Torsten Asmus

For investors looking to make a direct bet on inflation, the ProShares Inflation Expectations ETF (NYSEARCA:RINF) tracks 30-year US inflation expectations as measured by the performance of inflation-linked bonds relative to regular bonds. While there are many ETFs that can be used to make bets on inflation rising or falling, the RINF tracks market expectations directly, and it looks undervalued at current levels. The problem with this ETF is that it does not generate any returns unless inflation expectations rise. It is therefore best to be used as a short-term trade rather than a long-term investment.

The RINF ETF

RINF tracks the performance of the FTSE 30-Year TIPS (Treasury Rate-Hedged) Index, with long exposure to US TIPS (Treasury Inflation Protected Securities) and short exposure to US Treasury of equal maturity. The spread between these two instruments gives us the average inflation expected over the next 30 years by bond market participants. Treasury yields rise relative to TIPS yields when market participants expect higher inflation over the long term, causing the fund to gain value. As inflation expectations will ultimately converge towards actual inflation as time passes, the RINF can be thought of as a bet on the long-term actual inflation rate.

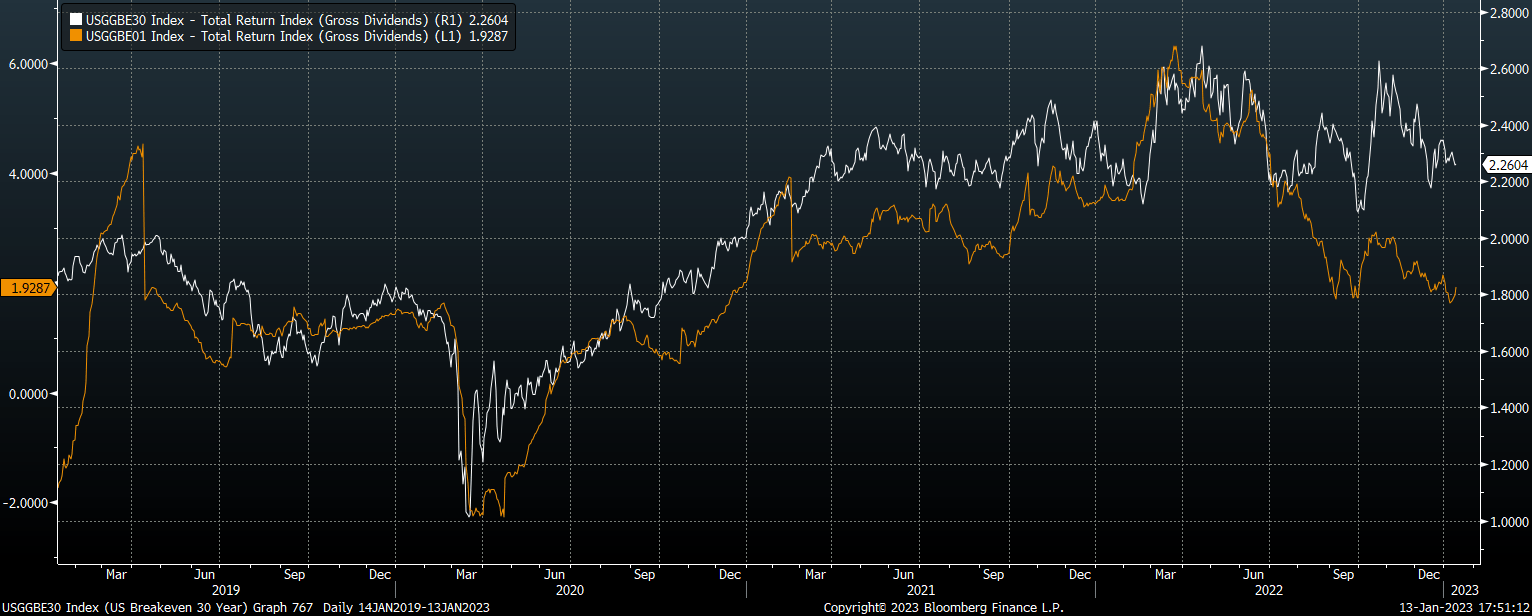

1-Year Vs 30-Year US Breakeven Inflation Expectations (Bloomberg)

Despite the long-term focus of the fund, however, its performance is closely correlated to short-term inflation expectations. The reason being that the same factors that drive changes in the near term tend to be extrapolated out over the long term.

RINF Has Done Its Job Since 2020

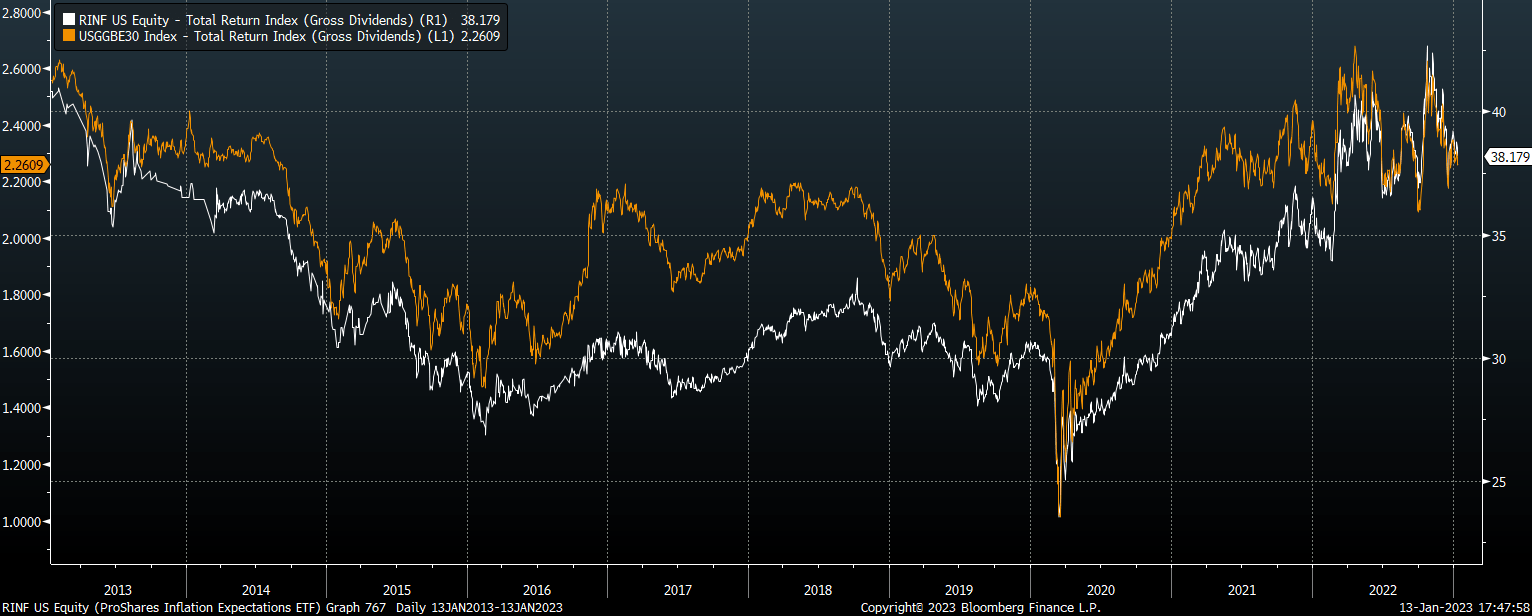

Of all the ETFs to choose to make a bet on inflation, the RINF is the most direct as it tracks the bond market’s expectations of inflation. This can be seen on the chart below, which shows the performance of the RINF versus the 30-year US breakeven inflation expectations, which is ultimately what the fund seeks to track.

RINF ETF Vs 30-Year US Breakeven Inflation Expectations (Bloomberg)

I first turned bullish on the RINF back in early 2020 in ‘Inflation Expectations Are Way Underpriced‘, arguing that inflation expectations were completely out of line with the fundamental inflation outlook facing the US economy. Since the Covid crash lows 30-year breakevens have risen from 1.0% to 2.3% currently, having fallen from a peak of 2.7% in April last year. Over this period the RINF has generated returns of 62%, performing exactly as it is supposed to do.

Long-Term Inflation Expectations Seem Too Low…

30-year breakeven inflation expectations currently sit at just 2.3%, which seems far too low in the context of the current inflation rate and the long-term average inflation rate. Over the past 20 years CPI has averaged 2.5%, and even if we strip out the impact of the recent inflation surge, it still averaged 2.1% from 2002 to 2020. It seems highly optimistic that inflation will return back to average levels considering the growing structural pressures on government spending due to the ageing population and the huge level of external debt the US holds.

…But The RINF May Not Be Suitable For A Buy And Hold Strategy

That said, the RINF may not be the best way to benefit from inflation coming in higher than expected over the long term due to its high expense ratio of 0.3% and the fact that it does not generate any income. This means that returns will be negative unless we see inflation expectations rise. The RINF is a more appropriate for taking short-term bets on inflation. As noted above, as long-term inflation expectations tend to closely track short-term inflation expectations, the RINF can be used to take a view on the latter. As we saw in 2020, while the government response to Covid was clearly going to be inflationary from a long-term perspective, 30-year breakevens fell over 0.8%, causing a 20% decline in the RINF.

Be the first to comment