Leonid Sorokin

Introduction

I’ve written about Global Tech Industries Group (OTCQB:GTII) two times on SA so far, the latest of which was in September. Back then, I said that its business ventures hadn’t performed well over the past 18 months and that it could be a good time to open a small short position.

Well, the past few months have been eventful for the company with the highlights including a FINRA inquiry into the decrease of the strike price of the 2021 warrants, a listing on a blockchain-powered securities exchange called Upstream, and the launch of an investigation into possible naked short selling. In addition, GTII released its Q3 2022 financial results, and I think they look underwhelming. Let’s review.

Overview of the recent developments

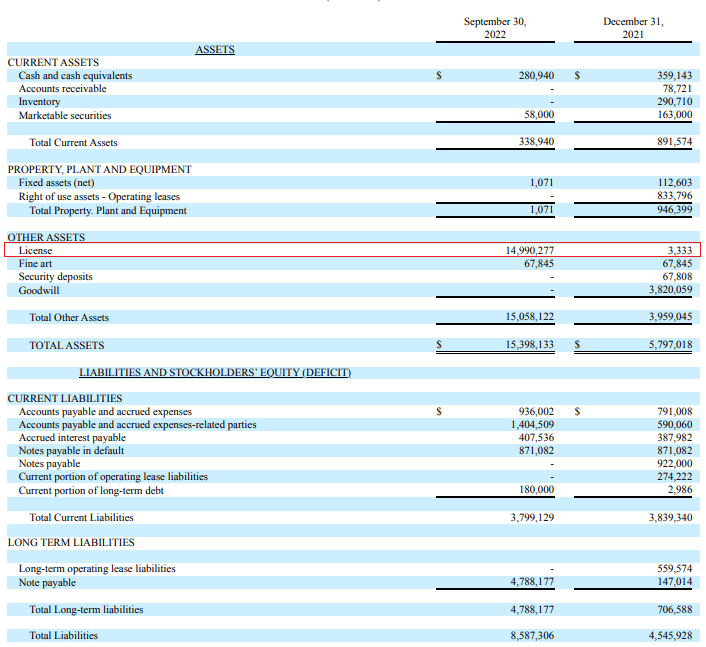

In case you haven’t read any of my previous articles about GTII, here’s a quick description of the business. The company describes itself as a “mini conglomerate” with subsidiaries and affiliates involved in intellectual properties, proprietary systems, and trade secrets in bioscience, green-tech, and global health technologies. Over at SA, the company was described as a crypto exchange in early May as it declared a special dividend payable in Shiba Inu (SHIB-USD) tokens. Looking at the Q3 2022 financials, there’s not much to talk about as GTII had no revenues and a license accounted for $14.99 million the $15.4 million total assets as of September.

Global Tech Industries Group

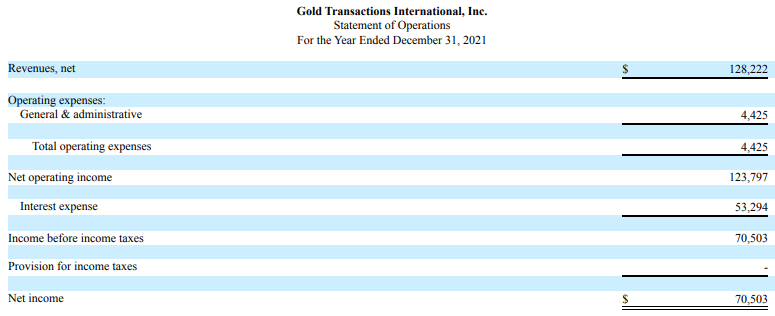

This is a license that the company got in June through the purchase of gold trader Gold Transactions International which gave it access to a network that buys gold from artisan miners internationally and then provides transportation, assaying, refining, and storage services to a free trade zone in Dubai. I doubt it has much value considering the gold trader had revenues of just $0.13 million and a net income of $0.07 million in 2021.

Global Tech Industries Group

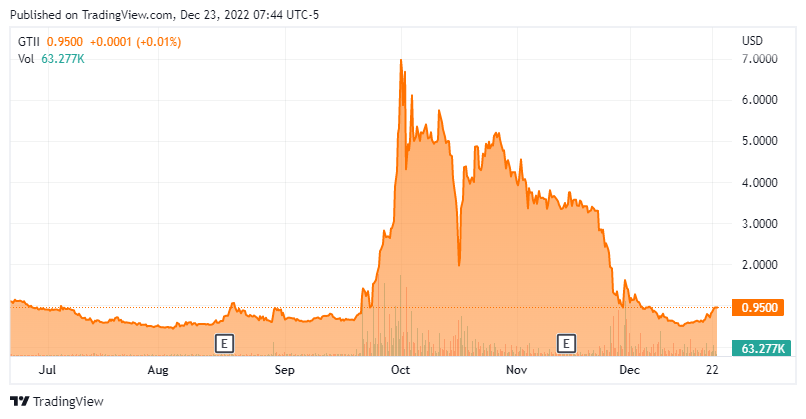

Turning our attention to the Shiba Inu dividend, GTII revealed in its Q3 2022 financial report that the Depository Trust & Clearing Corporation has declined to facilitate or process the distribution of the tokens and FINRA determined that the request to pay this dividend was deficient (see page 22 here, not that Shiba Inu seems to be misspelled as Shibu Inu). In my view, this dividend is immaterial considering those billion Shiba Inu coins are worth just $8,318 as of the time of writing. Yet, GTII seems determined to distribute a digital dividend. The company mentioned once again in its quarterly report that it plans to digitalize two pieces of art that it bought for $67,845 and issue an NFT to shareholders as a dividend, although there is no clear timetable for when this might happen (see page 13). And on November 13, GTII announced that it’s listing on the Upstream platform after searching for a way to deliver a digital dividend to its shareholders since spring. The other expected positives of this move include a broader reach and wider audience, but I expect the effects to be inconsequential. After all, it’s a new app powered by the Ethereum blockchain with a low number of downloads. Besides, the daily trading volume on the OTC has usually been above 1 million shares since late September when the market valuation of GTII started soaring.

Seeking Alpha

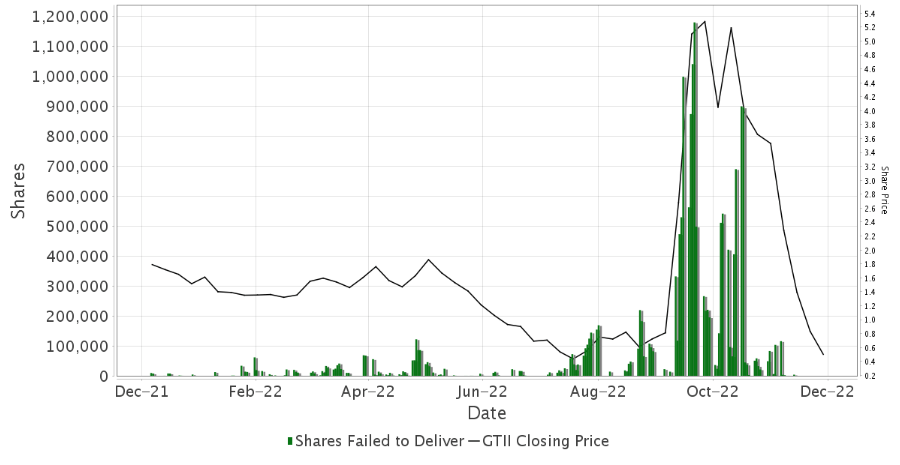

Speaking of which, the company said on October 6 that it believed its market valuation was rising mostly due to more buyers entering the market as the share price came close to the $2.00 strike price for its 2021 warrants. On September 27, GTII decided to lower the strike price from $2.75, saying this was a way to reward its loyal shareholders with an opportunity to participate at a lower price. GTII gave up on the idea just a few days later but unsurprisingly FINRA decided to launch an inquiry into the whole operation. Yet, the share price went below the $2.75 level over three weeks later which raises doubts about the theory that the market valuation was rising due to more buyers entering the market. The share price movements over the past two years have been erratic and on November 30, GTII announced that it decided to hire a law firm to investigate the matter as it believes it may have been the target of a market manipulation scheme involving naked short selling. Naked short selling includes short selling shares that have not been affirmatively determined to exist and it’s illegal. This may result in the failure to deliver the shares and can artificially drive a stock’s price down as well as impact its liquidity. In essence, you owe the shorted shares to the buyer but fail to deliver. While there was a significant number of failure to deliver events over the past few months, it’s worth noting that many of them occurred while the share price of GTII was rising. The chart below shows the combined figure that includes both new fails on the reporting day as well as existing fails.

Fintel

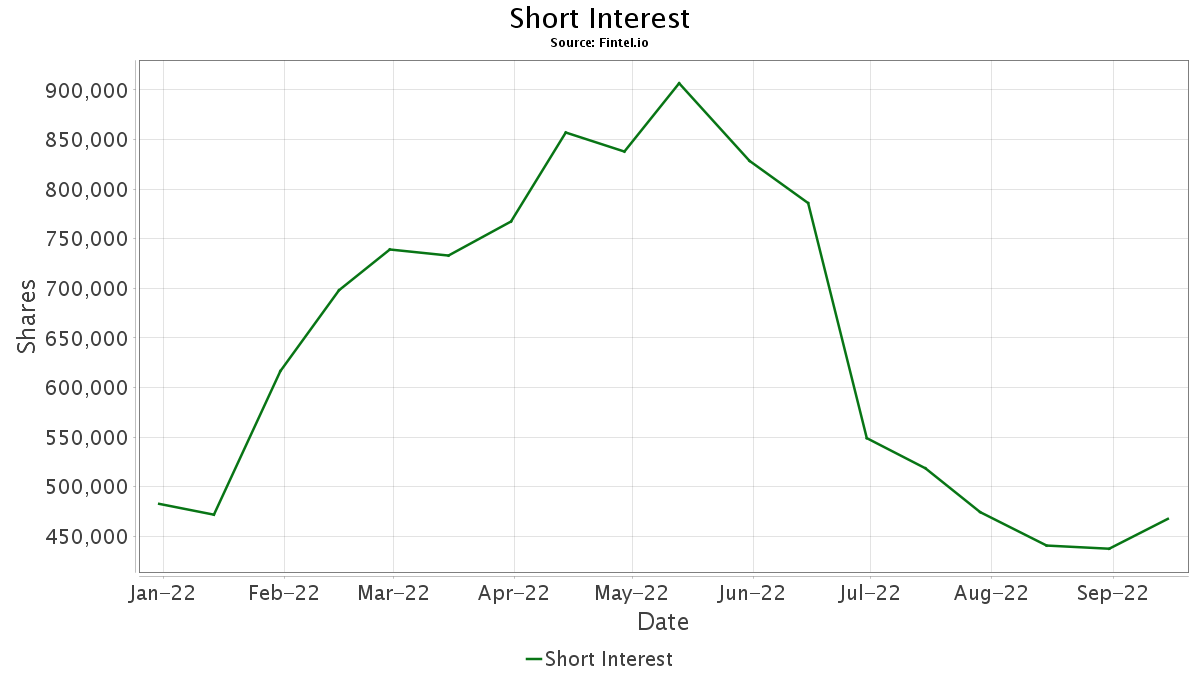

In my view, it’s unlikely that there has been a significant amount of naked short selling here as the short interest has usually been relatively low, well below the daily trading volume.

Fintel

Investor takeaway

Overall, I think Q3 2022 was another disappointing quarter for GTII investors from a financial point of view as the company still had no revenues and liabilities continued to pile up. I think that the situation is dire as GTII revealed it didn’t have enough cash to pay its officers their wages in cash (see page 13). There was a working capital deficit as of September and the tangible book value was in the red. In my view, the listing on Upstream and the investigation into naked short selling are unlikely to boost investor interest.

So, how do you play this? Well, I think that the best course of action could be to avoid this stock. In my view, the time for short selling has passed as the share price has decreased significantly since late November, and data from Fintel shows that the short borrow fee rate stands at 83.83% as of the time of writing.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment