itchySan

Trex (NYSE:TREX) performed remarkably well in the second quarter, but gave very disappointing guidance for the second half of the year, which sent shares tumbling.

In Q2 2022 continued demand for outdoor living products drove 24% top line growth even against a difficult comparison with last year’s robust performance. This excellent revenue growth fueled a 49% increase in diluted earnings per share to $0.79. Part of the growth experienced was driven by pricing actions taken in 2021 and 2022, however there was also higher volume.

Unfortunately for the company, towards the end of June it experienced a sudden reduction in demand from distribution partners, due to concerns over a potential easing in consumer demand as a result of rising interest rates, declining consumer sentiment and expectations of a general slowing in the economy. Therefore the company expects its channel partners to meet demand partially through inventory draw-down, rather than reordering product and maintaining current inventories. Trex believes the current draw-down will likely impact the next 2 quarters and will be meaningful in nature.

Trex sounded confident that it can mitigate some of this softness by taking market share, and that it is well positioned to face the difficult environment. We particularly liked this quote from CEO Bryan Fairbanks during the earnings call:

With our brand strength and market-leading position, additional capacity and expanded product lines, we view the current market as an ideal opportunity to accelerate and expand our market share in the composite category, convert more wood decks to Trex decks and strengthen our distribution and retail partnerships.

Trex Q2 2022 Earnings Results

Second quarter net sales increased 24% to $386 million, driven by 25% growth in net sales at Trex Residential to $374 million. The increase in Trex Residential net sales was primarily due to a 20% increase in average price per unit, a mid-single-digit growth in volume as well as channel inventory fill. Trex Commercial contributed $12 million to sales during the quarter. Consolidated gross margin of 40.7% expanded 270 basis points year-over-year driven primarily by price realization at Trex Residential, increased capacity utilization and a continuing focus on cost reduction measures, offset by continued inflationary pressures on raw materials, labor and transportation.

Financials

Gross margins for Trex Residential and Trex Commercial were 41.7% and 12.6%, respectively, compared to 38.7% and 21.6% in the second quarter of 2021. SG&A expenses of $40 million decreased 160 basis points to 10.2% as a percentage of net sales compared to 11.8% in the 2021 quarter as a result of a reduction in accrued incentives and improved operating leverage, driven by double-digit revenue growth.

Net income for the 2022 second quarter was $89 million or $0.79 per diluted share, representing increases of 45% and 49% respectively, from net income of $61 million or $0.53 per diluted share in the year ago quarter. Earnings per diluted share grew faster than net income thanks to the significant share repurchases the company made. The company repurchased another 2.8 million shares of its common stock during the quarter. It also commented that it expects to continue to be a buyer of Trex shares given their strong cash flow generation, confidence in their long-term growth prospects, and their view that Trex shares represent a compelling value.

Trex Balance Sheet

Fortunately, the company is entering this period of economic uncertainty with a strong balance sheet. As of the end of the second quarter, the company had no debt on the books, giving them tremendous flexibility to do share repurchases, as well investing in the brand, R&D, and potentially M&A.

Guidance

The big disappointment in the quarterly report came with the guidance, which the company provided for the next two quarters. Trex anticipates third quarter consolidated net sales will be in the range of $185 million to $195 million, and fourth quarter consolidated net sales will be $180 million to $190 million. In Q3, the company expects EBITDA margins in the range from 16% to 18%. And in Q4, it expects EBITDA margins in the range of 22% to 25%. EBITDA margins should improve sequentially from Q3 to Q4, as the company receives the full benefit from its cost-reduction initiatives.

The company believes the current inventory draw-down will be substantially completed by year-end when the channel will again be operating at very low inventory levels.

TREX Stock Valuation

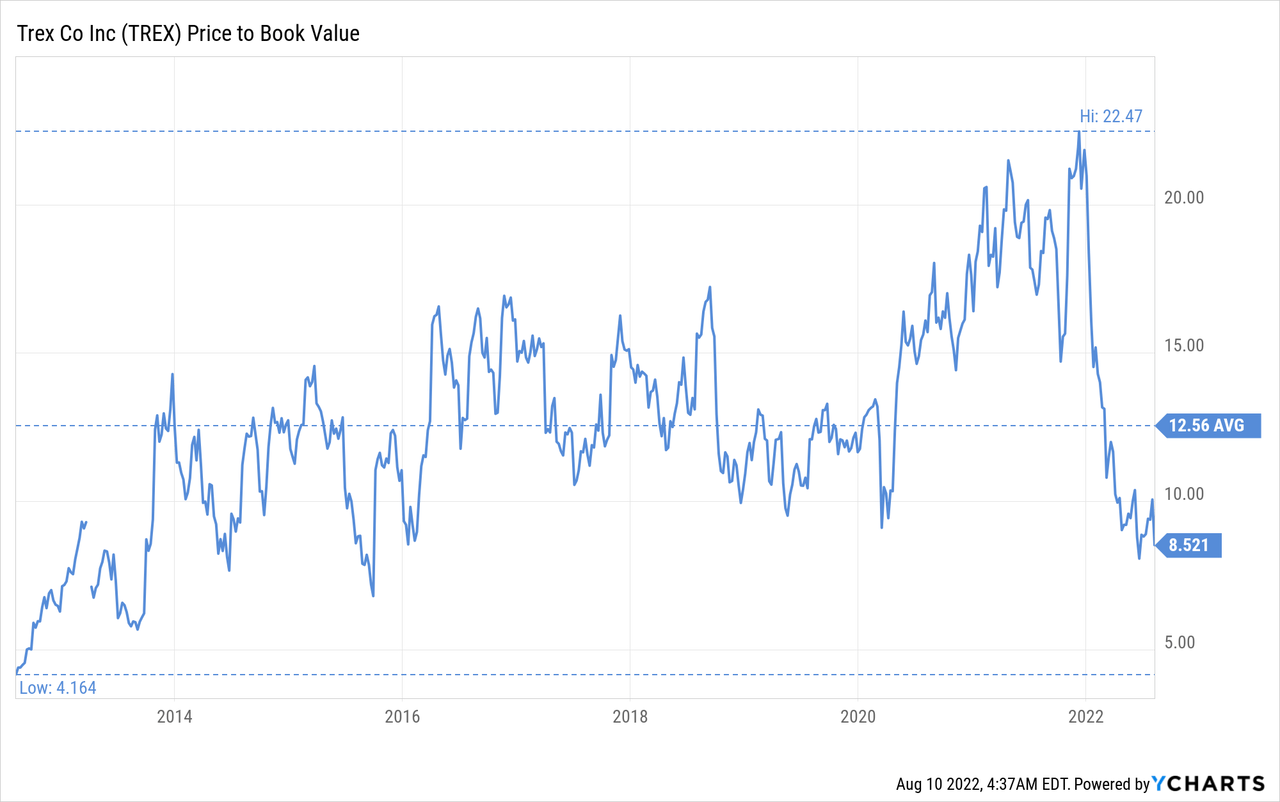

Despite the disappointing guidance, we believe shares to be significantly undervalued. The company appears to agree given their significant share repurchases that they are doing. Looking at some valuation multiples, we can see that they are below historical averages by a meaningful amount. For instance, price/book value is about a third below its ten year average, and had is actually lower than it was during the COVID crash of 2020.

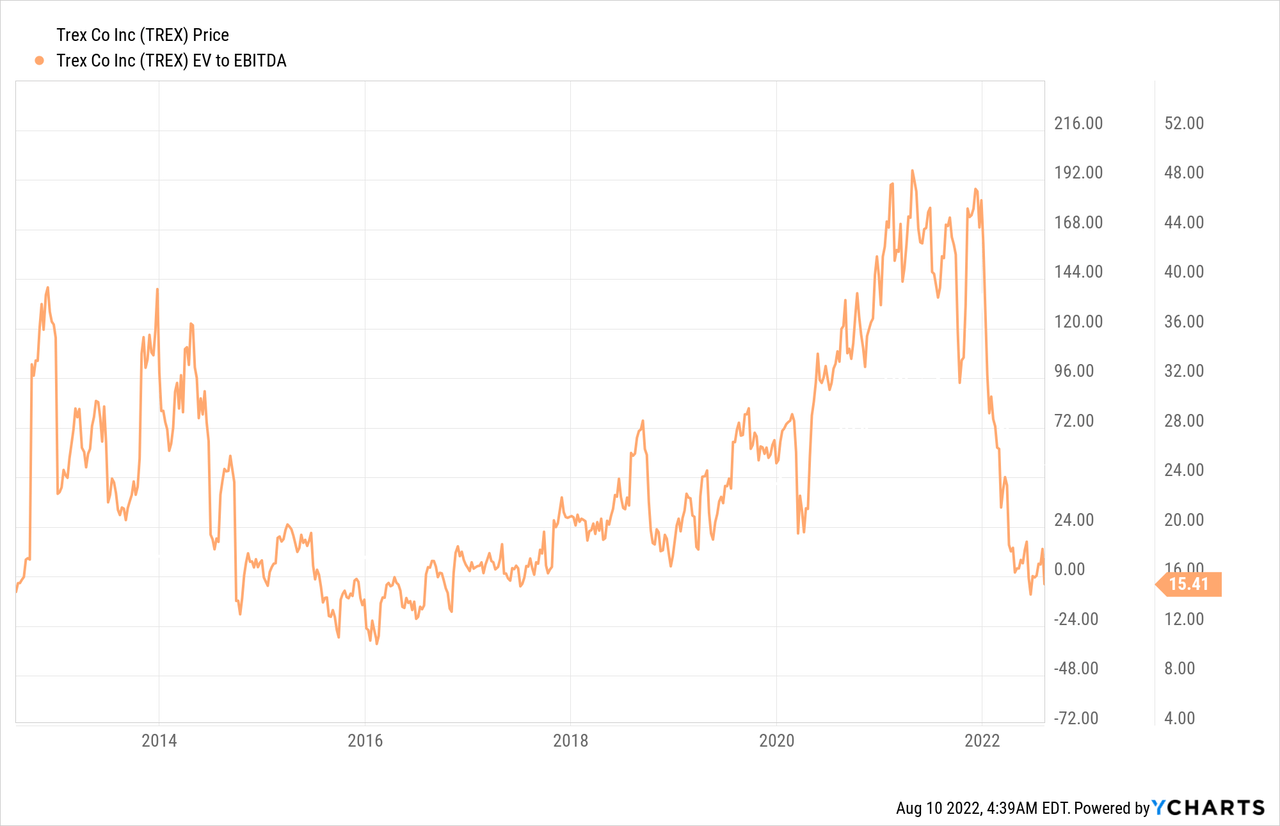

Similarly, EV/EBITDA is below the COVID crash of 2020, and not that far from its ten year lows of close to 12x. We think shares were overvalued when they were trading with an EV/EBITDA of more than 40x, but given the quality of the company, the lack of long-term debt, and the growth tailwinds the company has, we believe that 15x is cheap for the company, and certainly low compared to its historical valuation.

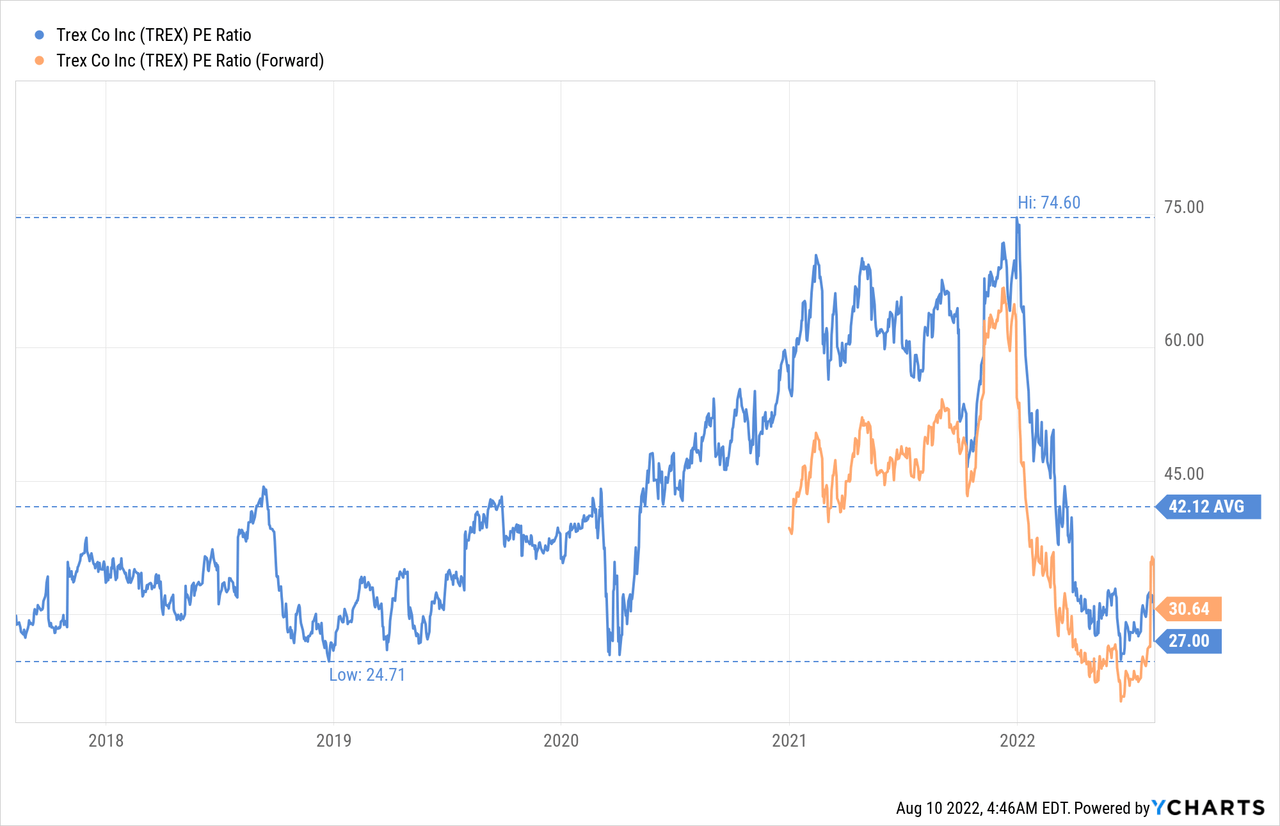

The price/earnings ratio is also close to its ten year low of ~24x, currently at ~27x. The forward price/earnings ratio is actually higher as analysts seem to have started updating their models to account for the weak guidance provided for the rest of the year.

Risks

The main risk we currently see with Trex is that is appears to be entering a period of soft demand, and things could get worse before they get better again. We believe the company is strong enough to survive the downturn, and might even manage to gain market share, but the risks with the company have certainly increased given the weak demand picture.

Conclusion

Guidance for the next two quarters was extremely weak, and we believe that the market reaction of a tumbling share price was appropriate. That said, we continue to see a lot of long-term value, with shares significantly undervalued compared to their historical averages. We believe risks for the company have increased, but given its solid balance sheet without long-term debt, we are confident that the company will be a survivor and might even manage to take market share during the downturn.

Be the first to comment