NYS444/iStock via Getty Images

Thesis

Many of you probably heard some rephrased version of this quote. The newest version I heard was during my teenage son’s driving lesson. When you drink and drive, you are still a fool even if you had a good time and got home safe. It could not be truer in investing.

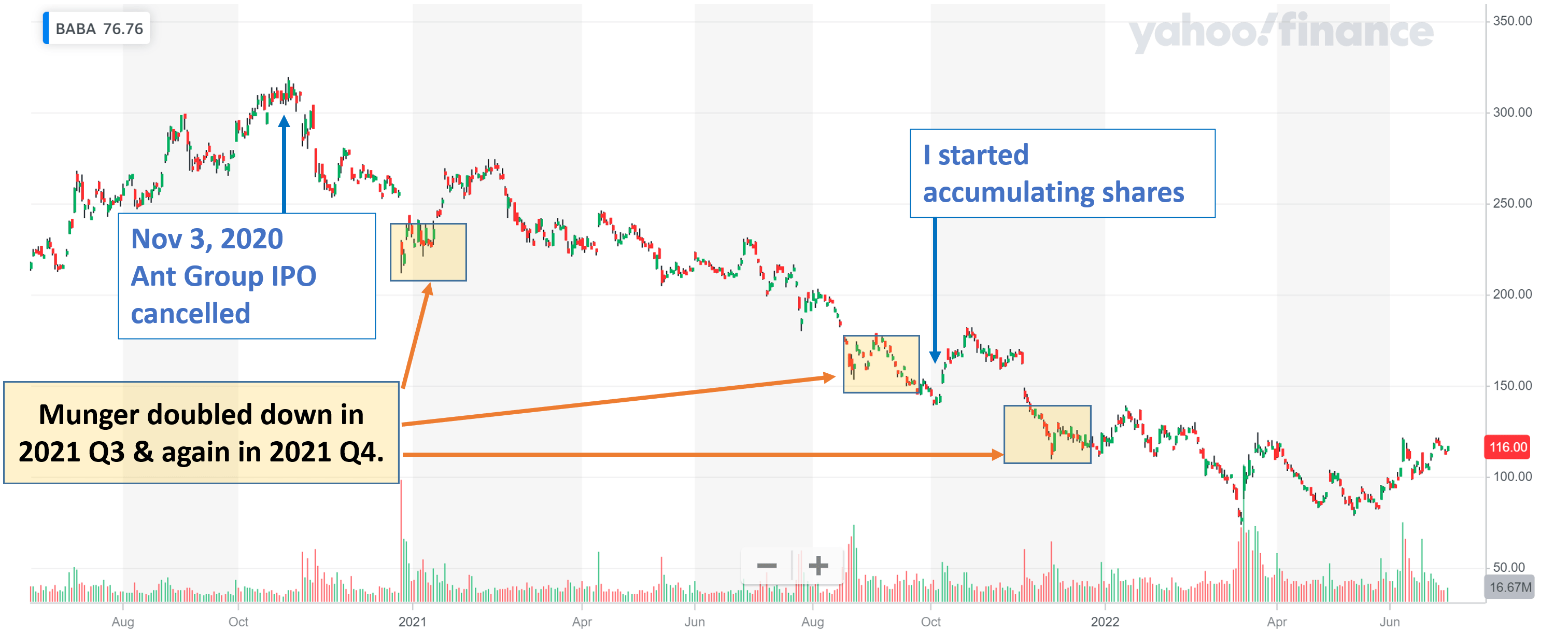

The goal of this article is to reflect on the above wisdom with my Alibaba (NYSE:BABA, OTCPK:BABAF) position in the past year or so. I started accumulating BABA shares around October 2021 as you can see from the following chart. And my average cost basis is about $115. So, after almost a year of a rollercoaster ride (pretty much a one-way downward ride most of the time), my BABA position is finally above water – by a teeny bit.

In investing, losing money for the wrong reason (or for any reason at all) obviously is painful. But what’s truly dangerous is making money for the wrong reason, because it can lead you to lose more. Therefore, the goal of this article is twofold. First, I thought it worthwhile to briefly reflect on some of the key lessons relearned (really re-learned), which hopefully can better shield myself and other investors from such costly lessons. Second, I will offer some forward-looking views on BABA stock with its recent development, particularly its leading position in the eCommerce space and the possibility (and risks) of the Ant Group IPO.

Yahoo Finance

Lessons learned

First, I am glad I followed my own rules and accumulated shares layer by layer. Do not trust your (or anyone else’s) “convicted buy” or “all in” judgment. After a certain stage in life, any “all-in” judgment is by default a bad judgment – even if it turns out to be profitable (remember, you are still a fool even if you survived a bonfire party in an ammo depot). I run a market service with members juggling multiple financial priorities, and I constantly emphasize such a skewed risk/reward profile. The risk/reward profile is so skewed past a certain stage in life. If your all-in bet worked out, what is the upside? It is limited. You can only retire once in this lifetime. But if it does not, what is the downside? It is unlimited. You cannot afford to start over again.

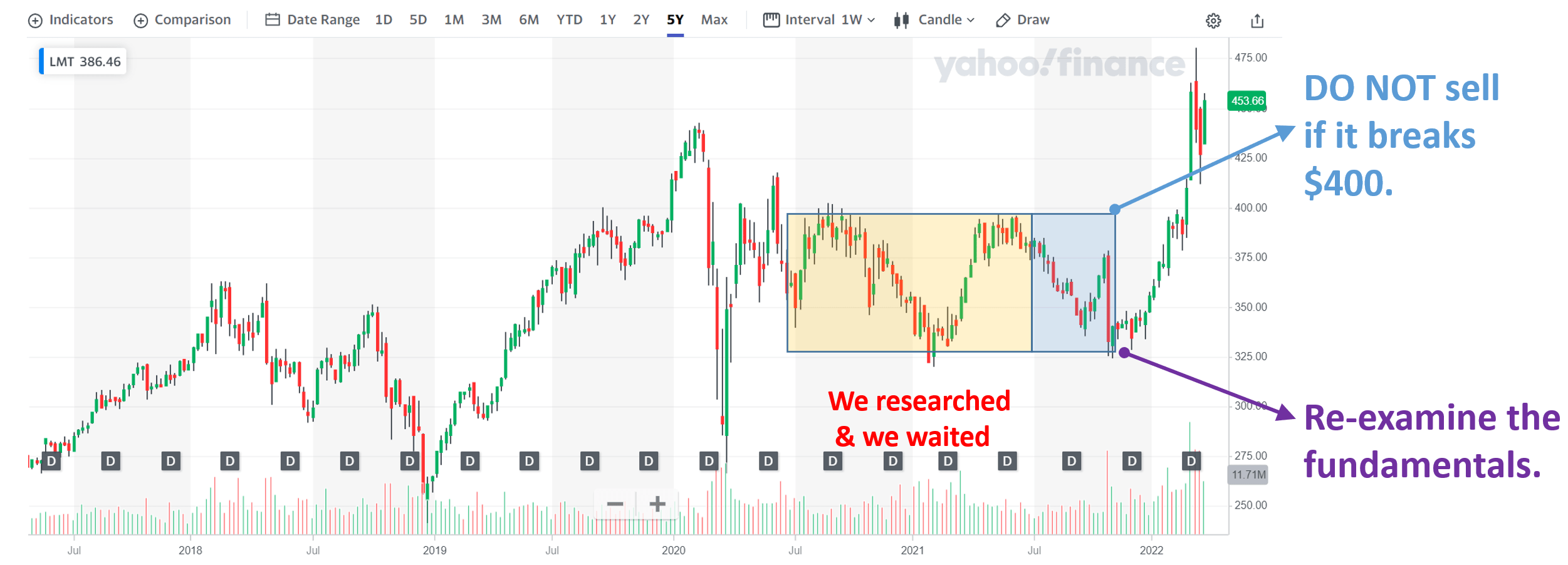

Second, I had to relearn the costly lesson of patience again. I have been writing about my own patience test. And an example detailed in my free blog article here is shown below. A simple test is the so-called consolidate window, as shown in the yellow box below. I’d like to see a consolidation window of at least a year, a rule I’ve followed and enjoyed successes with many other stocks like Lockheed Martin (LMT), British American Tobacco (BTI, OTCPK:BTAFF), et al. But with BABA, I somehow convinced myself this time is different and acted prematurely as you can see from the chart above.

Lastly, part of being humans is that we cannot rely on our brain to override our own brain. As such, much of my learning process is to codify such lessons into tools that can be used over again in the future both for myself and for others, another underpinning philosophy of our investing and marketplace community.

Yahoo Finance

BABA leads the eCommerce

Now, move on to the BABA stock itself. My past writing has discussed various specific aspects of it. So here I thought it might be a good idea to take a step back and provide a higher-level overview. My bull thesis is quite simple and can be capsulated in just one short sentence: the shift of our world toward eCommerce is unstoppable and BABA is a leader currently on sale.

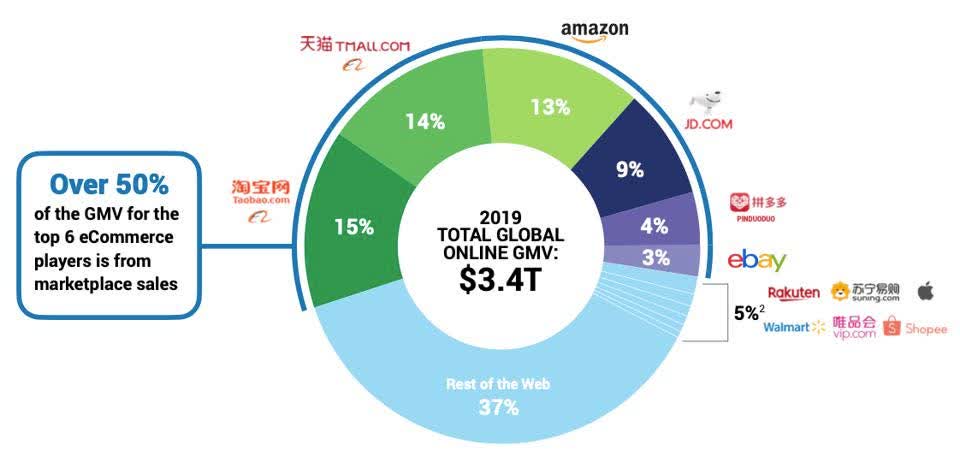

Today we have to emphasize “eCommerce,” just to distinguish it from the “normal” offline commerce. I foresee that not far into the future, all commerce will be eCommerce by default. And according to the following Forbes report, current global eCommerce is dominated by only 6 companies. Together, these 6 companies account for over half (58% to be more precise) of the global eCommerce. And you can see that 4 are from China, with BABA being the leader. The Forbes report pointed out that (emphasis added):

And just four Chinese companies account for almost half of global digital sales. The biggest digital commerce companies, with the percentage of the global e-commerce market that they own are Taobao.com 15%, TMall.com 14%, Amazon 13%, JD.com: 9%, Pinduoduo 4%, and eBay: 3%. One key reason: retail in China is simply much more digital than it is in Europe or North America.

I totally agree with Forbes’ view (highlighted above by me), and BABA is in the best position to capitalize on the tectonic shift of China toward everything digital.

Forbes

The Ant Group IPO

Now, switching to the Ant Group IPO. One consideration that made me think BABA was different and acted in haste was its miscarriage IPO in Nov 2020. My judgment at that time was that the IPO “just” needed more review and stamps. Probably I made the right call, but I certainly misjudged the timeframe (which goes back to my patient test above).

Now, according to a Bloomberg report, a revival of the Ant Group IPO seems like a realistic possibility. The following specifics are quoted from this report (slightly edited by me):

Ant Group is poised to apply for a key financial license as soon as this month, according to people familiar with the matter, a sign that its lengthy overhaul following a squashed 2020 listing is getting closer to satisfying China’s financial regulators.

The People’s Bank of China intends to accept Ant’s application to become a financial holding company once it’s submitted and will then start a review process, which could take months, said the people, asking not to be identified discussing a private matter. Officials will examine Ant’s capital strength and business plans, as well as the compliance of its shareholders and senior management before a final signoff.

The timeframe and actual valuation of the IPO is uncertain (elaborated in the risk section below). However, regardless of the specific timetable and valuation, I think the symbolic and psychological effects are more crucial and effective here.

Final thoughts and risks

Investing provides a wicked learning environment and often rewards wrong actions. My BABA experiences serve as a good example. To survive the market in the long term, we not only need to make money but also make money for the right reasons.

Specific to BABA, I remain bullish on its long-term prospects. It’s the best-positioned stock in my view to capitalize on the world’s eCommerce revolution, especially in the Asian Pacific region, the epicenter of the remaining revolution.

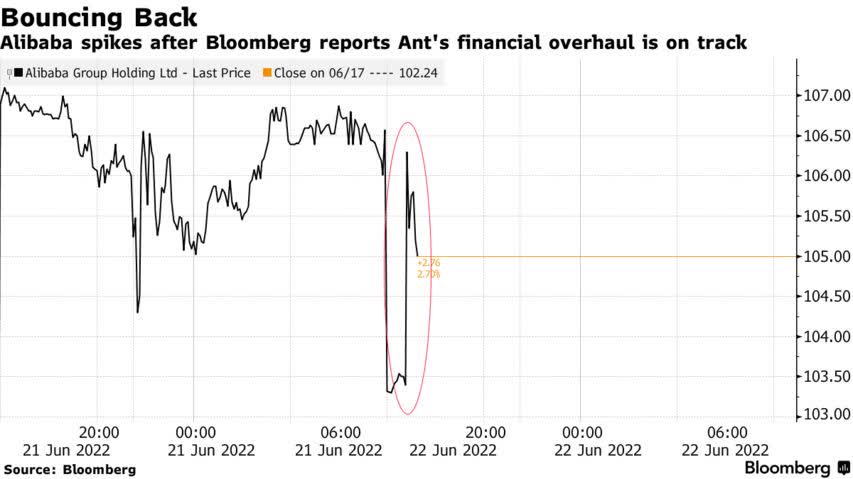

The Ant Group IPO, which got me interested in the stock in the first place, now seems to be back on the table, although investors need to be aware of the risks here. The development is quite speculative at this stage and can trigger extreme short-term volatility. As an example, the following chart shows its price actions after the Bloomberg report. The valuation is also uncertain even if it ultimately made it to IPO. Before the Nov 2020’s cancellation, Ant’s valuation was estimated to be in the $150 to $120 billion range (and BABA owns 1/3 of it). However, much has changed, and it is uncertain how much its valuation has decreased after all the new regulations are imposed.

Bloomberg

Be the first to comment