Ninoon

(Note: This article was in the newsletter on December 22, 2022.)

Medical Properties Trust, Inc. (NYSE:MPW) has long been associated with Steward. Lately that association has turned into a liability in the eyes of the market despite nothing but financial success. It just goes to show how some innuendo along with some numbers that are guesses (combined with cherry picked facts) can make a convincing argument for people that do not realize that the limits of the numbers presented are the logic upon which those numbers came from. If the logic is based upon a guess, then the resulting conclusion is likewise a guess.

No matter how scary a bear case can look, it can only be as good as the foundation upon which it is based. Right now, the bear case foundation is looking pretty shaky while heading downhill at a pretty good pace.

Bear Case

The first bear case is that there are no Steward financials. There are all kinds of assertions about possible disclosure violations and sometimes worse thing than that. The fact is that all these assertions have so far been met with crickets. That inaction has to be taken into consideration because any serious violation usually means action by the SEC. Such action could still occur. But despite the assertions that are made from various sources, no action has been taken so far. At the very least, the presumed violations are not that serious. At best, there are no violations. Now let’s see what the future holds.

Steward announced the completion of the bank line extension despite a lot of sentiment to the contrary. Supposedly Steward needed audited financials for the completion. If that is the case, then it may also be a reason that Steward financials were not included as a Medical Properties Trust filing in the current fiscal year. In any event, a bank line is rarely a cause for serious financial issues. Of all the companies I followed to bankruptcy, none had a problem with the bank line at the time of filing. Several even drew down the whole credit line just before they filed.

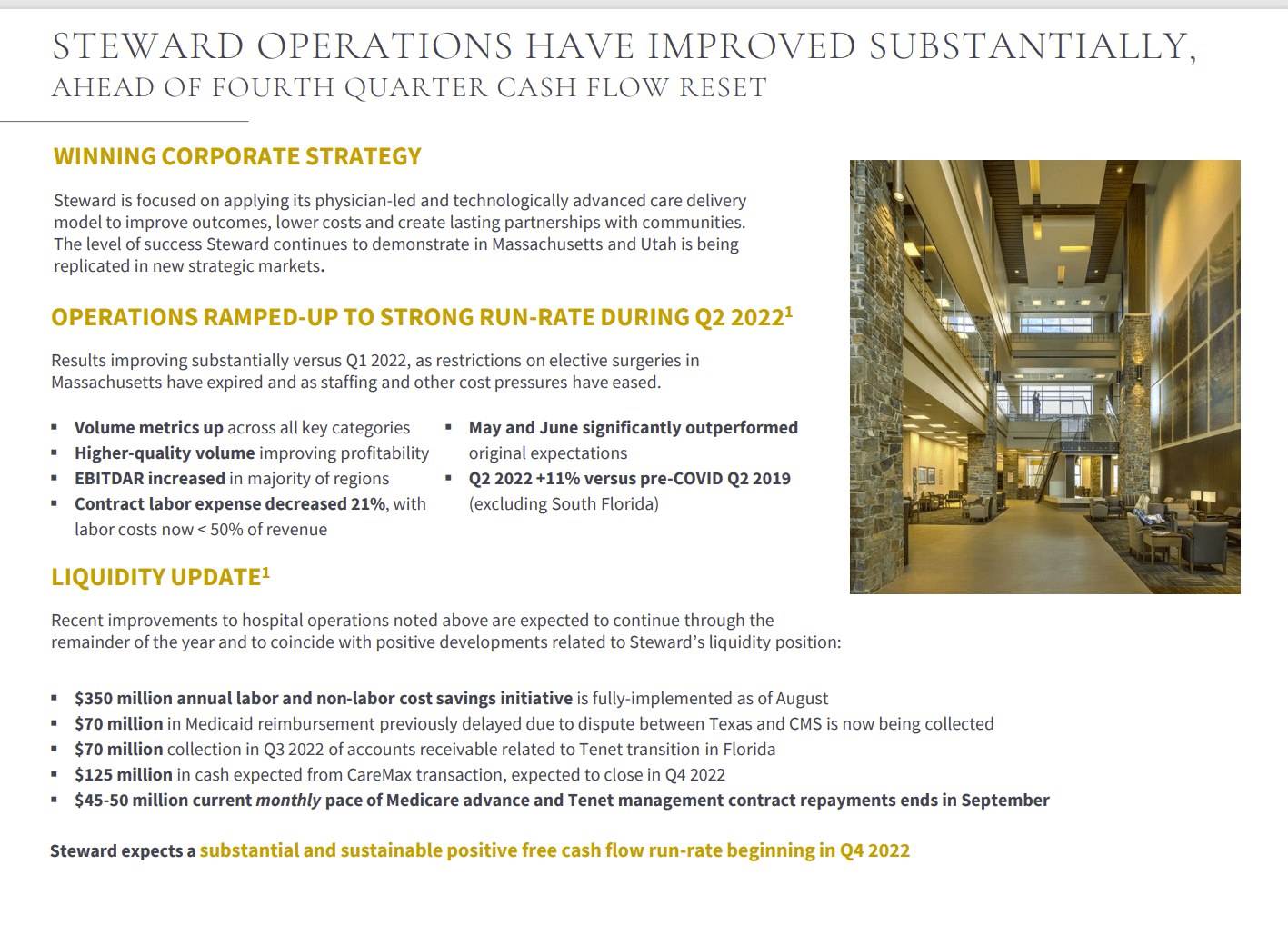

The last bear case probably has the most credibility. There are worries about Steward’s cash flow after the pandemic caused losses. Even considering those worries, management gave an update on Steward’s financial progress in the current fiscal year.

Medical Properties Trust Update On Steward Financial Progress (Medical Properties Trust August 2022, Corporate Update)

Then the very public focus shifted to the vagaries of the update and how “no one” really could verify the accuracy because nothing close to sufficient data was supplied. But that misses the whole point of this business.

The focus should instead be on:

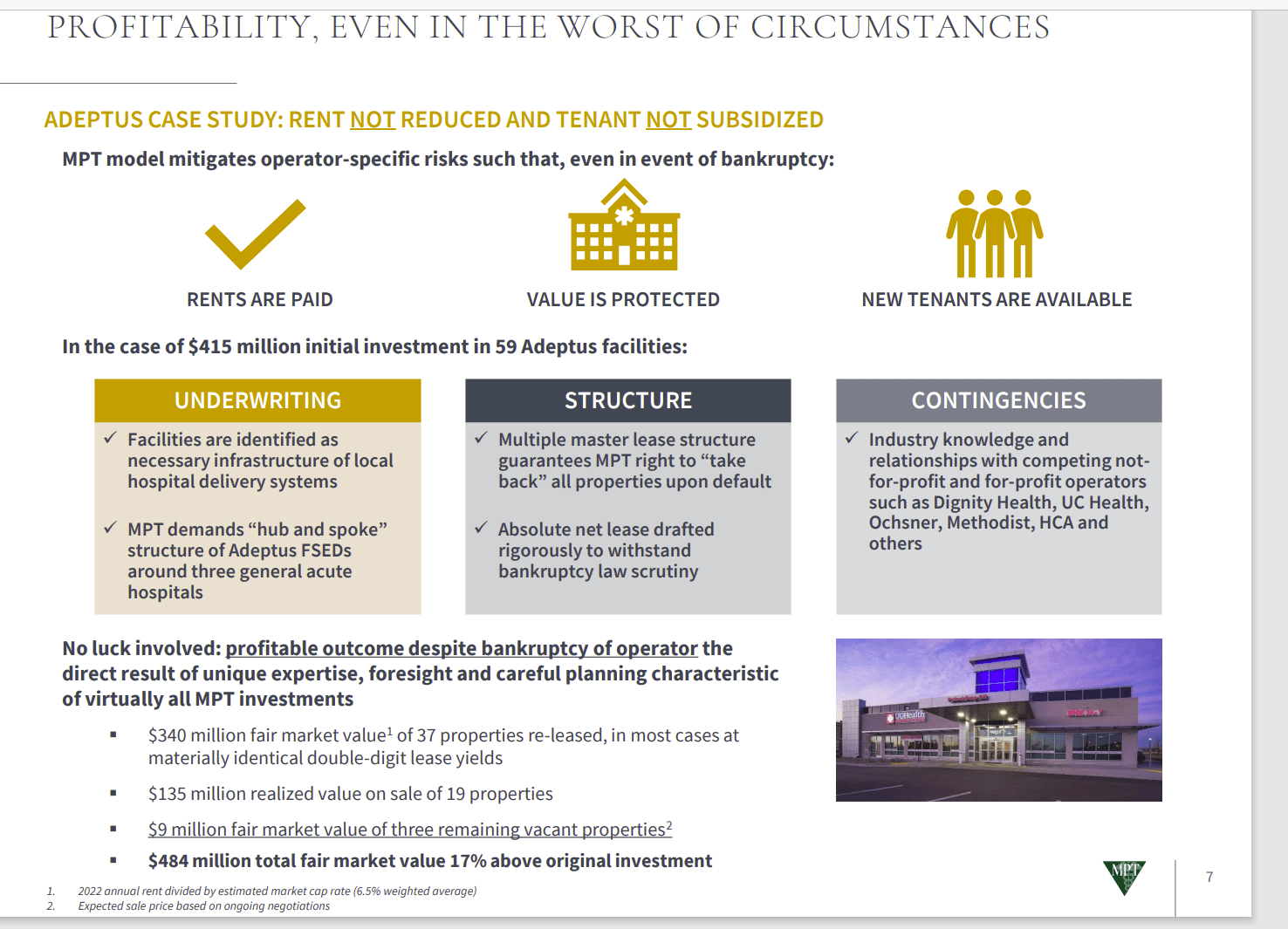

Medical Properties Trust Preparation For Worst Case Bankruptcy Scenario (Medical Properties Trust April 2022, Corporate Presentation)

After a leasing deal is done, there will be operators that head downhill for one reason or another. But what investors need to know is if management has already planned for that situation. Management has in various ways explained similarly to the above slide that they are ready for the worst-case scenario before they ever do an agreement. Otherwise, the agreement does not get done. It is the old “Golden Rule” of business (“He who has the gold makes the rules.”).

Another words, this management has made a contingency plan to be paid in the event the worst possible outcome (bankruptcy) happens. Management has further disclosed that it does not happen often. But when it has happened, things have pretty much turned out as management has planned.

For the bear case to have any merit, there needs to be a solid reason for a very different outcome in the future. Right now, there has been no solid reason given other than Steward has financial issues. But as was just discussed, management is ready if things get worse and has a plan. Therefore, unless there is a material change, either the company collects the money owed or the company collects the money owed. That is the history.

Creating Distrust

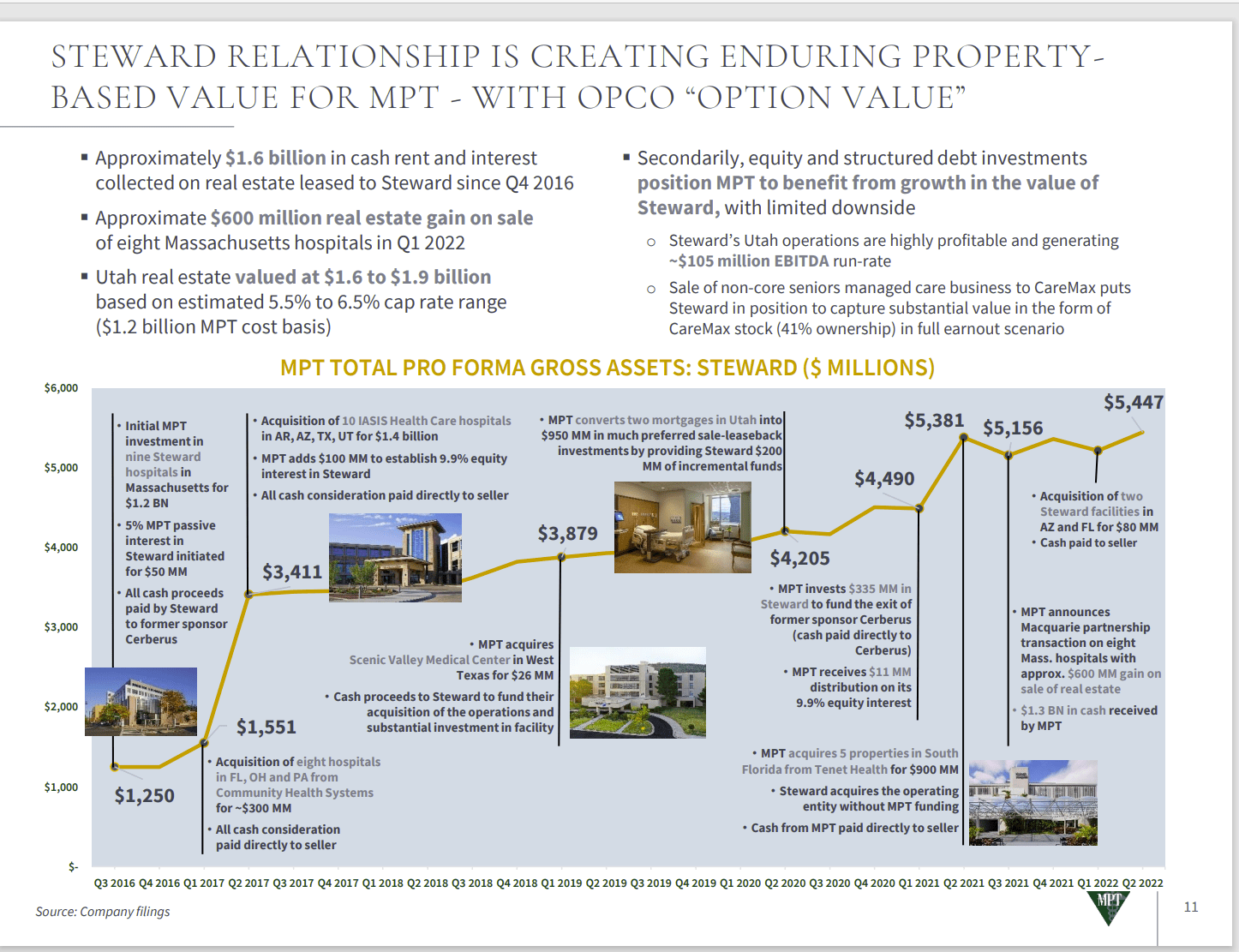

The main objective of any short attack is to create enough distrust to destroy long-standing business relations. In this fashion bears destroy companies to make a profit from the wreckage. Steward is not only material to Medical Properties Trust, but it is also a very profitable arrangement. Hence this business arrangement will get special attention. If the profits get destroyed, then the business ceases to exist for a darn good short attack profit.

Medical Properties Trust Results Of Steward Business Relationship (Medical Properties Trust August 2022, Corporate Presentation)

The relationship has so far clearly benefited the company (and hence the shareholders). There would need to be a definitely material change in the history above for this relationship to be either broken off or become less important.

One thing to note from the above is that if the properties are worth more than the lease, then the properties can be sold to raise cash with the owner pocketing the difference for its own benefit. That is a potential margin of safety in this business arrangement that gets overlooked with the bear argument.

Medical Properties Trust has in fact raised some cash and repaid some debt with more possible moves to increase potential liquidity in the future.

Debt

Last but not least has been the remark about the company bonds selling for less than par. That should have been expected as the Federal Reserve raises interest rates. The key is the additional “risk premium” inherent in the price. This company is not exactly rated “AAA” so there will be some premium. But there is nothing to indicate that there is serious trouble ahead with the current bond yields. Companies I follow in deep trouble have bond yields of 20% to maturity. That is not the case here.

Now higher interest rates can be a risk in that lower interest rate debt may have to be eventually refinanced. But the current round of interest rate increases by the Federal Reserve really does not appear to be a multi-year event. Instead, the move to quash inflationary expectations is typically at most an 18-month exercise.

Even now, the largest inflationary component, the housing component (which lags behind one year in the calculation), has been declining for some time. Therefore, the largest part of the CPI calculation is already declining and will for the current year because it has been declining since last year. That leaves the volatile food and energy part of the calculation which is nothing close to the problem one reads about constantly.

The volatile food and energy may mean that interest rates may not get as low as they were. But they also are unlikely to remain high for long now that housing costs are no longer fueling increasing core inflation.

That means that the low price of the company bonds will likely be a temporary issue. It is true that if the company does any deals in the current interest rate environment, that management will need a return to cover the higher interest rate costs. But as long as high interest rates do not persist for “years,” there is minimal risk to the company debt structure or cash flow.

The Future

Management is likely to survive the period of higher interest rates by simply “hanging on” and waiting for a lower interest rate environment. Deals are unlikely to get done when the market sees a transient high interest rate environment. Now should something cause the view to change, then the whole situation would need to be re-evaluated. Right now, there is nothing to indicate that is the case.

It is very likely that fiscal year 2023 will not involve any growth. Instead, the fiscal year will likely be a consolidation and simplification fiscal year. The pandemic was financially stressful for a lot of medical field organizations. So, a year of balance sheet repair throughout the industry is very likely.

The good news is that business as usual has resumed. Therefore, the company is likely to report decent cash flow while maintaining the dividend. Once the current high interest rate environment passes, then growth is likely to resume along with increasing dividends.

The current price is therefore a bargain even though the high dividend yield indicates some level of higher risk. A basket of companies like this should outperform the market over the next few years.

Be the first to comment