Author’s note: Written by Stanford Chemist for Cash Builder Opportunities.

With COVID-19 likely turning into “COVID-forever,” vaccine manufacturers such as Moderna (NASDAQ:MRNA) have a chance to make continued profit from the regular boosters that would be required, especially when/if new variants inevitably emerge. Last week, the FDA approved bivalent vaccines from MRNA and Pfizer (PFE) for use in booster shots. These vaccines contain two mRNA components of the SARS-CoV-2 virus, one from the original strain of SARS-CoV-2 and the other one in common with the BA.4 and BA.5 strains of the omicron variant that’s currently spreading most quickly around the world.

US FDA

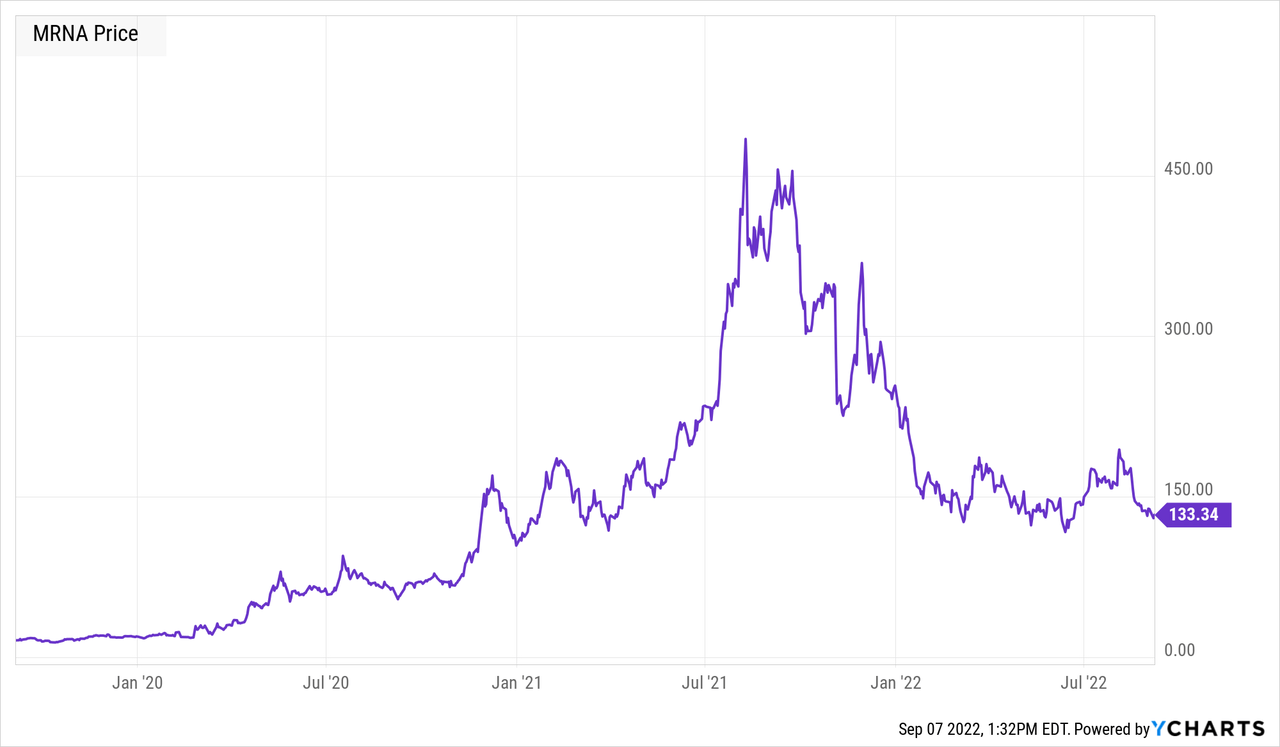

The significant medical and socioeconomic burdens imposed by COVID spurred MRNA’s share price to all-time highs of near-$500 during mid-2021. However, its share price has since dropped by over two-thirds since then.

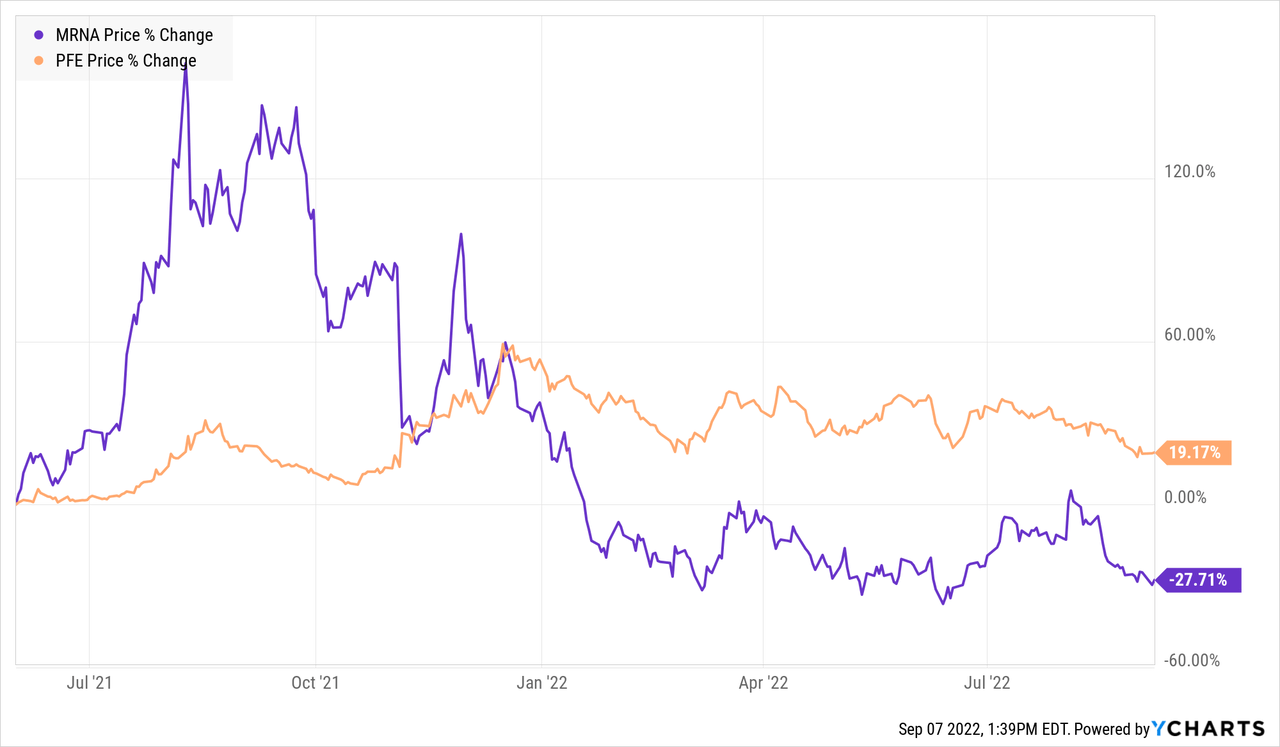

What happened? There was likely a multitude of factors. First, MRNA was caught in the vicious sell-off in growth stocks that has occurred over the past year. Second, the COVID vaccine is currently MRNA’s sole source of revenue. With the Omicron variant being milder than previous strains, as well as with other non-vaccine antivirals on the way, there’s a risk that vaccines would be in less demand in the future. These could be reasons why MRNA’s share price has been much more volatile than PFE, which produces the other major mRNA vaccine used today (BioNTech’s (BNTX) Comirnaty).

On the positive side, Moderna’s vaccine is actually considered to be one of the best vaccines available, with even slightly better efficacy than the Pfizer/BioNTech shot. Moreover, the mRNA platform is in principle easily adaptable to other infectious diseases, which could give the company an entry into other markets in the future. With the huge spike in earnings, Moderna is able to plow these into R&D which could potentially pay off big in the future. The company currently has a range of vaccines and therapeutics in its pipeline targeting both infectious and non-infectious diseases.

