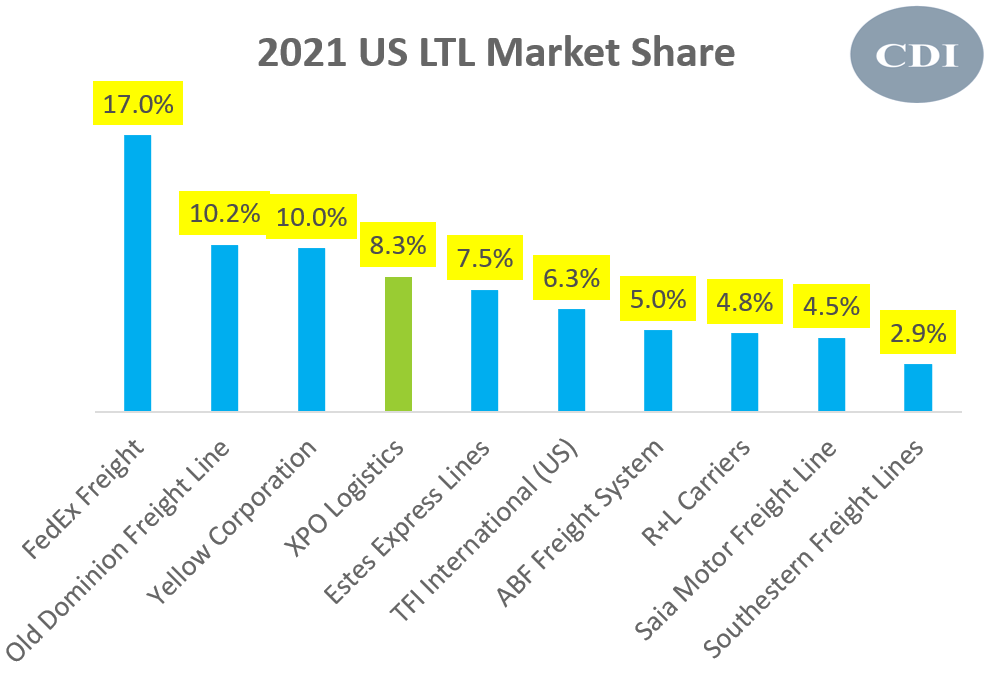

Larger LTL operators like XPO are positioned to gain share

In the $51 billion LTL business, XPO is the fourth largest player with 8.3% market share as of 2021:

2021 US LTL Market Share (Logistics Management, CDI Research)

The LTL industry has a long tail with more than 120,000 players. However, smaller long-tail players are becoming less competitive, to the benefit of market leaders as cost pressures place larger operators in a better position to find offsetting margin levers.

Operating leverage benefits offset rising driver costs

In a survey of 200 trucking companies conducted by Inbound Logistics, the highest number of respondents (85%) answered “Driver-related costs” when asked “What are your greatest challenges?”

According to IBISWorld, wages have grown as a share of revenue from 26% to over 29% over the 2018 – 2022 period. Moreover, this figure is expected to rise above 30% in 2023. Scale players are better positioned to mitigate these headwinds due to operating leverage benefits.

Insourcing trends give an edge to larger operators

Insourcing linehaul operations is capital intensive, providing large players an exclusive opportunity to execute on this margin lever.

Old Dominion

During a Q2 FY22 earnings call, Adam Satterfield, the CFO of Old Dominion Freight Line (ODFL) mentioned that they are moving towards fully insourced linehaul operations.

Yellow

COO Darrel Harris explained on Yellow’s (YELL) Q2 FY22 earnings call that they were integrating their linehaul network during the summer of 2022.

XPO

During the latest Q3 FY22 earnings call, XPO’s CEO Mario Harik noted plans for insourcing third-party line haul operations. Overall, insourcing of linehaul operations should improve the profitability of scale players and provide opportunity for market share gains via improved pricing, delivery speed and service quality.

U.S. LTL industry has a long growth runway

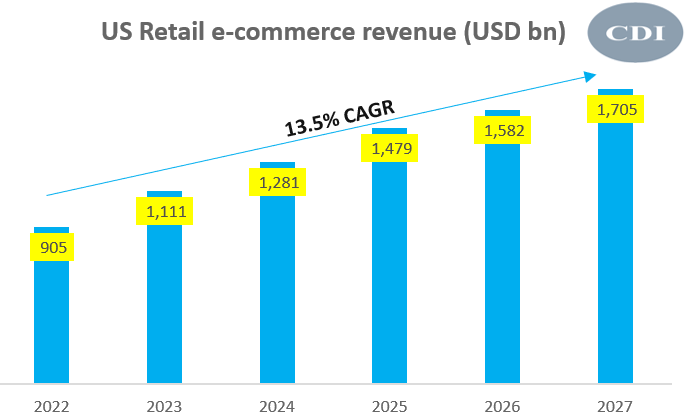

It’s clear that e-commerce is a key growth driver:

US Retail E-commerce Revenue (eMarketer, CDI Research)

Data from eMarketer suggests a 13.5% CAGR in e-commerce revenue growth, driven by COVID-led accelerated habituation of online purchases.

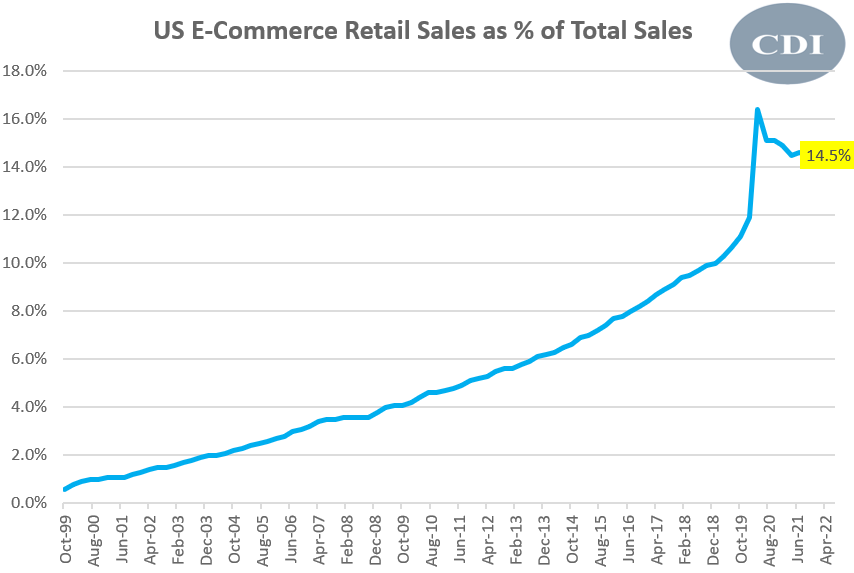

US E-Commerce Retail Sales as % of Total Sales (United States Census Bureau, CDI Research)

The mix of e-commerce retail sales in the U.S. has accelerated from 12% to 14.5% over the last two years. This is a structural post-COVID change. Acceleration in retail sales increases the need for supply chain resources such as warehouses, terminals, trucks and drivers to make more e-commerce deliveries happen at faster speeds and superior service levels. This increases the demand for LTL freight.

Importantly, much of this increased demand is getting captured by outsourcing as LTL operations are becoming more complex and specialized. This will benefit LTL specialists such as XPO.

Reshoring and near-shoring boosts LTL demand

Compared to pre-pandemic times, the number of CEOs highlighting plans to reshore or near-shore their supply chains is up 10x. Construction of new manufacturing facilities is up more than 116% since H1 2021 to H2 2022. These trends open up opportunities for LTL players in the supply chain.

Spinoff leaves XPO with a better business

In November 2022, XPO spun off its trucking brokerage business RXO (RXO), leaving mostly US LTL operations and European operations, which makes up ~33% of overall revenues. The company intends to divest away European operations as well in due course. The new XPO has a better business profile and is focusing more on the core LTL business.

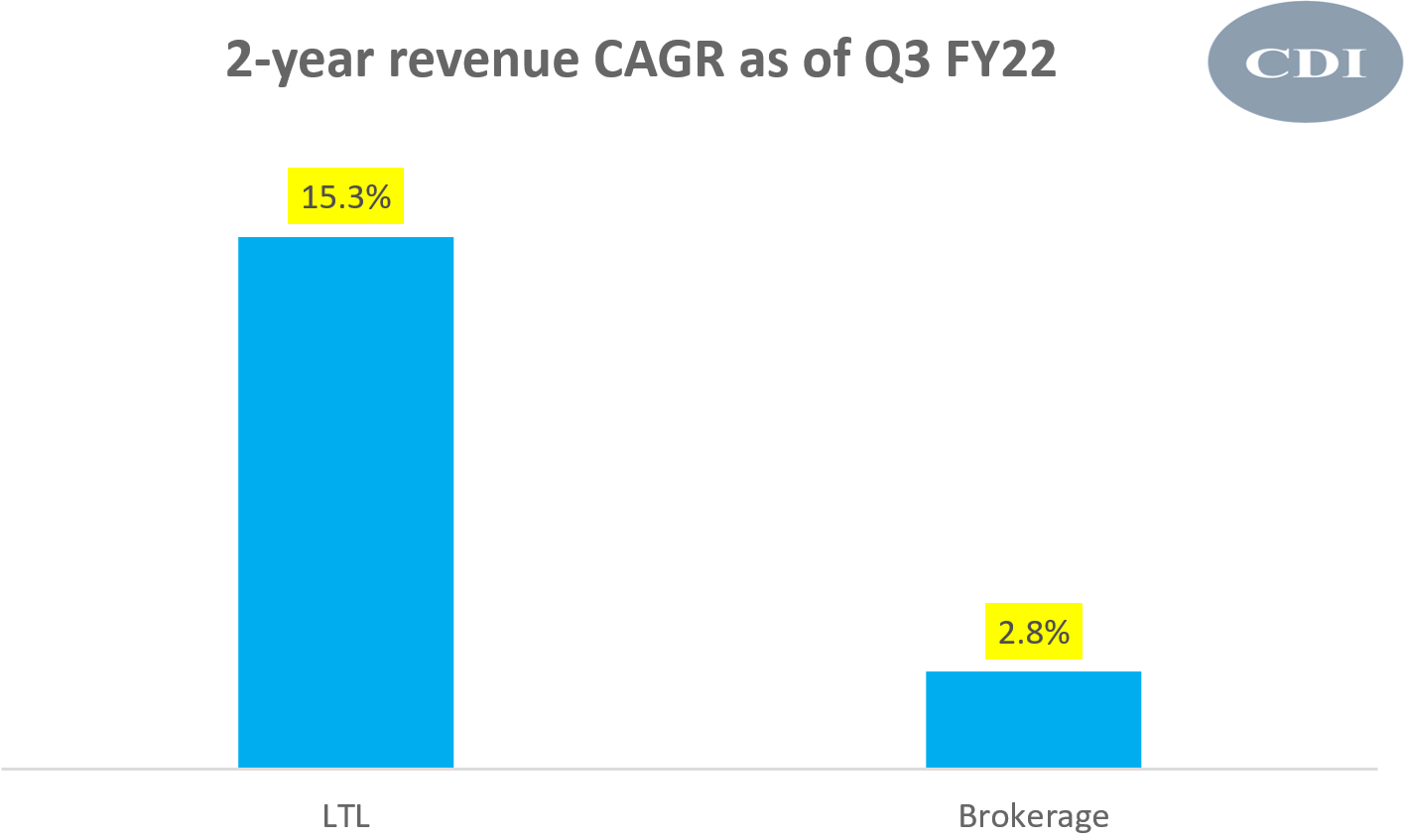

XPO’s LTL business has superior revenue growth

XPO’s LTL business has grown faster than the brokerage business on running two-year basis.

2-year revenue CAGR of LTL and Brokerage business (Company Filings, CDI Research)

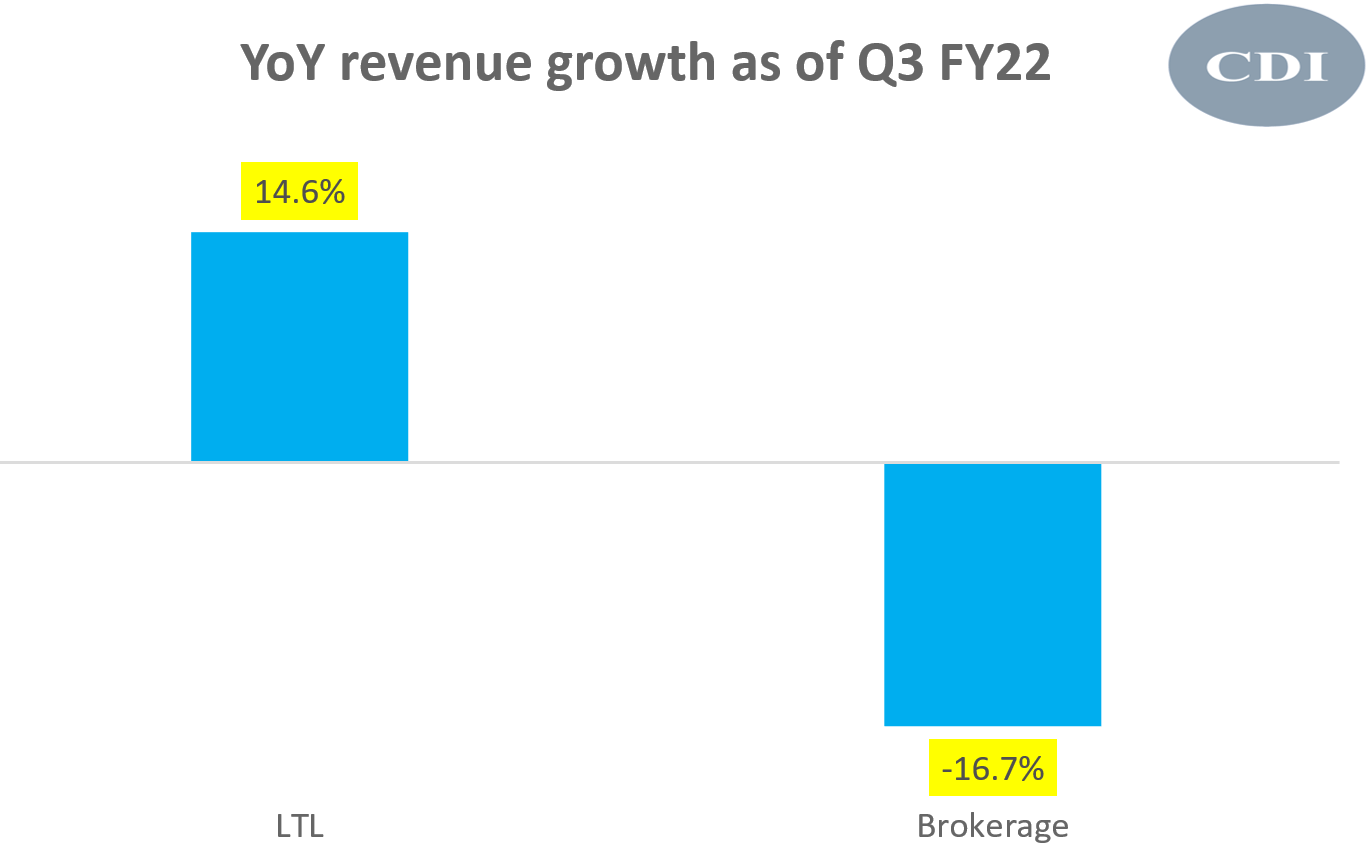

This gap in growth rate has accelerated in the rolling year:

2-year revenue CAGR of LTL and Brokerage business (Company Filings, CDI Research)

The brokerage business has had growth struggles over recent quarters due to a 30-40% fall in spot market trucking rates. Contract rates are also seeing signs of weakness, suggesting continued weakness ahead. On the other hand, there is resiliency in LTL rates.

Thus, XPO post-spinoff has a better piece of the growth pie.

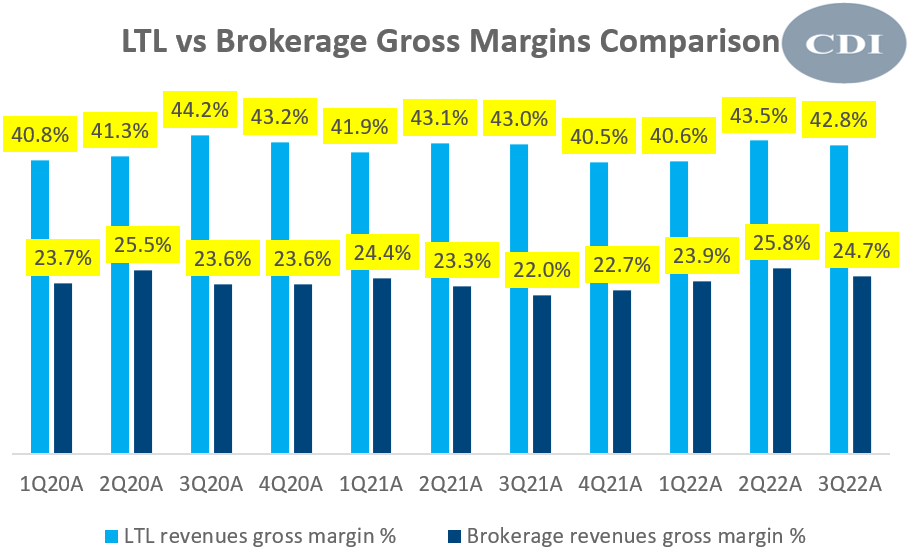

XPO’s LTL business has superior gross margins

LTL vs Brokerage Business Gross Margins (XPO, CDI Research)

The LTL business has much higher gross margins than that of the revenue business. Gross margins have been rather stable above the 40% range, indicating a quality business.

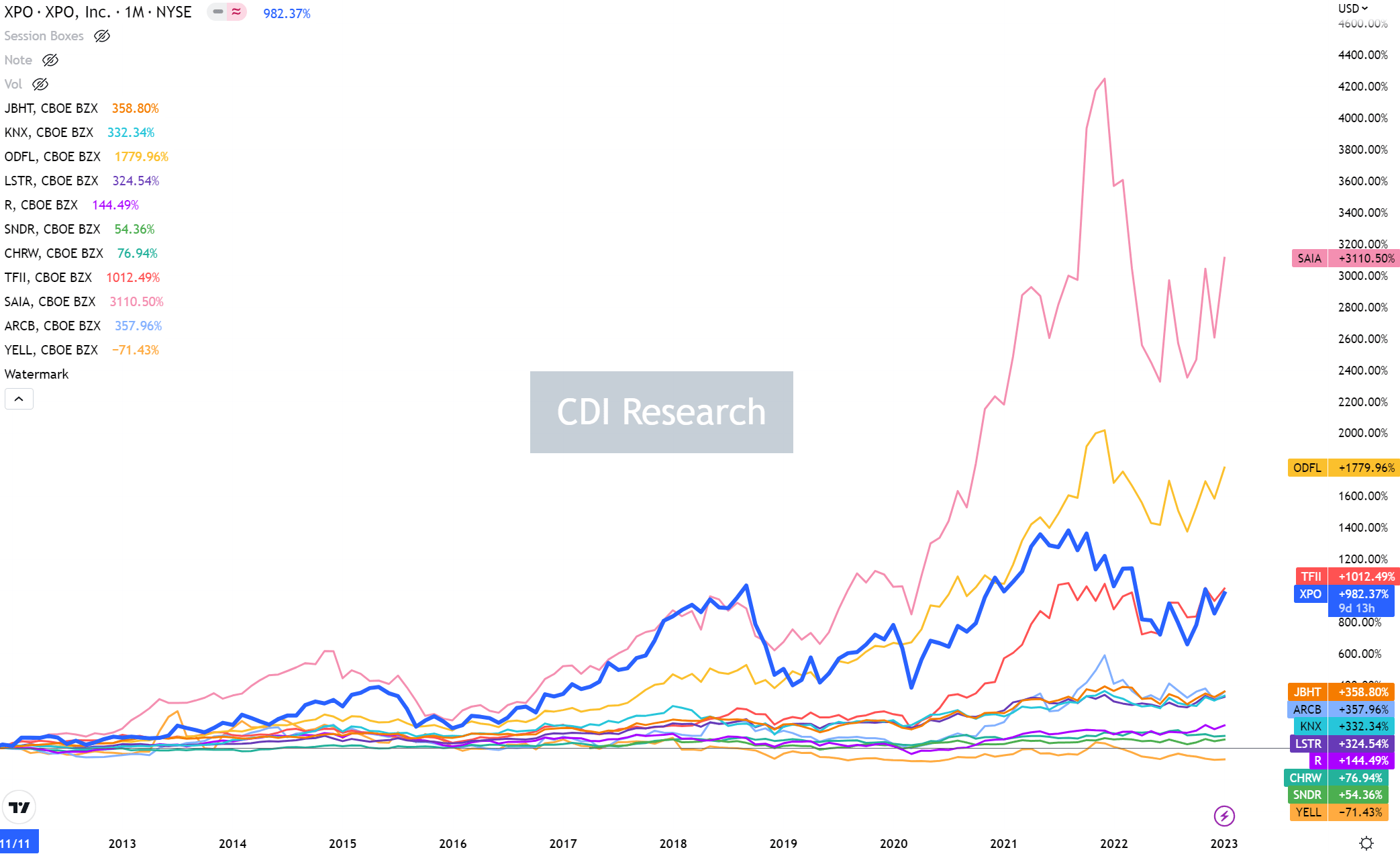

Mario Harik came in as chief information officer of XPO in November 2011, using a data-driven approach to revamp operations. We have confidence in his abilities and believe he is the right leader to optimize the pure-play LTL business; XPO has been one of the outperformers in the trucking industry since his joining month:

Trucking Stocks Relative Performance (TradingView, CDI Research)

XPO used to be the absolute outperformer till 2018. Since then, its non-LTL businesses have dragged back its performance due to both cyclical and structural headwinds driven by technology disintermediation and new entrants. We believe with the technology-oriented experience of Harik as the new CEO, XPO can unlock various efficiencies to make good data-driven decisions. With a leaner LTL-focused business, XPO has the right to win to regain the stock performance leadership position among its peers.

XPO’s capacity additions will lead to market share gains, margin expansion

The LTL industry capacity has reduced over the last 10 years. Considering this supply-constrained situation and the strong growth tailwinds ahead, management is investing in capacity additions to rapidly accumulate a growing share of the market. Harik says the primary reason for capacity additions is to “say yes” to customers more often. This is a sign that demand is the primary constraint in the LTL market, which is why adding capacity makes sense.

Trailer manufacturing leads to volume growth and agile service delivery

XPO has backward integration in manufacturing of truck trailers. In Q1 FY22, the company added a second production line to its trailer production and as of Q3 FY22, the company was on-track to add a third production line in Q4 FY22. This doubles trailer production in 2022 with 4700 new trailers. All trailers produced by XPO in 2022 is used by the company, indicating unsaturated demand fulfillment.

In 2023, management will add 50% more capacity, to produce at least 7,000 trailers annually. The risks of oversupply are low as there is a pent-up demand of more than 100,000 trailers, driven by alignment of trailer refresh cycles. Also, having its own trailers gives XPO greater agility to meet customer demands, improving its right-to-win.

Expansion of terminals and network doors will increase volumes

XPO is investing in network depth via the addition of more terminals and dock doors. It plans to expand door capacity by 6% by the end of 2023 and as of Q3 FY22, 41% of this expansion is complete. The investments have already helped boost the top-line of XPO. As Harik noted in the Q3 FY22 earnings call (linked above):

As an example, we opened up a terminal in Atlanta six months ago. And in the month of September, we’ve seen tonnage in the Atlanta market go up 38% on a year-on-year basis.

Insourcing of linehaul network will improve margins

Outsourced line haul costs make up 10-11% of revenues. Management has indicated that in-sourcing can result in a 30-40% cost reduction per mile. Based on this, we estimate a 300-600bps lever for potential margin improvement.

Fleet age reduction will lower maintenance costs

XPO is due for a reduction in average fleet age from 5.9 years to 5.0 years, resulting in a 20-25% reduction in maintenance costs realized fully by the end of 2024. Assuming this reduction in cost occurs in the direct operating expenses line and noting the Q3 FY22 direct operating costs figure of $363 million, we compute an implied 200-300bps overall improvement in margins realized over 2 years.

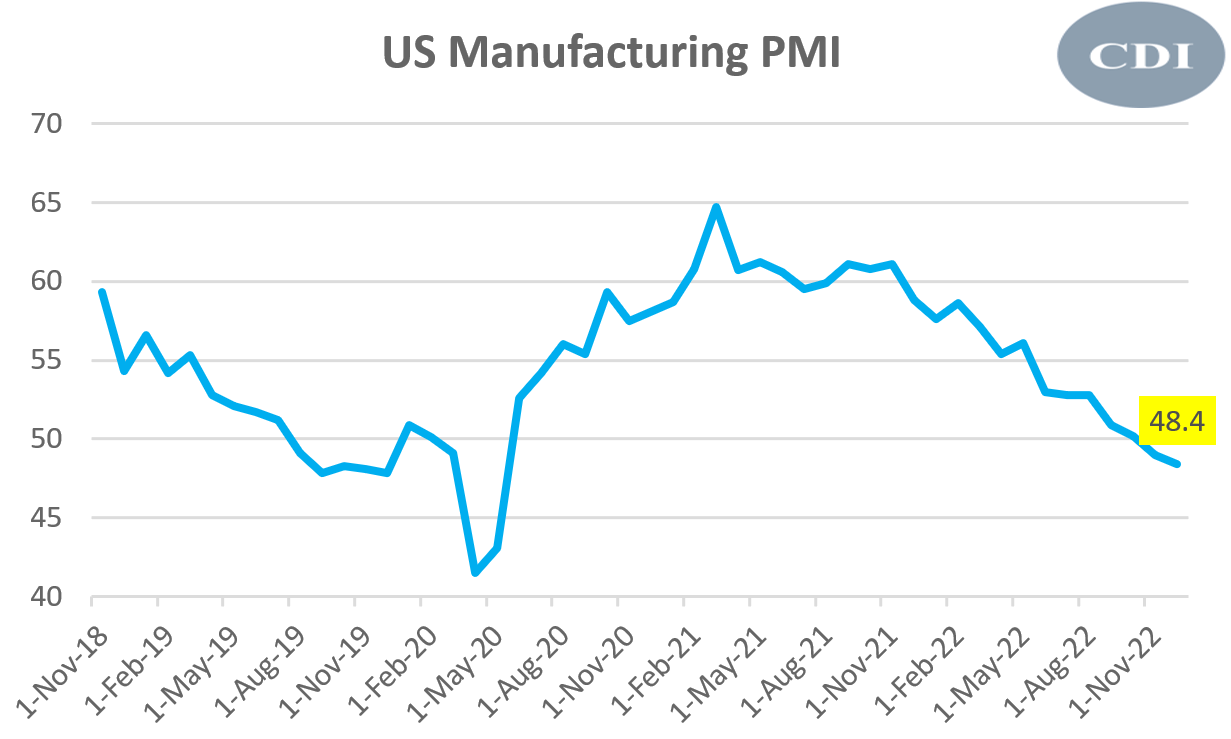

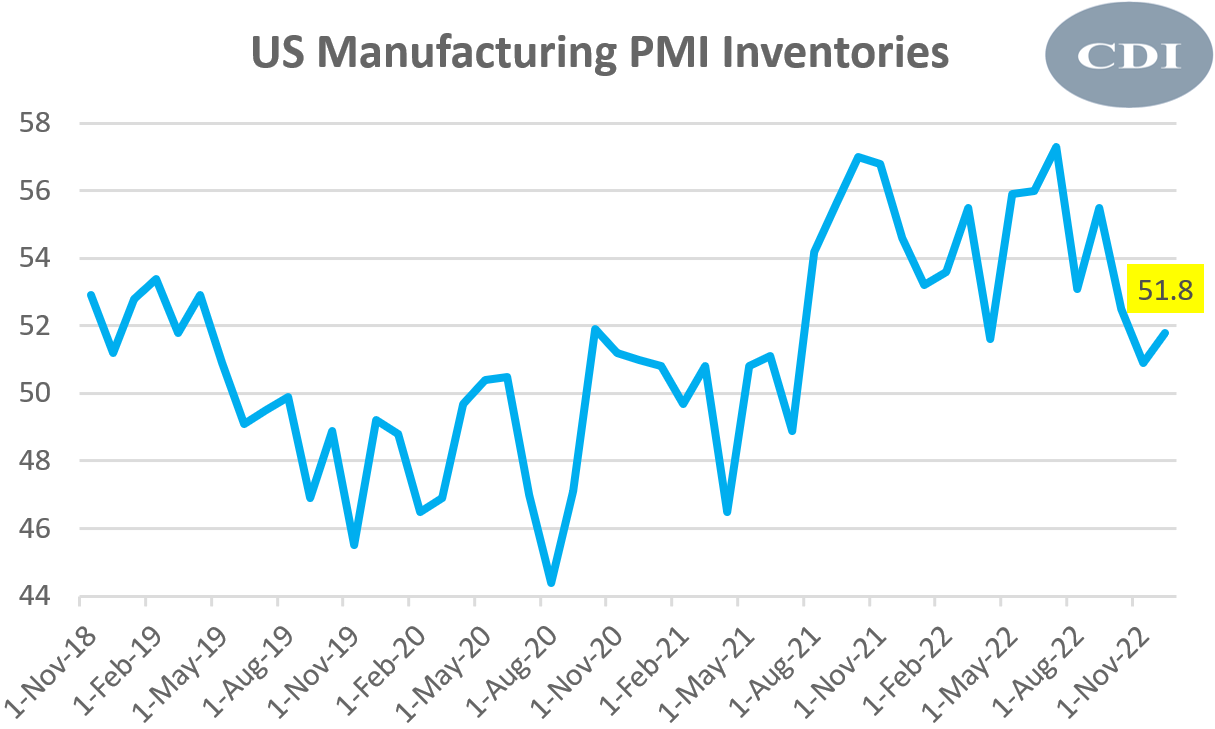

Strong momentum with a healthy demand outlook; manufacturing inventory buffer to cushion volume declines

The U.S. PMIs are contracting with a 48.4 print as of December 2022:

US Manufacturing PMI (US ISM Manufacturing PMI, CDI Research)

This is not a good sign for trucking volumes. However, there is a silver lining.

US Manufacturing PMI Inventories (US ISM Manufacturing PMI, CDI Research)

Inventories are still expanding, indicating stock buffers in the system. This can provide a cushioning effect to freight volume declines.

XPO volume growth is outpacing the industry

The company’s delivery volumes are trending strongly. As per the Q3 FY22 earnings call (linked above):

A key inflection point came in September when we flipped tonnage positive year over year. Our tonnage trend continued to surpass typical seasonality in October. I’m pleased that our results are strengthening relative to our peers.

This is another validation of XPO’s moves to expand capacity.

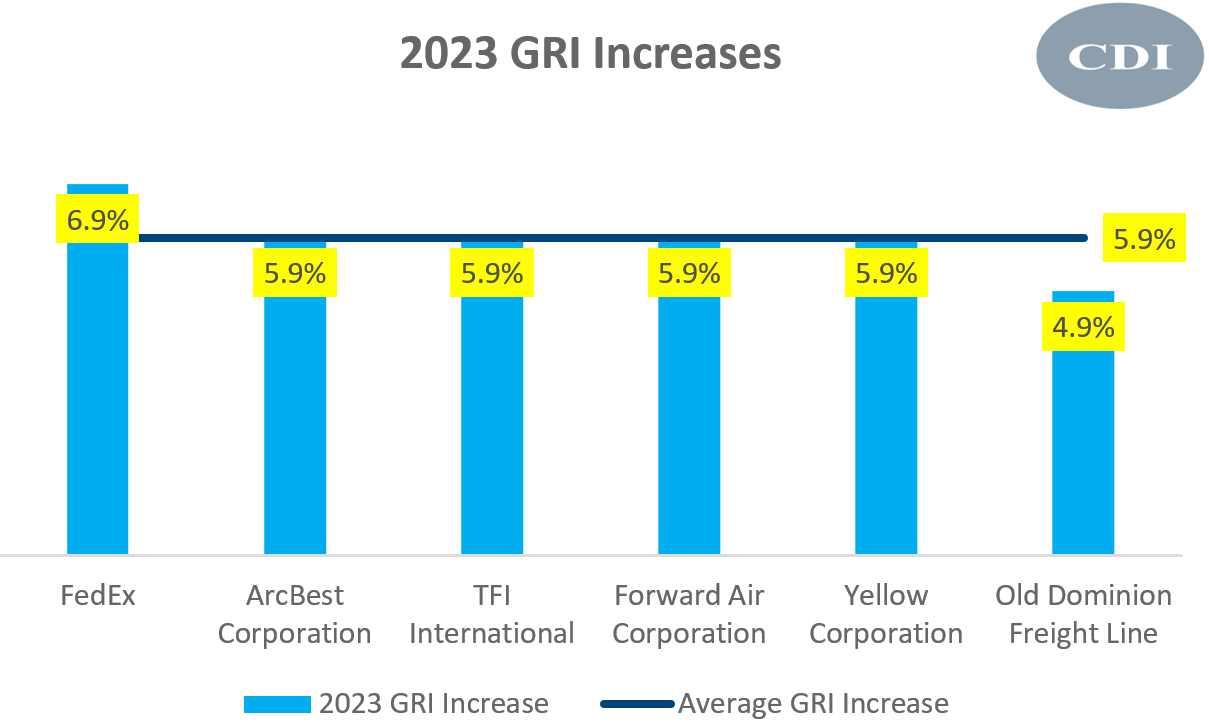

Price improvements will continue

Based on company filings, across the LTL industry, 2023 general rate increases (GRIs) have averaged 5.9%:

2023 GRI Increases (Koho, CDI Research)

Over the past two years, XPO’s LTL pricing yield has grown at a rate of 13.7% CAGR; well-above the industry’s pricing two-year pricing CAGR of 4.5%. In the last 12 months, XPO’s yields accelerated to grow at a rate of 16.4% CAGR. Given this record, we expect XPO to at least keep in-tandem with industry level GRI increases.

Management’s bullish commentary is believable

Management commentary in the Q3 FY22 earnings call (linked above) is bullish on multiple fronts. A couple of examples:

On customer onboarding:

…we onboarded several large customers in the third quarter that have the potential to become top 10 customers.

On deal wins:

In the second quarter, we had record business wins. In the third quarter, we have had another quarter of record business wins. Our pipeline is the highest it’s been, and we’re trending in the right direction.

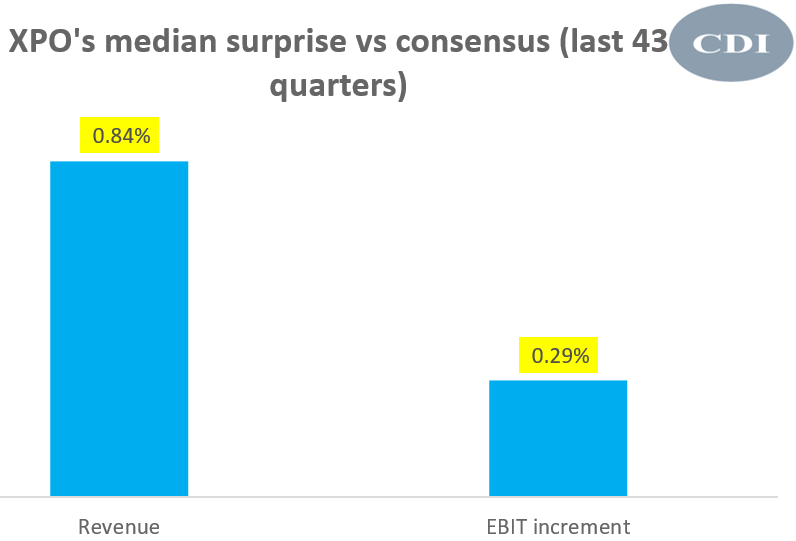

Can we trust their commentary?

Surprise vs Consensus History (CDI Research)

With a median revenue surprise of +0.84% and a median EBIT increment surprise of 29bps, XPO has generally outperform Wall St’s expectations. Thus, we are inclined to believe XPO management’s words.

Valuation

There is compelling upside for XPO based on EV/EBIT valuation.

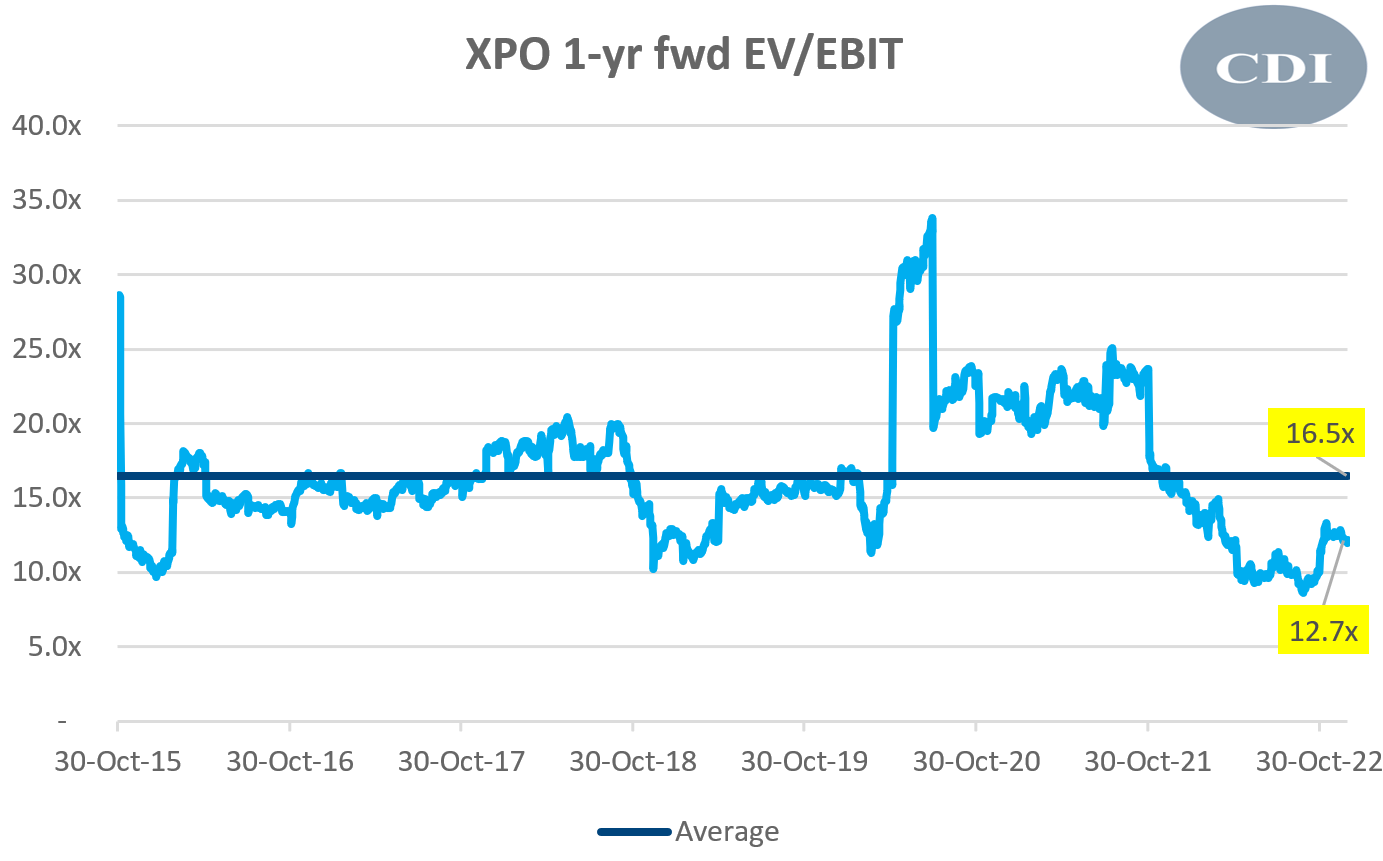

XPO 1-yr fwd EV/EBIT (CDI Research)

XPO currently trades at a one-year fwd EV/EBIT multiple of 12.7x, implying a 23% discount to the long-term average multiple of 16.5x. Considering the company’s former position as industry’s top performer before brokerage business drags, the return to an LTL-focused business, secular industry tailwinds, capacity expansions and growth momentum, we believe XPO deserves at least a 16.5x multiple.

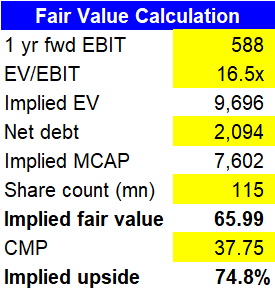

XPO Fair Value Estimate (CDI Research)

Applying a 16.5x multiple to FY23 consensus EBIT numbers of $588 million, we derive a fair value of $65.99, corresponding to a compelling 74.8% upside.

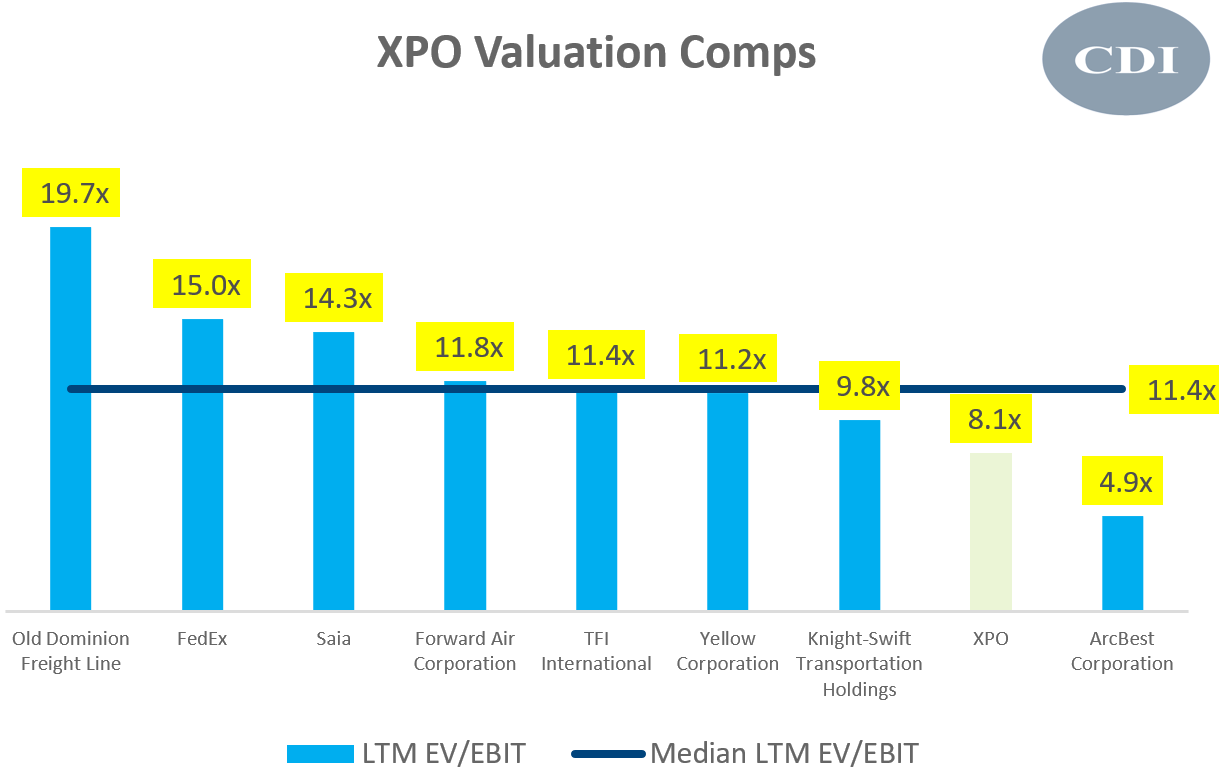

Discount relative to peers indicates mispricing

LTM EV/EBIT Valuation Comps (CDI Research)

XPO’s peers include Old Dominion Freight Line (ODFL), FedEx (FDX), Saia (SAIA), Forward Air Corporation (FWRD), TFI International (TFII), Yellow Corporation (YELL), XPO (XPO), and ArcBest Corporation (ARCB). All peers are in the top 25 list of the U.S. LTL industry.

At an LTM EV/EBIT of 8.1x, XPO trades at a 28.9% discount to the peer average of 11.4x. Given our view on XPO, we believe represents a gross market mispricing.

Risks

Three key risks to monitor are:

- Industry-wide capacity additions leading a surplus market and price cuts

- Extended weakness in the manufacturing and retail end-user sectors curbing volume growth

- Lower-than-expected 2023 GRI increase by XPO

The first risk is the most potent if it occurs, although XPO has a first-mover advantage in capacity additions to reap most of the initial gains from expanded volumes. The second risk has a moderate chance of occurrence. We are comforted by the demand-constrained nature of the industry, XPO’s undemanding valuations and confidence in market share growth.

Lower pricing might be acceptable if it is well-compensated by volume growth. There are early signs of greater price sensitivity by customers as FedEx’s latest earnings call marked a shift toward budget-friendly delivery options.

Catalyst

Management wants to divest the European business, which currently makes up ~33% of revenues. This divestment would be a positive catalyst for XPO because the underlying economics of the European business is weaker with degrading quality of revenues and margins.

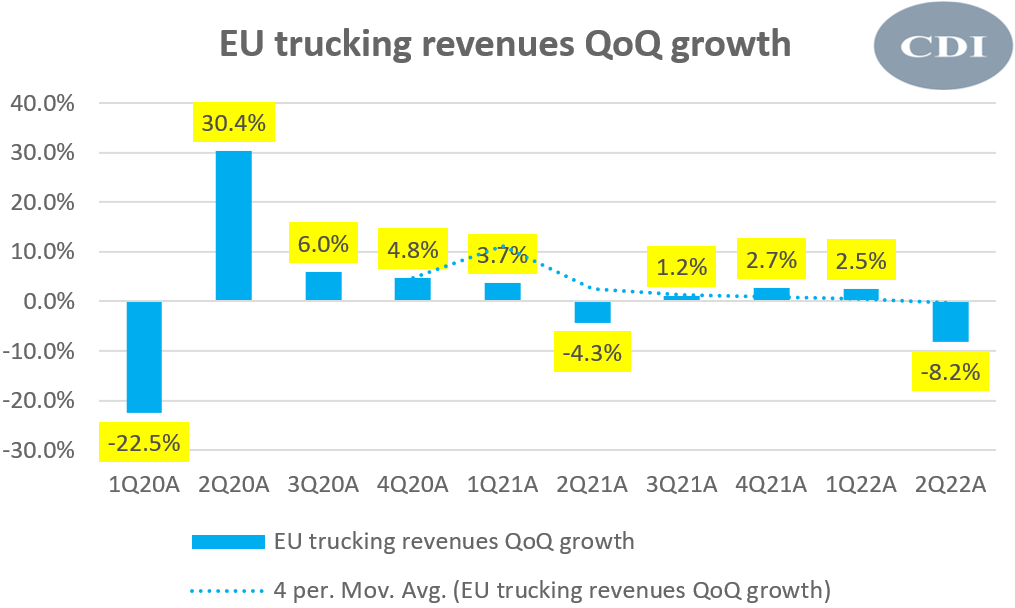

EU Trucking Revenues QoQ (CDI Research)

Revenue growth has been tepid below 3% CQGR over the past few quarters.

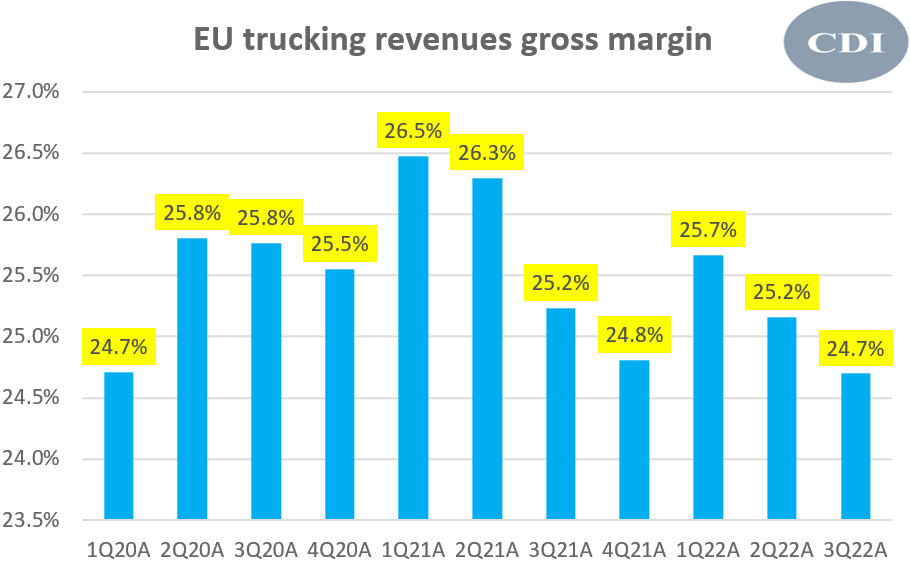

EU Trucking Gross Margins (CDI Research)

EU trucking gross margins have seen a consistent decline since the peak of 2021.

Conclusion

XPO is a compelling investment opportunity with 75% upside. It is supported by a structurally attractive LTL market favoring larger players that also has powerful growth tailwinds from e-commerce, reshoring, and near-shoring of supply chains.

Faster revenue growth and higher gross margins lead to a better pure-play LTL business profile post XPO’s spinoff of its brokerage business, which was facing cyclical headwinds. CEO Mario Harik has the right mix of capabilities to unlock further growth and margin potential at XPO via a broad capacity addition strategy to elevate demand constraints.

XPO’s business momentum is strong and we expect the relative outperformance over the industry to continue as the company returns to a golden age.

Be the first to comment