onurdongel

On Wednesday, January 18, 2022, Kinder Morgan, Inc. (NYSE:KMI) announced its fourth quarter 2022 earnings results. At first glance, these results were not particularly impressive. Kinder Morgan missed the expectations of its analysts in terms of revenues. Although it did beat on earnings, it was only by $0.01 per share so it is nothing to write home about.

This does not counter the thesis that we have long presented for Kinder Morgan, however, as the company continues to have the characteristics that make it an excellent dividend stock. In particular, Kinder Morgan enjoys remarkably stable cash flow, which we can see reflected in the earnings results. The company is likely to be able to maintain this stability going forward along with some growth as we enter 2023, and so it continues to be a core holding of our energy income portfolios.

Results And Growth Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Kinder Morgan’s fourth-quarter 2022 earnings report:

- Kinder Morgan reported total revenues of $4.579 billion in the fourth quarter of 2022. This represents a 3.48% increase over the $4.425 billion that the company reported in the prior year’s quarter.

- The company reported an operating income of $1.104 billion in the most recent quarter. This compares quite favorably to the $950 million that it reported in the year-ago quarter.

- Kinder Morgan transported an average of 40.072 trillion BTU of natural gas per day during the reporting period. This represents a 4.01% increase over the 38.527 trillion BTU of natural gas per day that the company transported on average in the equivalent quarter of last year.

- The company reported a distributable cash flow of $1.217 billion in the most recent quarter. This represents an 11.34% increase over the $1.093 billion that the company reported last year.

- Kinder Morgan reported a net income of $670 million in the fourth quarter of 2022. This represents a 5.18% increase over the $637 million that the company reported in the fourth quarter of 2021.

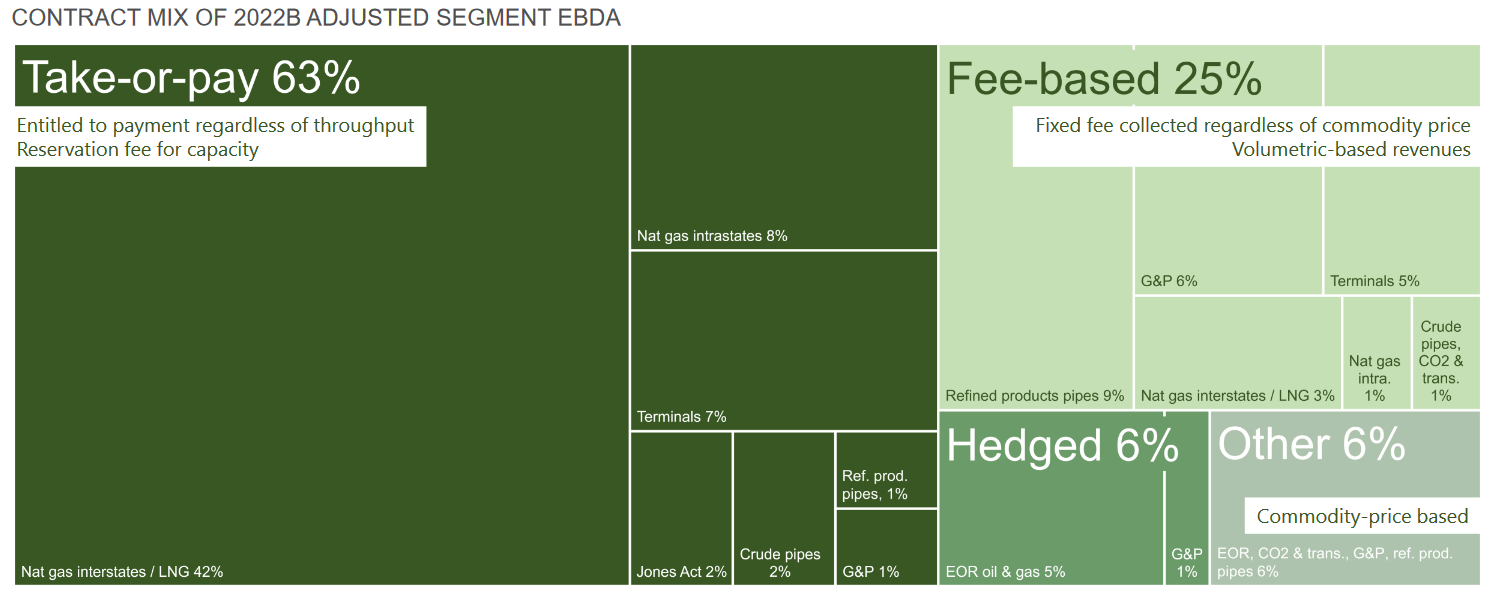

It seems essentially certain that the first thing that anyone reading these highlights will notice is that essentially every measure of financial performance improved compared to the prior year’s quarter. One of the biggest reasons for this is that Kinder Morgan transported more natural gas through its infrastructure network. We can see that in the highlights just above. The reason why this results in improved financial performance is because of the business model that the company uses. In short, Kinder Morgan enters into long-term contracts with its customers under which the customer sends natural gas, crude oil, and refined products through Kinder Morgan’s pipeline network. The customer is then charged based on the volume of resources that are moved through the system, not on their value. In fact, approximately 88% of Kinder Morgan’s cash flow comes from these volume-based contracts:

Kinder Morgan

This is what provides the cash flow stability that we appreciate with this company. After all, the volume-based business model provides Kinder Morgan with a great deal of insulation against a decline in resource prices. The contracts also specify certain volumes that the customers have to send through the network, which protects Kinder Morgan against volume declines that might accompany a weak energy price environment. We can see the general stability reflected in the highlights above as most of the company’s financial figures improved year-over-year, but they certainly did not show the kind of growth that we might expect from a company in the technology sector.

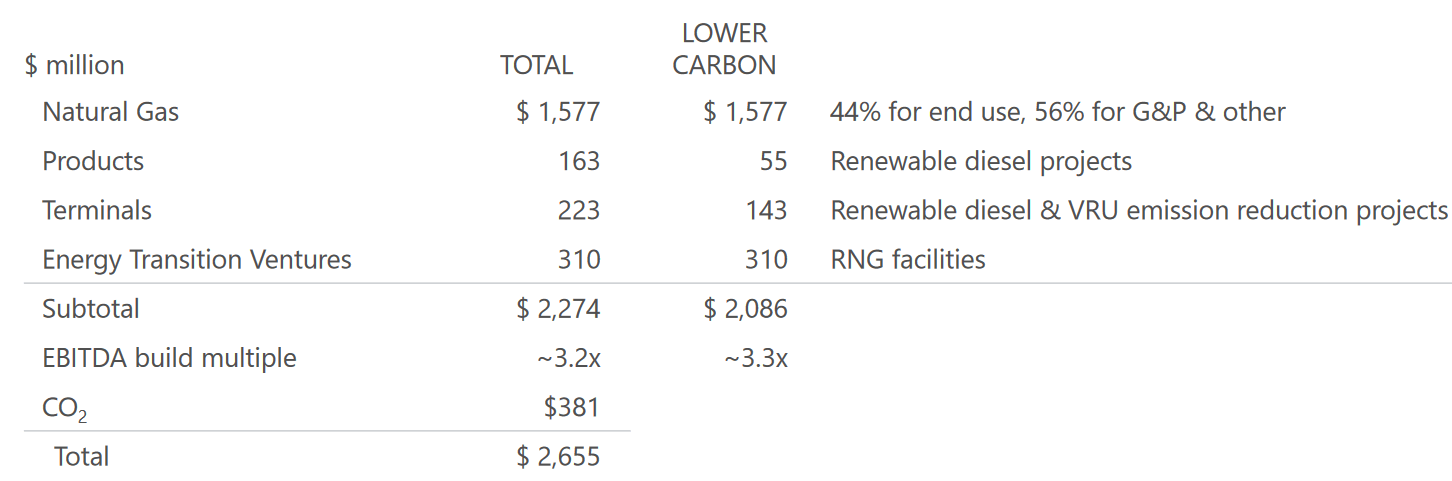

As investors, mere stability is not sufficient to hold our interest. After all, Kinder Morgan’s 6.05% current yield is nice but a regular money market account is now yielding over 4%. Thus, the dividend alone is no longer sufficient reason to hold the stock. Fortunately, Kinder Morgan is positioned to deliver growth going forward, the early stages of which were reflected in the company’s year-over-year numbers. The way for the company to generate growth is to increase the volume of resources that it can transport. This seems only logical given its business model. The company is in the process of doing exactly that as it currently has $2.655 billion worth of new infrastructure currently under construction:

Kinder Morgan

The construction of new infrastructure is necessary for the company’s growth because of a very simple reason. A pipeline, terminal, or storage facility is only capable of handling a limited quantity of resources, Thus, in order to increase its capacity, the company needs to construct new infrastructure. The projects that Kinder Morgan currently has under construction will mostly come online in 2023, although it does have a few that come online later than that.

The nice thing about all of the company’s current growth projects is that Kinder Morgan has already secured contracts from its customers for their use. This has the advantage of ensuring that Kinder Morgan is not spending an enormous amount of money to construct infrastructure that nobody wants to use. The company also knows in advance exactly how profitable each of these projects will be before it begins construction on them. This is nice because it ensures that Kinder Morgan will realize a sufficient return to justify its investment in the new project.

In this case, the company’s projects will generate sufficient EBITDA to pay for themselves in about 3.2 years. This is a very good figure that is much more attractive than the 6-year payback period that The Williams Companies (WMB) has for its current growth projects. Kinder Morgan thus seems to be generating much higher returns on its invested capital than its peers, which ultimately benefits shareholders.

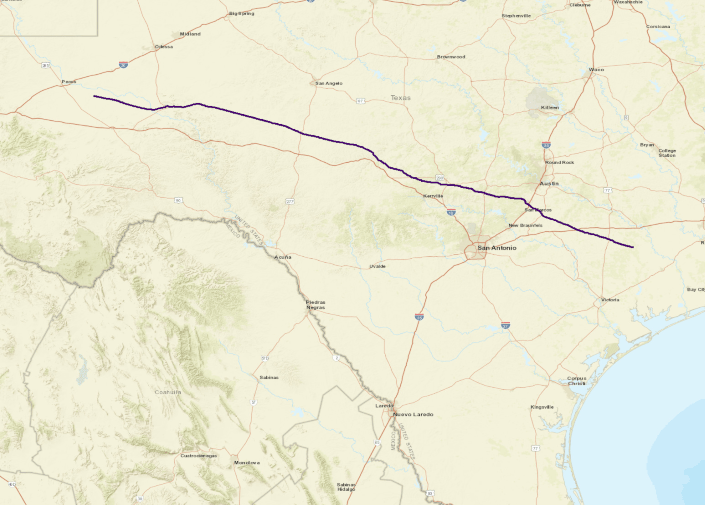

Kinder Morgan made a great deal of progress on some of its growth projects during the fourth quarter. One of these is the expansion of the Permian Highway Pipeline system, which I have discussed in a few recent articles. The Permian Highway Pipeline is a 430-mile natural gas pipeline system that is capable of carrying approximately 2.1 billion cubic feet of natural gas per day from the Waha Hub in West Texas to the Gulf Coast:

Kinder Morgan

The project that Kinder Morgan is currently working on is intended to increase the capacity of this pipeline by 550 million cubic feet per day, bringing its total capacity to approximately 2.65 billion cubic feet of natural gas per day. This is in direct response to the rising production of and demand for natural gas in the United States and around the world. Indeed, the Energy Information Administration states that the production of natural gas in the United States will grow faster than demand in 2023. This surplus gas will be going to various markets around the world such as Europe and Asia, which have been seeing their demand for natural gas soar. I discussed this in a recent article.

During the fourth quarter of 2022, Kinder Morgan worked on acquiring the land and securing contractors in order to allow the construction of the pipeline expansion to begin. The company projects that it will be able to get a higher capacity in operation by November of 2023. Thus, we should see the impact of this project reflected in the company’s fourth quarter 2023 earnings results. That would therefore result in that quarter showing some year-over-year growth, which is always nice to see.

Another one of the company’s growth projects that it made some progress on during the fourth quarter was the expansion of the Tennessee Gas Pipeline System. This is one of the largest natural gas pipeline systems in the United States, running from the Gulf Coast all the way up to Pennsylvania. The system carries natural gas to supply West Virginia, New Jersey, New York, and New England. As I mentioned in an article here at Energy Profits in Dividends a few years ago, New England’s natural gas demand is rising quickly as the region attempts to transition away from fuel oil for home heating. The same is true in New York City.

Thus, we can see why this pipeline system is important and why increasing its capacity represents an opportunity for Kinder Morgan. In order to exploit this opportunity, Kinder Morgan has agreed to increase the capacity of this system in order to supply 115 million cubic feet of natural gas per day to Consolidated Edison (ED), which will use the natural gas to supply its customers primarily in New York City. During the fourth quarter, Kinder Morgan began construction on two of the three compression stations that it requires to satisfy the contract with Consolidated Edison and should be applying for a permit to construct the third within the next few months.

Assuming that there are no problems with obtaining the permits from the Federal Energy Regulatory Commission, Kinder Morgan expects to have this expansion project online by the middle of the fourth quarter of 2023. Thus, we will have a second source of growth coming online at that time, providing Kinder Morgan with a further source of growth at that time.

Financial Analysis

As I have mentioned in various previous articles, Kinder Morgan employs somewhat more leverage than many of its peers, which is something that has always concerned me a bit. The reason for this is that debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt in order to repay the existing debt. This can cause a company’s interest expenses to increase following the rollover depending on the conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline may push it into financial distress if it has too much debt. Although a midstream energy company like Kinder Morgan tends to enjoy remarkably stable cash flows as we already discussed, bankruptcies have still occurred in the sector so this is a risk that we should not ignore.

The usual metric that we use to analyze a midstream company’s debt level is the leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us how long (in years) it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. As of the close of the fourth quarter of 2022, Kinder Morgan had a leverage ratio of 4.1x based on its twelve-month trailing adjusted EBITDA. This is a very good ratio for Kinder Morgan as it represents a significant improvement from the 4.5x ratio that the company has had in past quarters. However, it is still not as good as the sub-4.0x ratio that peer companies like MPLX (MPLX) possess. I generally like to see this ratio below 4.0x in order to add a margin of safety to the investment and unfortunately, we can see that Kinder Morgan is not there yet. However, analysts generally consider anything under 5.0x to be acceptable and Kinder Morgan more than satisfies that requirement. Overall, the company is probably fine with its current leverage, but I would still like to see it get its leverage ratio down to 4.0x.

Dividend Analysis

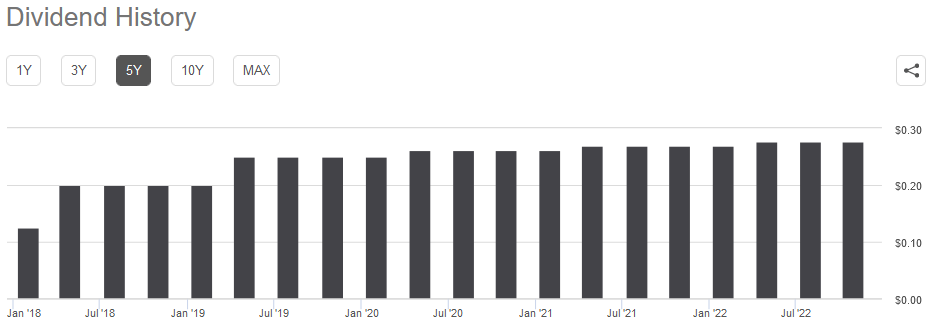

Kinder Morgan has long been a core holding in an energy income portfolio, which is partly due to the historically high yield that the company has paid out. As of the time of writing, Kinder Morgan boasts a 6.05% yield, which is substantially higher than the 1.61% yield of the S&P 500 Index (SPY). Unfortunately, Kinder Morgan cannot match the 7.43% yield of the Alerian MLP Index (AMLP), which contains many of its peers. Kinder Morgan does have a long history of dividend growth, however, and it is one of the midstream companies that was not forced to reduce its dividend back in 2020. This is something that many investors will likely find appealing:

Seeking Alpha

The company held its dividend steady for the fourth quarter of 2022 at $0.2775 per share, but Kinder Morgan usually increases its dividend along with its first quarter announcement so this is not exactly unexpected. The fact that the company does historically increase its dividend annually is something that is very nice to see in today’s inflationary environment. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as though we are getting poorer and poorer with time, which is an especially big problem for someone that is depending on their portfolio for income such as most retirees. T

he fact that Kinder Morgan increases the amount that it pays us annually helps to offset this effect and maintains the purchasing power of the dividend that we receive from the company. As is always the case, though, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to find ourselves the victims of a dividend cut since that would both reduce our incomes and almost certainly cause the company’s unit price to decline.

The usual way that we determine a midstream company’s ability to carry its dividend is by looking at its distributable cash flow. The distributable cash flow is a non-GAAP metric that theoretically tells us the amount of cash that was generated by a company’s ordinary operations and is available to be paid out to the common stockholders. As stated in the highlights, Kinder Morgan had a distributable cash flow of $1.217 billion during the fourth quarter of 2022. This works out to $0.54 per share but the company only declared a dividend of $0.2775 per share. Thus, its cash flow is sufficient to cover its dividend 1.95 times over. This is a very respectable coverage ratio that is easily in line with or better than the strongest companies in the industry. Analysts generally consider anything over 1.20x to be reasonable and sustainable over the long term. I am more conservative and like to see this ratio above 1.30x in order to add a margin of safety to the investment. As we can easily see, Kinder Morgan more than meets these requirements. The dividend should overall be quite secure today.

Conclusion

In conclusion, Kinder Morgan, Inc.’s fourth-quarter earnings results continue to show its worth as a core holding in any energy income portfolio. The company posted year-over-year growth in every relevant metric and looks likely to continue that growth trajectory over the next twelve months. In fact, it has a number of projects coming online that should ensure that it generates that growth along with a fairly high rate of return.

Kinder Morgan, Inc.’s 6.05% yield is a bit lower than some of the other companies in the sector, but the dividend growth should ensure that anyone buying today will soon be receiving a much higher yield-on-cost. Overall, our thesis for Kinder Morgan remains intact and the company earns itself a place in any portfolio.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment