imaginima

W&T Offshore, Inc. (NYSE:WTI) is an independent oil and gas producer that focuses its E&P activities in the Gulf of Mexico. The company has benefited significantly from the recovery in the energy markets, particularly in natural gas. As such, WTI posted a 1Y total return of more than 42%, significantly outperforming its 5Y and 10Y total return CAGR of 3.7% and -10.6%, respectively.

W&T’s exposure to natural gas has also increased markedly. For instance, natural gas revenue accounted for 42.7% of its FQ3’22 revenue, up from just 17.9% in FQ3’19.

However, its natural gas operations have also undergone significant volatility over the last few months, as NYMEX natural gas futures (NG1:COM) have plunged more than 60% from their August highs.

Notwithstanding, the company highlighted that it had hedged 100% of its FQ4 natural gas volume and about 20% of its oil volume. Notably, the natural gas hedges were entered “in conjunction with a non-recourse term loan.”

Moreover, With WTI down nearly 45% from its November highs, the market has likely baked in significant downside risks on its E&P revenue.

Accordingly, the consensus estimates indicate that WTI could undergo a significant moderation phase through Q4’23, before recovering. As a result, investors need to consider whether a recovery in 2024 is possible, even as its production volume in 2023 is expected to remain robust.

Notably, W&T expects “a potentially very large production increase going into [the] latter part of 2023.” Hence, the company appears confident of the medium-term recovery of the energy sector, despite worsening macroeconomic headwinds.

We believe investors need to watch China’s recovery carefully as it reopens rapidly from its COVID restrictions. While the initial COVID surge is expected to peak in line with the Chinese New Year festivities, its consumption, property, and manufacturing recovery is expected to be bumpy.

With W&T having no reported oil hedges going into 2024 as of November 8, management is likely banking on a strong recovery in crude oil futures moving forward.

OPEC+ remains a mitigating factor against weaker-than-expected recovery demand from China. Moreover, the Biden Administration is expected to replenish the SPR, even though it has yet to make a move, as the received offers didn’t meet its requirements.

WTI last traded at an NTM EBITDA multiple of 2.5x, well below its 10Y average of 4.7x. Hence, it’s pretty clear that the market has yet to re-rate WTI despite its remarkable recovery. We believe market operators have astutely priced in the crash in natural gas futures, as those spikes in August/September 2022 were not sustainable.

As such, we believe that WTI’s forward natural gas revenue performance has likely been de-risked. Hence, it should help lift its performance, as we postulate a potential bottoming in NG1.

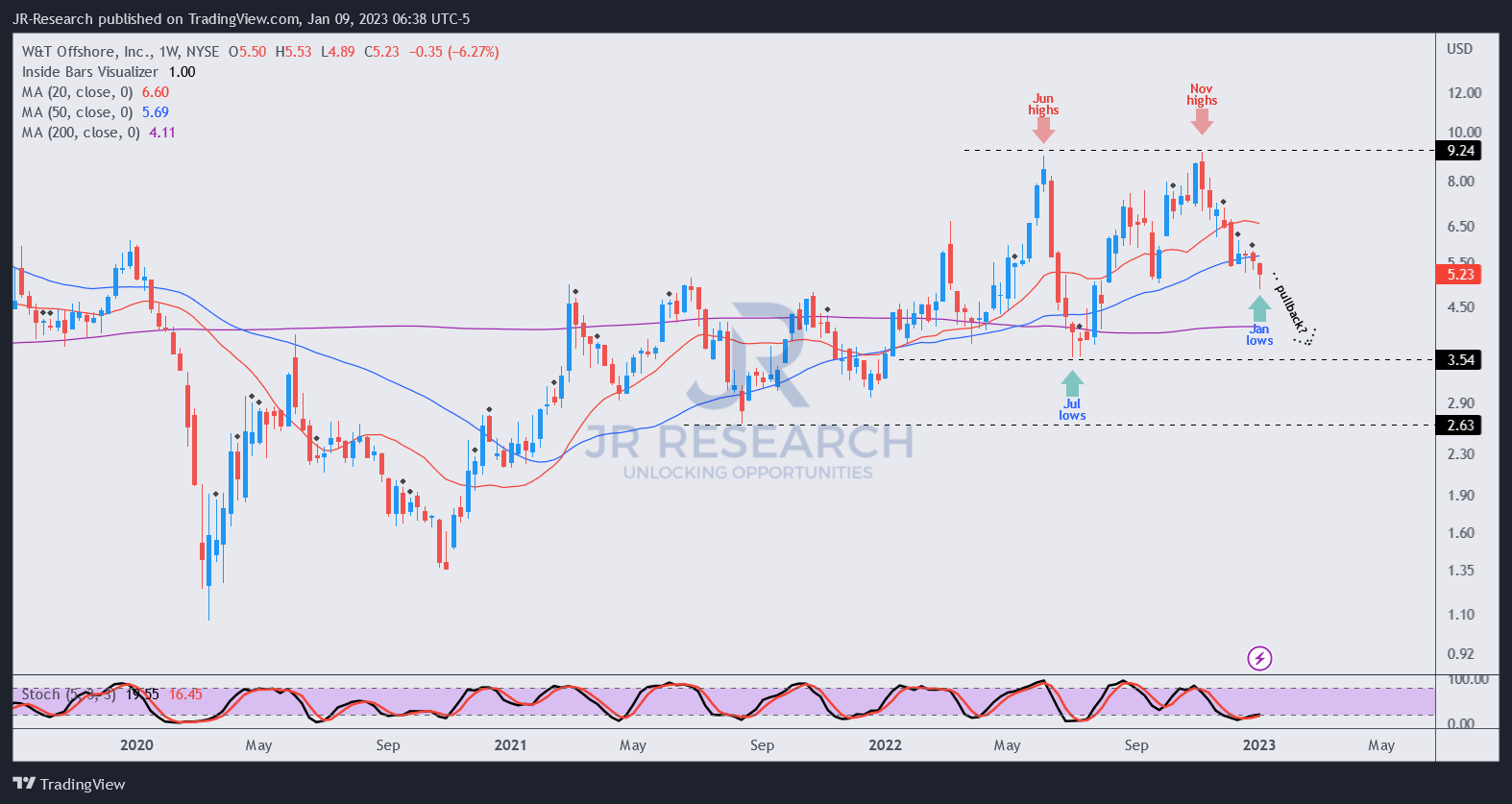

WTI price chart (weekly) (TradingView)

Moreover, WTI’s price action has also been relatively constructive on its medium-term chart. However, we gleaned that it’s at a critical juncture, with buyers needing to defend its 50-week moving average or 50-week MA (blue line), vital to sustaining its bullish bias.

Despite that, we believe that a cautious opportunity has appeared, as its momentum is also oversold. However, investors need to watch its potential recovery closely. If sellers reject a recovery of its 50-week MA decisively, it could indicate early signs of an unconstructive trend reversal, suggesting further caution.

Rating: Cautious Buy.

Note: As with our cautious/speculative ratings, it’s critical for investors to consider appropriate risk management strategies, including pre-defined stop-loss/profit-taking targets, within an appropriate risk exposure.

Be the first to comment