FG Trade

Thesis highlight

ContextLogic (NASDAQ:WISH) has tremendous upside if they manage a turnaround. I am recommending to buy a small position to gain exposure, and monitor the turnaround progress.

The entire thesis falls on management ability to turn this asset around which I believe they are on the right track. That said, this is a big leap of faith as they are multiple macro-factors that are certainly against the business.

Company overview

Wish offers e-commerce services. The company, which focuses on mobile commerce, assists merchants in reaching customers while also allowing users to personalize shopping and find products.

The market is huge

The market for international online shopping is huge, and it’s growing rapidly. SkyQuest predicts that by 2028, the value of global e-commerce will increased by a whopping 10 times from the estimated $5.7 trillion in 2022. Due to the convergence of edge computing and the maturation of supporting infrastructure, I see mobile as the undisputed leader in e-commerce. E-commerce as we know it today has not yet developed to meet the expectations and financial constraints of the world’s growing population, despite the fact that the market for such services is sizable and growing rapidly.

Value-oriented consumers constitute a sizable and rapidly expanding market that conventional e-commerce has largely neglected. For this market segment, price is often the deciding factor in whether or not to make a purchase. For those with limited financial resources, this is an especially pressing issue. Affordability will be paramount for first-time online shoppers, and I anticipate that the upcoming wave of ecommerce users from developing countries will make up the bulk of these value-conscious shoppers.

The continued success of discount stores shows that there is a large and dependable consumer market for goods at lower prices. While conventional stores are having a hard time, discount stores can stay afloat because value-oriented consumers will always be looking for a good deal. Despite their massive size, however, these discount stores have only met with moderate success in bringing their low-priced business models to the web.

Wish product offerings have compelling value proposition

The thrill of discovery is at the heart of the traditional store. Consumers often end up spending more money than they had originally intended when they shop in stores because they are able to browse and find new products they want. New product interest is often sparked by this type of exploratory navigation. The consumer experiences of many e-commerce sites and brands, on the other hand, are primarily search-driven rather than discovery-based because they were developed for the desktop. When this search-based experience is brought to mobile, people can shop for things they already know they need but have a hard time finding new things to buy. More and more people are using their phones for everything from banking to entertainment, and this increased usage has made mobile a great place for consumers to discover new products.

The WISH solution prioritized mobile from the start. The mobile version of the site is designed to feel familiar to those who are used to shopping in traditional stores. The platform is made to be user-friendly so that shoppers who aren’t familiar with a certain product or brand can easily peruse a wide variety of options. This is different from other e-commerce platforms where users usually visit with the intention of buying specific items, WISH’s user-friendly navigation and engaging user experience allows it to create a desire to purchase in users.

To put things in perspective, WISH claimed that the user interfaces and feeds are different for all users (I tried using a few phones and found this to be true, albeit small sample size). WISH uses big data technology, which permits extensive personalization, to achieve this goal. They make it easy for customers to find what they’re looking for by delivering tailored recommendations.

Network effects

The WISH platform has powerful network effects. WISH collects, analyzes, and uses data to enhance the shopping and selling experiences of both users and merchants. I believe that WISH’s utilization of data allows it to achieve significant benefits in operations, including personalization at the individual level and the potential for large scale growth.

Wish’s data advantage grows as the company gathers more information about its users and merchants, which in turn enables it to improve the platform’s overall user experience and attract more users and merchants. Customers are drawn to Wish because of the platform’s low prices and unique shopping experience, which ultimately results in higher sales for merchants. A larger user base contributes to a stronger feedback loop created by WISH users, which in turn increases engagement. If more sellers find financial success on Wish, more sellers will sign up and expand their operations there, increasing the variety of goods available and ultimately enhancing the Wish shopping experience for everyone. The cumulative benefits to consumers and businesses from this virtuous cycle are immense.

Competition

As the reader may have guessed, the competitive landscape is fierce. WISH is in direct competition with other online marketplaces like SHOP, EBAY, ETSY, etc., as well as Chinese-focused marketplaces like AliExpress.

Whereas WISH (when things are fixed) is a mobile-first, algorithmically driven, one-to-one shopping feed that had a sizable clientele around the world before things started to go south. Contrast this with a search-driven, top-down experience where broad, centralized selection is central to the retail value proposition, and you’ll see how the underlying architecture was designed to support something very different. There’s a reason Amazon wanted to pay $10 billion for WISH a few years ago.

This is a one-of-a-kind store that mashes up features of a dollar store with those of a treasure hunt. In addition, it caters to the unique set of requirements and habits that characterize “impulse” online purchases rather than those that characterize “normal” ecommerce interactions. To add to this, mobile is the only platform where gamification can have an effect; thus, a mobile feed is essential for gamified retail (which WISH is strong at).

That said, a lot of these features are backwards looking, and I am placing my bets that WISH can fix the business to achieve all these feats again. We will see.

Business turnaround is on track, but still early

For some historical context, let’s look at the beginning of WISH’s decline in 2Q21, when the company was hit by macro and company-specific headwinds, leading to a 29% drop in Marketplace revenue and a 126% increase in logistics revenue, respectively. As a whole, I think the reopening caused a decrease in user activity, as evidenced by a 13% decrease in global app installs and a 15% decrease in average time spent on the platform. Due to internal challenges, WISH shifted its user acquisition strategy to concentrate solely on keeping its existing users rather than acquiring new ones as ad prices continued to rise. Also, a CEO exit in 3Q21 was widely anticipated, but it did not help the stock story.

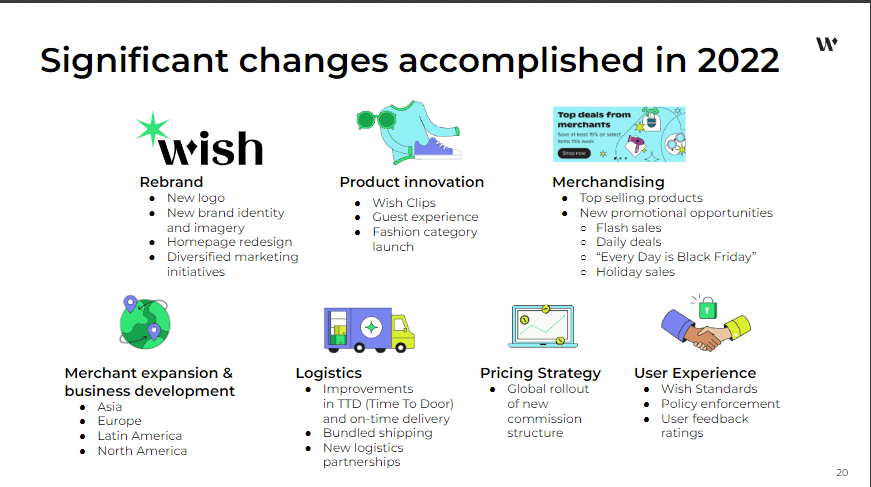

WISH, in my opinion, is still in the early stages of its turnaround at this time, with a new executive team at the helm. Enhanced user experience, strengthened merchant relationships, and operational efficiencies are WISH’s three primary growth pillars. In my opinion, management is focusing on the right issues, but they need to take decisive action if they want to restart the flywheel. My favorite part was when they updated the app with a new homepage and WISH Clips, which make the app look more modern and are sure to attract more users. The Wish Standards also feature a merchant incentive program designed to raise standards for participating businesses. Lastly, I also agree with the company’s choice to downsize the workforce and save money by rebuilding the platform.

Nov 22 ppt

Unit economics wise, I get that it is horrible today. If we look at the long-term financial targets (post FY26) stated initially, management was aiming for 20-30% EBITDA margins with a key assumption: S&M to reduce to 40-45% of sales (current 60+%). This assumption is not implausible. If we look at history, S&M as a % of sales has been trending down nicely since 2019 as the business grow. As such, the question is can WISH regain growth. I like to point out that pre-covid the business had over 100 million MAU at one point, and I believe they are able to reach back similar levels when they fixed all underlying issues. WISH latest earnings presentation has certainly shown positive signs of turnaround.

Nov 22 ppt

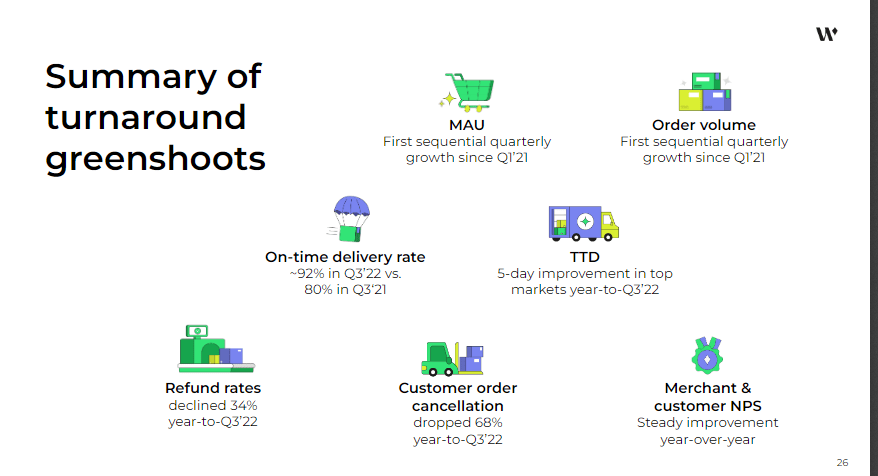

3Q22 EBITDA guide shows sign of positive traction

WISH reported revenue of $125 million for the third quarter, a decrease of 66% but slightly ahead of consensus estimates due to better-than-expected logistics revenue in spite of recent pricing changes and weaker macro. When compared to July, management predicts that October’s revenue will be flat to down. However, I anticipate that holiday seasonality will drive sequential upside, resulting in higher-than-expected revenue for the fourth quarter. Further, EBITDA for the third quarter was above expectations, as was guidance for the fourth quarter.

Recent price changes and a challenging macro environment, especially in the EU, continue to be headwinds for core marketplace growth even as WISH makes fundamental changes to its business model. However, there are indications of volume growth on the platform, which bodes well for logistics-related income. While the company has made progress in recent months toward its goals of stabilizing engagement and returning monthly active users to growth, I believe WISH is still in the early stages of its multi-year turnaround process.

The key things that I am paying attention to are:

- I’m keeping an eye on customer retention and engagement to see how well the company’s efforts to enhance the customer experience pay off.

- The reversal of free cash flow loss remains a major source of investor anxiety. Future working capital dynamics should allow WISH to better manage cash burn, in my opinion.

Valuation

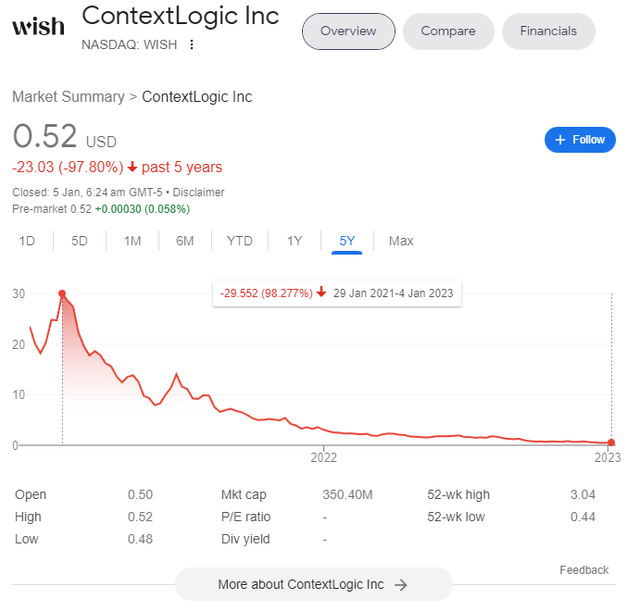

Before I go into the valuation, it is worth pointing that WISH is valued as if the asset will never recover, ever. A look at the stock price certainly supports this statement.

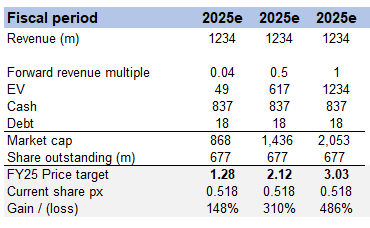

However, if one were to believe that there is a path to turnaround and WISH could eventually reach back to historical levels, the risk/reward is tremendous. Consensus estimates are for WISH to recover to 2018 levels by FY25. Suppose WISH can do it, the stock price could easily be worth multiple times the current share price.

My model depicts a range of multiples that WISH could be valued at (all within historical range), and it suggests a stock price of $1.28 to $3.03 in FY24. I believe the recovery in share price will happen in a very violent manner when it shows sign of recovery and FCF losses are well managed.

Own valuation

Risk

Turnaround fails

The entire thesis is dependent on WISH’s ability to turn around the business. If they do not, this business may be permanently harmed, and whatever we know about it based on historical data will be rendered useless. That is the worst-case scenario for shareholders.

Conclusion

I think it would be wise to initiate a small position and track the turnaround’s development.

The success of the entire thesis hinges on management’s ability to restore this asset, and I’m optimistic that they can do so. However, this requires a substantial leap of faith given the numerous macro-factors working against the company.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment