Michael Vi

We’ve been bullish on ServiceNow (NYSE:NOW) in the past, but we believe it is time to move the stock to a sell. Our bearish sentiment on ServiceNow is based on our expectations that macroeconomic headwinds are taking a bite out of subscription revenues as these headwinds persist and companies re-evaluate their spending priorities. We expect ServiceNow to underperform the competition in the near term.

ServiceNow is down nearly 39% over the past year, and we expect more downside ahead. The company provides products using Software-as-a-Service or SaaS cloud computing software for the management of workflows. While we like ServiceNow’s product and believe it operates in an expanding business, projected to grow at a CAGR of 15.9% between 2022-2028, we don’t believe the stock will grow meaningfully in the near term. We’re bearish on ServiceNow as we argue that the stock is still too pricey to invest in during a challenging market for growth stocks. We recommend investors sell the stock at current levels and wait on the sidelines for the macroeconomic headwinds to lift before revisiting entry points in ServiceNow.

Highly reliant on subscription revenue

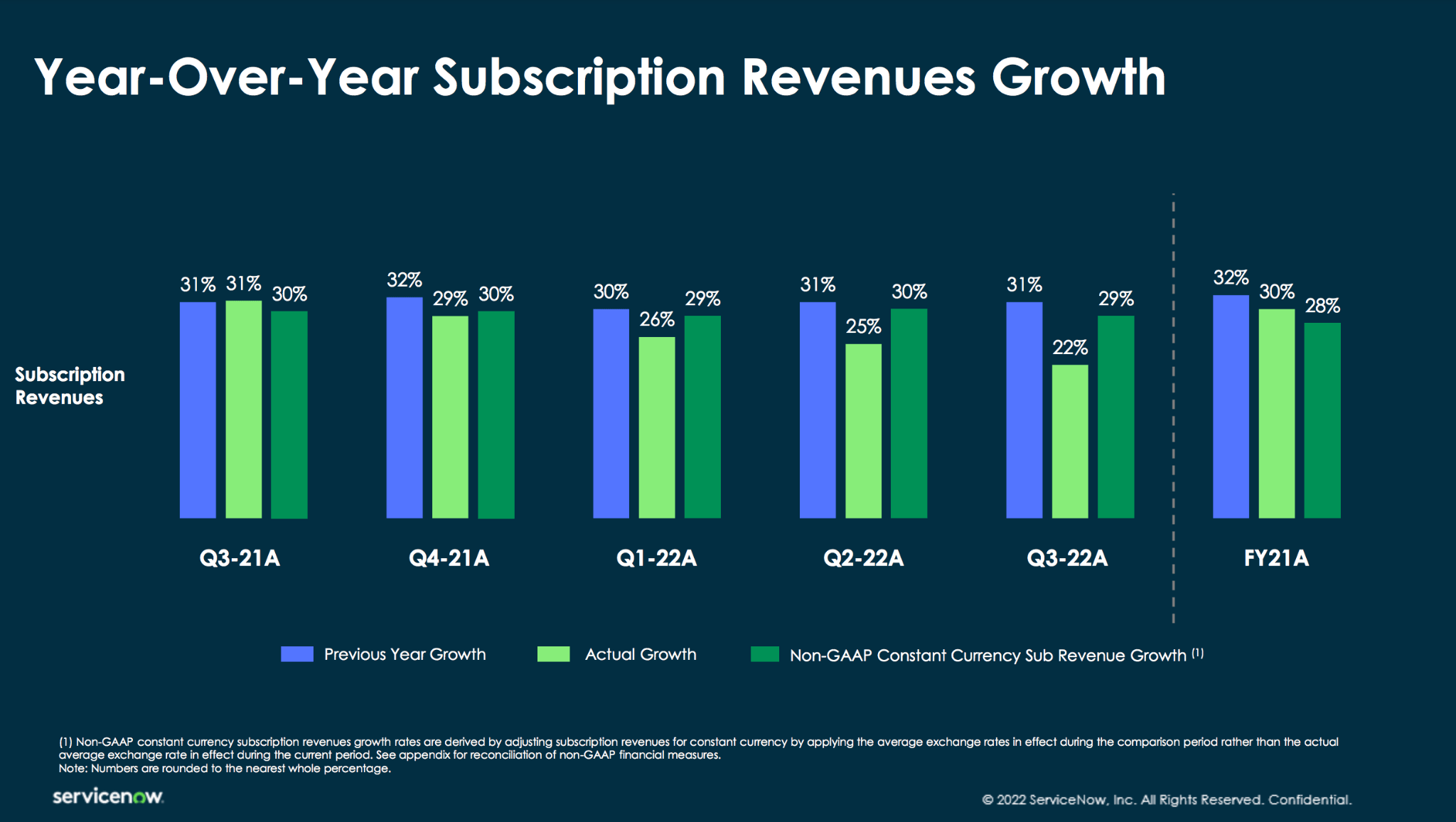

The bulk of ServiceNow’s revenue is derived from subscription revenues, accounting for nearly 95% of total revenue in 3Q22. We believe the actual growth of subscription revenue is slowing down, with actual subscription growth amounting to 22% in 3Q22 compared to 25% in 2Q22 and 31% a year ago in 3Q21. We believe companies looking to digitalize their workflows are not as incentivized as before to allocate significant budgets to cloud computing platforms to aid digital transformation. We believe companies’ hesitance comes from the rough macroeconomic headwinds with inflation at a 40-year high and the fed spiking interest rates in 2022 to a level unprecedented in the past decade. In the near term, we expect less demand for ServiceNow’s offerings compared to 2021 and believe investors should sell the stock as we expect subscription growth to continue to normalize throughout 1H23.

The following graph from ServiceNow’s 3Q22 earnings report outlines the company’s Y/Y subscription revenue growth.

3Q22 Investor Presentation

ServiceNow’s renewal rate in 3Q22 further confirms our concerns about slowing subscription revenue, with the company’s renewal rate down to 98% compared to 99% a quarter prior. While the sequential decline of 1% is not a significant drop, we believe it still highlights the weaker demand for ServiceNow’s offerings under current macroeconomic headwinds.

The following graph outlines ServiceNow’s renewal rate in 3Q22.

3Q22 Investor Presentation

Impact of FX headwinds

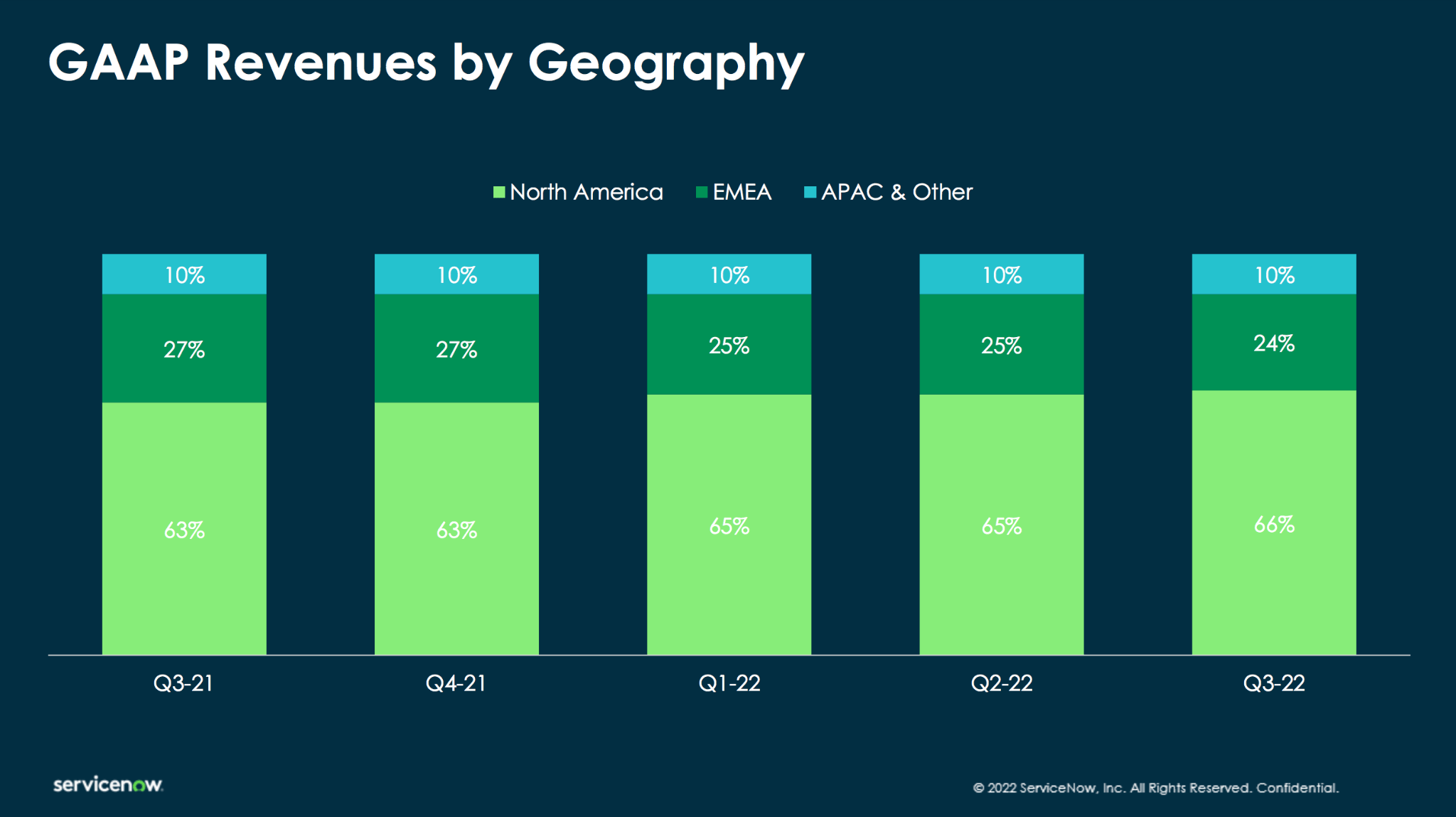

We’re also concerned about the impact of FX headwinds on ServiceNow. In 3Q22, the company reported a currency impact of -650bps on subscription revenues. The FX headwinds are expected to persist to 4Q22, with guidance estimating another -600bps impact. We believe the strength of the U.S. dollar may slightly hold back the company’s growth at the moment, specifically since ServiceNow derives the bulk of its revenue from North America, accounting for 66% of total revenue in 3Q22.

The following graph outlines ServiceNow’s revenue by geography over the past several quarters.

3Q22 earnings Investor Presentation

Oracle vs. ServiceNow

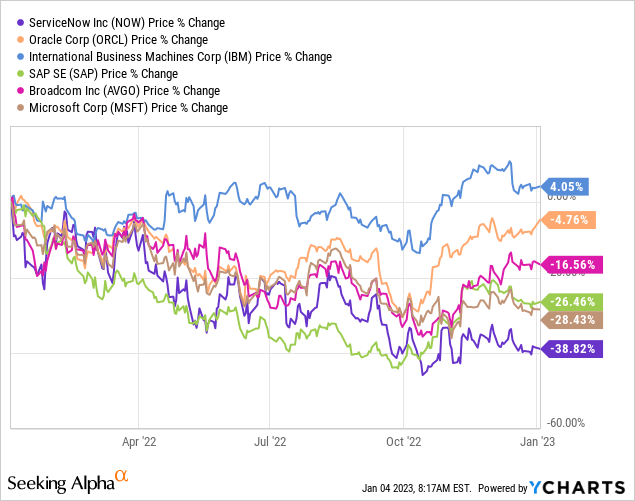

ServiceNow operates in a highly competitive industry of cloud computing platforms, and we’re more constructive on competitor Oracle (ORCL). While ServiceNow has grown at a faster pace than Oracle historically, Oracle appears to be taking the reins over the past year. Oracle is down a slight 6% over the past year, while ServiceNow is down 39% during the same period. For investors looking to jump into the software cloud computing space, we believe Oracle makes for a better investment than ServiceNow at the moment. Since we first wrote about Oracle in late September of last year, the stock has risen nearly 34%. We believe ServiceNow is not the best pick in the cloud computing space at the moment and expect the company to have more downside to be factored in before it becomes an attractive investment.

ServiceNow is also underperforming most of its main competitors over the past year. We don’t believe ServiceNow will outperform the competition during 1H23 and hence recommend investors sell the stock.

The following graph outlines ServiceNow’s stock performance in comparison to its main competitors: Oracle, International Business Machines Corp (IBM), SAP (SAP), Microsoft (MSFT), and Broadcom (AVGO).

TechStockPros

Valuation

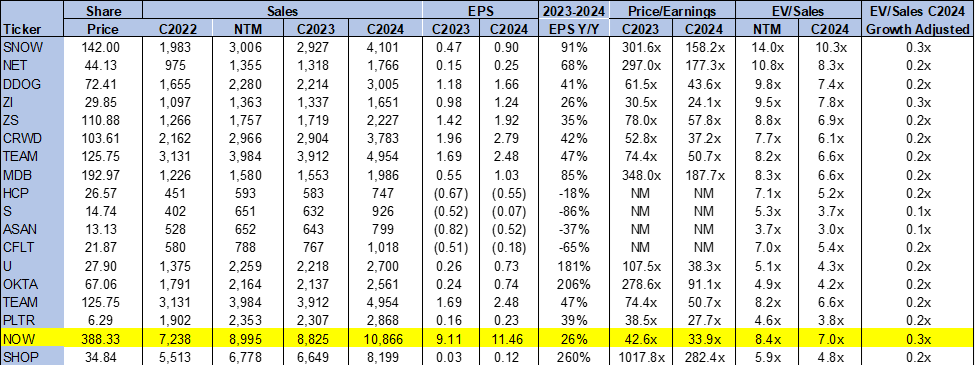

ServiceNow is trading at 33.9x C2024 on a P/E basis EPS of $11.46 compared to the peer group average of 90.05x. The stock is trading at 7.0x on EV/C2024 Sales versus the peer group average of 6.0x. Historically, ServiceNow has been a pricey stock, and we recommend against buying the stock based on weakness just yet. We believe the macroeconomic risks have yet to be fully factored into the stock and recommend investors sell the stock.

The following table outlines ServiceNow’s valuation.

TechStockPros

Word on Wall Street

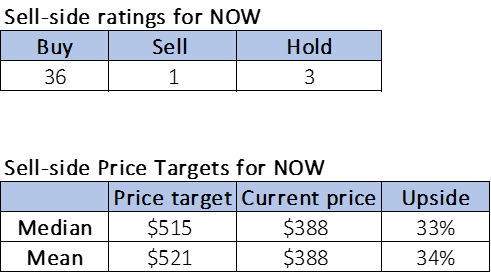

Wall Street is overwhelmingly bullish on the stock. Of the 40 analysts covering ServiceNow, 36 are buy-rated, three are hold-rated, and the remaining are sell-rated. We attribute Wall Street’s bullish sentiment on ServiceNow to the company’s position as a cloud computing platform serving 80% of the Fortune 500. Yet, we believe Wall Street and other analyses of the company on Seeking Alpha fail to take into account the impact of the macroeconomic environment that we expect to persist through 1H23.

The stock is trading at $388.The median sell-side price target is $515, while the mean is $521, with a potential 33-34% upside.

The following tables outline ServiceNow’s sell-side ratings and price targets.

TechStockPros

What to do with the stock

We’re sell-rated on ServiceNow. Our non-consensus bearish sentiment is based on our belief that the company will not outperform the peer group in the first half of 2023. While ServiceNow is well-positioned in the cloud computing market in the long run, we don’t believe the company’s subscription revenue is as resilient as investors would like it to be during current macroeconomic headwinds. We’re bullish on ServiceNow in the long run but believe the stock is too expensive to invest in at current levels, specifically when alternatives with more attractive valuations exist. We recommend investors exit the stock at current levels.

Be the first to comment