FG Trade/E+ via Getty Images

Summary

DoorDash (NYSE:DASH) management described it perfectly in their latest investor newsletter: “People need to and typically enjoy eating”. Food has been, and always should be, a relatively inelastic product. It’s hard to imagine a scenario where DoorDash’s core business is eradicated due to macro or industry-wide issues. Restaurants and grocers should continue to expand indefinitely, albeit slowly. While most people associate DoorDash solely as an industry-leading food delivery service provider, I believe it has the potential to become a multi-sector, on-demand delivery juggernaut. The company needs to continue focusing on expanding its market share while managing cost per order effectively.

Can DoorDash Sustain Its Growth?

Believing a company can sustain growth for years in a competitive space requires a lot of forward-thinking and maybe a little bit of luck along the way. Imagine having instant access to a one-stop shop for any goods you’d find at a brick-and-mortar store that can be delivered to you the same day. DoorDash has the foundation and infrastructure to achieve this. To better illustrate, let’s use an example. There was a video circulating online earlier this year of a person who was out with friends at a park during a hot summer day wearing long pants. Rather than suffering in the heat or having to go home and change clothes, they decided to order shorts from DICK’S Sporting Goods (DKS) via DoorDash from their phone. In just a matter of minutes, a “Dasher” (nickname for the delivery person for DoorDash) showed up at the park and hand-delivered a brand-new pair of shorts. Pretty convenient I’d say. There are countless scenarios where DoorDash can add value for everyday consumers like this, but it will take time for them to achieve.

Taking a step back, there are a few reasons why I believe DoorDash remains a growth story with upside potential to reach profitability:

- Market penetration remains low, both U.S. and Internationally.

- Costs per order have been reducing each quarter.

- A recent commitment to expand partnerships with grocery stores and other industries seeking an on-demand e-commerce platform

Although DoorDash receives its fair share of criticism, perhaps the sell-off may be overdone at this point. This company went public at a high valuation and is considered a growth stock since it is able to justify its negative profit margins with impressive revenue expansion. With that being said, I have to admit it’s very challenging to set a price target or give a reasonable valuation estimate for a company such as DoorDash. There are just too many variables that can quickly alter revenue or margins and in turn, its share price. I think it’s more important to focus on the longer-term vision for this company as many investors did with Tesla or Amazon during the early days before either company turned a profit.

Growth stocks have been hit hard this year with rising interest rates, but it’s important to remember that markets price companies based on future expectations. Opportunity costs continue to rise, and investors appear to have lost patience with any companies that are not currently profitable.

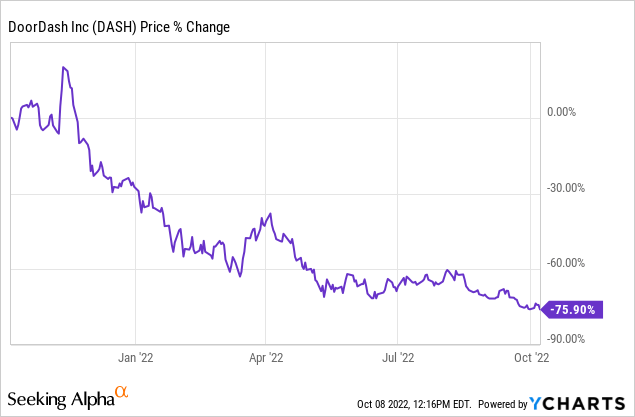

Figure 1: DASH 1-Year Share Price Performance

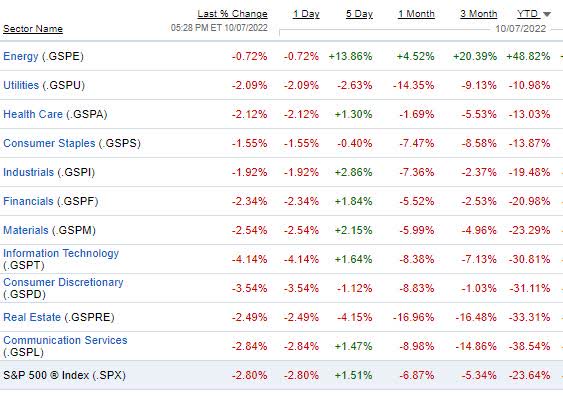

I believe there will be a time again when investors’ risk appetite roars back. Throughout history, this is evident. The 2020-2021 rapid increase in equity markets (where it seemed like everyone was making huge investment gains) is the perfect example in my opinion. Investors took on huge amounts of risk and it paid off. For now, sectors that are historically correlated with the economy may continue to suffer with a looming recession in the United States. Consumer Discretionary (where DoorDash is classified) is the third worst-performing sector behind Technology and Real Estate YTD, down more than 30%. The data below is as of October 7th, 2022.

Figure 2: U.S. Equity Sector Performance

Fidelity

A lot of negative expectations are already being priced into cyclical sectors such as Consumer Discretionary, but that will change. When? No one knows (except maybe the Fed) but DoorDash could benefit greatly when the tides do change from a high-level sector perspective.

Market Penetration Remains Low

5 years ago, the food delivery marketplace was dominated by Grubhub. As more participants entered the market, things changed fast. So far, it looks like DoorDash could be the sole victor, but it’s far from over. There are numerous reports from Bloomberg and consulting firms such as McKinsey illustrating DoorDash’s rapid growth over the last few years:

BusinessofApps

However, it’s important to remember that this is just in the United States. DoorDash has bigger plans to expand globally, and rightfully so. Its business strategy clearly has been working in the United States as it continues to take market share. However, they currently have a very small footprint outside the United States versus its biggest competitor Uber Eats. To combat this, DoorDash recently completed its acquisition of Wolt, a Finnish technology company known for its delivery platform for food and merchandise. Management hopes this could spearhead their presence overseas. While it’s too early to tell the specifics of what DoorDash has in mind for Wolt, it’s clear they are invested in international expansion, which is a great sign for revenue growth.

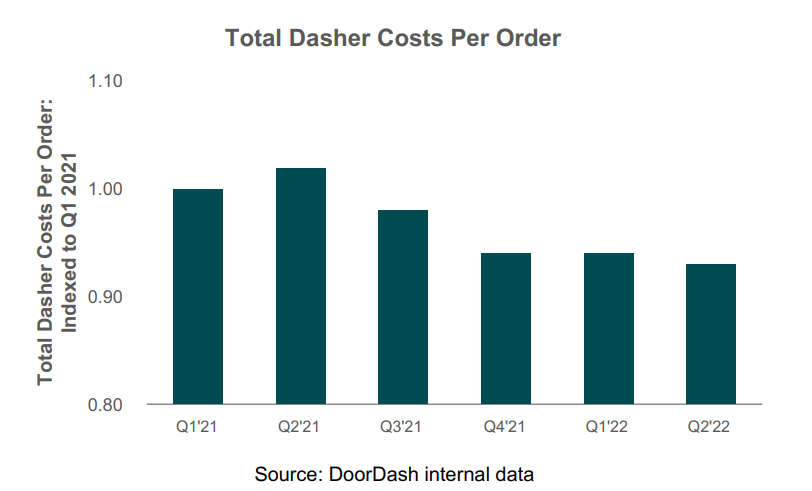

Costs Per Order Are Declining

While the top-line revenue growth is still impressive (for now), DoorDash faces the challenge of reducing costs so it can finally become profitable. Costs per order have been reducing since the second quarter of 2021, but headwinds lie ahead.

Figure 3: Total Dasher Costs Per Order

DoorDash Investor Letter

Total Dasher costs include Dasher acquisition costs, Dasher pay, and the cost of Dasher benefits, including gas rewards and mileage-based payment programs. The good news is that costs have been trending in the right direction since last year. The bad news is that the U.S. Labor Department recently announced it might reclassify gig workers as employees, rather than contractors. Companies such as Uber (UBER), Lyft (LYFT), and DoorDash would be negatively impacted from a cost perspective obviously as it would require significantly more benefits to employees. This is one of the most notable risks DoorDash faces in my opinion, as it should not be overlooked. There would likely need to be some type of change to its current business model or expansion into new industries in order to become profitable, a path filled with uncertainty.

Grocery Store And E-commerce Expansion

While some of the largest grocery retailers such as Walmart (WMT) and Kroger (KR) continue to expand their fulfillment capabilities in-house, smaller chains have struggled to expand. This is where I believe DoorDash has a huge opportunity, and the proof is already evident. From June 2021 to June 2022, DoorDash saw a 130% increase in customers ordering from a grocery store on its platform. Most of the partnerships are with small to mid-size companies across the country, and new partnerships were announced just last month with Giant Eagle, Weis Markets (WMK), and The Raley’s Companies, just to name a few.

But there’s no reason to stop at grocery stores. DoorDash could continue expanding to other sectors and eventually become a one-stop shop for everything e-commerce. As an example, DoorDash recently partnered with DICK’S Sporting Goods to offer on-demand delivery for over 700 stores across 47 states. The convenience of ordering something online and having it delivered on the same day is unmatched. Imagine ordering things such as office supplies, clothes, or tech equipment that can be delivered to you in less than an hour. Not even Amazon (AMZN) can compete with that efficiency (or perhaps they will eventually?).

Conclusion

DoorDash, along with most growth stocks, has taken a beating this year. As many of you already know, rising interest rate environments typically don’t bode well for high multiple companies that aren’t currently profitable. While in my opinion, an 80% decline for DoorDash brings it back down to a more reasonable valuation, the company still has a ton of room for improvements to justify its current share price. It’s going to be a “show me” story over the next few quarters, and if DoorDash can’t show any growth in its margins or new details around expansion plans, investors may have to reevaluate the longer-term prospects for this company. I believe there are catalysts on the horizon for DoorDash to return back to the hyper-growth rates it recently had from 2020-2021. Investing in this company will require patience and an understanding of the long-term vision, but has the potential to be incredibly rewarding.

Be the first to comment