-slav-

Silvergate (NYSE:SI) is a bank that should benefit from increasing net interest margin as the Fed continues to hike rates. The market is very concerned that like other crypto-plays, Silvergate may face legal risks or even bankruptcy.

These concerns may be throwing the baby out with the bathwater, though given the recent turmoil in crypto it is reasonable to expect Silvergate to lose deposits, the bad news here is already more than discounted in the price in my view.

Silvergate is a well-managed bank, that is being valued more like a speculative crypto startup. Deposit outflows and legal issues create some risks, but these appear overstated. A fair value for the shares may be around $40-$60/share based on earnings and book value, and it’s not unreasonable that the preferreds should trade much closer to $25.

Silvergate is a Bank

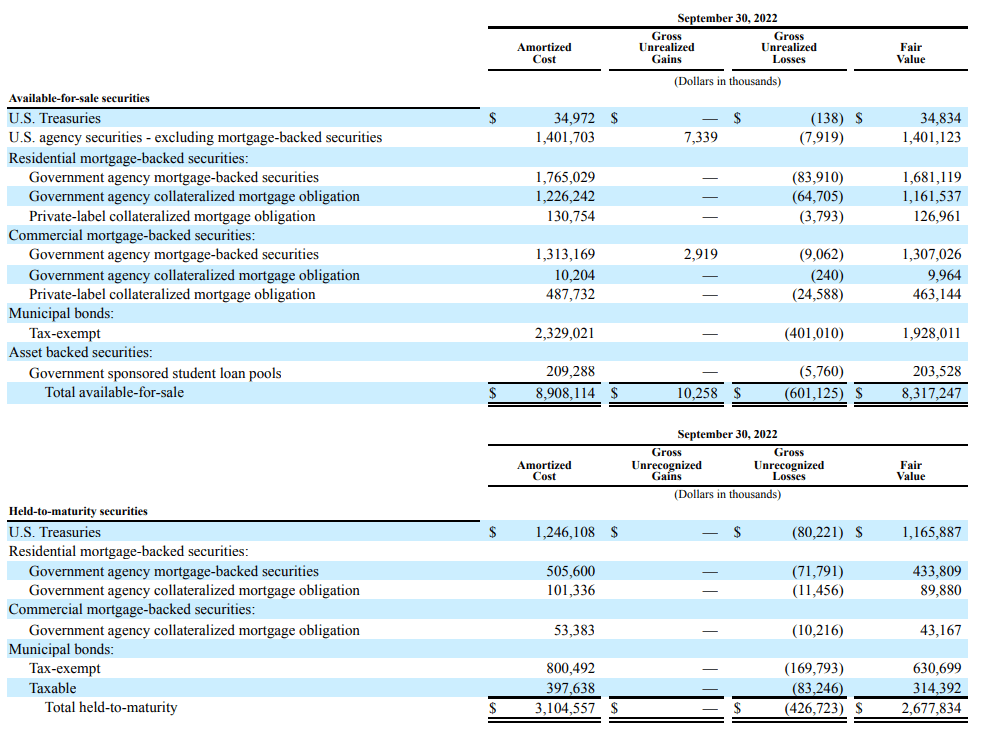

The crucial thing to understand is that Silvergate is a bank. It is regulated as such and below is a note from its Q3 10-Q. At the time it held approximately $11 billion (note that value has very likely fallen, but we’ll get to that) in relatively low-risk debt securities such as Treasury bonds and municipal bonds. Encouragingly, interest rates are rising, and it is not unreasonable to expect the debt portfolio below to have a yield of 3.5%-4% if we look at the current yield curve.

Silvergate securities portfolio (Silvergate 10-Q (Q3 2022))

Deposit Losses

Now, the issue with Silvergate and one reason it has traded off so sharply is that companies like FTX (and also BlockFi) apparently deposited money there. As such it announced in a mid-November update that deposits had declined to $9.8B. Of course, no bank likes to see that. Still it’s understandable in the current crypto winter, various companies that deposited at Silvergate now cease to exist. The impact on Silvergate appears to be that the balance sheet shrinks, they return the deposits to the customer and sell the accompanying assets that the deposits were invested in. Again these assets were typically Treasury bonds and similar, so not hard to do, and typical for a bank.

Net Interest Margin

The net interest margin at Silvergate is compelling. Let’s haircut the recent deposit number to $9B from the mid-November update of $9.8B and assume that they can capture a 4% yield on those deposits, and note they pay out effectively zero interest on deposits (I estimate 0.05% imputed from the last 10-Q, which I will call zero for simplicity), so it’s largely all net interest margin. That represents estimated income of $360M (or $9B x 4%).

