S&P 500, HANG SENG, ASX 200 WEEKLY OUTLOOK:

- Dow Jones, S&P 500 and Nasdaq 100 indexes closed –0.68%, -0.72% and -1.14% respectively

- Russia-Ukraine tensions and worries about an impending Fed rate hike weighecd on market sentiment

- Asia-Pacific markets look set to follow a sourlead. US markets are shut for the Presidents’ Day holiday

Ukraine Crisis, Core PCE, US Earnings – Asia-Pacific Week-Ahead:

Wall Street stocks ended a volatile week with a sour tone as investors weighed escalating geopolitical tensions at the border of Russia and Ukraine. US President Joe Biden warned about an imminent Russian attack after reports showed increased outbreaks of violence and ceasefire violations in the area. He saidon Friday that Russia may attack multiple Ukrainian cities beyond the capital of Kyiv. Gold prices rallied alongside crude oil, both of which are highly sensitive to geopolitical risks. Stocks pulled back alongside Bitcoin, underscoring anti-risk sentiment as the political skies remain far from clear.

Lingering geopolitical unrest and fears about the Fed tightening monetary policy may continue to suppress risk assets in the near term. This Friday’s core PCE price index – the Fed’s key inflation gauge – will be in the spotlight. The reading is expected to hit a fresh four-decade high of 5.1% in January, up from December’s print of 4.9%. An overshooting number may further strengthen the Fed’s hawkish stance and accelerate the expected pace of rate hikes. Against this backdrop, stocks may be put under pressure as their intrinsic value is reduced when future cashflows are discounted at higher baseline rates of return.

On the earnings front, about 84% of the S&P 500 companies have reported results so far, among which 77% have beaten market expectations with an average earnings surprise of 8.5%. The blended earnings growth rate for those companies is 30.9%on–year, marking the fourth straight quarter of earnings growth above 30%, according to Factset. It is worth noting that nearly three quarters of companies have highlighted inflation during their earnings calls, underscoring rising price levels that are having an outsized impact to their margins and operations.

US CPI vs. Fed Target Rate

Source: Bloomberg, DailyFX

APAC markets look set to kick off the week on the back foot following a sour lead from Wall Street. Futures in Japan, Australia, Hong Kong, South Korea, Taiwan, Singapore, India and Indonesia are all poised to open in the red. Those in mainland China, Malaysia and Thailand are in the green. US markets are shut on Monday for the Presidents’ Day holiday, undermining trading activity due to fewer market participants.

Hong Kong’s Hang Seng Index (HSI) plunged late Friday following a regulator’s call for Meituan – China’s largest food delivery platform – to cut fees they charge restaurants. Meituan’s share price plunged 15%, pulling the HSI and the Hang Seng Tech Index (HSTECH) down by 1.9% and 3.2% respectively. This shows that policymakers may not loosen their grip over China’s Big Tech firms any time soon, defying speculation that authorities may ease control over them to cushion the slowing economy.

HSBC and Alibaba will report earnings on 22nd and 24th Feb respectively and may have an outsized impact on HSI and HSTECH indices.

For the week ahead, Tuesday’s US manufacturing PMI as well as Wednesday’s RBNZ rate decision and press conference dominate the economic docket alongside Friday’s US core PCE price index. Find out more from the DailyFX calendar.

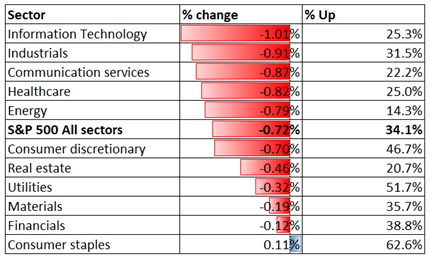

Looking back to Friday’s close, 10 out of 11 S&P 500 sectors ended lower, with 65.9% of the index’s constituents closing in the red. Information technology (-1.01%), industrials (-0.91%) and communication services (-0.87%) were among the worst performers, whereas consumer staples (+0.11%) registered a small gain.

S&P 500 Sector Performance 18-02-2022

Source: Bloomberg, DailyFX

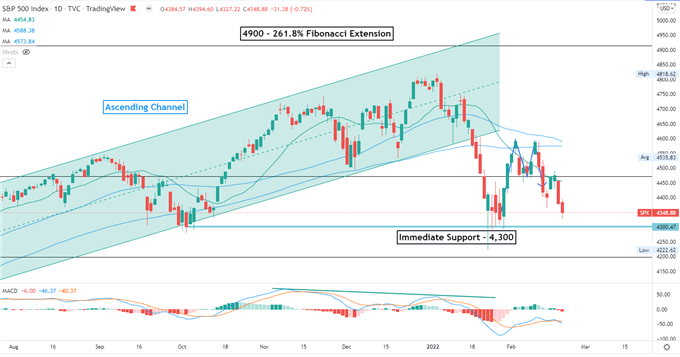

S&P 500 Index Technical Analysis

The S&P 500 index may have entered a meaningful correction after breaching below an “Ascending Channel” as highlighted on the chart below. Prices have likely formed a “Double Top” chart pattern last week, hinting at further downside potential with an eye on 4,300 for support.Breaching below 4,300 will likely expose the next support level of 4,200. The MACD indicator formed a bearish crossover beneath the neutral midpoint, suggesting that selling pressure is prevailing.

S&P 500 Index – Daily Chart

Chart created with TradingView

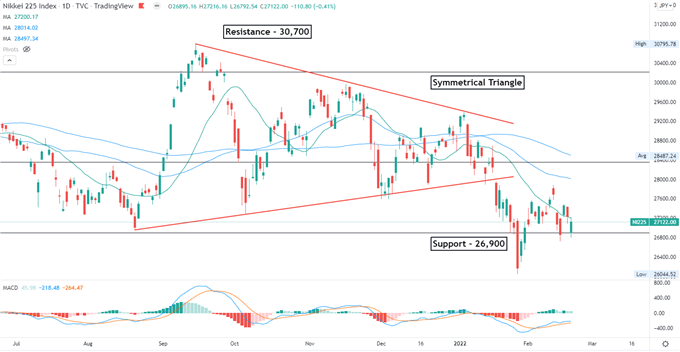

Nikkei 225 Technical Analysis:

The Nikkei 225 index breached below a “Symmetrical Triangle” pattern and thus opened the door for further downside potential. Prices are consolidating near a key support level of 26,900, but the overall trend remains bearish-biased. The lower trendline of the “Symmetrical Triangle” has now become an immediate resistance. The MACD indicator is trending higher beneath the neutral midpoint, suggesting that buying pressure may be building.

Nikkei 225 Index – Daily Chart

Chart created with TradingView

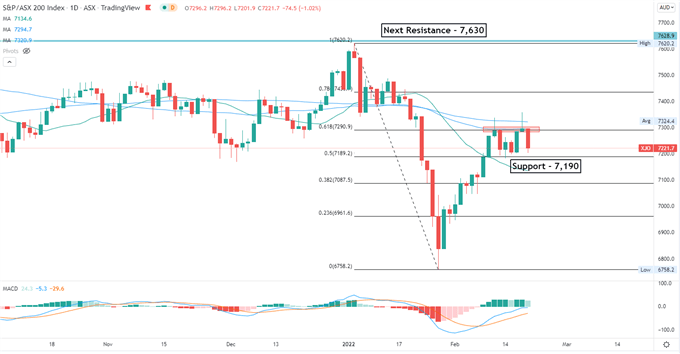

ASX 200 Index Technical Analysis:

The ASX 200 index has rebounded after a meaningful correction in January. Prices are challenging the 61.8% Fibonacci retracement – a key resistance level. Breaching this level will likely intensify buying pressure and open the door for further upside potential with an eye on 7,435. The MACD indicator is flattening beneath the neutral midpoint, suggesting that selling pressure may be building.

ASX 200 Index – Daily Chart

Chart created with TradingView

— Written by Margaret Yang, Strategist for DailyFX.com

To contact Margaret, use the Comments section below or @margaretyjy on Twitter

Be the first to comment