Thomas Barwick

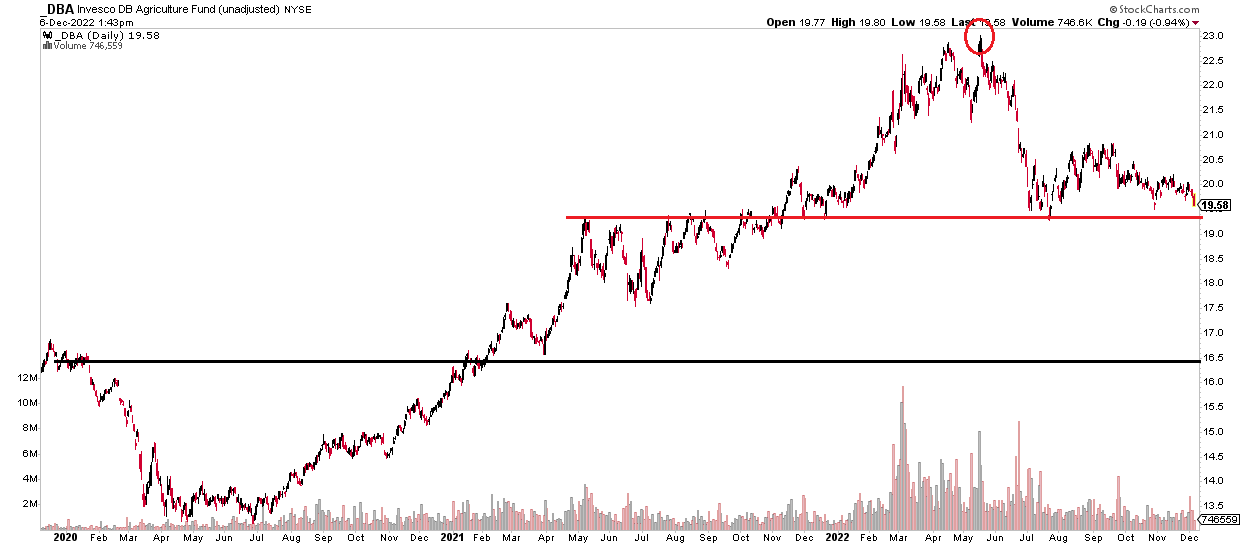

Agricultural commodities are on the brink of a big bearish breakdown. The Invesco DB Agriculture Fund (DBA) hangs just above key support. Should the line break, a bearish price objective to about $16.50 would trigger.

That is a key technical risk for many once-popular ag stocks that have retreated in recent months as inflation fears ease and recession risks rise. One foreign high-dividend name also hangs near critical technical support, but how do the valuation and growth outlooks appear? Let’s dig in.

Ag ETF Nearing A Key Level As Recession Fears Loom

Stockcharts.com

According to Fidelity Investments, ICL Group Ltd (NYSE:ICL) together with its subsidiaries, operates as a specialty minerals and chemicals company worldwide. It operates in four segments: Industrial Products, Potash, Phosphate Solutions, and Innovative Ag Solutions (IAS). The Industrial Products segment produces bromine out of a solution that is a by-product of the potash production process, as well as bromine-based compounds; produces various grades of potash, salt, magnesium chloride, and magnesia products; and produces and markets phosphorous-based flame retardants and other phosphorus-based products.

The Israel-based $11.1 billion market cap Chemicals industry company within the Materials sector trades at a low 5.1 trailing 12-month GAAP price-to-earnings ratio and pays a high 10.6% trailing 12-month dividend yield, according to The Wall Street Journal. The firm recently declared a $0.2435 dividend after reporting a mixed quarter that included a bottom-line beat and top-line miss.

Higher bromine and potash futures would be bullish for ICL, as would a lower US dollar. Immediate concerns are around the ongoing Russia/Ukraine conflict – escalations would support commodity prices in all likelihood, thus providing a tailwind to ICL.

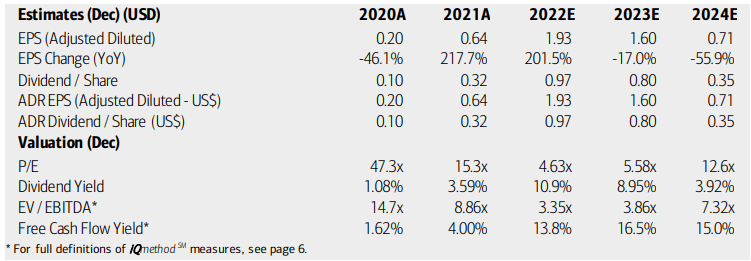

On valuation, ICL’s earnings are volatile with $1.93 of adjusted EPS expected this year, then falling to $1.60 in 2023. More per-share profit declines YoY are expected in 2024, too. Dividends should fall commensurate with profits, as is common with many foreign companies.

Still, the firm’s forward operating and GAAP P/Es look ok, but still low if we assume 2024’s smaller profits. BofA recently reiterated that ICL is a top quant name on its low volatility and high yield list, which is an encouraging sign. With a low EV/EBITDA multiple and high free cash flow yield, the stock earns an A Seeking Alpha valuation rating. I continue to like the valuation near-term, but growth risks should be monitored and the dividend may decline.

ICL: Earnings, Valuation, Dividend Forecasts

BofA Global Research

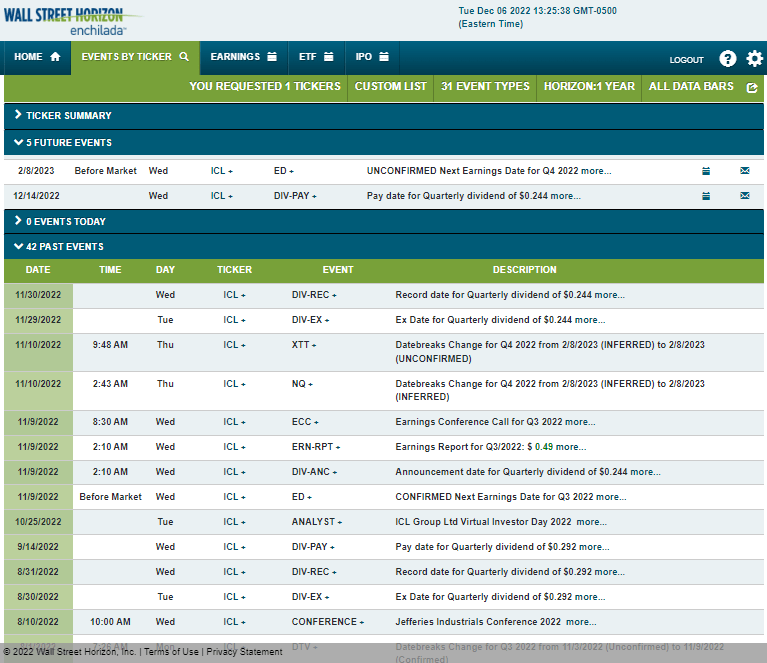

Looking ahead, corporate event data from Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Wednesday, February 8 BMO. Before that, the stock has a dividend pay date of Wednesday, February 14. The calendar is light otherwise.

Corporate Event Calendar

Wall Street Horizon

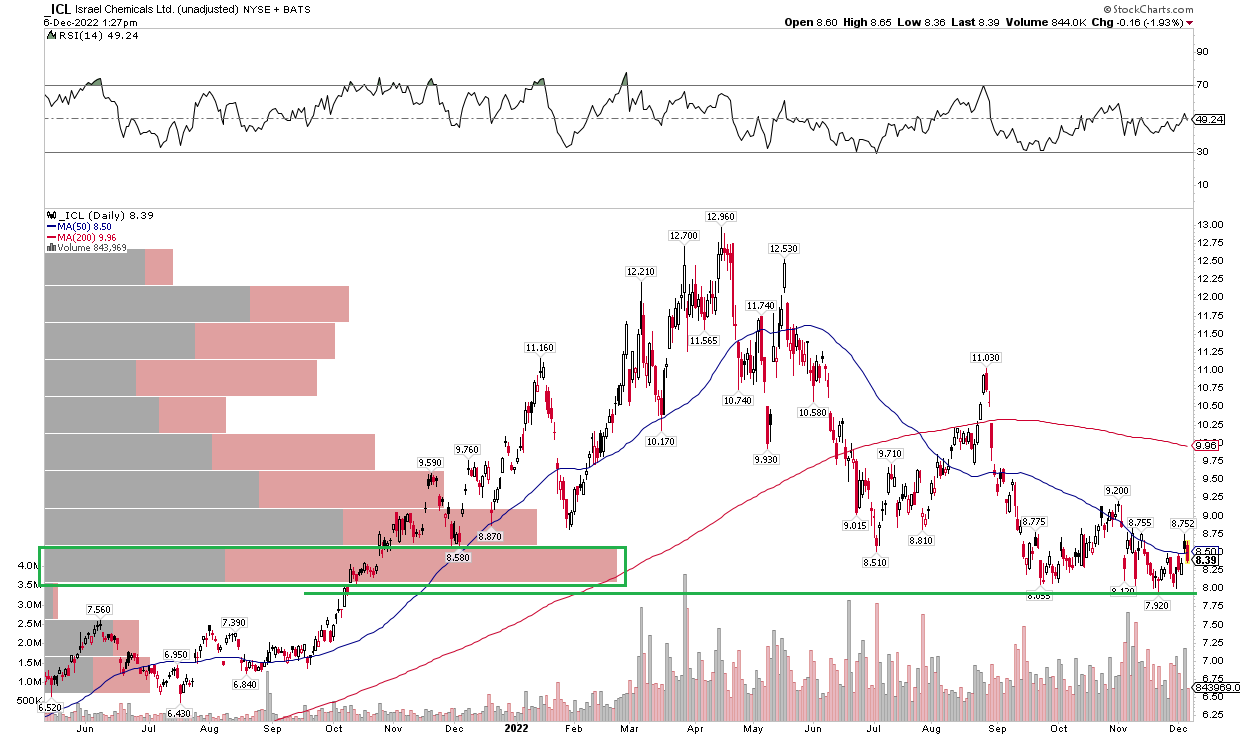

The Technical Take

I continue to see support at the $8 mark on the chart of ICL. It probed under $8 in November, but then rallied to its high from earlier in the month. While there is a pronounced downtrend off the April 2022 high, a long position with a stop near $7.50 is still a good risk/reward.

A recent development, however, is a downtrend support line from the July 2022 low – that could mean a bullish falling wedge may persist further. So, I am less confident about how the chart will go from here. With a declining 200-day moving average, and shares having stalled above $9, the bulls may have their work cut out to take ICL higher with vigor.

ICL: Watching Important support Near $8

Stockcharts.com

The Bottom Line

I’m less excited about ICL given a mixed quarter and uncertain earnings despite a solid valuation and free cash flow that should support the yield for now, but I see downside risks to the payout. The chart has also turned more mixed.

Be the first to comment