LUMIKK555

The new year is about to begin and it means that the traditional “Top 5 Mining Stocks to Watch” list is here. Unfortunately, the “top 2022 companies” were unable to replicate the great results of the “top 2021 companies“. However, they were definitely worth watching. Centerra Gold (CGAU) successfully closed the dispute with the Kyrgyz government, GCM Mining merged with Aris Mining (OTCQX:TPRFF), Taseko Mines (TGB) is on the verge of obtaining the final permit for the Florence project and only recently announced the financing package, and Western Copper and Gold (WRN) completed a feasibility study for the Casino project and extended Rio Tinto’s (RIO) rights. Unfortunately, the positive company-level developments were overshadowed by unfavorable broader stock market sentiment and commodity market weakness that emerged between June and October.

The list of companies worth watching in 2023 is presented below. All the companies should encounter major catalysts in 2023. Although they are not risk-free, they offer significant upside potential. Just like every year, I know that there are definitely some other companies with high potential that could have been considered for inclusion into the Top 5. If you are missing such a company on the list, please feel free to mention it in the comments section.

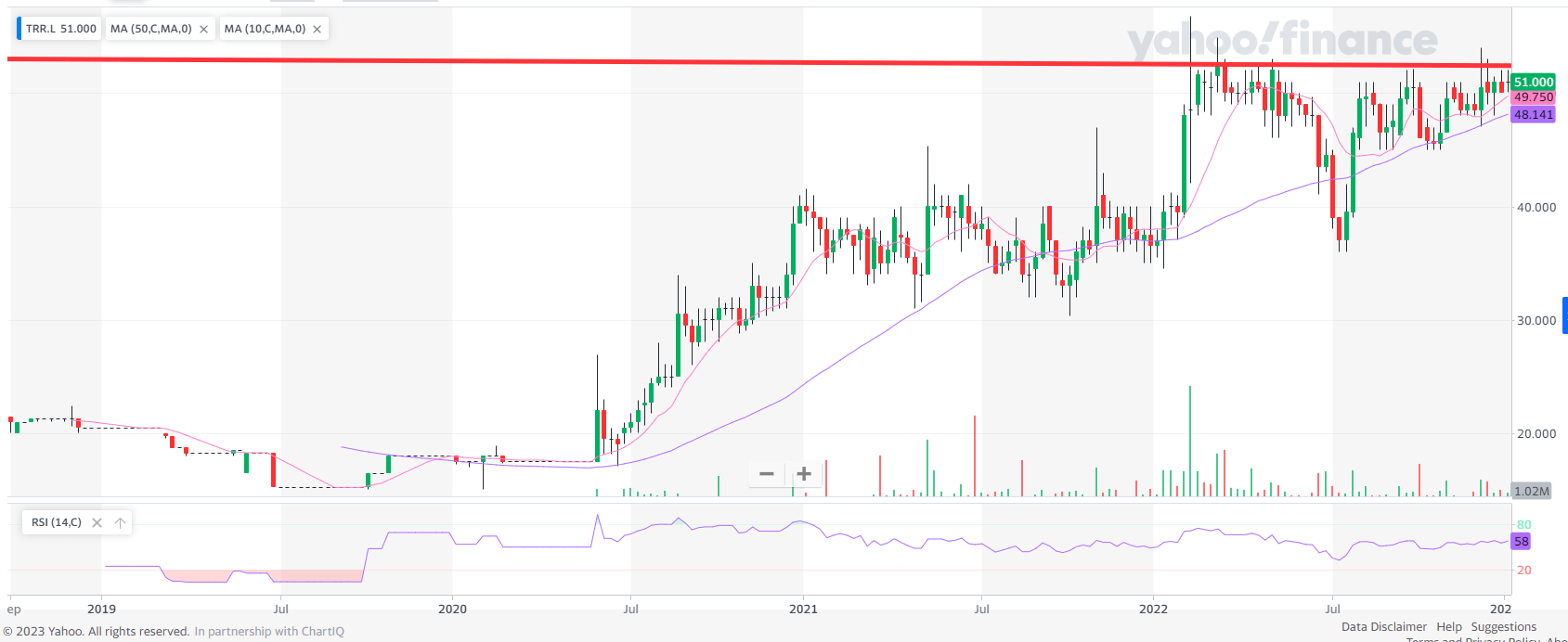

5. TRIDENT ROYALTIES (OTCPK:TDTRF)

This year’s no.5 is not a typical mining company, but a royalty company. Unlike the majority of its peers, Trident’s main assets are not focused on precious metals, but on lithium. Trident is generating revenues of around $9.6 million per year right now (the Q3 revenues annualized). However, this should change soon, as the Sonora lithium project owned by Ganfeng Lithium (OTCPK:GNENY) is about to start production by the end of this year. Trident owns an option to acquire a 1.5% Gross Revenue Royalty on the project.

The Sonora Lithium mine should be producing 17,500 tonnes of lithium carbonate per year over the first 4 years, and 35,000 tonnes following the mine expansion. There should be also 28,800 tonnes of potash per year produced. Trident estimates that the royalty covers around 96% of production over the initial 19-year mine life. At the current lithium carbonate price of approximately $75,000/t, the royalty should generate nearly $20 million per year for Trident. In the first stage of production. After the mine expansion, it should be nearly $40 million. However, on November 1, Trident announced that Ganfeng intends to accelerate the expansion and increase the stage 2 capacity from 35,000 to 50,000 tonnes. At the current lithium carbonate prices, it would mean over $56 million per year for Trident. By the way, Trident’s current market capitalization is $180 million. It means that the Sonora royalty alone has the potential to push Trident’s share price at least 200% higher. Not to talk about the other assets.

However, there is one problem with the Sonora royalty. Bacanora Lithium, the former owner of Sonora and currently a subsidiary of Ganfeng, is challenging its validity. This is the reason why Trident was able to acquire the option to buy the royalty for only $26 million. The good news is that a Court in Alberta has already dismissed the case in 2021. But Bacanora appealed the decision. The final court hearing is set for January 13. If Trident wins, which seems highly probable, its shares should experience a major boost. Another major catalyst will be the Sonora production start-up, late this year. (a more detailed analysis of Trident Royalties can be found here)

Source: Yahoo Finance

Lion One Metals is developing the alkaline Tuvatu gold project. The alkaline deposits are relatively rare. They are usually large and high-grade. Some of the most famous alkaline deposits are Porgera (25 million toz gold) and Lihir (40 million toz gold). Lion One has identified numerous similarities between Porgera and Tuvatu. Also the drill results delivered in 2022 confirm the high-grade nature of the deposit. The question is whether Tuvatu will be able to compete with the abovementioned deposits also in terms of the size. But as it remains open in several directions and at depth, this possibility cannot be excluded.

In 2022, Lion One reported several exceptional drill intersections at depth below the current resource area. They include 20.86 g/t gold over 75.9 meters (starting at depth of 443.4 meters) 12.22 g/t gold over 54.9 meters (starting at depth of 576.1 meters), or 17.89 g/t gold over 23.7 meters (starting at depth of 594.5 meters). The current resource estimate contains only indicated resources of 274,600 toz gold at a gold grade of 8.5 g/t and inferred resources of 384,000 toz gold at a gold grade of 9 g/t, but the new one (released probably sometime in 2023), should deliver much improved numbers. Not only the grades but also the overall volume of contained gold should increase significantly. The ultimate goal is to outline and develop a high-grade multi-million-ounce gold deposit.

Lion One keeps on drilling not only Tuvatu, but it has identified also several regional targets. There are 8 drill rigs on the property right now. So the drill results should keep on coming. But there is another major catalyst scheduled for H2 2023. Lion One is developing a small-scale mining operation that should get into production before the end of 2023. There is not much information, but according to a recent interview with Quinton Henning, Lion One’s technical advisor, it should have a throughput rate of 300-350 tpd. At a feed grade of 8.5 g/t and 90% recoveries, this small-scale operation should be able to produce around 30,000 toz gold per year. It is not much, but if it is successful, the cash flows should help to cover a major portion of Lion One’s exploration expenditures. At the current market capitalization of around $115 million, Lion One offers significant upside potential. (a more detailed analysis of Lion One Metals can be found here)

Source: TradingView

Ascot Resources is merging two brownfield projects, Premier and Red Mountain, into one. The mining operations were originally projected to start before the end of 2022, but due to some financing issues (the original debt financing was canceled), some of the construction activities had to be suspended. But on December 12, a new financing package was announced. As a result, the project is fully funded now and the first production is expected in late 2023 or early 2024.

The mine should be able to produce 132,000 toz gold and 370,000 toz silver per year on average, over 8-year mine life. The AISC was projected only at $769/toz gold. However, given the inflation pressures, it will be probably slightly higher, possibly somewhere in the $900-1,000 range. At the current gold price, the mine should be able to generate significant cash flows, especially when compared to Ascot’s market capitalization which is approximately $320 million right now. When I picked Ascot as the “October Idea of the Month“ for the members of the “Royalty & Streaming Corner”, its share price was approximately 50% lower. But it still offers significant upside potential. Especially given the fact that only less than 1/2 of resources is included in reserves. Moreover, Ascot keeps on delivering great drill results. For example, on October 27, Ascot announced the intersection of 31.92 g/t gold and 22.21 g/t silver over 10.69 meters, and 15.91 g/t gold and 31.5 g/t silver over 8 meters. This shows that there is significant potential for a major expansion of the relatively short initial mine life.

Source: TradingView

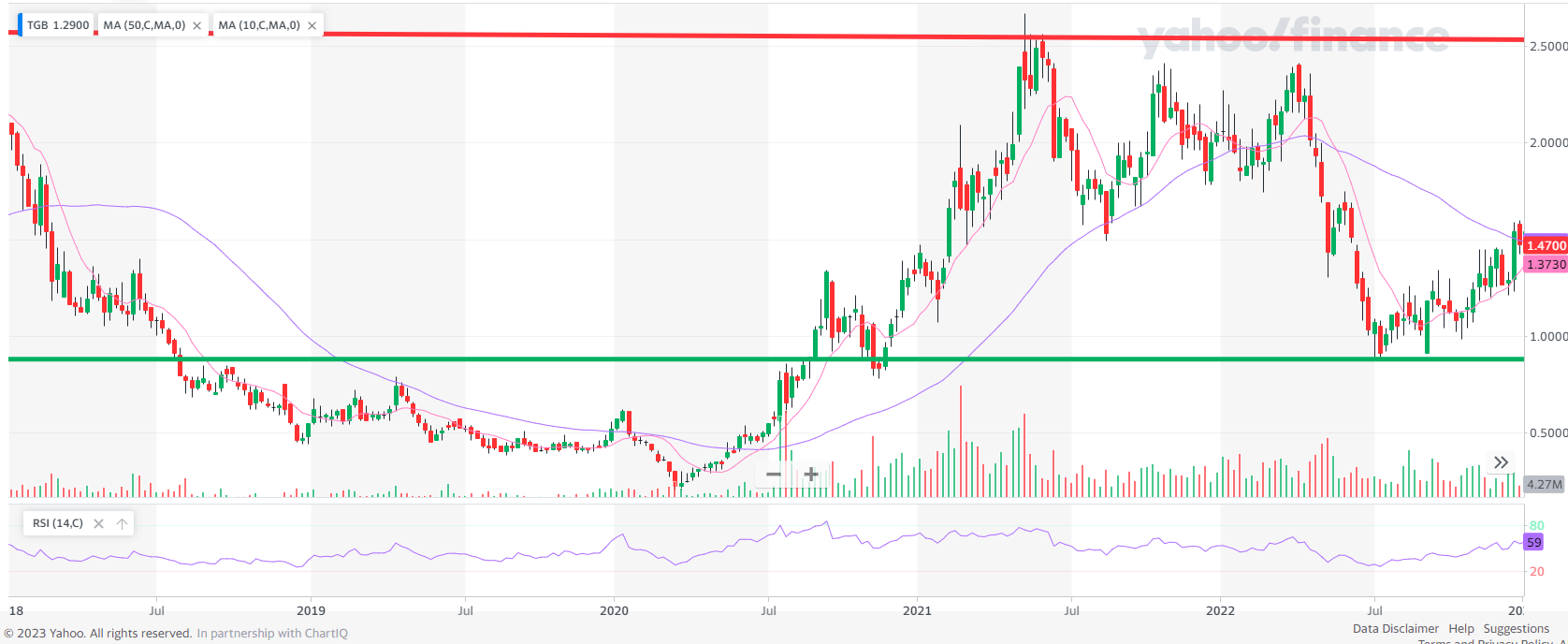

2. Taseko Mines

A bet on copper is Taseko Mines. Taseko is a copper producer, as it operates its 75%-owned Gibraltar mine. However, the upside is provided not by the Gibraltar mine but by the Florence copper project. The deposit contains reserves of 2.5 billion lb copper, of which, 1.7 billion lb should be recoverable by the in-situ recovery method. The initial CAPEX was estimated at $227 million, and the annual production rate at 85 million lb copper over 21-year mine life. The operating costs were projected only around $1.1/lb copper. Although the CAPEX as well as OPEX will be most probably higher than originally expected, the mine should be very profitable at the current copper prices. At a copper price of $3/lb, the after-tax NPV(7.5%) should be $680 million, and the after-tax IRR 37%. Although the costs will be higher than outlined by the feasibility study, the copper price stands at $3.75/lb right now, which should more than compensate for the increased costs. As a result, the approximately $700 million after-tax NPV should still be valid. It compares well to Taseko’s current market capitalization of $420 million. Not to talk about the value of the producing Gibraltar mine, and other projects including New Prosperity, Yellowhead, or Alley. (a more detailed analysis of Taseko Mines can be found here)

Only on December 20, Taseko announced that Mitsui (OTCPK:MITSY) agreed to pay $50 million for a 2.67% copper stream from Florence. Moreover, Mitsui has the option to pay Taseko another $50 million which would lead to the cancelation of the copper stream and Mitsui acquiring a 10% interest in Florence. After the money from Mitsui is added to Taseko’s available liquidity of approximately $150 million and cash flows that are being generated by Gibraltar, Florence should be fully funded (assuming no major cost overruns).

The only thing missing is the Underground Injection Permit. Although it takes much longer than originally expected, the process of its issuance should be really close to an end. The U.S. Environmental Protection Agency issued its draft in August, and the public comment period concluded in late September. The permits are expected any day now. It will be a major catalyst. Another one will be the commencement of construction activities. And although the construction should take around 18 months, as the production will be nearing, Taseko’s share price should experience a major re-rate.

Source: Yahoo Finance

Adriatic Metals is my no.1 for 2023. The year 2022 was the year of major construction activities at the Bosnian Vares project which is more than 50% complete now. Only on December 30, Adriatic announced the initial debt draw-down. Moreover, it confirmed that the project remains fully funded and on track for the first production in Q3 2023. This is great news, as Vares should become a cash machine for Adriatic.

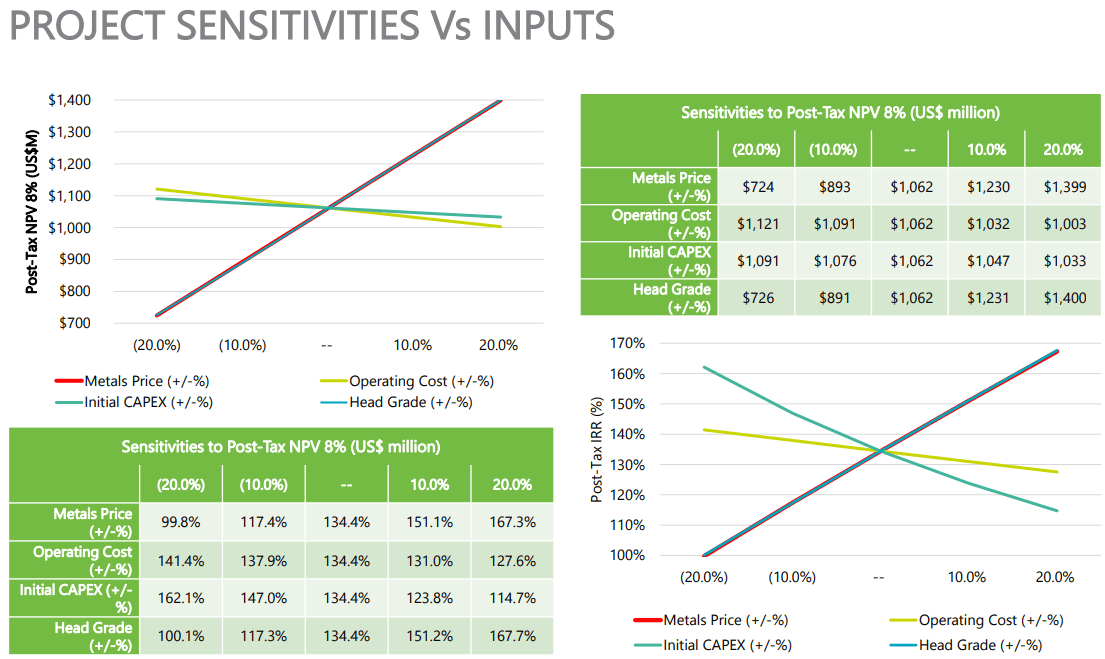

According to the August 2021 feasibility study, the mine should be able to produce 3.71 million toz silver, 62.7 million lb zinc, 46.2 million lb lead, 2.8 million lb copper, 21,800 toz gold, and 2.9 million lb antimony (or 11.2 million toz of silver equivalent) per year on average, over 10-year mine life. However, over the first 5 years, the production should equal nearly 15 million toz of silver equivalent per year. The AISC should be only $7.3/toz of silver equivalent, and the initial CAPEX should be only $168 million. The economics of the project are great. At base-case metals prices of $25/toz silver, $1.36/lb zinc, $1.04/lb lead, $4.3/lb copper, $1,800/toz gold, and $1.04/lb antimony, the after-tax NPV (8%) equals $1.062 billion, and the after-tax IRR equals 134%.

Source: Adriatic Metals

Yes, the base-case prices are higher than the current metals prices. However, as can be seen in the sensitivity analysis above, at 10%-lower metals prices, which is approximately in line with the current market prices, the after-tax NPV(8%) equals $893 million, and the after-tax IRR equals 117.4%. Both numbers are really great. Especially when compared to Adriatic’s current market capitalization of around $570 million. Moreover, Adriatic’s aim is to expand the mine life of Vares to more than 20 years. And it is important not to forget about Adriatic’s other asset, the Serbian Raska project which has potential similar to Vares. After Vares is up and running, Adriatic should start unlocking Raska’s value.

Source: TradingView

Happy and successful year 2023!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment