The eurozone problem

It’s entirely true that it’s just great to have the same money in use over a trading area – it definitely increases trade across that area. This is known as the “Rose Effect”. So, super, except having the same money across an economic area means that monetary policy must be the same across that area. This is by definition, you can’t have different base interest rates in the same currency across a free trading area – just not possible.

These two effects balance each other out in their desirability at some point. Generally, such balances in economics are called the “optimal” point. The benefits of the one effect are balanced by the ill effects of the other. A standard analysis of the eurozone tells us that it’s much, much too large to be an optimal currency area.

Now, I agree, I’m extreme on this point. But I insist that this means that we’re just not going to see decent economic performance across the area. This is because I’m a fundamentalist. Sure, various bits of Keynesian pump priming and all that, other clever policies, can work. But they work at the margin and they only work if the underlying basics of the economy are correct.

That is, nothing that is superimposed upon incorrect microeconomic nor monetary policies is going to work. I have my doubts about the continental system of regulation – that microeconomics – but that’s another matter. An incorrect monetary system is going to mean that the eurozone economy just isn’t going to work. By that I mean growth is always going to be well below potential.

For us as investors that means the entire eurozone is simply a sector to avoid. Sure, of course, there will be specific interesting stocks, situations and companies. But in terms of our allocation across economies and world regions, we should be underweight to absent from the eurozone markets. Sorry, I just insist that we’ve got decades yet to come of miserably low growth.

CPI

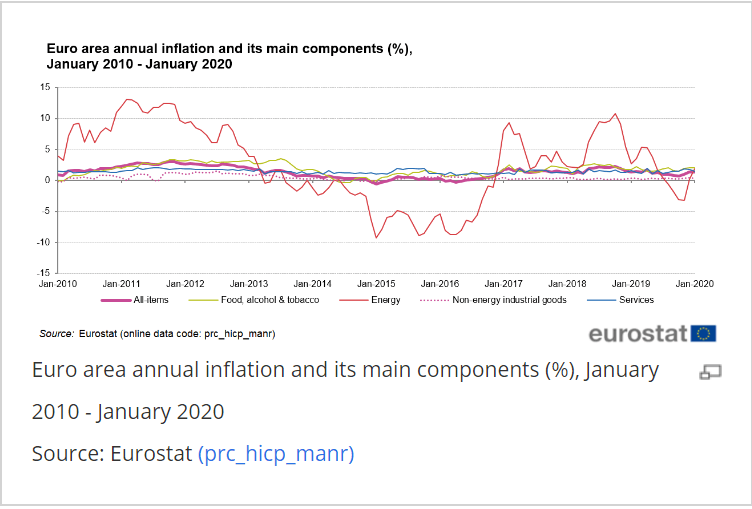

As an example of this problem look at the latest CPI figures in the eurozone:

Final numbers confirmed that euro zone inflation rose to 1.4% y/y in January from 1.3% in December.

Or:

(Eurozone CPI from EU Commission)

{kind=link}

The ECB target for inflation is 2%. So, not too shabby, except it’s, as always, core inflation that matters:

The core rate fell sharply to 1.1% y/y from 1.3%.

So, the ECB needs to be doing something to raise that inflation rate.

Constituent countries

We’re seeing much the same story in France:

France’s EU-harmonized inflation rate increased to 1.7% y/y in January after hitting 1.6% in December. In month-ago terms, however, prices fell 0.5% after rising 0.5% in the previous month. National consumer prices held steady at 1.5% y/y. The core rate decelerated slightly to 1% y/y,

Core inflation, net of energy and unprocessed food, ticked up to 0.8% y/y from 0.5% previously. But the upward trend in core inflation over the past few months is mostly explained by more volatile components, notably transport services inflation, which are highly exposed to fluctuations in demand.

OK, so policy choices

The ECB might have some policies they can use. Except, well, no, not really. Interest rates, the base rate, are already negative – 0.4% in fact. There’s little to no room to take them yet more negative. At some point, large depositors will abandon the banking system and move into cash. Yes, of course, it’s absurd to think that someone will hire a vault and put tens of millions into it, but that will happen at some price. At which point the money supply collapses of course. Exactly the opposite of what anyone actually desires.

They could do more QE. Except there’s a political limit here. Germany has insisted that purchases of government bonds must be apportioned. Not by the outstanding amount, but by the relative sizes of the various economies. So, there’re vast amounts of Italian govt bonds around, but they can’t be bought unless a greater amount of German bonds are. And Bunds are in rather short supply – the country is running a budget surplus after all. So, it’s not possible to mop up those Banco di Italia issues because Bundesbank ones to balance them don’t exist.

There’s always fiscal policy of course, but there is no eurozone oversight of fiscal policy – that is reserved to the nation states. There’s no point in any one of them trying reflation on their own as the effects would just spiral off into the other linked economies.

Note that this problem about fiscal policy applies in good times as well as bad, one other reason I think the eurozone is going to underperform for decades.

So, what can they do?

The other idea is to try lowering the value of the currency. Of course, individual countries can’t do that – something that would solve much of the problem if Italy and a couple of others could, or if Germany could raise theirs. The ECB could try lowering the value of the euro of course. But then that’s what they’ve been trying to do. They’ve been quite clear that they expect the major effect of QE to be through the external value of the euro.

And, you know, it’s not working. Too much of eurozone trade is internal meaning that the external value of the currency isn’t important enough to jump start the economy of 400 million people.

Putting it together

Sure, I’m gloomy about this. But then I have been since the idea was first mooted in the mid-1990s. The entire construction has a flaw at its heart – it’s not an optimal currency area and therefore should be trying to be a single currency area. The problems predicted are exactly those that are happening. An impossibility to use monetary policy to enliven a moribund economy.

This is compounded by the political considerations meaning that no policy tools are left to deal with matters either. The internal constraints mean that the ECB is at the real meaning of the zero lower bound. Even though interest rates are now negative, they can’t make monetary policy loose enough to juice the economy. This is when fiscal policy really is the only tool left. Yet there is no central fiscal policy.

Those who believe that this will lead to the creation of a joint and central fiscal policy aren’t paying attention to national politics. There is simply no way at all that Germany will allow Brussels to dispose of the 15 to 20% of GDP that would be necessary to have that central fiscal policy.

So, I don’t think the eurozone is going to work.

My view

Sure and I don’t think that Italy is about to leave the eurozone – much as I think it should and much as I was arguing Greece should have done already. I think the problem is different. This system is never going to work. But they’re going to stumble along with it for years yet. This means that the eurozone is going to continue to underperform for years yet.

Yes, of course the business cycle still exists. There will be times when growth rises in the eurozone. But those bursts will be lower, rarer and shorter than they would be without the euro. They’ll also be lower, rarer and shorter than those places which haven’t hamstrung themselves by adopting an entirely inappropriate monetary system. The slumps will be longer, lower and more common by that same measurement and for the same reason.

I simply expect years, decades, of economic underperformance from the eurozone.

The investor view

There are good reasons why we might still invest in the eurozone. If we’re resident inside it for example – having at least some investment in the local currency you live in is a good idea. There will also always be special situations that make sense.

But the general macroeconomic oversight – in my prediction – is that this is a corner of the world to be avoiding. As with, say, Argentina and such places that regularly disappoint – as Argentina has for a century now – put money elsewhere.

The reason why this could all be wrong is that the EU will get its economic act together and either abandon the euro itself or integrate into the one single fiscal policy and treasury. Myself I think the odds of either are close to zero but others might differ.

The eurozone is locked into an appallingly bad economic policy straitjacket. Avoid.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment