Viorika

Investment Thesis

LendingClub (NYSE:LC) reported uninspiring Q4 earnings, which left investors disappointed. There were two fundamental problems at play.

Firstly, LendingClub’s solid revenue growth days are now in the rear-view mirror. The sort of revenue growth rates that investors become accustomed to in 2022 are not going to repeat in the near or medium-term in my view.

Secondly, its Marketplace volumes appear to be more correlated to the higher interest rate environment than many previously factored in.

Altogether, I continue to argue that investors would do well to avoid this name.

2023 Prospects Are Going to be Challenging

A year ago I suggested that investors should avoid LendingClub and not buy this stock. At the time the stock was at $17.

LC author’s work

And yet, today, the economy is substantially worse. Even though there are notable pockets of strength within the economy, I believe that most even-headed and impartial investors agree that the economic outlook is uncertain and headed for a significant amount of contraction in 2023.

Next, I continue to argue that LendingClub is not a fintech player, but a neobank.

My contention is that this business should be valued very similarly to a bank. The only difference is that it’s less established than some of the bigger banks, so its revenues are going to be more susceptible to the economy and as such more volatile than traditional banks. Let’s continue our discussion of its prospects with this background in mind.

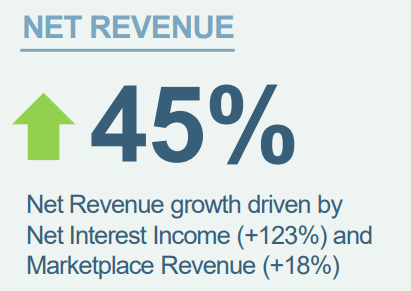

LendingClub’s Revenue Growth Rates Slow Down

LC investor presentation

In the graphic above you see what LC’s full-year net revenue was, a whopping 45% y/y increase. That being said, the vast majority of this growth is now in the rear-view mirror.

Because LC actually ended Q4 with its revenues up 0.2% y/y (no typo). Recall, this revenue had already been guided for back in Q3, so there wasn’t much of a surprise here.

What was surprising is that LendingClub didn’t seem to have enough confidence in its underlying business to guide for the full year as had been its prior practice.

At a time when investors were already feeling shaken with the stock down more than 40% in the past year, this lack of confidence in management’s own outlook will likely not boost investors’ confidence.

The Core Problem: LendingClub’s Flagship Product

LendingClub seeks to dominate the market for unsecured personal loans, to help its members manage their loans, spending, and savings.

LendingClub often describes itself as a hybrid fintech platform with a bank attached. But its crown jewel is its Marketplace platform.

LendingClub’s marketplace is a peer-to-peer lending platform. Arguably, LendingClub’s Marketplace is why investors got involved with LendingClub to start with.

However, the problem now is that LendingClub’s Marketplace total revenue was down 29% y/y. Then, further complicating matters, this revenue stream makes up approximately half of its net revenue.

Consequently, what’s happening within its Marketplace business is that in this higher interest rate environment, higher funding costs for loan investors are slowing down its Marketplace business.

To echo this sentiment, this is what LendingClub stated in its earnings call yesterday,

As we have spoken about for several quarters, the rate environment is putting pressure on marketplace volumes as the relative value we can provide is compressed until we can reprice our loans to reflect the dramatic increase in cost of funds for especially our non-bank investors.

On a positive note, LendingClub has decided that now it will make tough choices including restructuring and reducing its workforce. LendingClub believes that this action could save an annualized figure of approximately $30 million.

The Bottom Line

In summary, clearly for investors, LendingClub poses a fair amount of uncertainty. This business was supposed to be a secular growth opportunity.

Investors weren’t valuing it as a cheap cyclical bank. At a nearly $1 billion market cap, investors likely wanted to see a through the cycle increase in profitability. But this doesn’t appear to be on offer by LendingClub.

I recognize that LC is already trading at a multi-year low, and this could be perceived as the time for bargain hunters to get involved. However, I charge this is not the time to deploy hard-earned capital into LendingClub.

Be the first to comment