aprott

Novo Nordisk A/S (NVO) secured the FDA approval for Wegovy, the weight loss version of the compound called semaglutide, for the indication of reducing risks of major cardiovascular adverse events (‘MACE’) in early March. Novo Nordisk is already enjoying significant commercial success with the type 2 diabetes version of semaglutide called Ozempic, and more recently, Wegovy is off to a strong start and would have higher uptake if it were not for the supply constraints as demand is exceeding supply.

The MACE (heart health) label expansion not only makes Wegovy more attractive for overweight and obese patients wanting to lose weight, it further extends Novo Nordisk’s leadership position in the obesity market as no competitor other than Eli Lilly and Company (LLY) will have such a broad label anytime soon. It took nearly six years from the start of the SELECT trial to FDA approval. And the expanded label that includes a heart health benefit makes Wegovy eligible for Medicare coverage which unlocks another large addressable market with millions of patients becoming eligible.

I have not covered Novo Nordisk other than in the late 2021 article where I outlined what the company is getting from the $3.3 billion acquisition of Dicerna Pharmaceuticals which was my portfolio stock at the time. That was a neutral rating on Novo Nordisk as I did not have a strong view of the company at the time, and I am initiating coverage today with a buy rating. The valuation is a bit on the high side, but I believe it is justified by the several years of expectations of very strong top and bottom-line growth.

The cardiovascular outcomes data that led to Wegovy’s MACE approval

The early March approval of Wegovy was based on the SELECT cardiovascular outcomes trial, where Wegovy demonstrated a 20% reduced risk of MACE compared to a placebo when added to the standard of care. The risk reduction was not only observed for the composite MACE endpoint that includes cardiovascular death, non-fatal heart attack or non-fatal stroke in adults with either overweight or obesity and established cardiovascular disease, it also reduced the risk of death from any cause by 19% compared to placebo, and the findings were independent of age, sex, race, ethnicity, body mass index, or renal function impairment.

The New England Journal publication from last year shows these benefits in graphic form and the consistency between endpoints.

New England Journal of Medicine

Wegovy, and generally, the GLP-1 agonist class of drugs, have some safety and tolerability tradeoffs, consisting primarily of gastrointestinal disorders (nausea, vomiting, diarrhea), as well as a somewhat higher risk of gallbladder disorders, but I believe the risk-reward is heavily skewed in Wegovy’s favor.

MACE or heart health label expansion makes Wegovy eligible for Medicare coverage

The heart health label expansion in March finally makes Wegovy eligible for Medicare coverage as Medicare does not cover obesity medicines. The healthy policy research organization KFF says that 3.6 million people with Medicare could be eligible to take Wegovy for heart health. The out-of-pocket cost may be high for many of these patients, but the new IRA provision that caps out of pocket costs to $2,000 starting next year should help improve affordability of these drugs.

KFF further estimates that Medicare spending would rise by $2.8 billion if just 10% of the eligible population use the drug for a full year. My rough math suggests KFF estimates Medicare will pay approximately $650 per Wegovy prescription, or approximately half the list price. This would make the total addressable Medicare market worth $28 billion for Novo Nordisk. However, 3.6 million is only 7% of total beneficiaries and this was a 2020 estimate and the actual numbers could be higher, and the number of Medicare patients who are obese or overweight is estimated at 13.7 million.

It is hard to have an accurate estimate of the potential revenue contribution of the Medicare channel opening up for Wegovy, but it is likely to be significant, and I expect Medicare sales to contribute $6 billion to $10 billion in revenues for Novo Nordisk by the end of the decade by capturing 20% to 30% of the smaller market estimated by KFF (and assuming very modest price inflation), and likely more than $15-20 billion if the broader population ends up being eligible and assuming lower penetration rates. And these numbers are still very material for Novo Nordisk as the current Street estimate for total revenues in 2030 is $82.5 billion.

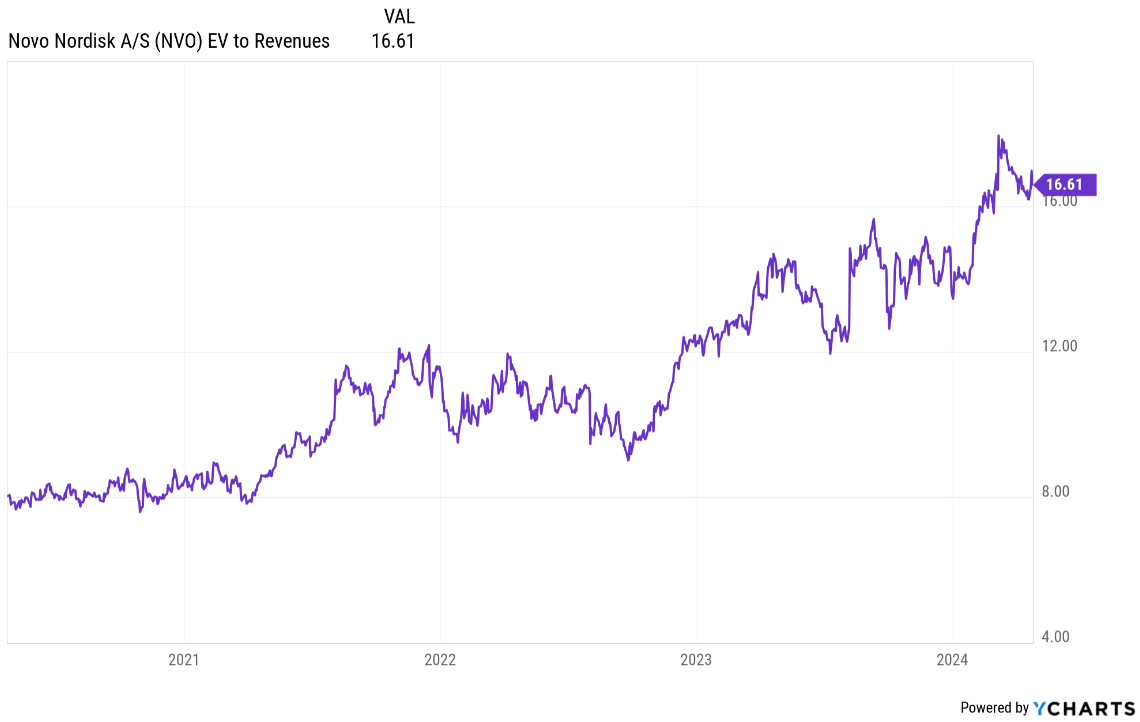

Valuation demands high growth, but it should be there

Novo Nordisk’s enterprise value/revenue has been expanding in the last few years, driven by the success of Ozempic and more recently Wegovy, but it has been a function of accelerating growth.

Ycharts

Revenue growth has accelerated from only 3.4% in 2021 to 18.3% in 2022 and 35% in 2023. Current topline growth estimates for 2024 and 2025 are 22.5% and 20.3%, respectively, but I do think they may be underestimating the growth potential of Novo Nordisk’s obesity franchise. Even if the stock remains flat, the valuation multiples will compress back to 2022 levels by 2026 and that is assuming the company meets current revenue and earnings growth expectations.

There are still supply constraints for Wegovy that are still masking its full growth potential, and the competitive advantages are not going away anytime soon, and I continue to see the obesity and adjacent markets as a duopoly in the next 5-6 years due to the significant head start of Novo Nordisk and Eli Lilly.

It is highly unlikely that any of the competing products in development will have product labels that even closely resemble the current label that Ozempic and Wegovy have or the label Eli Lilly’s tirzepatide (Mounjaro/Zepbound) will have in the not-too-distant future: type 2 diabetes, weight loss, cardiovascular risk reduction (the SELECT trial started in mid-2018 and the FDA approval was secured in March 2024, nearly six years later), heart failure with preserved ejection fraction (with FDA/EMA applications being recently submitted), knee osteoarthritis, and there was also recently a successful study of tirzepatide in obstructive sleep apnea.

Both companies are also working on next-generation therapies that are likely to have improved weight loss and the next area of intense focus could also be improved body composition through improved fat mass reduction along with limited loss of lean body mass.

Conclusion

The approval of Wegovy for the reduction of cardiovascular risk in people with overweight and obesity marks an important milestone for Novo Nordisk and the GLP-1 class of drugs Wegovy belongs to. The approval should not only lead to greater adoption across the overweight and obese populations as Wegovy has now proved patients can have improved heart health alongside weight loss, but it also makes the product eligible for Medicare coverage which should provide a further boost to Novo Nordisk’s total revenue and profits in the following years.

Be the first to comment