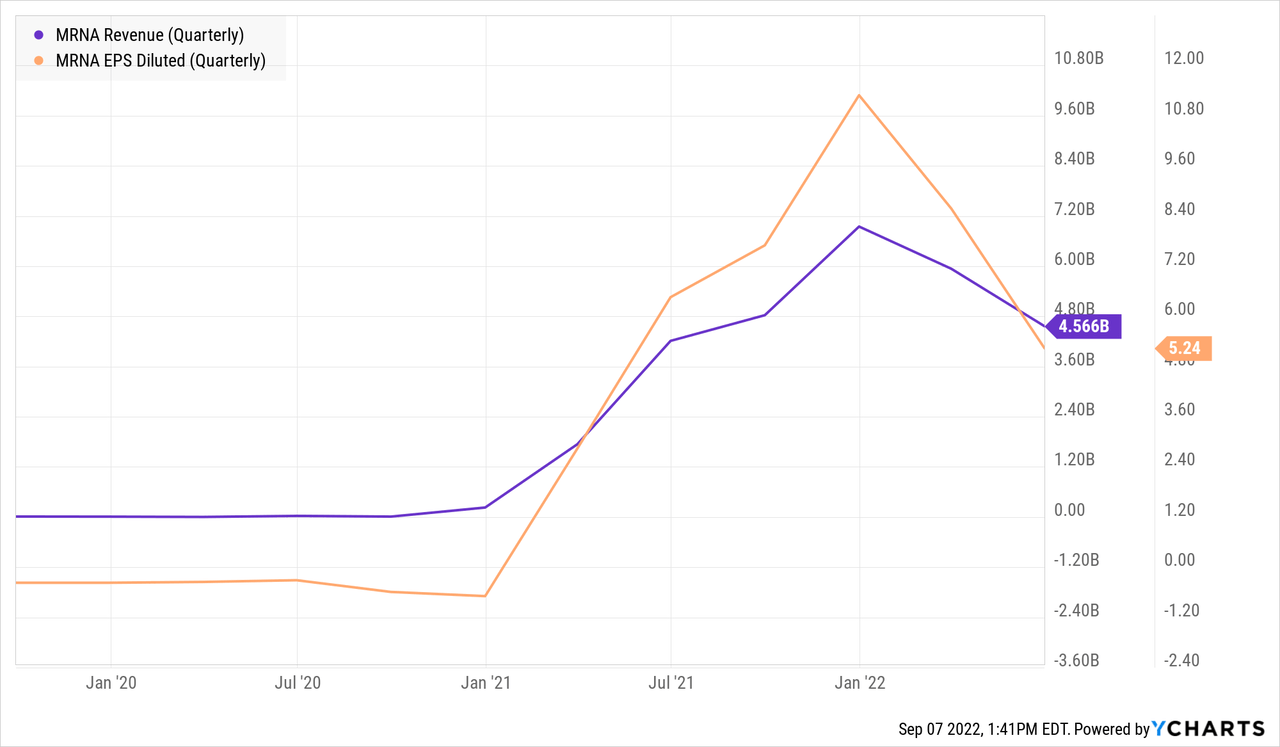

The biggest risks to the MRNA thesis are (1) that in the future, the COVID-19 vaccine is no longer needed, or supplanted by even superior alternatives and (2) that Modern’s R&D pipeline yields little to no fruit. While the second factor is impossible to predict with certainty, we already know that the demand for existing vaccines is going to drop significantly given the decreased lethality of current COVID-19 variants combined with the fact that more and more of the world’s population will become fully vaccinated. Indeed, analysts already are pricing a massive drop in earnings and revenue for 2023 and beyond.

Seeking Alpha

Seeking Alpha

Put options strategy

At Cash Builder Opportunities, we use options to generate additional yield from both dividend and non-dividend paying stocks. We discussed the ideas behind selling options for income in a previous article: Why We Sell Options. In that article, we discussed (among other things) the mechanics behind selling put options.

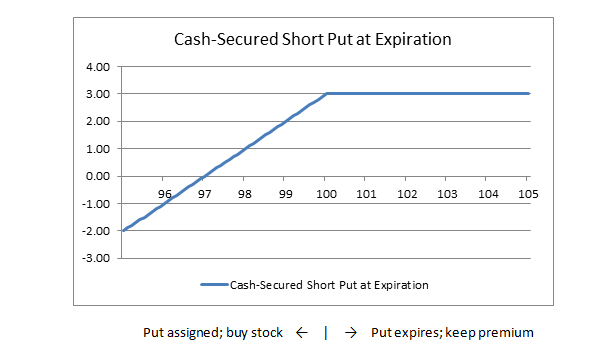

What we’re essentially doing is selling another investor insurance. That gives them the right to “put” shares to you should the security trade below the strike price at expiration. We have a limited gain in that our upside is capped at the premium collected. On the other hand, we also have a known and limited downside as well. The maximum downside can be substantial but is limited to the price of the security going to $0. To illustrate this, we’ll use an image from Fidelity that helps visualize the upside and downside.

Fidelity

The uncertainty regarding MRNA’s future earnings is why I require a very large margin of safety for MRNA options trade. Back in January of this year, I showcased a long-dated put idea on MRNA to our member community (see MRNA: Growth Idea: Selling Long-Dated MRNA Puts). This $80 put had an expiration date of July 15, 2022, and it expired safely out of the money at expiry. This allowed us to pocket the entire $3.15 premium from selling the put option ($315 per contract), corresponding to an annualized yield of 7.43% on a cash-secured basis.

With volatility still currently elevated, I feel that now is a good time to share another MRNA put options idea. For this trade, I’m highlighting the $85 put option expiring on Jan. 20, 2023, which is around 4.5 months away. This gives a very wide margin of safety from the current share price of ~$134, as the strike price is -36% below the current share price. Moreover, $85 is only slightly above where the stock was trading at in December 2020, before the FDA gave its first approval to the vaccine for practical use. Given the latest positive developments of the approval of Moderna’s bivalent booster for the newest Omicron variants, I’m making a calculated bet that MRNA’s share price will not decline below $85 by Jan. 20, 2023.

Taking $3.50 as the midpoint of the bid-ask spread for this option (live quote on Sept. 7, 2022), the annualized premium yield of this put is 11.2% on a cash-secured basis.

Interactive Brokers

The trade will lose money if MRNA declines below the breakeven point of $81.50 by Jan. 20, 2023, which is calculated as the strike price minus the option income received. Hence, investors should be comfortable being assigned MRNA stock at a cost basis of $81.50 (~40% discount to the current share price) as the worst-case scenario.

Summary

In summary, this cash-secured put idea provides either 11.2% annualized yield on cash or the opportunity to buy MRNA stock at $81.50.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment