andresr

In a few weeks, earnings season will begin, and real estate investment trusts will present their fourth-quarter and full-year results. One such trust will be Medical Properties Trust Inc. (NYSE:MPW), whose valuation will have dropped by 49% by 2022 and whose dividend of 10.4% remains one of the most hotly debated topics.

Since 2023 has just begun, I’ll examine whether Medical Properties provides passive income investors with a dividend with a high degree of safety, or whether the trust will have to reduce its payout to respond to changes in dividend coverage.

High Margin Of Safety, Market Misjudges Dividend Risks

Medical Properties leases its real estate to hospital operators, who pay Medical Properties a handsome monthly rent. The trust is geographically diverse, with operations in the United States and Europe, and the business model is recession-resilient in the sense that healthcare expenditures are unrelated to the broader economy’s cyclical contractions.

Medical Properties has guided for of $1.80 – $1.82 per share in funds from operations in 2022 which, at a present price of $11.14, implies a price-to-FFO ratio of 6.15x. Even if Medical Properties generates 0% FFO growth over the next five years, the stock’s high margin of safety reflected in the valuation makes it appealing as a high yield passive income investment.

The question that many passive income investors with MPW in their portfolios are probably asking right now is whether the healthcare trust will have to reduce its dividend payout in 2023.

The short answer is: most likely not.

Between January and September, Medical Properties earned $1.08 per share in adjusted funds from operations while paying out $0.87 per share in dividends (at $0.29 per share per quarter).

The implied pay-out ratio, based on adjusted funds from operations, was 80% in 2022 (YTD), indicating that the healthcare trust is not approaching a dangerous level that would necessitate a dividend cut. This level is typically attained when the pay-out ratio exceeds 95% of AFFO.

Adjusted Funds From Operations (Medical Properties Trust)

While some investors are concerned about a dividend cut, I am going to take a risk here: MPW will not only not cut its dividend, but will also announce a dividend increase very soon.

Based on the pay-out metrics presented in the table below, I don’t see why Medical Properties would have to reduce its dividend pay-out (MPW has had a consistent dividend pay-out ratio of 80% in the last twelve months), and the trust is also looking at improved liquidity.

Dividend (Author Created Table Using Trust Information)

Ample Liquidity Reduces Risks For Passive Income Investors

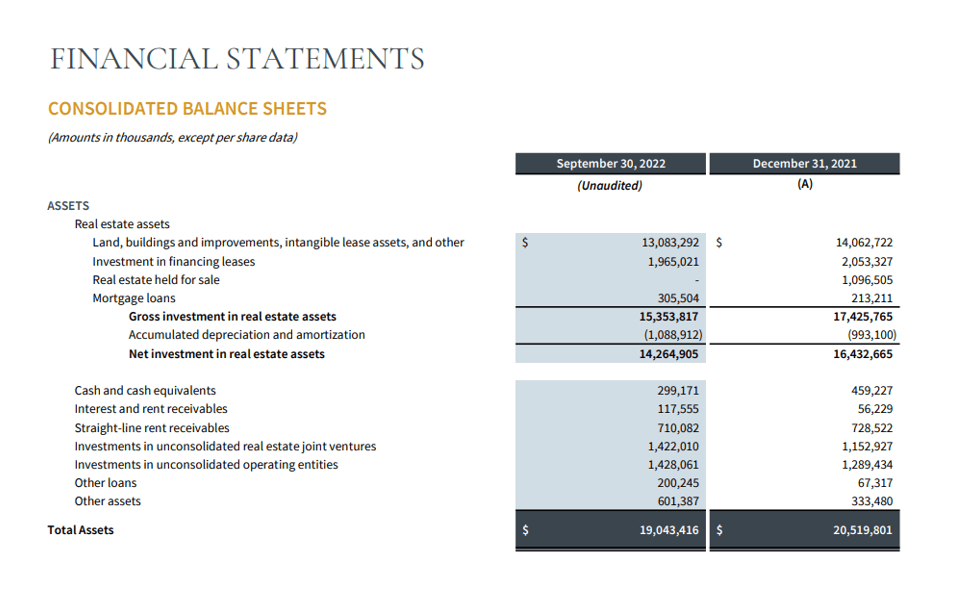

Medical Properties has a strong balance sheet and liquidity position, which is expected to improve further in 1Q-23. As of September 30, 2022, the trust’s balance sheet showed $300 million in cash/cash equivalents, and management is exploring strategic options for some of its hospital assets.

For example, management announced in October that it would sell three Connecticut hospitals to Prospect Medical Holdings for $457 million.

Medical Properties is also expected to receive a $200 million loan repayment in the first half of 2023 in connection with LifePoint Health’s acquisition of a majority stake in Springstone Health.

These transactions will strengthen Medical Properties’ strong liquidity position, making it even less likely that the trust will have to reduce its dividend payout in 2023 due to a lack of resources.

Balance Sheet (Medical Properties Trust)

Why My Analysis Could Be Off-The-Mark

Only a significant and unexpected decline in the health of MPW’s operator base could cause a decline in Medical Properties’ funds from operations and dividend coverage.

The pay-out ratio based on AFFO, as replicated above, shows that the dividend is quite secure even if the trust’s operator health deteriorates significantly.

MPW could withstand a 20% drop in adjusted funds from operations and still cover its dividend payments.

My Conclusion

Medical Properties was one of the market’s most punished healthcare real estate investment trusts in 2022, but that doesn’t mean the market is correct.

Given that MPW’s dividend is handsomely covered by funds from operations and healthcare spending is unaffected by cyclical contractions in the economy, I believe MPW could see a strong turnaround in 2023.

I also believe that MPW will not only not cut its dividend, but will increase it to $0.30 per share in 1Q-23.

What adds to the margin of safety here is that Medical Properties would easily be able to meet its dividend commitments to the trust’s shareholders even under a 0% FFO growth assumption.

Be the first to comment