Michael M. Santiago/Getty Images News

Based on Q4’22 results by Mobileye Global (NASDAQ:MBLY), the split from Intel (INTC) has been very productive. The ADAS company reported strong growth to end the year and saw healthy additional customer interest following the media attention on the IPO. Unfortunately though, my investment thesis remains Bearish on the stock trading at a premium valuation in a tough market for technology stocks.

Business Ramp To Slow

Mobileye is no doubt in the middle of a promising ramp in spending in the auto tech sector. The company saw Q4’22 revenues surge 59% YoY to $565 million.

Beneath the surface though, the numbers were a little skewed in the quarter. On the Q4’22 earnings call, Mobileye discussed a pull forward in demand due to higher EyeQ chip prices in 2023 and a lack of SuperVision chip supply in the 1H of the year leading to lower revenues in both Q1 and Q2.

In fact, Mobileye only guided to 2023 revenues of $2.237 billion at the midpoint when the Q4 run rate was already up at $2.356 billion. The ADAS leader won’t generate much revenue growth throughout the year after a big end to 2022.

Long term, the business is very promising. The company now has a massive order pipeline with $6.7 billion worth of design wins in 2022 while Mobileye only generated $1.9 billion worth of revenues for a 3.5x multiple.

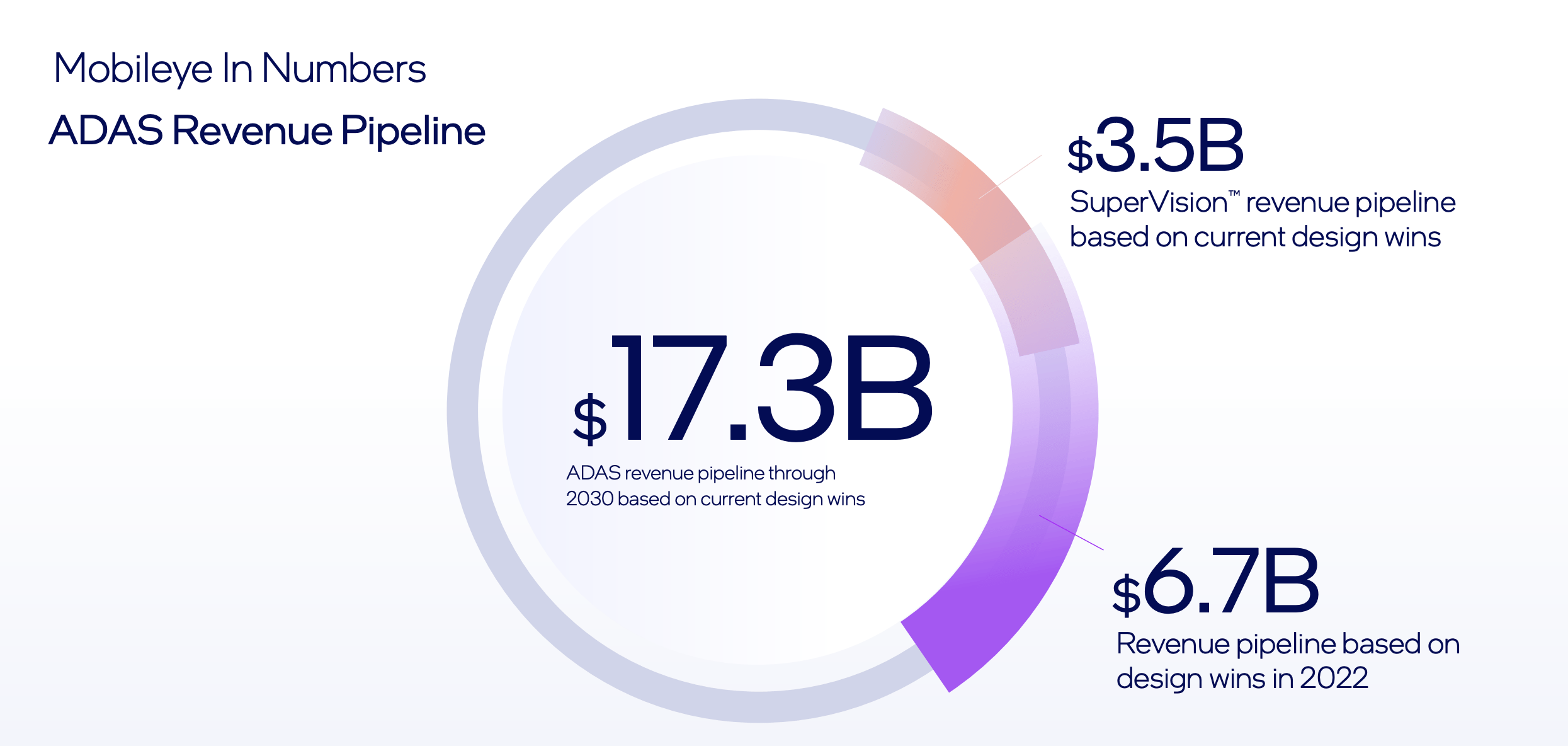

Source: Mobileye CES 2023 presentation

The auto tech company has an impressive order book through 2023 of $17.3 billion per the presentation back at CES. In addition, this amount doesn’t apparently include $1.5 billion in consumer AV line of sight revenues from a single program starting in 2026 and another $3.5 billion from autonomous MaaS revenue pipeline through 2028 from 3 top partnerships.

The company has a strong pipeline due to additional content on new vehicle models in a positive sign Mobileye can grow without needing vehicle growth. The average system pricing in Q4’22 was $56.20, up from $48.30 last Q4.

The CEO sees the ending 2023 chip price at over $60 with a long-term move to over $100. Per Amnon Shashua on the Q4’22 earnings call, the design wins last year averaged $105 in content:

In terms of future business generation, 2022 was a record year. Just in that year alone, we generated new business representing $6.7 billion of estimated future revenue at about $105 per unit on a content per car blended basis. This is about 3.5 times our actual revenue in 2022 and double our current ASP.

Mobileye doesn’t lack any long-term revenue growth opportunity. Also, the company is already solidly profitable and generated an impressive $546 million in operating cash flows in 2022.

Unlike most independent auto tech companies, Mobileye is both profitable and has a strong cash balance sheet with a cash balance of $1.0 billion. The problem here is a stock valuation already up at nearly $30 billion.

Too Rich

The stock trades at nearly 14x 2023 sales targets. Mobileye trades at 50x EPS targets. Neither number is absurdly egregious, but the stock just doesn’t offer any upside from these levels and Intel could pressure the stock by unloading more shares after reporting a horrible quarter after the close with signs of substantial cash burn.

Even just looking at the order book increase of $6.7 billion for the year, the stock trades at 4.5x those future sales. The stock definitely deserves a premium multiple based on this large order book, but investors would have to pay up to 15x sales targets in order for Mobileye to produce a solid return for investors in 2023.

As the company reports sequential sales declines to start the year, the stock is likely to dip in 2023. Investors should look to purchase Mobileye on any major dip.

Takeaway

The key investor takeaway is that Mobileye has an impressive order book setting the company up for massive growth in the decade ahead. Unfortunately, the stock is already priced for the growth of the next few years trading at premium multiples already.

Investors are best to wait for the sequential revenue declines in the 1H of 2023 to hit the stock before investing for the long-term growth story.

Be the first to comment