Costs

Then the company has run-rate costs of $132M based on the last quarter. That’s mainly the salaries of bank staff. As such $360M-$132M with a tax rate of 20% is $182M of net income. For comparison to our simple calculations, net income for Silvergate was $40M for Q3 2022.

Valuation

Silvergate appears to be very cheap. With a market cap of $530M it’s trading at 2.9x my estimated earnings and a broadly similar PE on trailing earnings 3.0x. It’s also trading at 0.39x book. This is incredibly cheap for a bank. Today the average bank trades at 1.2x-1.4x book and the S&P 500 is trading for around 20x earnings. So it’s not unreasonable that the shares could trade to around 3x-4x their current value, if valuations were to normalize.

Risks And The Bear Case

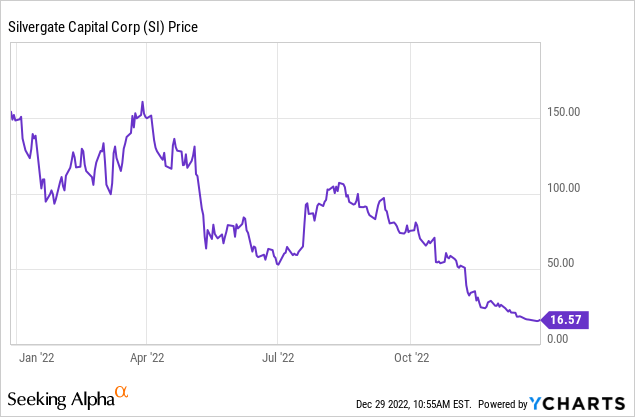

Still there are risks with Silvergate and it has clearly been a great short in 2022 with the shares falling 90%.

- Death of crypto – most depositors at Silvergate are firms involved in the crypto industry, if they cease trading and shrink, then Silvergate’s assets will correspondingly shrink. This has happened in 2022. Recall that deposits declined from $11B at September 30, 2022 to $9.8B in mid-November. It appears a lot of that fall may have been due to FTX with deposits of potentially around $1B, though we don’t know the exact figure. If the crypto industry disappears, then Silvergate is at risk.

- Legal risks – FTX deposited money at Silvergate. This presents some legal risk to Silvergate, it is subject to a class action and has received questions from Senators. This could lead to fines, legal costs and reputational damage. This issue will likely drag on for a while. The main allegation is that Silvergate facilitated transfers from FTX to Alameda. While this appears true in a mechanical sense of a bank letting its client move money, it is unclear that a bank letting its customer transfer funds presents too much legal risk. Yes, of course FTX was behaving in inappropriate ways, but it is not clear how a bank such as Silvergate should have known or prevented that especially when prior to the collapse FTX was generally regarded as a leading firm in the crypto industry.

- Loan losses – Silvergate could also see loan losses. However, it only lends against Bitcoin and appears to do so conservatively.

Sensitivities

For context, if Silvergate were to be fair value at current levels it would have to lose around $800M in legal costs and/or loan losses to cause the current price to reflect its book value. Or alternatively to be trading at around 10x earnings, with a corresponding reduction in net interest margin, it would have to see a decline in deposits to roughly $4.5B or half the level as reported in mid-November, which already reflected FTX outflows. These are not impossible scenarios but do appear extreme.

Unique Assets

Silvergate may also have additional upside. I think for now it’s sufficient to argue that Silvergate is an inexpensive bank. However, the company also has the Silvergate Exchange Network, allowing their clients to easily move money to other clients at the bank. Also, Diem, which may become an interesting crypto payment solution, and was acquired for around $200M. These are both potential sources of further upside, and once the storm clears, means that Silvergate could become an acquisition target. However, you do have to believe that crypto is not dead. Though note that today that Bitcoin trades at over $16,000 with a market cap of over $300B.

It seems fair to argue that Silvergate is not merely a cheap bank but a differentiated one that is well-positioned to capitalize on continuing usage of digital currencies. Again, none of this appears to be reflected in the share price today, and it is not necessary for the investment case to work.

Two Ways To Play This

Then you can either invest in the equity of Silvergate, or own the preferred shares which yield around 11% today and trade at around half their liquidation value of $25. Both appear attractive at current levels.

Conclusion

Despite an awful 2022, the market implies very bad things are in store for Silvergate. This is at a time when net interest margin should increase as interest rates are rising. In order to invest in Silvergate, you must believe that it won’t be subject to large legal settlements and that deposit outflows will not continue at large levels. Also, loan losses must remain moderate, when they have been low so far. I believe there is significant margin of safety here, and though the timing is unclear and legal issues and pessimism on crypto could drag on for months, even years, Silvergate appears to offer an interesting setup for 2023 and beyond.

Be the first to comment