Daniel Berehulak/Getty Images News

Tata Motors Limited’s (NYSE:TTM) last 15-year performance has been subdued as compared to other automobile companies globally. There have been various reasons for the same, with the acquisition of non-profitable business of JLR during 2008-09 being the primary one. In addition, the launch of a lower ticket size Nano car for India also didn’t take off as expected.

However, the tide is turning now, and the company is aggressively gaining market share in domestic markets. Three years back, the ratio of Tata Motors cars in metro cities would have been one out of fifteen, but now at least one five cars out of fifteen are of Tata!

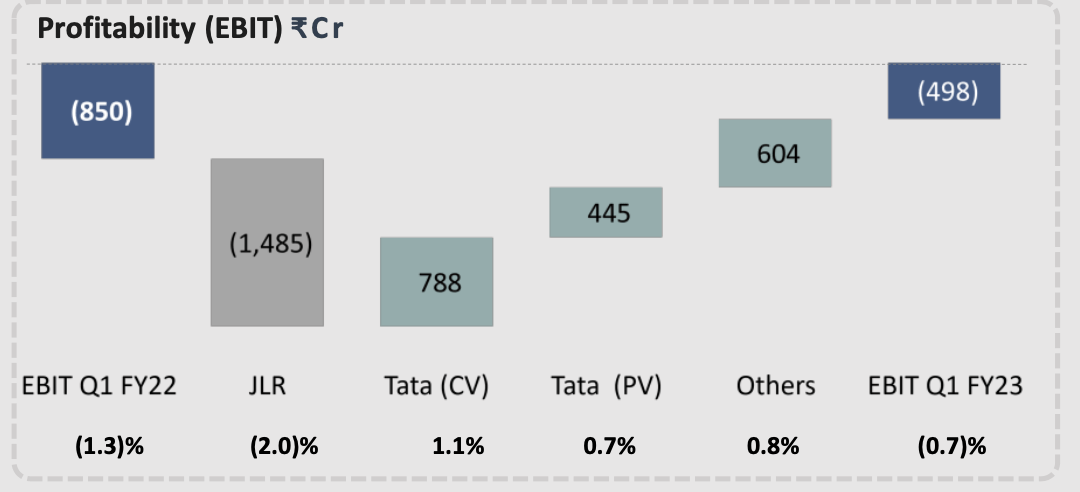

Q1FY23 numbers confirm the trend, as most of the JLR’s loss is getting now absorbed by the company’s other domestic launches across the CV and PV space. JLR’s loss this quarter was also affected by the partial lockdowns in China and reduced supply levels, which is likely going to improve going forward (according to the management)

TTM’s EBIT to improve further on rising domestic demand (Investor Presentation (Q1FY23))

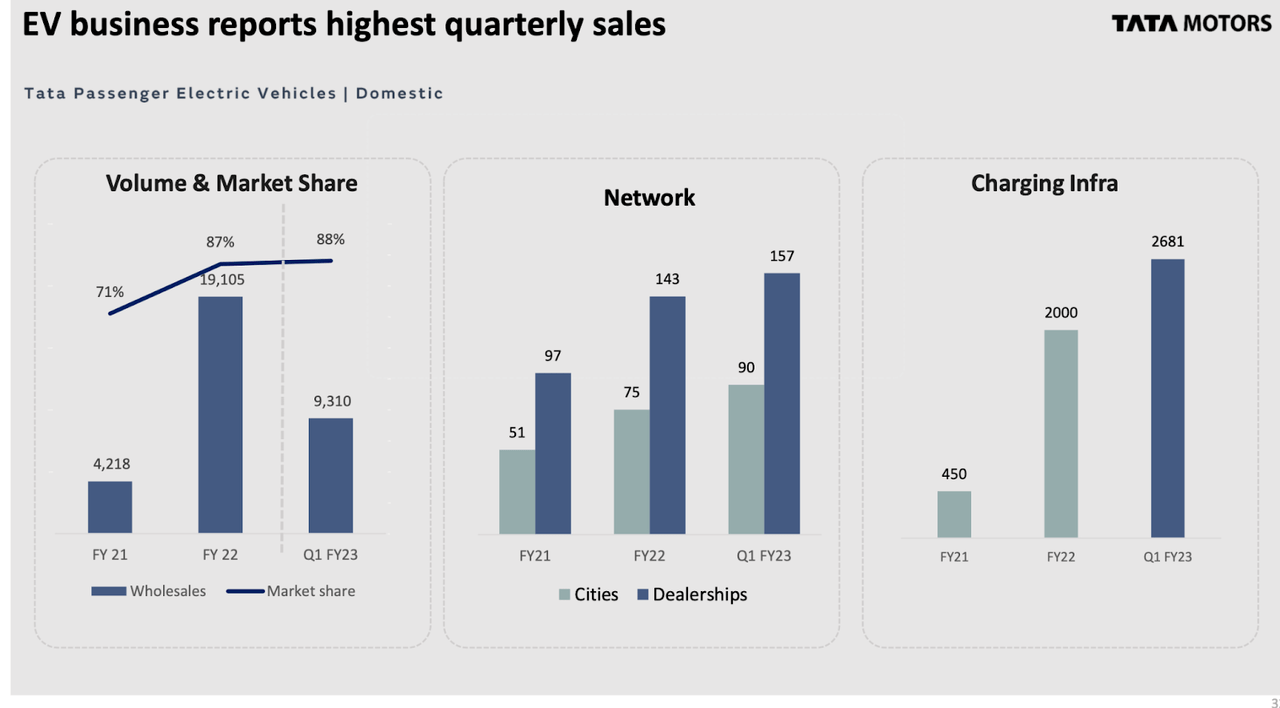

The company currently enjoys one of the highest market shares in electric vehicles across Passenger Vehicles segment (chart below) indicating that it is the preferred choice by customers. Tata Motors is one of the very few companies in the world which enjoys an in-house ability to leverage one of the best technologies (operational, efficiency, AI and VR), as it has two sister technology companies – TCS and Tata Elxsi to support the company’s vision. So it can easily surpass its peers in terms of technological excellence in future. The latest acquisition of Tata in air space (Air India) will only lead to technologies and economies of scale in the future across its automobile products as well. The company’s expansion of its network across cities and dealerships clearly shows the demand for its products is on a rising trend (2nd graph in chart below)

EV market share stands at 88% in Q1FY23 (Investor Presentation)

The company’s vision is to achieve positive free cash flow (“FCF”) of (£1b) by year-end through price hikes and ramp up of products. TTM aims to become zero net debt company by FY24 and double its EBIT’s margin to double digits by FY26 which is a positive catalyst.

As mentioned in my previous articles also, the auto sector in itself is poised for a growth spurt led by easing of chips supply, technological transition to electric vehicles (“EVs”), unavoidable replacement cycle which got delayed due to covid-19, and the government’s push for EV. The demand from the growing millennial segment which forms 30% of the population and who are the major wealth inheritors will only add to the consumption story.

A long term compounding stock investment is when you spot the right growth triggers getting partially reflected in financial and operational performance. TTM has started to show few green shoots and I believe this can be a good long-term bet. The management’s vision and efforts have started paying off and the company is expanding its network to cater to the increasing demand. This gives enough comfort to take a calculated risk-adjusted investment in this stock. Most of the brokerage houses are also positive on the company’s long term prospects.

Thus, I would suggest to accumulate on dips and hold for a ten year period for long term compounding returns. There might be macro risks from increasing interest rates or any other factor and thus would recommend to gauge the same.

Be the first to comment