Tim Boyle

Hanesbrands Inc. (NYSE:HBI), a consumer goods company, designs, manufactures, sources, and sells a range of basic apparel for men, women, and children.

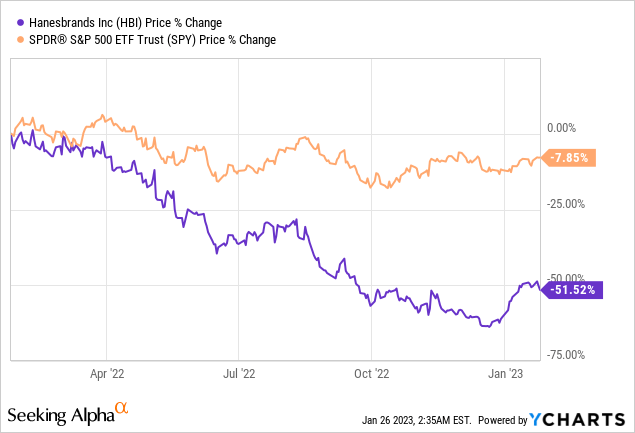

The firm has lost more than half of its market value in the past 12 months, substantially underperforming the broader market.

The primary driver of the poor performance of many firms in the consumer discretionary sector has been the challenging macroeconomic environment. Throughout 2022, the consumer confidence level has hit historic lows, raw material prices and transportation costs have skyrocketed, while the strong USD relative to other currencies has created an unfavourable FX environment for many.

In today’s article, we are going to take a look at how Hanes’ profitability and efficiency has been impacted in the previous years and whether the current valuation is reflective of that.

To do so, we will be focusing on the firm’s return on equity or ROE, which we will be decomposing to three parts, following the DuPont analysis.

Return on Equity

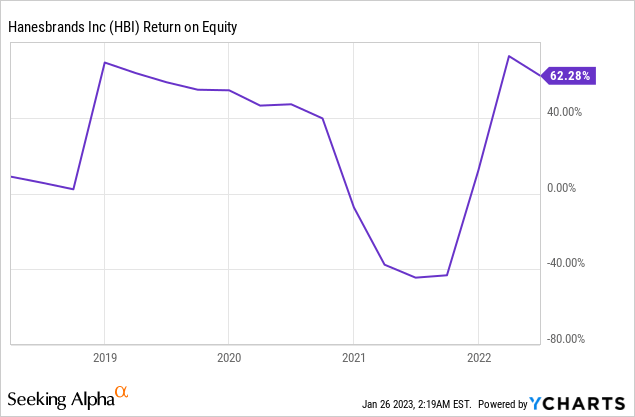

ROE is an important measure of financial performance and it is often used to gauge the corporation’s profitability and its efficiency of generating profits. As investors, we would normally like to see return on equity improving or staying stable over the years. A downward trend can often raise concerns.

While Hanes’ ROE has been trending slightly downwards in 2019 and 2020, it has fallen off the cliff at the end of 2020 and beginning of 2021. However, in the recent quarters ROE has returned back to pre-pandemic levels.

In order to understand what is exactly behind this trend, we need to decompose the ROE measure into three components. These components are: net profit margin, asset turnover and the equity multiplier.

ROE decomposition (investopedia.com)

Net profit margin

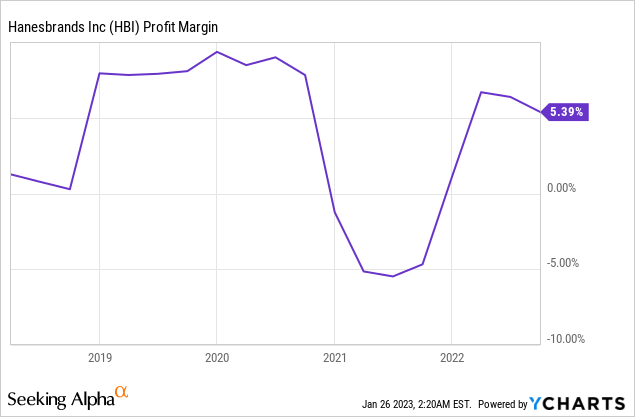

The net profit margin has been relatively stable over the past years, despite the sharp drop in the beginning of 2021. We can already see that this measure is likely to be largely responsible for the observed dynamic in the ROE.

The question that we have to answer, is why has there been this large drop in ROE, and whether the sharp jump back is sustainable or not?

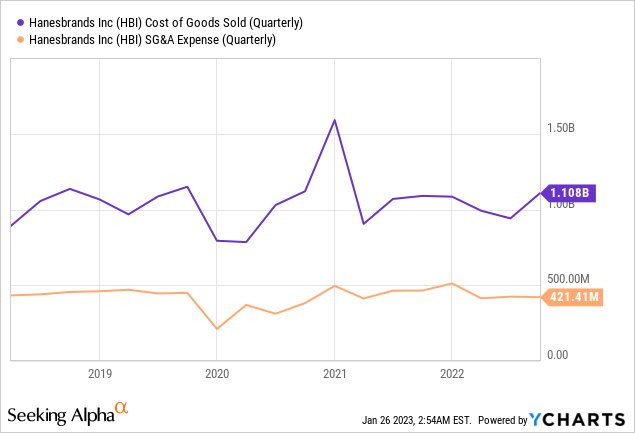

Let us take a brief look at the costs and expenses over this time period. The cost of goods sold have peaked in the beginning of 2021, but have stayed relatively stable during the rest of the period. SG&A expenses have been also managed well, and stayed relatively flat over time.

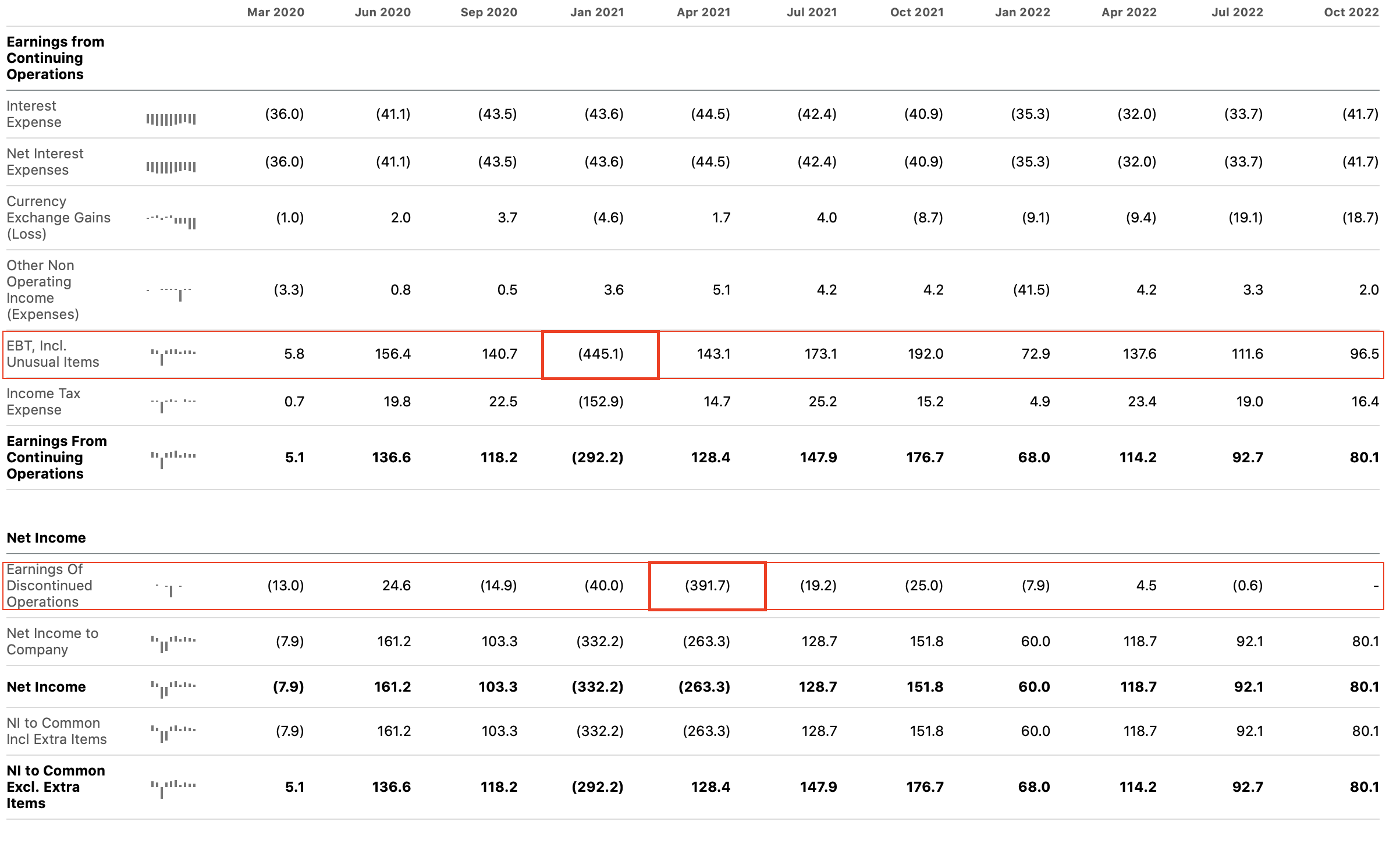

For this reason, we have to look somewhere else for the cause of negative profits in 2021. Looking at the income statement, we can see that unusual items or discontinued operations are responsible for the net margin and ROE volatility.

Income statement (Seeking Alpha)

So why is this all important?

In 2023, we expect the macroeconomic environment to slightly improve. Consumer sentiment is likely to be somewhat better than it was in the previous year, which could benefit firms in the consumer discretionary segment. Also, raw material prices, including oil and gas prices have moderated over the past months, which could benefit the firms on the cost side. Going forward, we believe that HBI’s net profit margin is likely to be sustained or even slightly improved in the next quarters. If adjusting for the unusual items/discontinued operations, Hanes has demonstrated that it can remain resilient, even during times of downturns.

Asset turnover

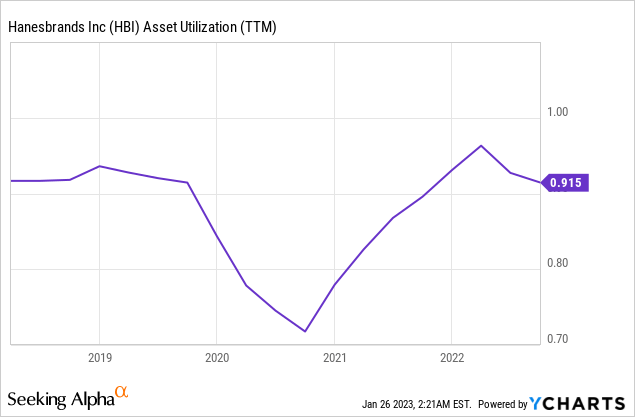

The asset turnover ratio (or sometimes called asset utilisation) measures the value of a company’s sales or revenues relative to the value of its assets. It shows, how effectively the company is using its assets to generate sales. Generally, we would like to see the efficiency improving or staying stable over time. In the case of Hanes, it has stayed relatively flat, despite the decline in the second half of 2020, which has been driven by the decline in revenue.

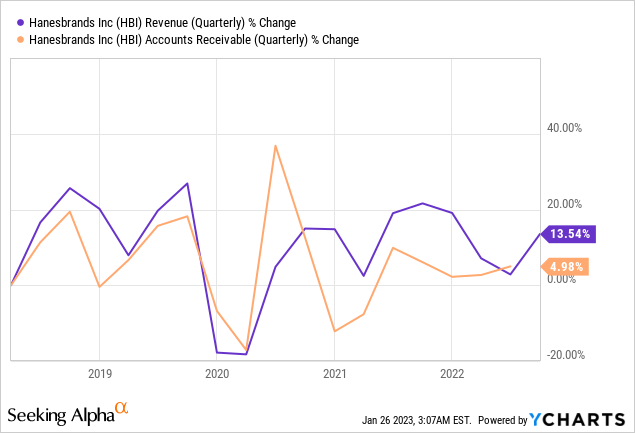

We need to also understand that this is a measure, which can be relatively easily manipulated. If the firm starts to recognise its revenue differently, or starts to sell more on credit, this measure may appear to be stable or improving, while in fact it could be the other way around. When looking at the change of revenue and accounts receivables, we can see that they have been moving together and no sharp increase in accounts receivables is observable. this likely means that HBI has not been trying to manipulate its sales figures.

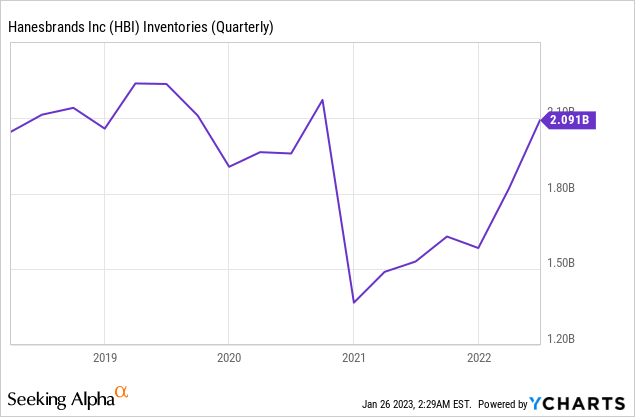

And at the same time, their inventory levels have been also well managed.

From this perspective, we believe that HBI’s efficiency is likely to remain stable in the coming quarters as it has been in the recent years.

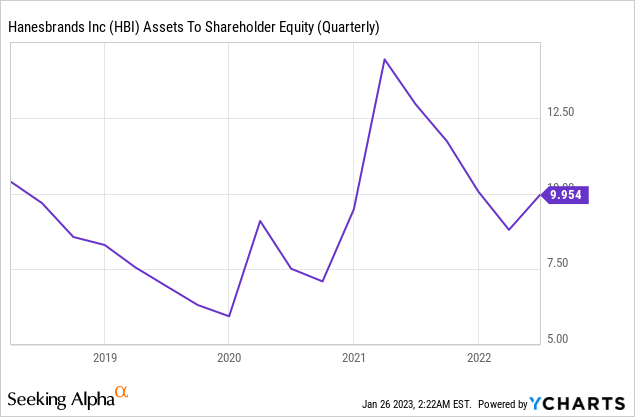

Equity multiplier

The last part of the three step decomposition of the ROE is the equity multiplier, which is simply the ratio of assets to shareholder equity. A higher ratio indicates more leverage, meaning that the firm is using a larger amount of debt to finance its assets.

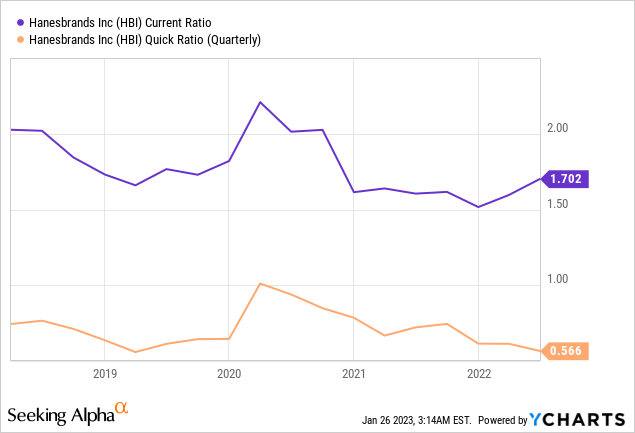

Despite the volatility, this ratio is also currently around the pre-pandemic levels. However, this is a metric that we would like to see slightly improving. The current- and the quick ratio are liquidity ratios, indicating whether the firm has enough current assets to meet its current liabilities. We would ideally like to see both of these above 1.

While the quick ratio has been below 1, historically, it has usually been slightly high than the current reading.

So the main question comes now, shall we invest in HBI’s stock based on its profitability and efficiency?

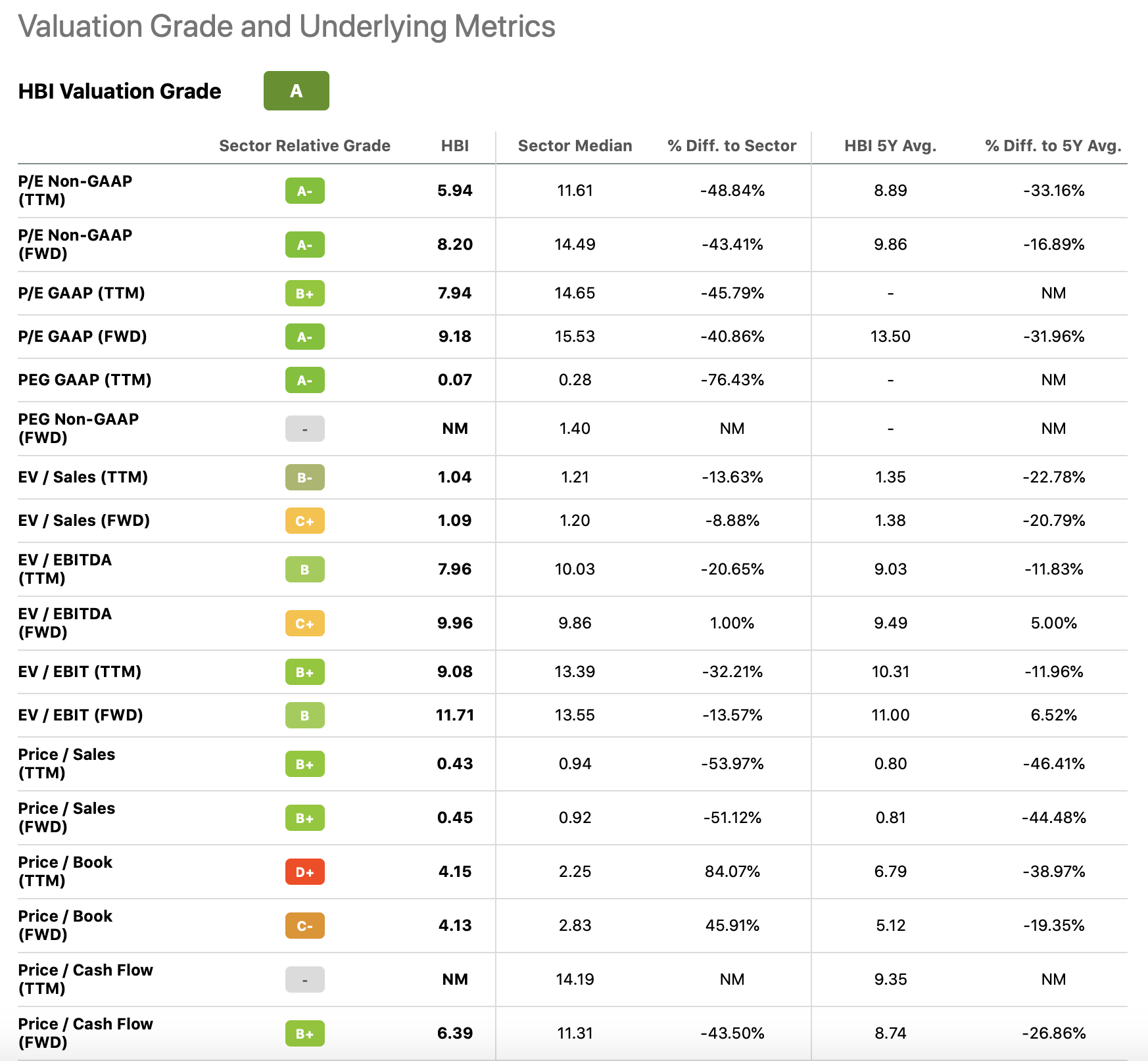

Valuation

To answer the question we have to understand the valuation and the returns to shareholders.

Valuation metrics (Seeking Alpha)

According to most of the traditional price multiples, Hanes is selling at a significant discount compared to the sector median, and also compared to its own 5Y averages. At the same time, the firm’s profitability and efficiency has not severely declined and also the macroeconomic environment seems to be improving. For these reasons, we believe that this discount may appear to be an attractive buying opportunity.

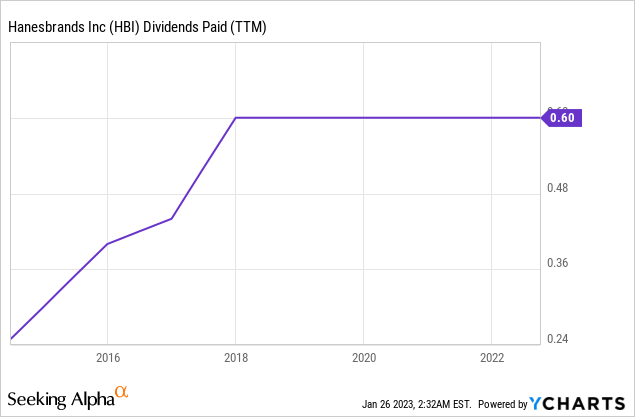

Further, the firm has also been rewarding its shareholders with dividends over the past 9 years, although the dividends have not increased lately.

Although the payout ratios are somewhat high, they appear to be sustainable.

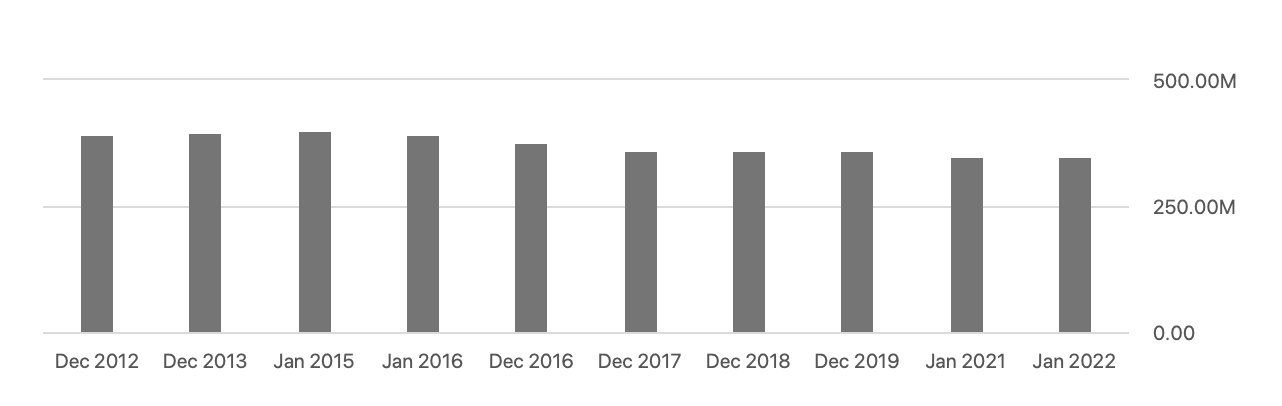

Dividends have not been the only source of return however; the firm has also kept purchasing its shares back over the last decade.

Shares outstanding (Seeking Alpha)

While the firm may not be growing, we believe it could be an attractive holding in a diversified portfolio. The valuation, along with the returns to shareholders appear attractive, while the efficiency and the profitability of the company has been staying relatively stable over the past years, despite the macroeconomic challenges.

For these reasons, we rate HBI’s stock as “buy”.

Be the first to comment