metamorworks

Fabrinet (NYSE:FN) is a leading manufacturer of advanced optical communications devices along with a growing segment of lasers and related sensors. Beyond applications in telecom, data technology, healthcare, and aerospace; it’s the automotive industry that has been a strong growth driver for the business incorporating features like LIDAR and laser lighting.

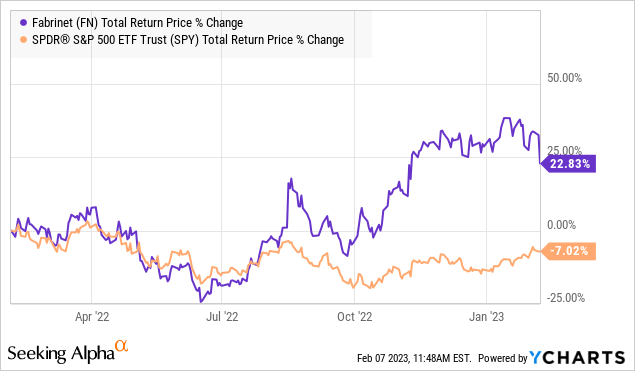

Indeed, FN just reported its latest quarterly result highlighted by record sales and margins which are particularly impressive in the context of several macro headwinds. Shares have been a winner, returning more than 20% over the past year, even reaching an all-time high earlier in January.

By all accounts, the outlook is positive with the company supported by solid fundamentals. At the same time, some mixed guidance by management suggesting softer trends into the current quarter has worked to dampen the momentum in the stock. We’ll also note that the company’s valuation appears stretched relative to a peer group of competitors. Our call here is to expect increasing volatility in FN from current levels.

FN Earnings Recap

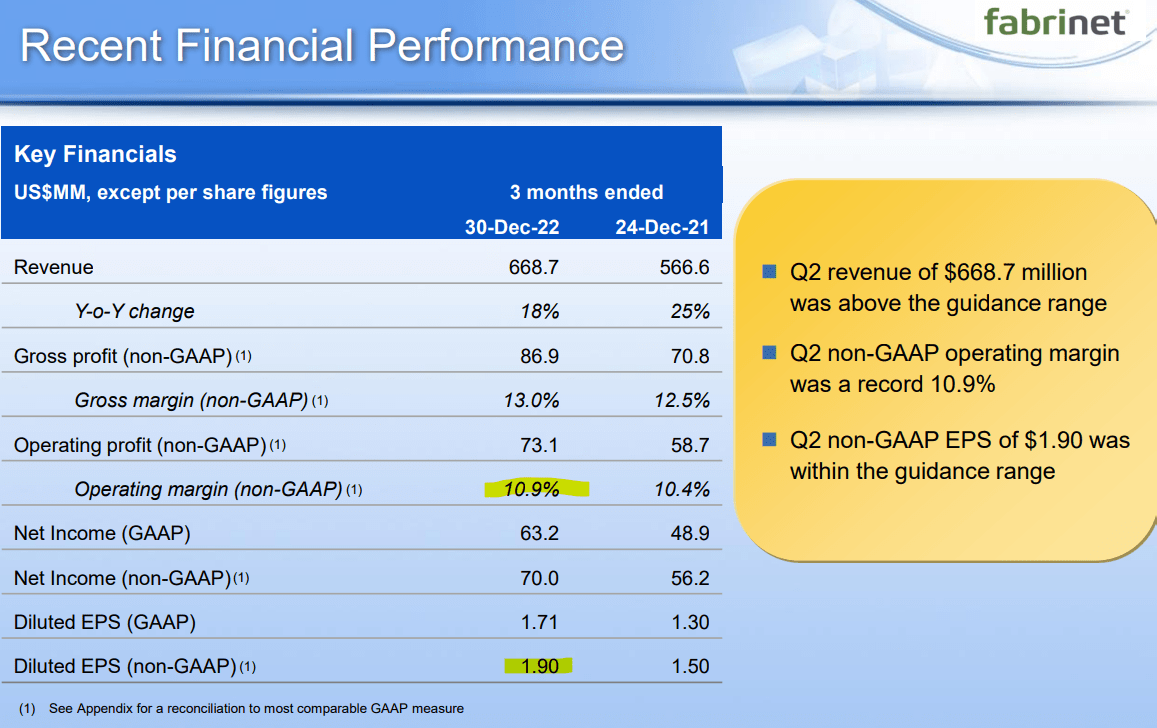

This was Fabrinet’s fiscal 2023 Q2 earnings with non-GAAP EPS of $1.90, which was $0.03 above consensus, and up from $1.50 in the period last year. Revenue of $669 million climbed by 18% year-over-year and was also ahead of estimates.

source: company IR

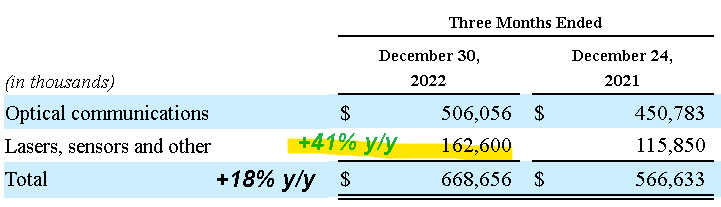

The non-GAAP operating margin at 10.9% was a company record and was up 50 basis points from Q2 fiscal 2022. A large part of that dynamic considers an ongoing sales mix shift with the “Lasers, sensors, and other” segment revenue reaching $163 million in revenue, up 41% y/y. This trend has outpaced the larger Optical Communications business, where revenue was up by 12% y/y.

As mentioned, the strength has been from automotive industry demand, with sales more than doubling y/y, which followed the positive result from the prior Q1. This point was made clear during the earnings conference call:

As in Q1, growth in non-optical communication was driven primarily by automotive revenue, which was a record $94.8 million more than double from a year ago and up 9% from Q1. In addition to a better supply environment for these products, we also benefit as from continued demand strength for newer automotive products.

In other words, demand from automobile manufacturers recovering following the disruptions during the pandemic has been a strong point for Fabrinet over the past year. The company is recognized as differentiating itself by offering customizable production lines catering to OEM needs. This includes not only components for premium car models with high-tech features or electric vehicle manufacturers, but a generalized trend where even entry-level cars are utilizing more and more LEDs, and safety sensors types of devices.

source: company IR

On the other hand, some of the other areas of the business have been weaker. Revenues from “industrial lasers” were down -13% sequentially from Q1. On the core Optical Communications side of the group, management claimed the supply chain availability of certain products worsened and expect those constraints to tighten.

That theme has carried into the current guidance for Q3, where Fabrinet sees revenue between $640 million to $660 million. At the midpoint, this forecast is below the consensus of $656 which may explain some of the share price weakness in FN, which sold off on the Q2 earnings print. From the conference call:

We remain optimistic about the long-term demand trends across our business. And our ability to manage supply constraints as effectively as possible. At the same time, our general supply environment has improved, the availability of certain components worsened in Q2 impacting telecom revenue. From what we are currently seeing, we expect these constraints to be even tighter in Q3.

The new guidance implies an increase of 15% y/y, although this is also a slowdown in pace from the recent quarter and also -2.7% lower sequentially from Q2. Management expects Q3 EPS between $1.86 and $1.93, roughly flat from Q2.

Our initial take is that there are some reasons to be skeptical of this target considering it would imply another uptick in the operating margin, which will be difficult if the supply chain constraints continue. From there, the risk is that there is some downside to the final numbers.

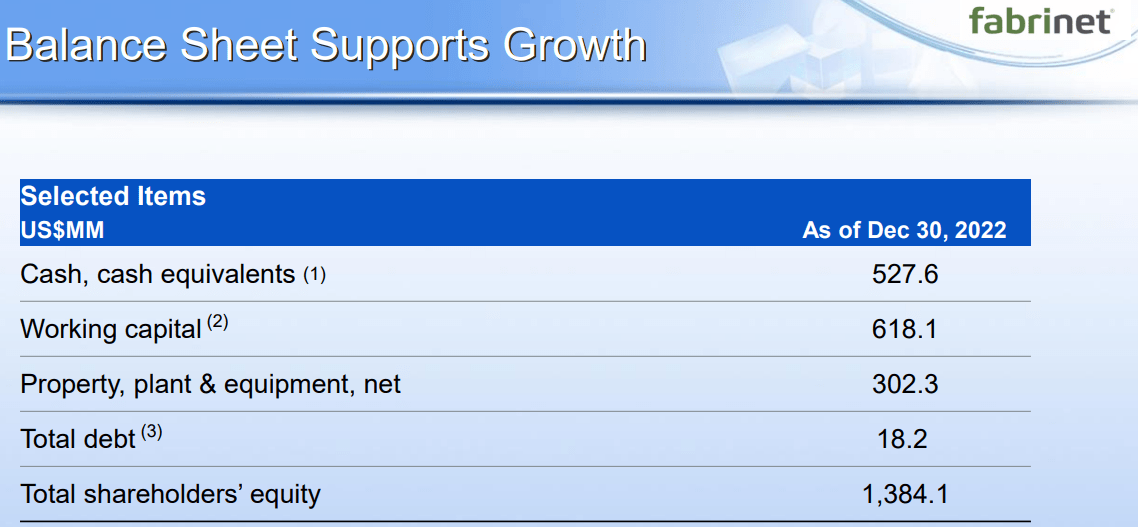

Nevertheless, we can point to the rock-solid balance sheet, which remains a strong point in the company’s investment profile. Fabrinet ended the quarter with $528 million in cash and equivalents, against just $18.2 million in total debt. The setup is supportive of the company’s share repurchasing authorization with $92 million remaining under the existing program.

source: company IR

Is FN Overvalued?

There’s a lot to like about Fabrinet as a high-quality leader in a segment of tech that maintains a positive long-term growth outlook. We can look out one to two years from now and the current headlines of supply chain constraints will likely be remembered as just short-term noise in the big picture.

We expect conditions to improve with an eventual global economic rebound adding a boost to the business on the demand side for the segments that have been lagging. Separately, the company’s new manufacturing facility “Building Nine” in Chonburi, Thailand completed last year adds to its capacity as a runway for further growth.

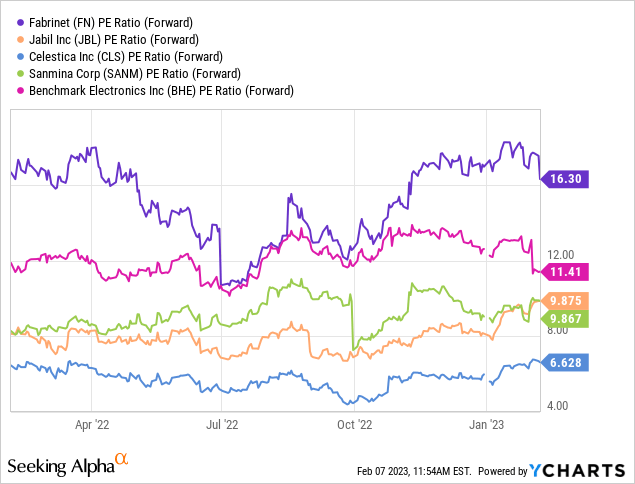

In the near term, the challenge here likely comes down to a sense that much of the strong points in FN’s story have already been incorporated into the stock. Shares are up more than 60% from their lows last June indicative of the improved macro backdrop. The result is that FN’s valuation has opened a large spread relative to industry peers.

Among competitors cited by Fabrinet in its annual report, it’s clear that FN trading at a forward P/E ratio of 16x is at a large premium compared to names like Benchmark Electronics, Inc. (BHE) at 11x, Jabil Inc. (JBL), and Sanmina Corp. (SANM) both at 10x or Celestica Inc. (CLS) at 7x. The contrast is similar in other multiples across the EV to EBITDA ratio and even price to free cash flow.

There is a case to be made that FN’s net cash balance sheet and momentum in lasers and automotive sensors support a premium, but we also believe there is some room for the spread to narrow lower.

Getting into fiscal 2024, FN’s top line growth is expected to normalize towards a 12% annual rate through 2025. The consensus EPS forecast to climb from $7.59 this year, to $8.38 in 2024, representing a 10% increase next year, which is below the revenue trend and suggests a view that the margin gains FN has achieved in recent years are near its upper structural limit in the near term.

Seeking Alpha

FN Stock Price Forecast

Balancing our positive view of the company against the expectation of a growth slowdown from the exceptional rates in recent quarters, we rate FN as a hold. The big takeaway from this latest quarterly report is that we don’t see a good reason why shares should breakout out higher.

With the stock already selling off by as much as 10% from its recent highs, it’s probably too late for shareholders to sell and we certainly wouldn’t call FN a short idea. The baseline here is for some consolidation around the current level, looking ahead to the next few quarterly updates.

On the upside, we want to see some confidence from management that its specific supply chain constraints have settled while noting a recovery in demand from the lagging segments. The operating margin and cash flow trends will be key monitoring points going forward.

In terms of risks, a deeper deterioration in the global economic outlook would undermine the company’s growth trajectory. Weaker-than-expected results below estimates would open the door for a leg lower in the stock.

Seeking Alpha

Be the first to comment