IvelinRadkov

By Rob Isbitts.

Strategy

Schwab U.S. Broad Market ETF (NYSEARCA:SCHB) tracks the Dow Jones U.S. Broad Stock Market Index. The index includes the largest 2,500 publicly traded U.S. companies. This represents the vast majority of the U.S. stock market’s total capitalization.

Proprietary ETF Grades

-

Offense/Defense: Offense

-

Segment: Broad Equity

-

Sub-Segment: US Large Cap

-

Correlation (vs. S&P 500): Very High

-

Expected Volatility (vs. S&P 500): Similar.

Holding Analysis

SPHB holds the S&P 500 (SP500) stocks, plus roughly 2,000 more. This produces a portfolio that looks very much like the S&P 500, in terms of sector weightings and valuation ratios. Small cap and Micro cap stocks, which do not factor into the S&P 500, represent a modest 8% of SCHB.

Strengths

SCHB acts a lot like an S&P 500 ETF. It is Large Cap-focused and liquid. It is a huge exchange-traded fund (“ETF”), with nearly $20 Billion in assets. And it is a dirt-cheap index tracker at 3 basis points. All of those are positives if that’s what an investor is looking for. However, it is probably much more than many investors need.

Weaknesses

However, after so many years of dominance by the largest companies, and so much money pouring into S&P 500 Index funds, those additional 2,000 businesses don’t move the proverbial needle too much. So, SCHB looks nearly identical to the S&P 500. For example, the 3 largest sectors (Technology, Financials and Healthcare) make up just over 50% of SPHB, just as they do with the S&P 500.

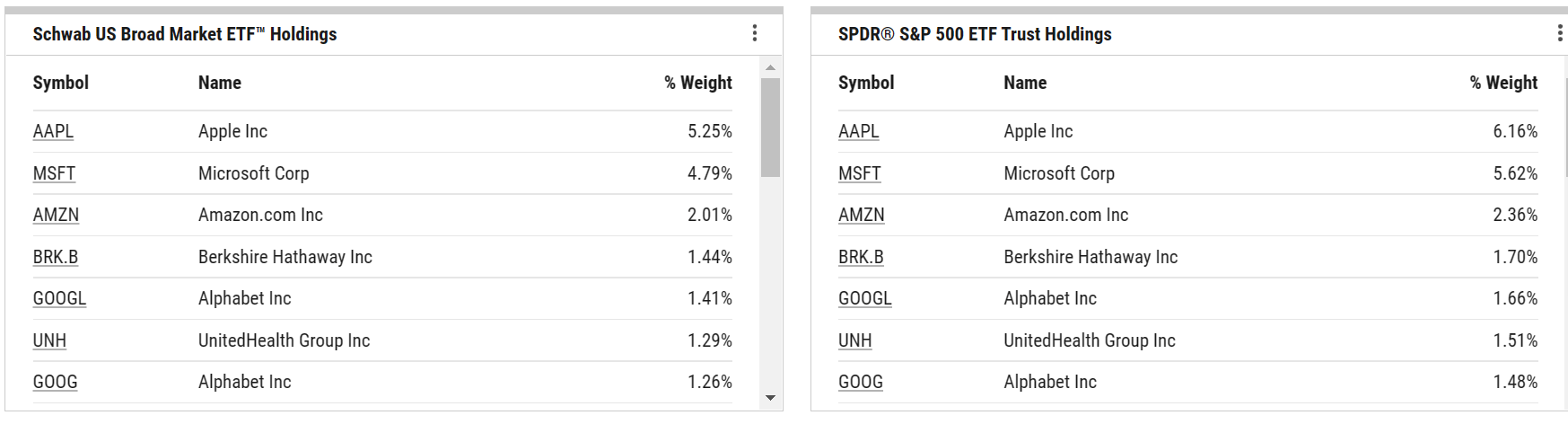

Here are the top 10 holdings of both SCHB and SPY. You see the same holdings, just with slightly higher weightings to them in SPY, as it does not include those other 2,000 stocks.

SCHB vs SPY Top Holdings (YCharts.com)

Opportunities

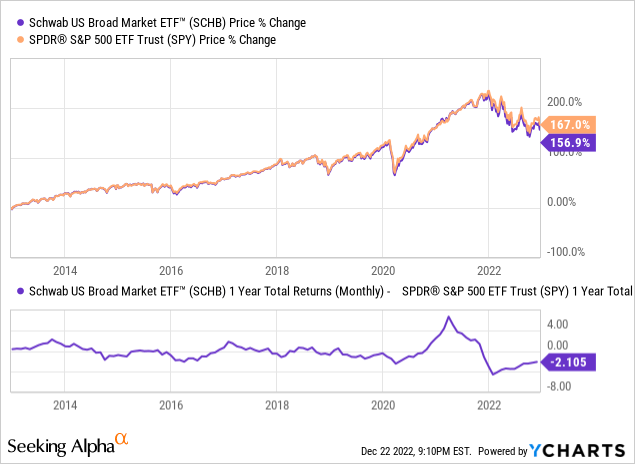

To find something other than the puny expense ratio to consider an opportunity with SCHB, we need to get pretty granular. So here we go. This is a chart of 1-year rolling returns of that ETF and SPY. In the bottom part of the graph, you can see that nearly all the time, the 2 ETFs mimic each other’s performance. The only exception of note was during the pandemic’s onset, when temporarily, SCHB outperformed slightly when the stock market had it huge bounce back. However, you can see that was short-lived, as the performance gap quickly closed.

Threats

The biggest threat here, as is the case with many equity ETFs we follow, is not SCHB itself. It is what it is. But investors should be very careful in applying some sort of expected alpha to this ETF. Diversification is a good thing, but 2,500 securities is too much of a good thing, as we see it.

Proprietary Technical Ratings

-

Short-Term Rating (next 3 months): Sell

-

Long-Term Rating (next 12 months): Sell

Conclusions

ETF Quality Opinion

SCHB as an ETF product appears quite stable. $20 Billion in assets and industry giant Schwab behind it will do that for a fund.

ETF Investment Opinion

But that has nothing to do with our investment opinion here. SCHB gets a solid Sell rating from us on a forward-looking basis. That’s because it is indistinguishable from the S&P 500, and our intermediate to long-term view, technically, quantitatively, and fundamentally on the broad stock market is one characterized by historically-high risk of a major loss. This has been the case in our work since late 2021, and nothing that occurred during 2022 has significantly altered that view.

To be clear, we will never say “the broad stock market won’t go up.” Because no one knows that. What we are saying, with a firm stance, is that while any investment can go up in value at any time, what differs from market to market, from investment to investment, is the level of risk attached to that potential reward.

So, even if we thought SCHB had about a 15-20% chance to rise in price significantly during the next 12 months (and that’s about where we’d put the chances, based on a snapshot of our collective macro research), we would still not be telling investors to buy it here. Opinions on the broad market going into 2023 are as varied in direction and intensity as we’ve ever seen. But when we settle on the weight of the evidence, SCHB is both unattractive due to its link to the broad market, and unattractive due to the “over-diversified” aspect of it.

There will be a bull market in stocks again, but when that occurs, we expect to look elsewhere for exposure. Because no matter how low an ETF’s expense ratio is, the biggest cost to investors, by a wide margin, is deep capital losses in bear markets.

Be the first to comment