Written by Nick Ackerman. This article was originally published to members of Cash Builder Opportunities on August 20th, 2022.

The latest options expiration date passing has several of our trades expiring worthless. This includes puts we sold on Enterprise Products Partners (EPD), VICI Properties (VICI) and Gladstone Land (LAND). All three of these are dividend growers. I would have been happy to add these additions to my portfolio.

In fact, EPD is already a long-term core position for me. I held LAND previously, and VICI has caught my interest as a dividend-growing REIT. That’s what sets up the option put writing strategy as a bit of a win-win. You can add to names that you wouldn’t otherwise mind adding, putting your idle cash to work. If shares fall, you get the opportunity to buy shares lower than the market was pricing them when the trade was initiated. If shares stay above your strike price, then you simply get to collect the premium and can start the process over again.

Additionally, with the latest options expiration, we have Stanford Chemist’s covered call trade expiring worthless. This was on shares of the KraneShares CSI China Internet ETF (KWEB). We were originally assigned these positions earlier. We then turned around to write calls, employing the options wheel strategy as we often do with positions. With that trade, we collected a premium of $0.88.

Enterprise Products Partners

For me personally, this is the smallest position in my portfolio. I’m hesitant to add too much energy exposure. However, if there were a “blue chip” in this space, I’d have to consider EPD to be it. They have the capability and capacity to move more than just crude oil and natural gas, which makes them more versatile. As they continue to diversify what their pipes can move, I believe it puts them in a stronger position to remain relevant for longer.

Their conservative management and strong balance sheet have left them in a position of being an MLP that has produced a growing dividend over time. That’s on top of the latest yield at around 7%. A high yielder with growth is rare to find.

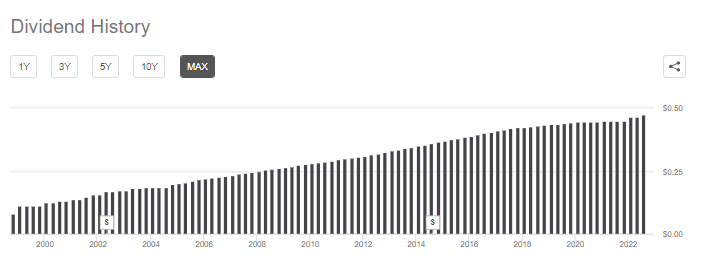

EPD Distribution History (Seeking Alpha)

While they were doing quarterly increases, that pace slowed through 2020 and 2021. However, we once again see the pace pick back up on the strength of the whole energy complex at this time due to higher energy prices. They raised their distribution at the beginning of the year and have done so again with the latest payout. Based on their last earnings report, their distributable cash flow came to 1.9x coverage. That leaves them plenty of capacity to continue raising even in the next economic slowdown.

The Trade: Sold Opening Puts on Enterprise Products Partners August 19th, 2022 – $25 strike collected $0.18

This trade was over just 16 days, so a relatively shorter-term trade. At the time, the price decline would have only been minimal to hit the strike price. However, the price of the units rose then, which led us to the trade expiring worthless. While the absolute premium amount wasn’t particularly large, the potential annualized return [PAR] reached 16.425%. That is right around my personal target of 15%.

This was my main thought behind entering this trade in the first place.

This is a position in the Core Income Builder Portfolio, so adding to it is something that I would welcome. This is a shorter-term trade with an expiration around two weeks away. In the end, I’ll either end up with some more units of an MLP I already own, or I walk away with a couple of bucks for my efforts.

For the next moves, I would consider selling more puts if the price of the units falls further. If we are in a bear market rally, that could happen before we know it. That being said, it will also depend on the price of crude. Despite being a midstream operation that should be more sheltered from energy prices, we know that, in reality, they are sensitive to oil prices.

VICI Properties

This wasn’t our first trade with VICI. Last year we sold assigned puts, which we then sold calls on. These calls were then called away as shares bounced back after entering the trade. That series of trades is precisely what we look for when employing the options wheel strategy.

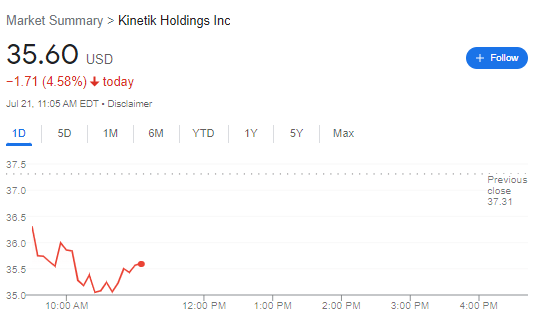

VICI also regularly pops up on the monthly dividend grower screening articles. That keeps VICI at the top of my mind. This trade, more specifically, was made in connection with selling Kinetik Holdings (KNTK) position. That made some room for another position in the Satellite Income Builder Portfolio.

I’ve been considering selling KNTK for a while now. It isn’t ideal that it is on such a down day, but the gains have still been strong since holding the name. I’ve actually held it longer than I originally thought. The momentum in energy persuaded me to continue holding.

KNTK Price (Google Finance)

My sole initial reason for buying shares on January 27th, 2021, was because they reinstated their dividend. I figured that investors would bid up the shares due to that excitement. That was when it was still Altus Midstream.

Share price performance only, I’m selling at around a 48% gain since that time.

When selling puts on VICI, it was basically right at the money, with shares trading at $32.84 that day.

The Trade: Sold Opening Puts on VICI Properties August 19th, 2022 – $32.50 strike collected $0.83

For that trade, it was for 29 days. The PAR came to 32.14%. The dividend equivalent of the premium collected based on the $0.36 quarterly dividend was a strong 2.3x. It was done in around a month when a quarterly dividend is paid every ~90 days, which is even more impressive.

This REIT still carries an impressive 4.16% dividend yield, but I would also like to see this name come back down some. The overall market has run a lot since the June lows. VICI has been running up with it too. So the next move here would also be to wait until the price falls back into the lower $30s.

Gladstone Land

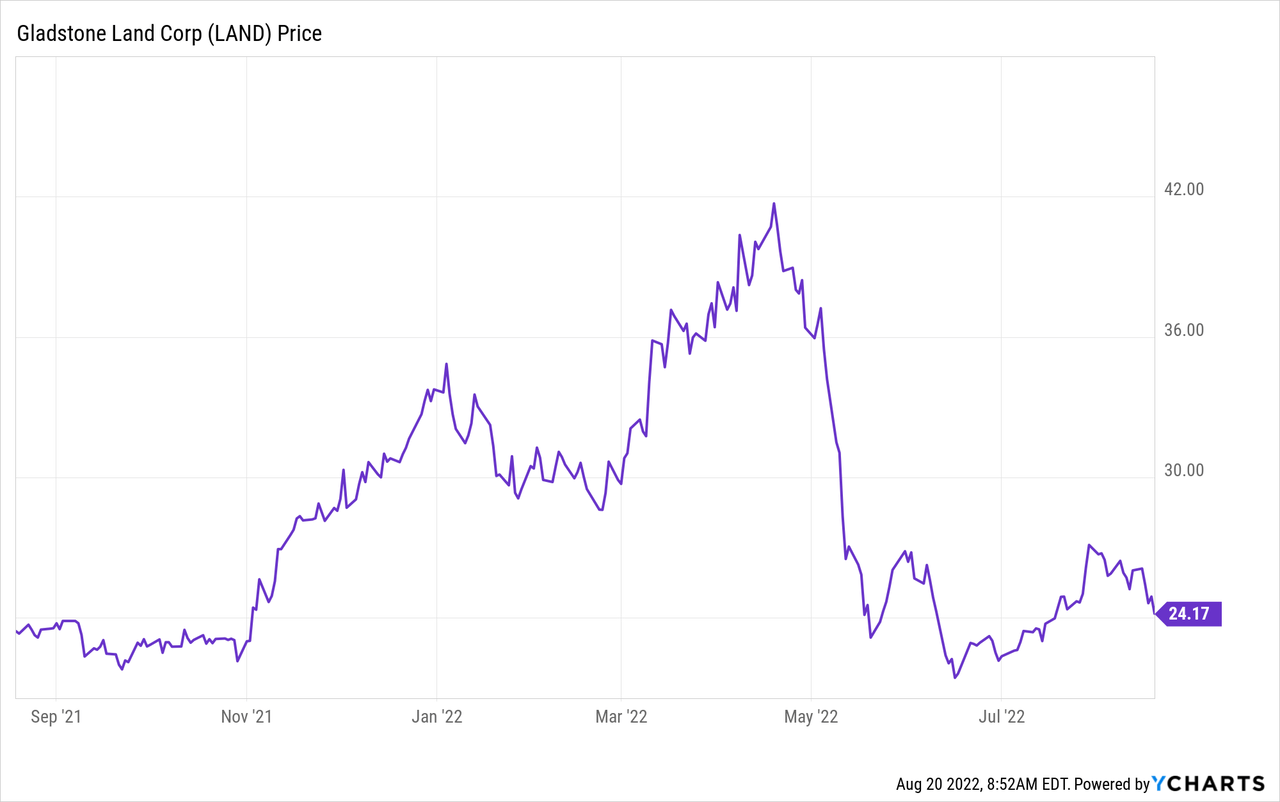

This name has been making quite the erratic moves lately. I shared more of my thoughts on LAND a couple of months ago. After the stock had fallen around 40% from its 52-week high, it was becoming closer to a viable investment again. I believe that under $25, one could start nibbling; I believe that below $20 is ideal, though.

After that posting, the price did continue to fall as expected. However, shortly after that, it began to make its way higher again. More recently, it has once begun selling off sharply. Here’s a look at the price over the last year.

YCharts

LAND “primarily targets fruit and vegetable cropland in regions with established rental markets and strong operations.” Their goal is to “build the premier farmland real estate company focused on the ownership of high-quality farms and farm-related properties that are leased on a triple-net basis to tenants with a strong operating history and deep farming resources. All our farms have abundant water sources and are currently 100% occupied.”

The price is being pushed around by being a great place to invest with higher inflation. As a farmland REIT, it should be well protected against inflation. However, the downside here is the location of their orchards, which are located in the western U.S., where droughts produce a lack of water. The higher inflation is also impacting their farmers, though with higher costs.

In the latest conference call, they made several remarks on this subject.

Water costs have increased, especially in the West, but our farms seem to be okay today. Farmers have passed on many of the increased cost to the food sellers like grocery stores and every family is feeling this extra cost that drive through the economy. So, we’ve slowed the purchases of farms due to worry that inflation will reduce many farmers’ ability to pay rent. Currently, we have two farmers who are slow on their paid rent, it’s below 3% of our rents, one of them tells us that the payments on the way.

They still mentioned that they have enough water for this year but didn’t provide any reassurance for next year.

A couple of other items that you always ask about. We continue to monitor the ongoing drought in the West. They had a very nice winter out there, but that’s about the last of it every now and then they get a little bit of rain. It’s a very, very dry since then. All of our properties in California continue in the position where the farmer has enough water to complete the current crop year. And, of course, we never know what next year is going to look like, but water remains a premium at west.

Previously, they stated that “all our farms have abundant water sources.” I might be trying to split hairs here, but it sounds like they might not be as confident going forward.

I believe that others might have been getting the same feelings, though, and that is why the stock price remains so volatile.

The Trade: Sold Opening puts on Gladstone Land August 19th, 2022 – $20 strike collected $0.59

LAND pays only a small monthly dividend of $0.0454. That means collecting a $0.59 premium resulted in 13x the monthly dividend. However, this was over 70 days. This translated into a PAR of 15.38%.

LAND Shares are trading slightly lower now than when we entered this trade. I believe that allows for us to make another trade rather quickly potentially. This is particularly true if last Friday’s big move lower is any indication that we are going to be pulling back from these latest highs. A move lower could take LAND down with it, providing a higher premium collection at the $20 strike price.

This is a very lightly traded name in the options space, so the bid and ask spreads are quite large. For example, the November 18th, 2022, expiration at the $20 strike shows the last trade completed at $0.45. The bid was $0.20, and the ask was $0.60.

Being that it is 90 days out, it would put us at a lower PAR than what we saw above, even if the $0.60 triggered. That’s the expiration I’m looking at for now. It also means we should see their next earnings reported before that expiration date.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment