Sundry Photography

Introduction

San Antonio-based Valero Energy Corp. (NYSE:VLO) released its second-quarter 2022 results on July 28, 2022.

Note: This article is an update to my article published on May 11, 2022. I have followed VLO on Seeking Alpha since December 2017.

A quick look at the overall business

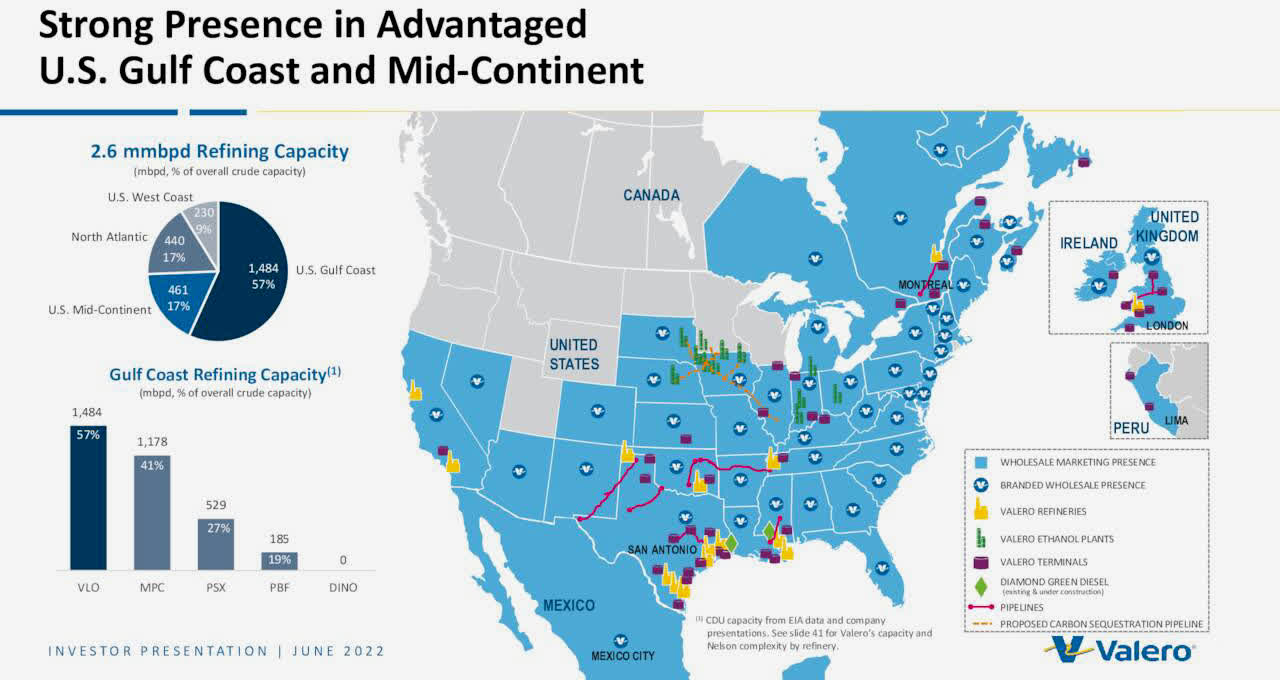

VLO Map Presentation (Valero Energy)

1 – 2Q22 results snapshot

The U.S. refiner reported second-quarter 2022 adjusted earnings of $11.36 per share, significantly increasing from $0.48 per share in the year-ago quarter. The results beat analysts’ expectations.

Total revenues surged from 27,748 million last year’s quarter to a record of $51,641 million in 2Q22, well over the consensus estimate.

The better-than-expected results were supported by increased refinery throughput volumes and a higher refining margin.

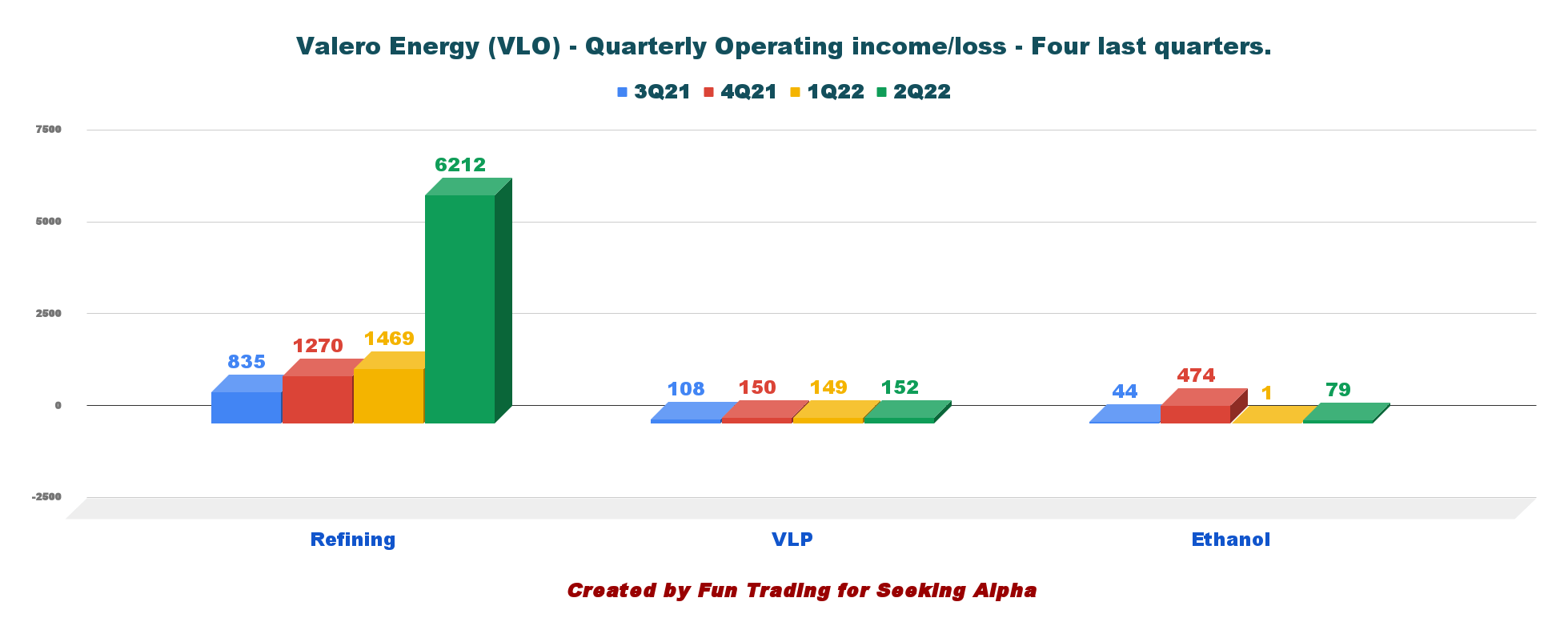

The quarterly operating income for the second quarter of 2022 is presented below. We can see that the refining segment has increased significantly and reached a record in 2Q22.

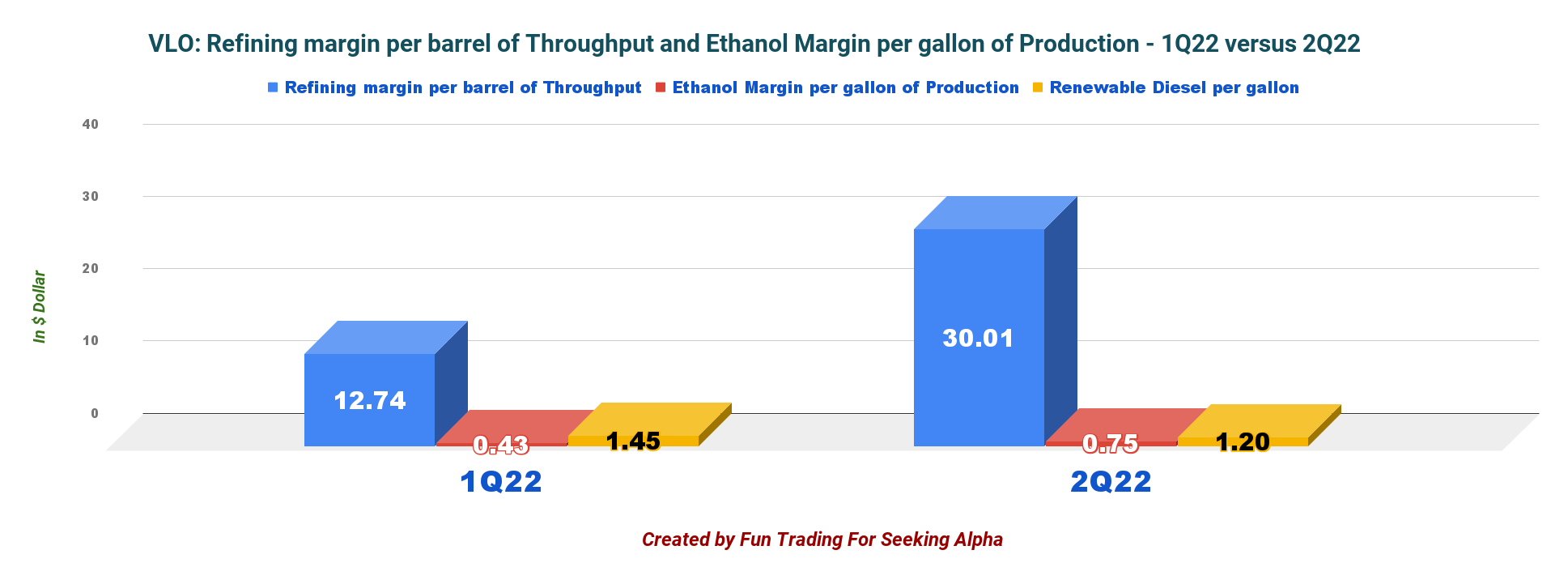

VLO Quarterly operating income history (Fun Trading) The refining margin per barrel of throughput increased to $30.01 from $7.95 the preceding year, while the ethanol margin increased from $0.62 to $0.75. VLO Refining margin per barrel 1Q22 versus 2Q22 (Fun Trading) CEO Joe Gorder said in the conference call: We’ve been increasing throughput since 2020, as demand recovered along with the easing of COVID-19 pandemic restrictions. Our refinery utilization rate increased from the pandemic low of 74% in the second quarter of 2020, to 94% in the second quarter of 2022. Refining margins in the second quarter were supported by continued strength in product demand, coupled with low product inventories and continued energy cost advantage for U.S. refineries compared to global competitors.

2- Investment Thesis

I have been a long-term VLO shareholder for many years, and I plan to keep a sizeable part of my long position for a long time horizon.

However, VLO has rebounded exceptionally well since the preceding quarter and has reached an over-valuation situation which has been one of the triggers for a substantial sell of my position at over $141 in mid-June. I said at the time:

Like Icarus flying too close to the sun, this situation will trigger a dangerous fall in time. Investors must recognize it and adopt a tailored long-term strategy that benefits from those extreme situations.

The refining business is characterized by a highly volatile environment requiring short-term trading using the LIFO method to turn this investment fruitful.

Those comments were spot on, and VLO dropped significantly soon after.

The third quarter will probably show a correction from extremely favorable margins experienced in the second quarter to more reasonable valuations. The Fed’s action on interest rates to fight rampant inflation will likely affect the economy and demand for fuel in H2 2022.

Thus, it is dangerous to use recent results as indicators and rely on primary financial ratios to determine a hypothetical fair value.

The crucial issue at stake here is the extreme volatility of the refining sector, which requires a particular trading/investing strategy that I promote in my marketplace, “The gold and oil corner.”

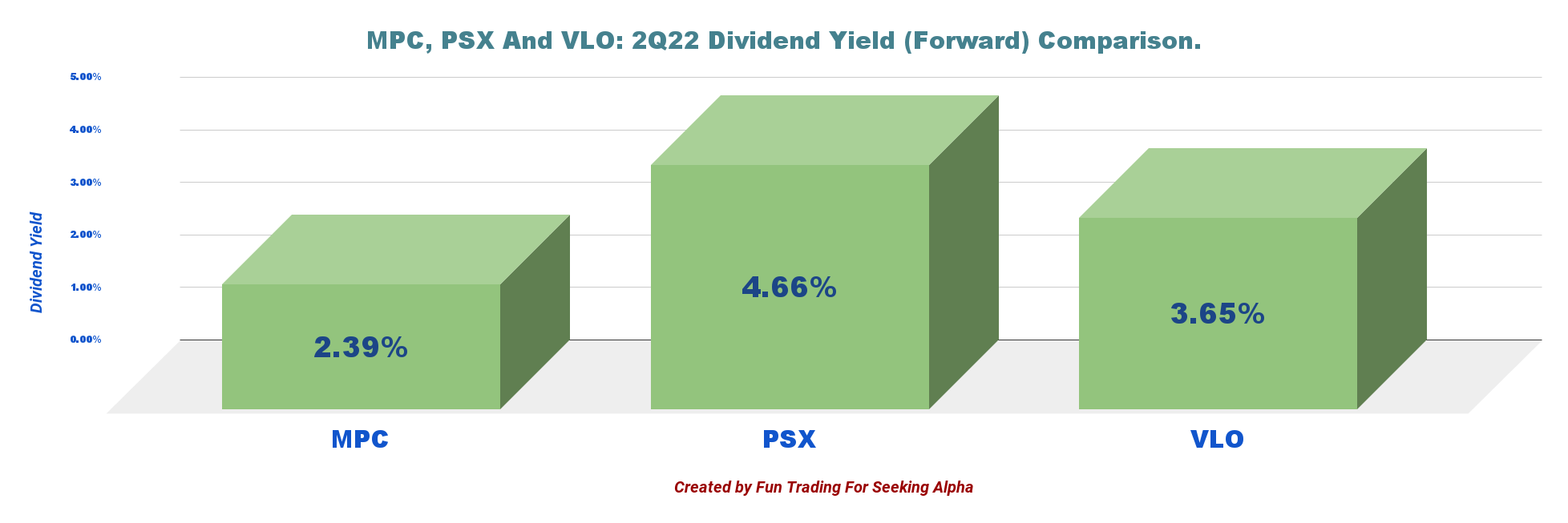

I believe trading short-term LIFO and profit from the wild fluctuations attached to this cyclical industry is essential. I recommend using short-term about 40% of your position and keeping a core long-term for a much higher target or enjoying a steady stream of dividends. VLO pays a dividend yield of 3.65%, which is relatively high and safe.

VLO Dividend comparison with peers (Fun Trading)

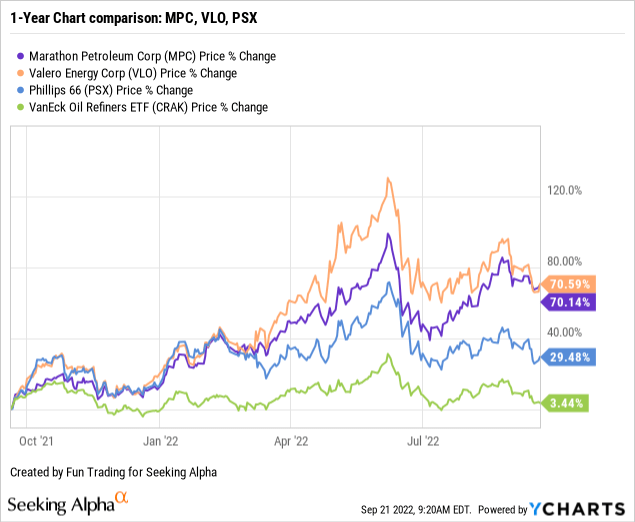

3 – Stock performance

VLO is now up 71% on a one-year basis, outperforming Phillips 66 (PSX) but very close to Marathon Petroleum (MPC).

VLO 1-Year chart comparison: MPC, VLO, PSX (Ycharts)

Valero Energy: Selected Financials – The Raw Numbers (Second Quarter Of 2022)

| Valero Energy | 2Q21 | 3Q21 | 4Q21 | 1Q22 | 2Q22 |

| Total Revenues in $ Billion | 27.75 | 29.52 | 35.90 | 38.54 | 51.64 |

| Net Income in $ Million | 162 | 463 | 1,009 | 905 | 4,693 |

| EBITDA $ Million | 1,199 | 1,366 | 2,029 | 1,970 | 6,854 |

| EPS diluted in $/share | 0.39 | 1.13 | 2.46 | 2.21 | 11.57 |

| Operating cash flow in $ Million | 2,008 | 1,449 | 2,454 | 588 | 5845 |

| CapEx in $ Million | 355 | 463 | 398 | 384 | 417 |

| Free Cash Flow in $ Million | 1,653 | 986 | 2,056 | 204 | 5,428 |

| Total Cash $ Billion | 3.572 | 3.498 | 4.122 | 2.638 | 5,392 |

| Total L.T. Debt (incl. current) in $ Billion | 14.68 | 14.23 | 11.95 | 13.16 | 12.88 |

| Dividend per share in $ | 0.98 | 0.98 | 0.98 | 0.98 | 0.98 |

| Shares Outstanding (Diluted) in Million | 407 | 408 | 407 | 408 | 404 |

| Oil, N.G. & Ethanol Production | 2Q21 | 3Q21 | 4Q21 | 1Q22 | 2Q22 |

| Throughput volume in K Bop/d | 2,835 | 2,854 | 3,033 | 2,800 | 2,962 |

| Ethanol in K gallon p/d | 4,203 | 3,625 | 4,402 | 4,045 | 3,861 |

| Brent price ($/b) | 69.00 | 73.22 | 79.85 | 97.34 | 111.69 |

| WTI price ($/b) | 66.09 | 70.58 | 77.36 | 94.46 | 108.66 |

| Natural gas price ($/MM Btu) | 2.93 | 4.25 | 4.54 | 4.32 | 7.23 |

Source: VLO PR

Revenues, Earnings Details, Free Cash Flow, Throughput Volume, Ethanol Production, And Margins

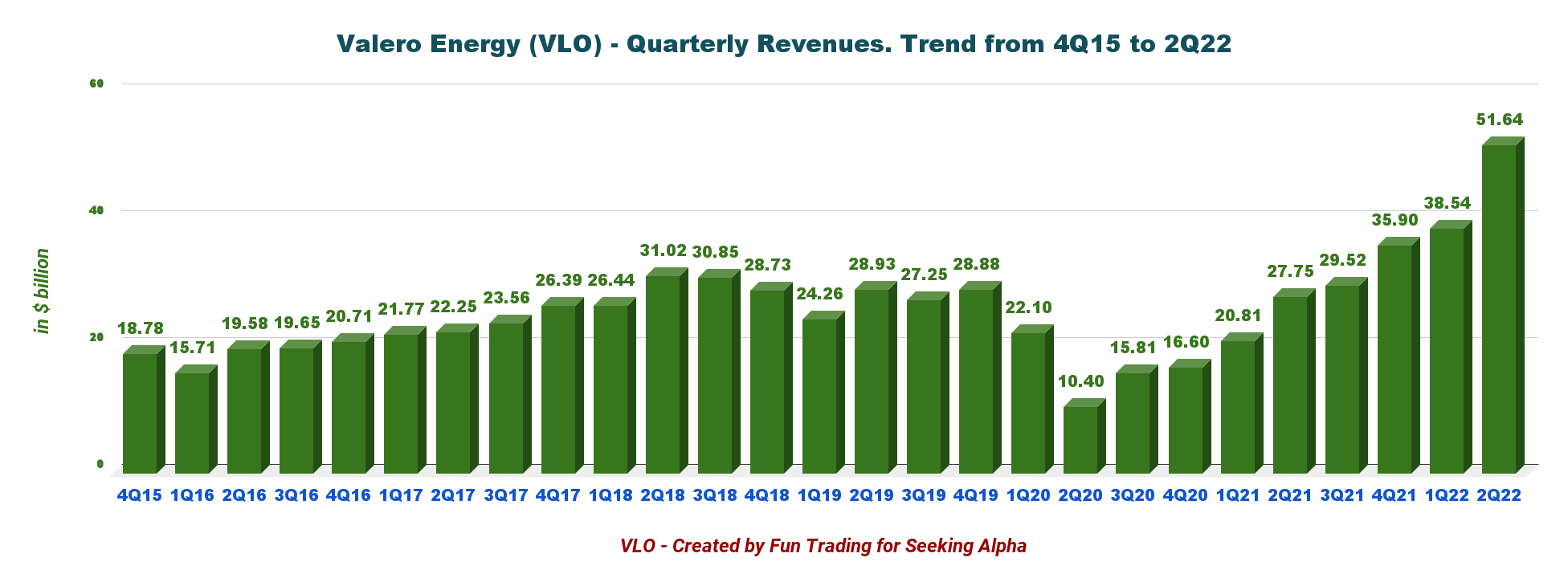

1 – Revenues were a record of $51.64 billion in 2Q22

VLO Quarterly Revenues history (Fun Trading)

Valero Energy’s revenue for the second quarter was $51.641 billion. The company posted a quarterly income of $11.57 per diluted share compared to $0.39 last year.

The total cost of sales rose to $45,162 million from $27,039 million last year, primarily due to the higher cost of materials.

The reported adjusted net Income was $4,609 million, or $11.36 per share, for the second quarter, compared to $260 million or $0.63 per share.

Review of the different segments:

- The refining segment: The operating Income was $6,122 million compared to $442 million in the year-ago quarter. Higher refinery throughput volumes supported the part again this quarter.

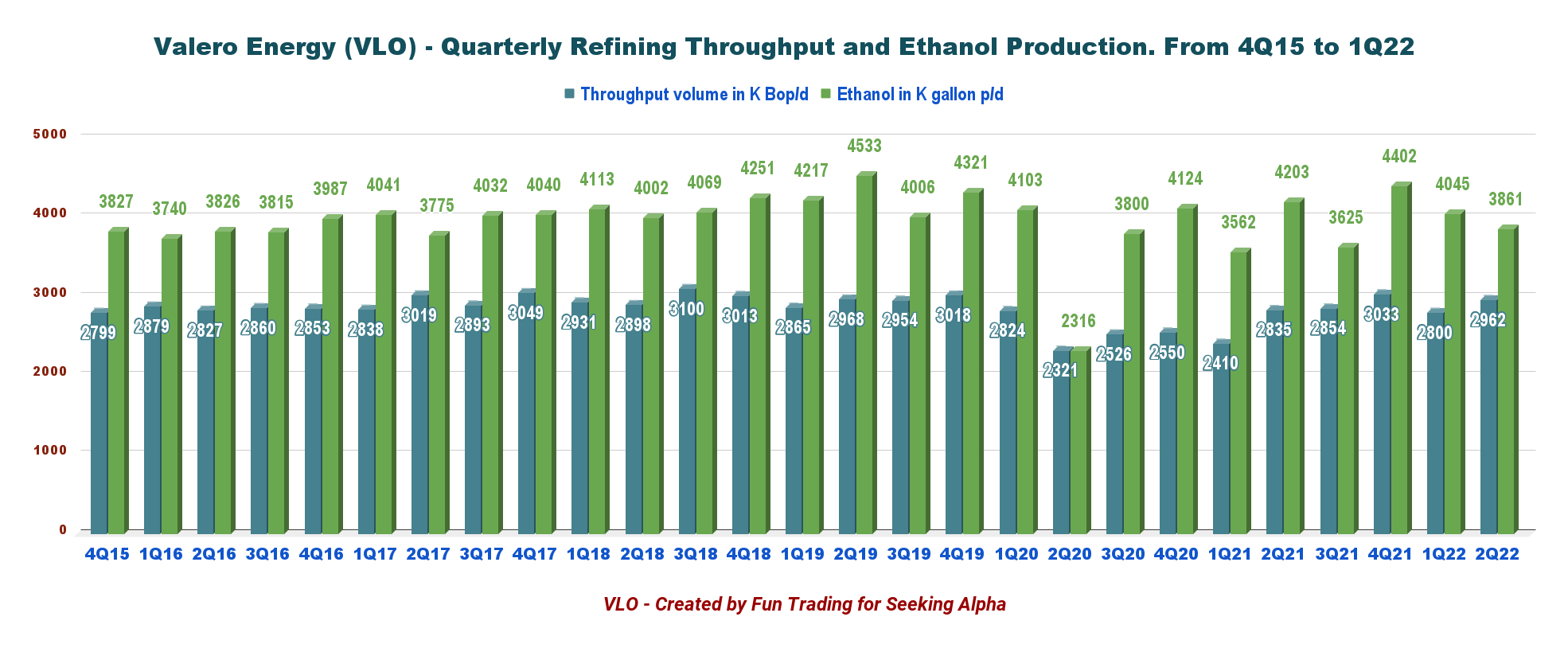

- The Ethanol segment: The adjusted operating profit was $79 million compared to $99 million in the second quarter of 2021. Lower ethanol production volumes were to blame. Production decreased to 3,861 thousand gallons per day from 4,203 thousand gallons a year ago.

- The Renewable Diesel segment: The segment’s operating Income dropped to $152 million compared to $248 million in the year-ago period. However, renewable diesel sales grew to 2,182 thousand gallons per day from 923 thousand gallons a year ago.

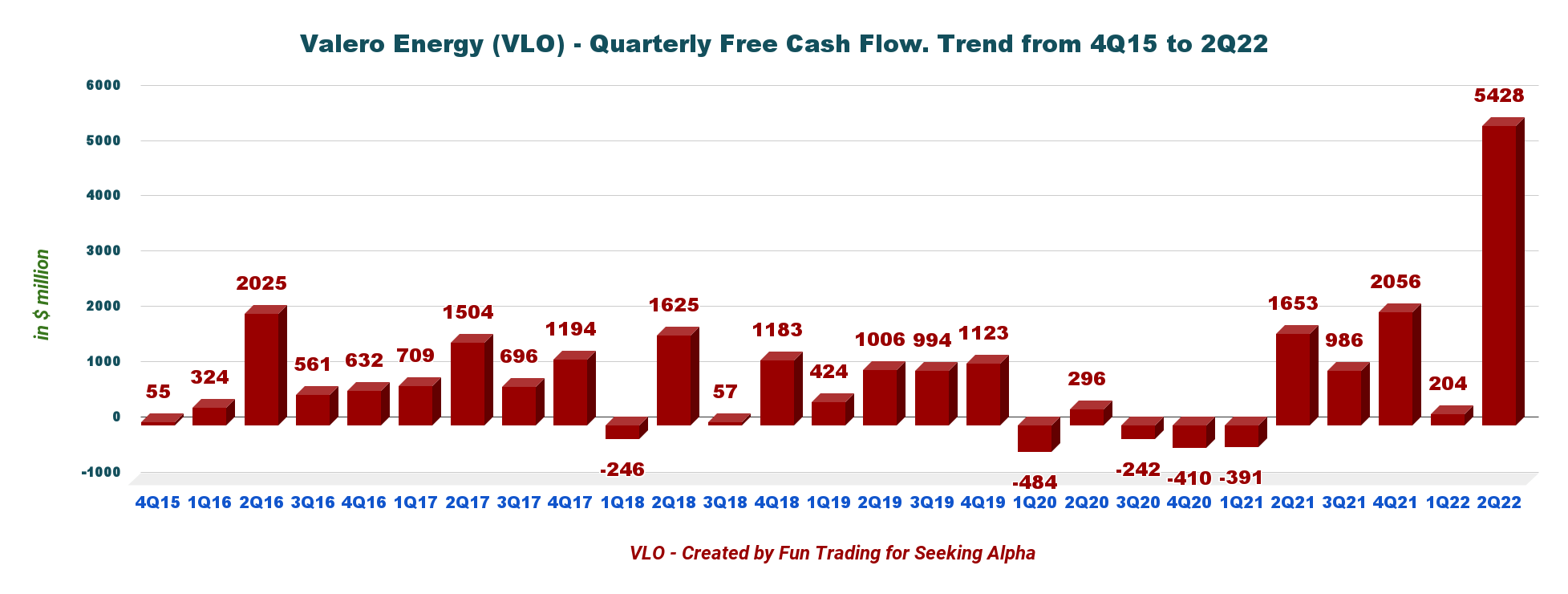

2 – Free cash flow in 2Q22 was a whopping $5,428 million

VLO Free cash flow history (Fun Trading)

Note: The generic free cash flow is the Cash from operating activities minus CapEx.

VLO had a trailing 12-month ttm free cash flow of $8,674 million. Free cash flow for the second quarter is $5,428 million, significantly up sequentially.

The quarterly dividend is unchanged at $0.98 per share. The dividend cash cost is now $1,583 million per year, while ttm free cash flow is $8,674 million, suggesting that VLO could pay a little more in dividends in 2022.

However, the situation has deteriorated somewhat since the release of the second quarter, and expecting a dividend increase in H2 2022 is less likely.

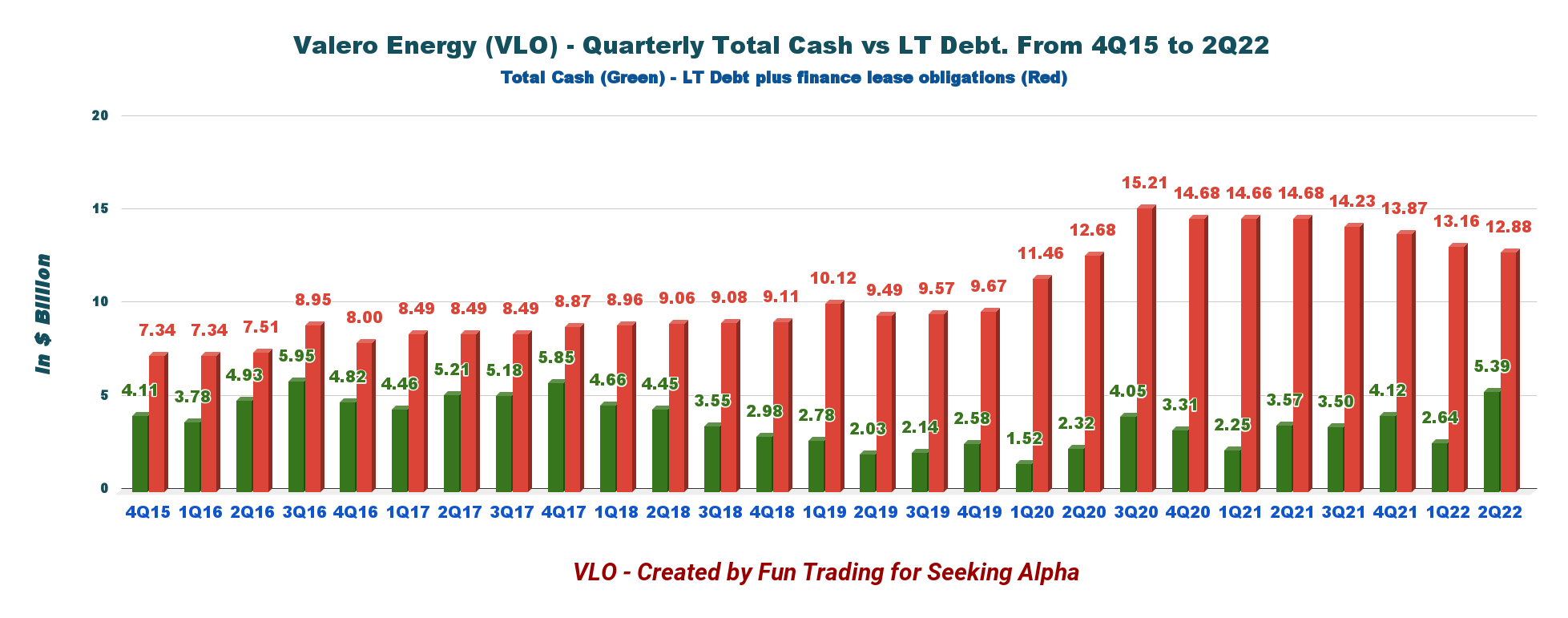

3 – Net debt was $7.488 billion as of June 30, 2022

VLO Quarterly Cash versus Debt history (Fun Trading)

Valero Energy had total Cash of $5,392 million in 2Q22, up from $2,638 million the preceding quarter. Total debt and finance lease obligations were $12,880 million compared to $14,680 million last year.

The debt to capitalization ratio, net of Cash and cash equivalents, was 25% as of June 30, 2022, down from the pandemic high of 40% at the end of the first quarter of 2021.

Valero cut debt by $300 million through the acquisition of the 4% Gulf Opportunity Zone Revenue Bonds (GO Zone Bonds), reducing Valero’s debt by $2.3 billion in the second half of 2021.

VLO has done an excellent job of reducing the debt, as seen in the graph above.

4 – Throughput and ethanol production in 2Q22

VLO Quarterly Throughput and Ethanol production history (Fun Trading)

Refining throughput volumes were 2,962K barrels per day for the second quarter, up 4.5% from last year.

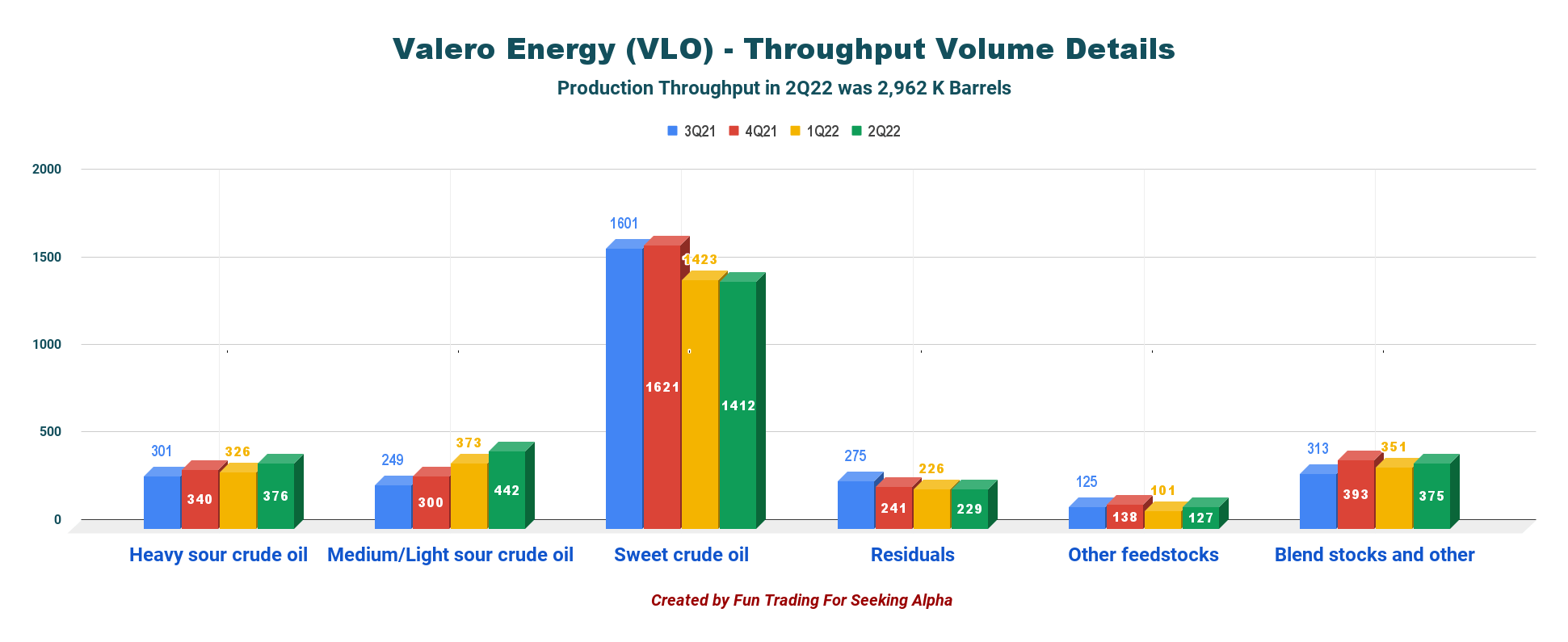

Feedstock composition for the last four quarters: Sweet crude oil is the highest.

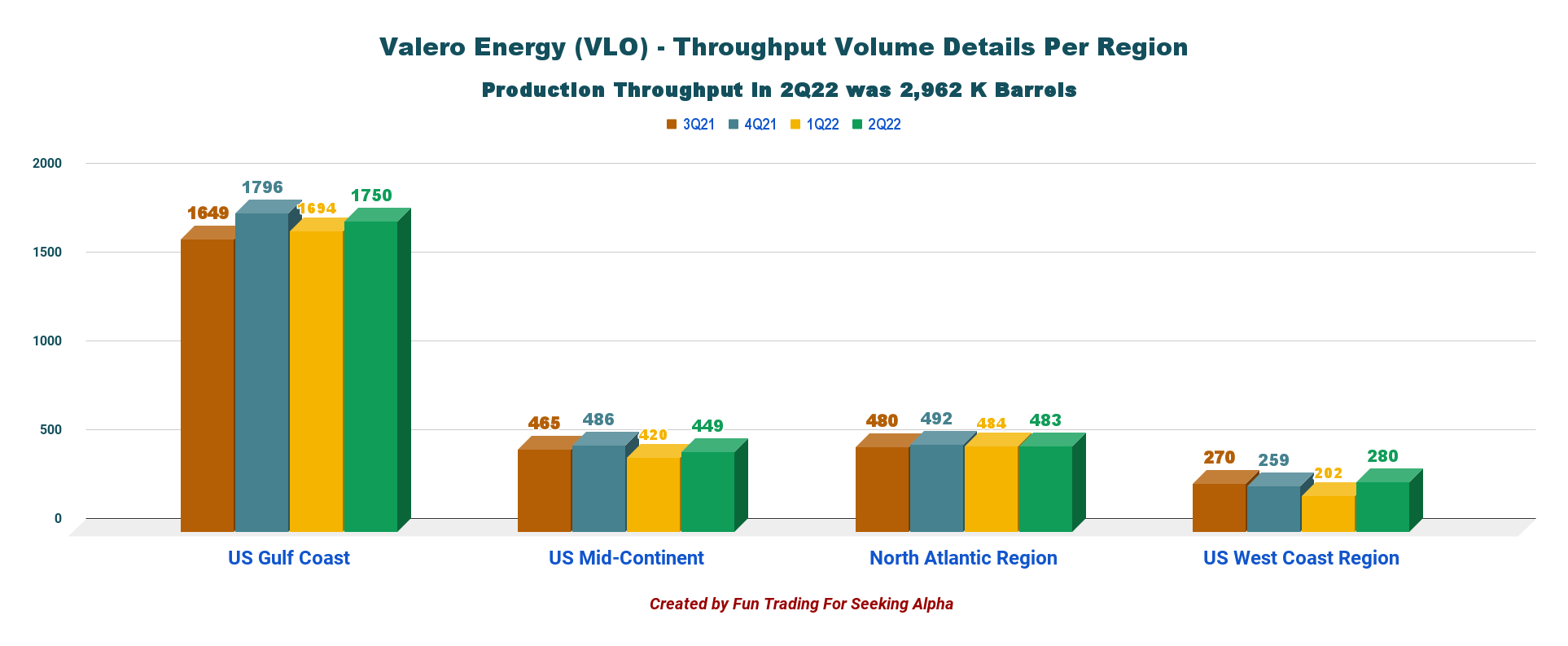

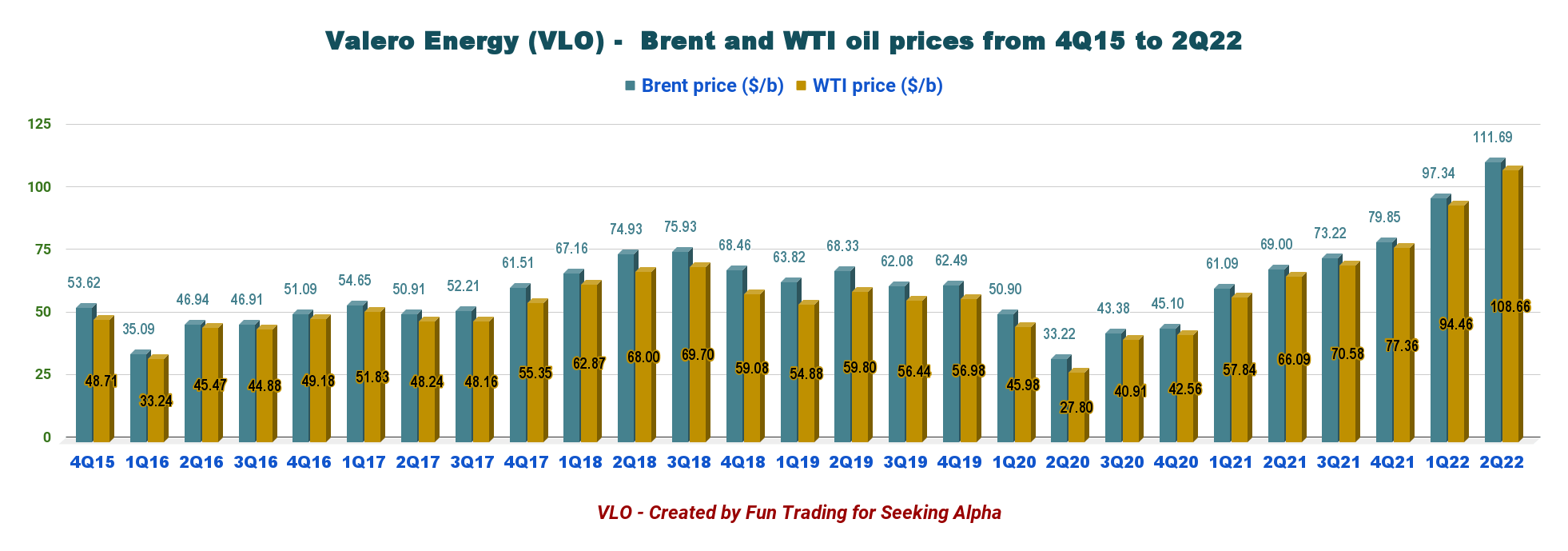

VLO Throughput Detail (Fun Trading) VLO Throughput per region (Fun Trading) VLO Quarterly Brent and WTI prices history (Fun Trading)

Technical Analysis (Short-Term) And Commentary

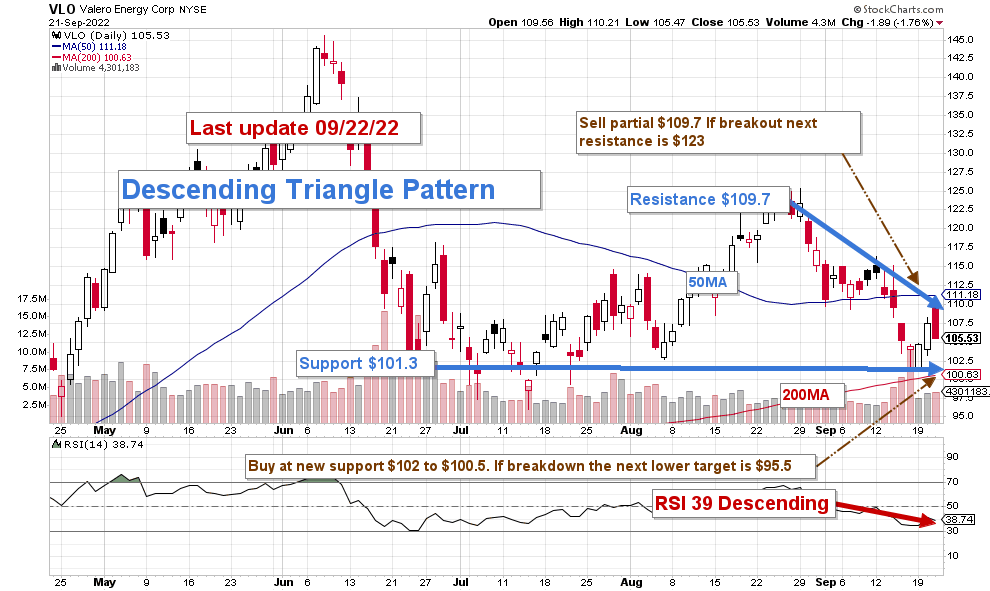

VLO TA Chart short-term (Fun Trading StockCharts)

Note: The chart has been adjusted for the dividend.

VLO forms a descending triangle pattern with resistance at $109.7 and support at $101.3.

The dominant strategy that I regularly promote in my marketplace, “The gold and oil corner,” is to keep a core long-term position and use about 40% to trade LIFO (see note below) while waiting for a higher final price target for your core position above $109.7 with potential higher resistance at $123.

The trading strategy is to sell about 40% at or above $130 and wait for a possible retracement. A possible upper resistance could be $135.20, but I believe it is unlikely to reach this level in 2022.

The most probable outcome is that VLO loses its strong momentum and drops to the support at $101.3, potentially dropping to the lower support at $95.5. Thus, I recommend buying VLO for between $101.5 to $95.5.

Note: The LIFO method is prohibited under International Financial Reporting Standards (IFRS), though it is permitted in the United States by Generally Accepted Accounting Principles (GAAP). Therefore, only U.S. traders can apply this method. Those who cannot trade LIFO can use an alternative by setting two different accounts for the same stock, one for the long term and one for short-term trading.

Warning: The TA chart must be updated frequently to be relevant. It is what I am doing in my stock tracker. The chart above has a possible validity of about a week. Remember, the T.A. chart is a tool only to help you adopt the right strategy. It is not a way to foresee the future. No one and nothing can.

Author’s note: If you find value in this article and would like to encourage such continued efforts, please click the “Like” button below to vote of support. Thanks.

Be the first to comment