DNY59

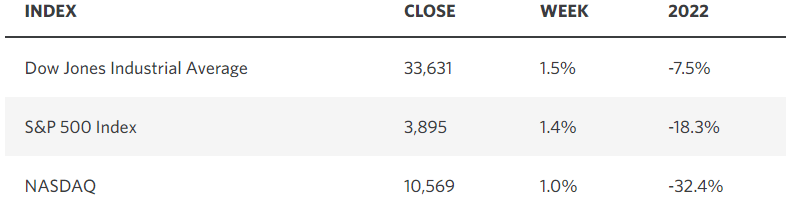

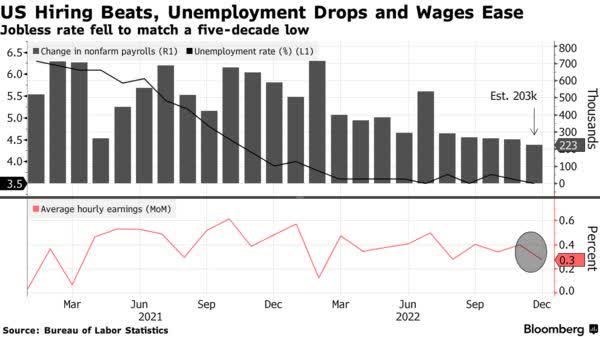

Santa Claus showed up after all, as the last five trading days of 2022 and the first two of the new year produced a positive return, which has historically boded well for the month of January and the rest of the year. That did not look to be the case on Thursday of last week when a robust payroll number of 235,000 from ADP, along with a drop in unemployment claims, sent the stock market in to a tailspin over concerns that a hot labor market would force the Fed to press harder on the brakes of the economy. Sentiment reversed course on Friday when the Bureau of Labor Statistics reported that nearly the same number of jobs were created in December at 223,000, and that the unemployment rate fell to 3.5%, resulting in a huge stock market rally to close out the first week of the new year.

Edward Jones

The difference on Friday was that wage growth declined more than expected, which is the Fed’s primary concern as it relates to inflation. I have consistently argued that we can see wage growth ease and the rate of inflation decline without putting millions out of work and slowing economic growth to the extent that it results in a recession. I think the economy is still on track for a soft landing, and we moved a step closer with Friday’s payroll report.

Bloomberg

Despite the robust jobs number, wage growth fell to a 16-month low of 4.6%, and the length of the workweek shortened for a second month in a row to show a further softening in labor market conditions.

Economy Policy Institute

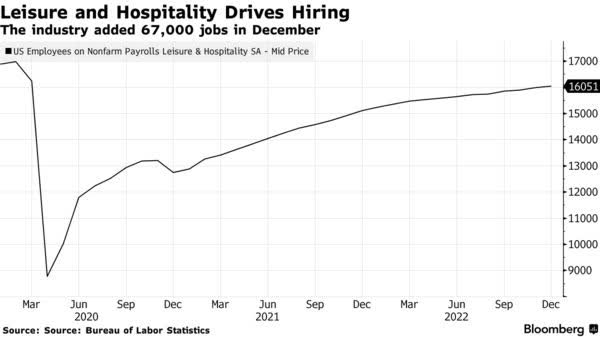

This is partly due to lower-wage positions in the leisure and hospitality industry driving employment growth, while sectors like technology, finance, and manufacturing shed jobs.

Bloomberg

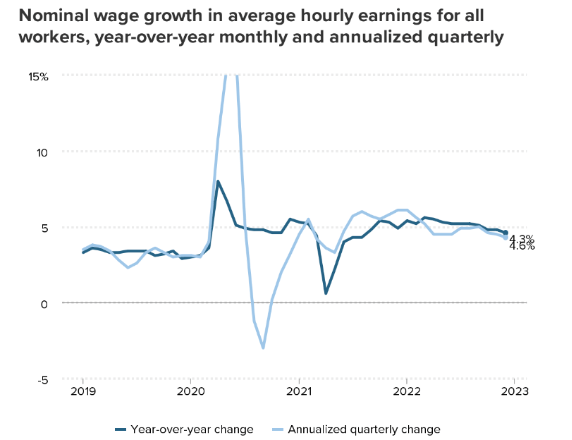

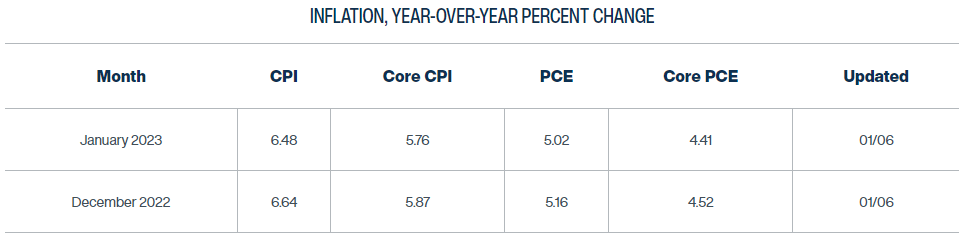

This is not a normal economic cycle, which I suspect the Fed appreciates but only behind closed doors, as members are obsessed with managing expectations. There have been mass distortions in economic activity first caused by the pandemic and then by the stimulus that followed, resulting in unprecedented deviations from the mean in the high-frequency economic data. Three years later we should be nearing normality. The spike in inflation to a 40-year high was largely caused by global shocks. It is often blamed on the surge in excess savings from stimulus and the spike in wage growth, but it is not that black and white. The accumulated savings and labor market strength have helped consumers endure much higher prices over the past two years more so than fuel them. Therefore, as surplus savings shrinks and wage gains fall to a still healthy 3-4%, the rate of inflation should also fall without forcing a significant rise in unemployment. In fact, as savings return to normal levels, the rate of inflation (yellow line below) is likely to fall below the rate of wage growth (blue line below), restoring real-income growth. That would be an extraordinarily smooth landing for the economy. It does not require a recession, and financial conditions are already tight enough to get us there.

Bloomberg

I expect we will see another decline in the Consumer Price Index for December when it is reported on Thursday, and the Personal Consumption Expenditures price index (PCE) will come later in the month just before the Fed’s next meeting. The Cleveland Fed’s model is forecasting a decline to 4.4% for the core PCE.

Cleveland Fed

The ISM Purchasing Managers Index (PMI) for the service sector fell sharply in December to 49.6, which is just below the 50 level that marks the line of demarcation between growth and contraction. It ends a 30-month streak of growth. I would be more concerned, but 11 of the 17 industries still reported growth. The good news is that supplier delivery times are improving, and pricing pressures are easing further. Still, this does suggest that we will see much slower growth in the first quarter of this year.

TradingEconomics

With housing and manufacturing seeing a sharp deceleration in activity, it is key that consumer spending continues to grow, as it is 70% of the economy’s horsepower. The softening of the labor market combined with much weaker PMIs for manufacturing and service sectors should be signals enough that the Fed end its rate-hike campaign, but it will likely raise by another 25 basis points at the end of the month, as the market is expecting. Regardless, the stock market is already pricing in this development and last week’s strong performance suggests investors are looking past the peak in the Fed funds rate. On to earnings season.

Be the first to comment