ProShares Trust II – ProShares Ultra Bloomberg Crude Oil (NYSEARCA:NYSEARCA:UCO) (the “Fund”) is a high-risk, double-long oil market exposure exchange-traded fund (“ETF”). Crude oil futures prices have been highly volatile this year, and so doubling the risk would not be appropriate for many investors.

Furthermore, the Fund attempts to track an index on a daily basis, subjecting investors to even greater risk if they hold UCO any longer. I highlight the risks explained by ProShares below.

I review the performance of USO since inception. It has lost 99% of its value.

I also explain my crude oil trading strategy and present real-time results compared to UCO since June 2022.

Finally, I provide my most recent oil market projections and conclude oil futures prices are overvalued.

ProShares

Risks

Below, I highlight some of the key risks in the prospectus. ProShares advises:

UCO’s use of compounding and leverage increases risk and could result in the total loss of an investor’s investment within a single day.

Due to the compounding of daily returns, holding periods of greater than one day can result in returns that are significantly different than the target return, and ProShares’ returns over periods other than one day will likely differ in amount and possibly direction from the target return for the same period. These effects may be more pronounced in funds with larger or inverse multiples and in funds with volatile benchmarks.

A fund will lose money if its benchmark’s performance is flat over time, and a fund can lose money regardless of the performance of its benchmark, as a result of daily rebalancing, the benchmark’s volatility, compounding, and other factors.

The Funds are not actively managed by traditional methods (e.g., by effecting changes in the composition of a portfolio on the basis of judgments relating to economic, financial and market conditions with a view toward obtaining positive results under all market conditions). Each Fund seeks to remain fully invested at all times in Financial Instruments and money market instruments that, in combination, provide exposure to its underlying benchmark consistent with its investment objective, even during periods in which the benchmark is flat or moving in a manner that may cause the value of the Fund to decline.”

ProShares

Expense Ratio and Grade

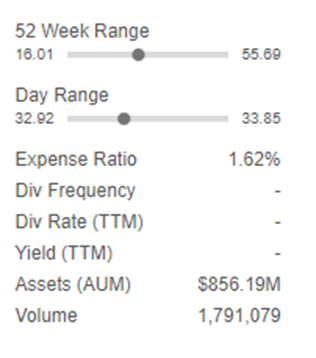

The Fund charges an expense ratio of 1.62%. Yet, it still has over $850 million in Assets Under management (“AUM”).

Seeking Alpha

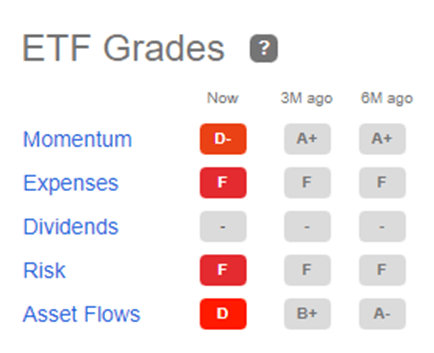

Seeking Alpha has graded the Fund’s expenses as an “F.”

Seeking Alpha

Performance

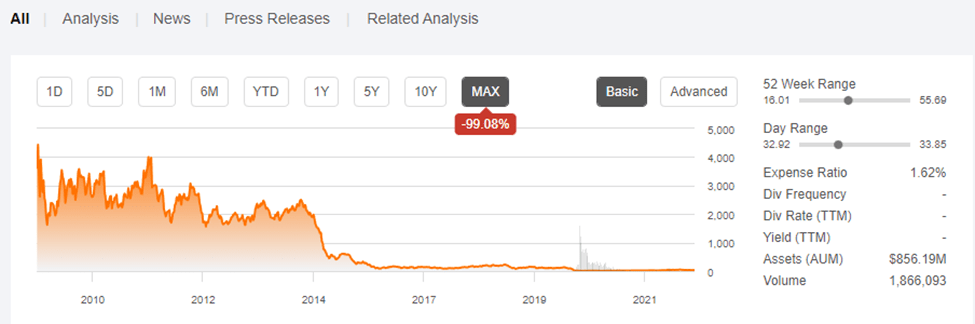

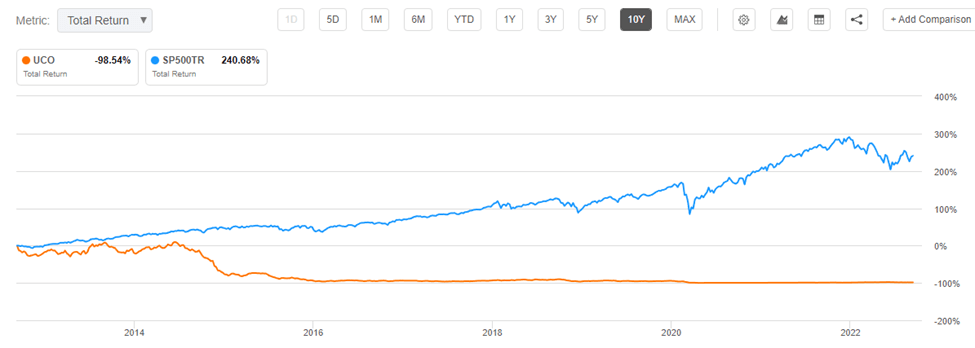

Since inception (11/24/08), the Fund has lost 99.08% of its value.

Seeking Alpha

Over the past 10 years, the Fund has lost -98.54 % of its value. By contrast, the S&P 500 Index Total Return (SP500TR) has gained 240.68 %.

Seeking Alpha

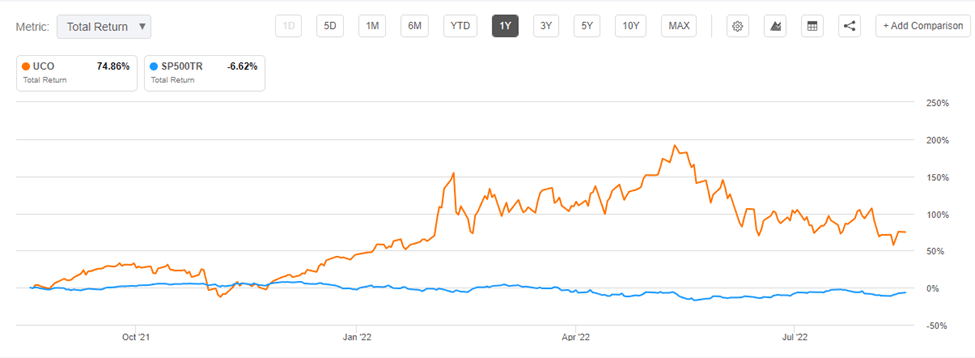

However, over the past year, the Fund has gained +74.88%. That compares to a loss of 6.62% in SP500TR.

Seeking Alpha

Comparison to BRS Crude Oil Trading Results

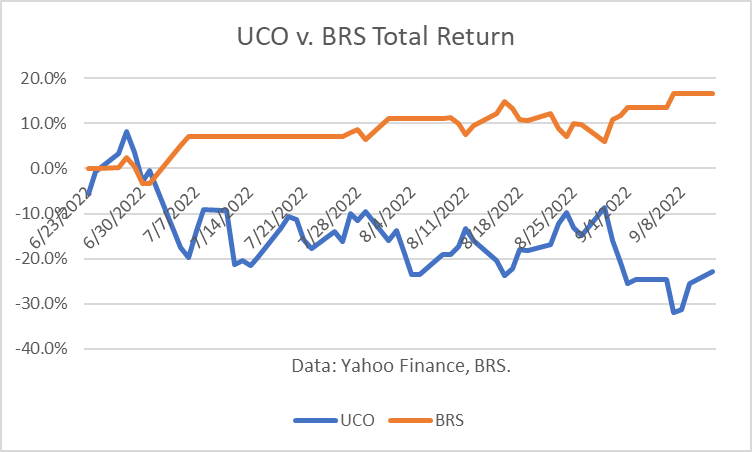

I commenced trading an energy futures portfolio as of June 23, 2022, consisting of NYMEX WTI crude, RBOB Gasoline, Heating Oil and Natural Gas. I post the daily positions and track record on my Seeking Alpha Marketplace service, Boslego Risk Services (“BRS”).

My algorithmic trading (AT) strategy is based on behavioral finance theory and, more specifically, an article written by Nobel economics laureate (2013), Robert J. Shiller. In his paper, “From Efficient Markets Theory to Behavioral Finance,” Shiller discusses the failure of the efficient markets’ theory to explain stock market prices and the “blooming of behavioral finance.” He proved that stock market prices exhibited “excessive volatility” from what would be expected, if market prices behaved according to the efficient markets’ theory.

For a more in-depth discussion, please see my article, DBO: An ETF For Oil Trading. My real-time results through September 12, 2022, for crude oil trading only, were up 16.5%, whereas UCO lost 22.9% over the same period.

Yahoo Finance data, BRS.

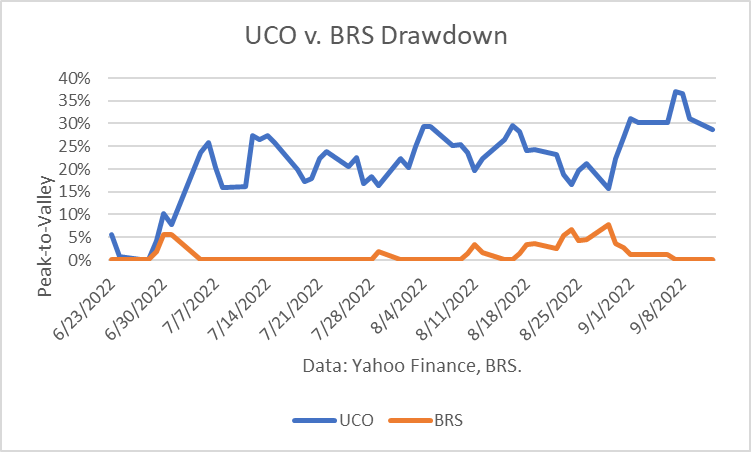

The Maximum Drawdown (“MD”) for the BRS crude strategy was 8%. The MD for UCO over those same days was 37%.

Yahoo Finance data, BRS.

Outlook

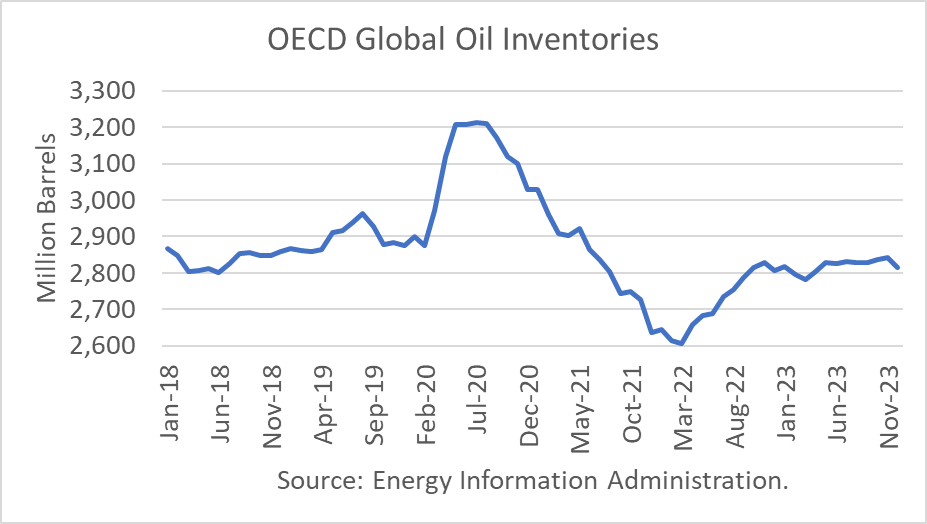

The Energy Information Administration (“EIA”) released its Short-Term Energy Outlook for September, and it shows that OECD oil inventories likely peaked at 3.212 billion in July 2020. In August 2022, it estimated stocks rose by 18 million barrels to end at 2.756 billion, 59 million barrels lower than a year ago.

The EIA estimated global oil production at 101.26 million barrels per day (mmbd) for August, compared to global oil consumption of 99.4 mmbd. That implies an oversupply of 1.86 mmb/d, or 58 million barrels for the month. Given the increase in OECD stocks of 18 million barrels, non-OECD stocks are implied to have decreased by 40 million barrels.

For 2022, OECD inventories are now projected to build by 167 million barrels to 2.808 billion. For 2023, it forecasts that stocks will build by another 7 million barrels to end the year at 2.815 billion.

EIA

On March 31st, the White House announced that the U.S. will release one million barrels of oil per day over the next six months, a total of 180 million barrels, the largest-ever Strategic Petroleum Reserve (“SPR”) release. Since then, approximately 122 million barrels have been released, the SPR’s lowest level since October 1984. Energy Secretary Jennifer Granholm said that the Biden Administration is evaluating further releases after the current program ends in October.

On April 1st, the International Energy Agency announced that a total of 240 million barrels would be released from the group, adding to the 180 million barrel U.S. commitment.

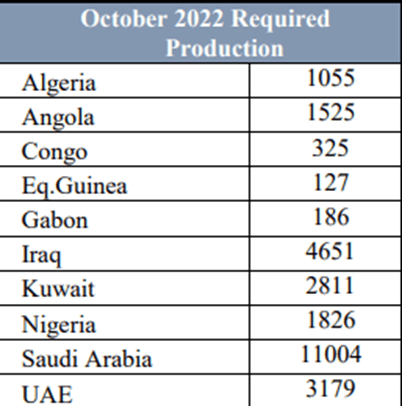

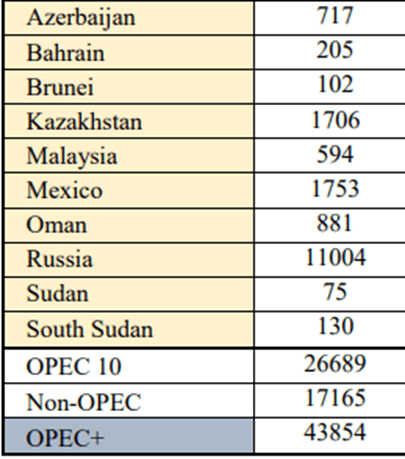

OPEC met on September 5th, 2022. The Ministers decided to:

Reaffirm the decision of the 10th OPEC and non-OPEC Ministerial Meeting on 12 April 2020 and further endorsed in subsequent meetings including the 19th OPEC and non-OPEC Ministerial Meeting on 18 July 2021.

Revert to the production level of August 2022 for OPEC and non-OPEC Participating Countries for the month of October 2022 as per the attached table, noting that the upward adjustment of 0.1 mb/d to the production level was only intended for the month of September 2022.

Request the Chairman to consider calling for an OPEC and non-OPEC Ministerial Meeting anytime to address market developments, if necessary.

Reiterate the critical importance of adhering to full conformity and to the compensation mechanism. Compensation plans should be submitted in accordance with the statement of the 15th OPEC and non-OPEC Ministerial Meeting.

Hold the 33rd OPEC and non-OPEC Ministerial Meeting on 5 October 2022.

OPEC

OPEC

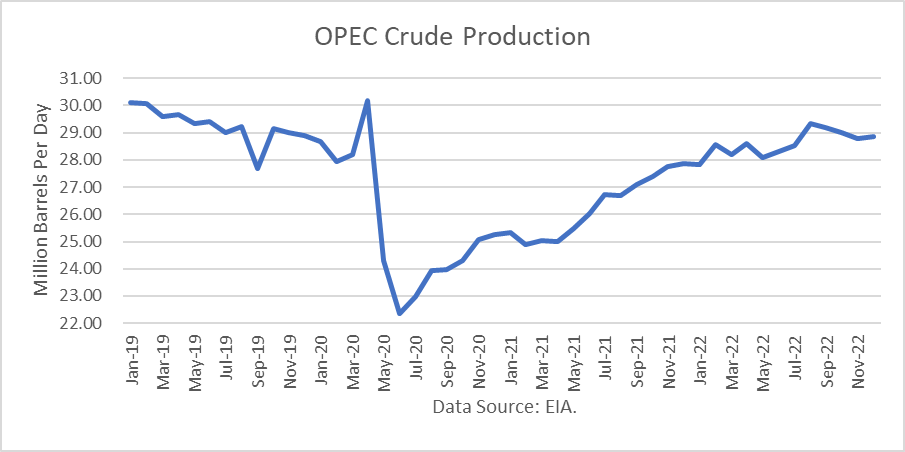

Presumably, the EIA forecast incorporates the OPEC+ plan to increase production. The EIA’s storage projections are based on OPEC crude production as depicted below.

EIA

Oil Price Implications

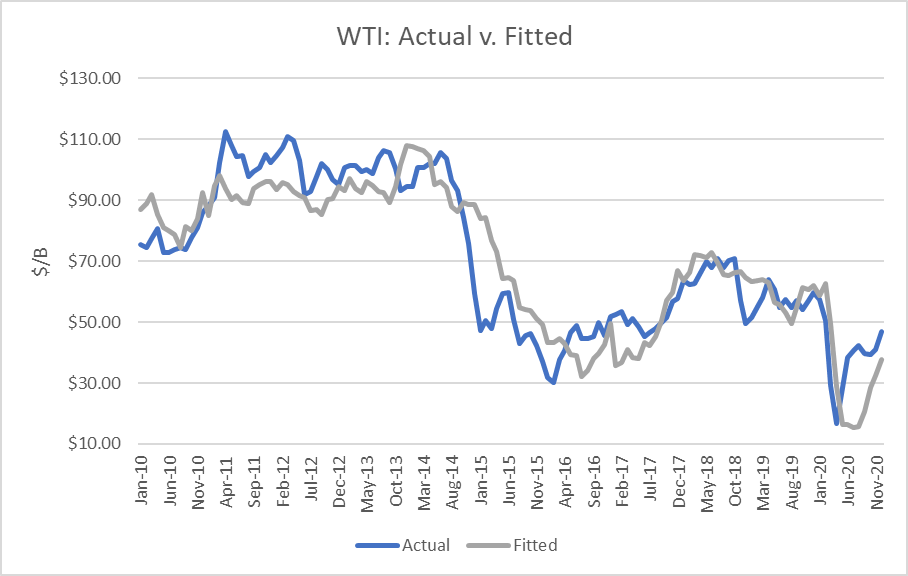

I updated my linear regression between OECD oil inventories and WTI crude oil prices for the period 2010 through 2020. As expected, there are periods where the price deviates greatly from the regression model. But overall, the model provides a reasonably high r-square result of 82 percent.

BRS, NYMEX

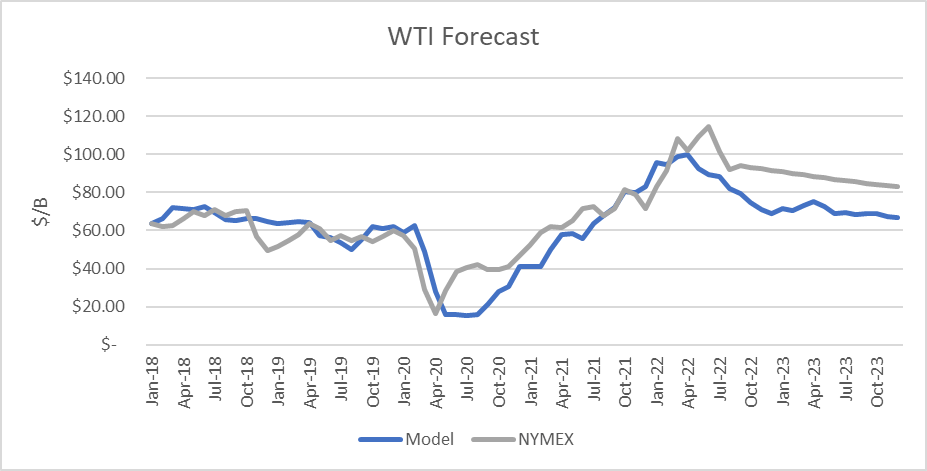

I used the model to assess WTI oil prices for the EIA forecast period through 2022 and 2023 and compared the regression equation forecast to actual NYMEX futures prices as of September 12th and the EIA’s STEO price forecast in September. The result is that NYMEX oil futures prices are presently overpriced through December 2023, as depicted below.

NYMEX, BRS.

Due to the 99%+ loss since inception, UCO is clearly not attractive as a long-term investment. However, in the short term, it may be used effectively as an oil trading tool by sophisticated traders.

Given my projections, I view oil futures prices as overvalued. Therefore, I would not purchase UCO, except for a short-term trade. However, I prefer to trade oil futures contracts themselves because they do not have an expense ratio.

Finally, ProSharess advises:

Prospective investors are strongly urged to consult their own tax advisors and counsel with respect to the possible tax consequences to them of an investment in the shares of a fund; such tax consequences may differ in respect of different investors.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment