Motortion/iStock via Getty Images

Note: All amounts in Canadian Dollars unless specified as US Dollars.

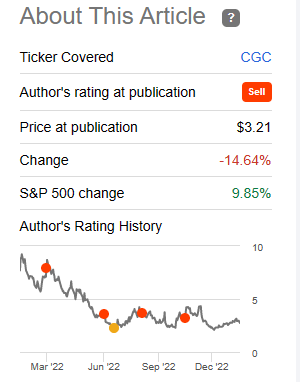

When we last covered Canopy Growth Corporation (NASDAQ:CGC), we had a clear message for investors.

It is going to slowly and methodically go lower. Bulls will hang on to every piece of news which suggests that CGC can make in-roads in the US. We think it is extremely capital constrained and its cash burn likely puts it on a path to bankruptcy within 24-36 months. There is also a ton of capital chasing opportunities within the US market, and we don’t necessarily see Canopy as even a tier two player. We reiterate our Sell rating and look for lower prices up ahead.

Source: “Gross Margins Finally Go Positive, But Will It Be Enough?”

The stock has followed through in the general direction and underperformed the S&P 500 ETF (SP500) by 24.5%, though in all honesty, we thought it would be far lower by now.

Seeking Alpha

We look at the just released fiscal Q3 2023 results to see if they hold a clue as to why CGC has not fallen at the rate we expected.

Canopy Growth Q3 2023 Earnings

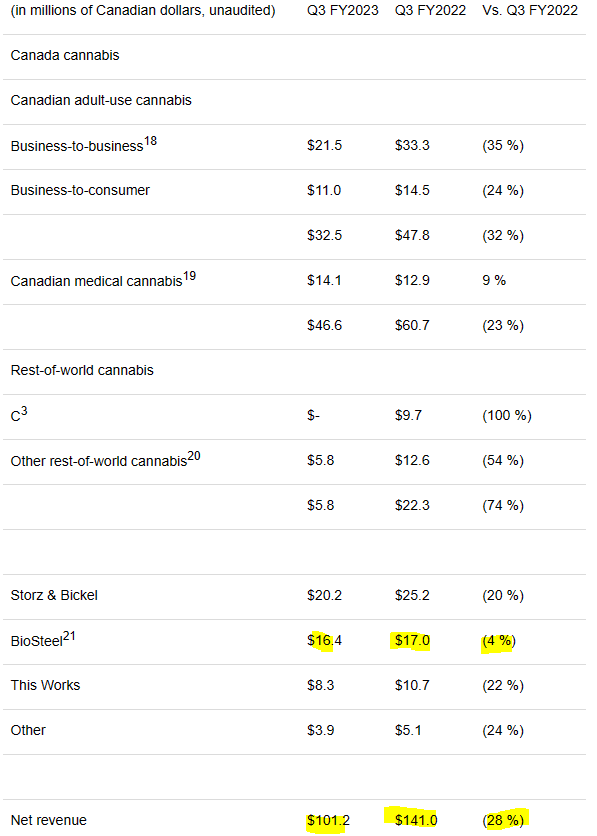

CGC has its fiscal year ending in March, so the quarter ending in December is the third quarter of the fiscal year. The top line missed by a mile with revenues coming in at $101.2 million. Estimates were close to $117 million. Note that most U.S.-based sites show estimates in U.S. Dollars, and for this quarter they were close to $87 million USD. Equally alarming was the drop year over year. Net sales dropped 28% from Q3-2023 There was a broad-based decline at every level that ranged from bad to terrifying.

CGC Quarterly Results Press Release

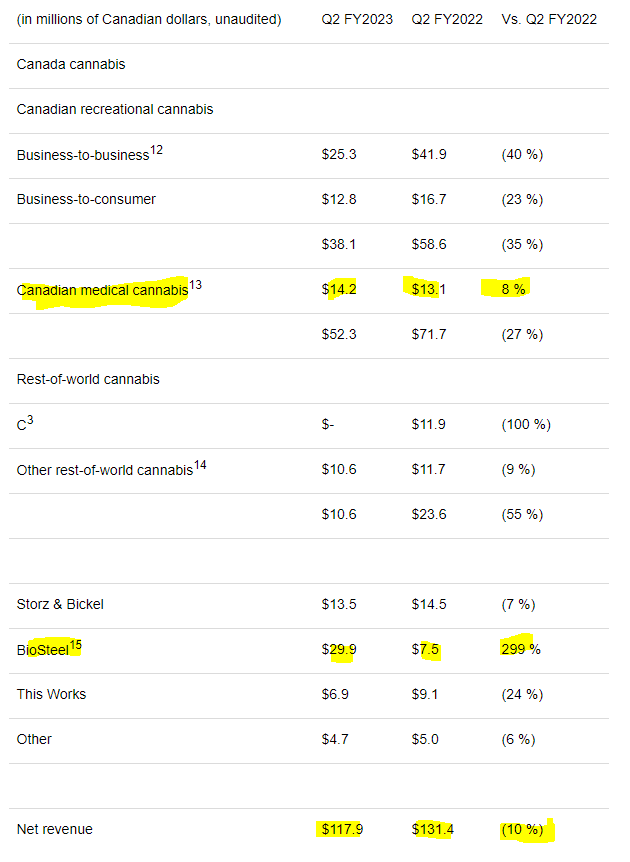

The last hope for the bulls was the growth of BioSteel. This sports/dietary supplement product line had shown some rapid growth in its early days. In fact, last quarter’s growth number was so impressive that we just went with a “Sell” rating on CGC vs a “Strong Sell.” You can see below that last quarter, BioSteel was only 1 of 2 categories that grew.

CGC Q2-2023

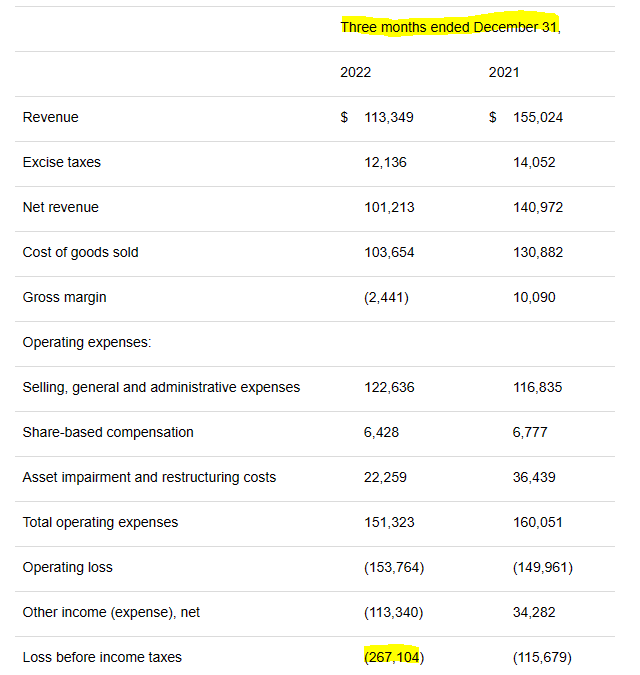

With this segment topping out, there will be little hope for the company to grow its way out of the hole they are in. And it is a very big hole indeed. The company had a net loss of $267 million in the last 3 months.

CGC Quarterly Results Press Release

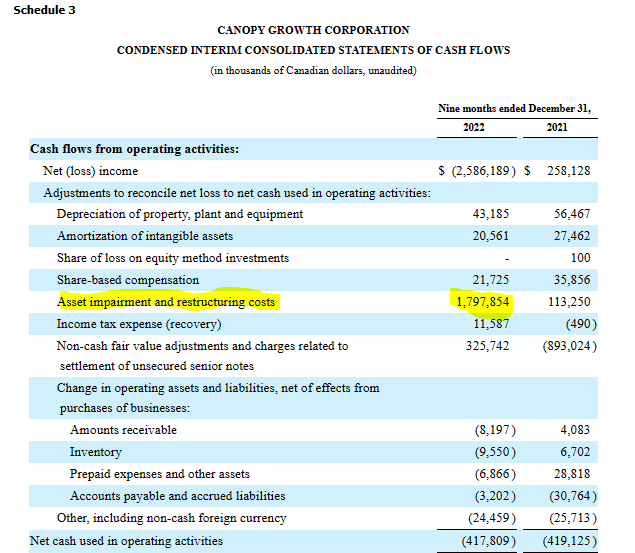

That is 15% of its market capitalization. Even if you just look at the operating loss, it is pretty brutal. We actually think the straight GAAP look is the best way to examine chronic money losers like CGC. That $1.8 billion of asset impairment over the last 9 months is a real cost.

CGC 8-K

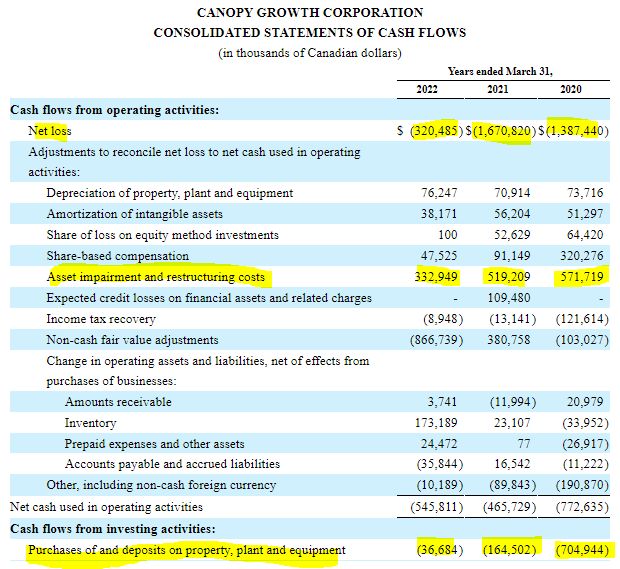

That “asset impairment” is hardly unique, either. Here are the 3 previous years.

CGC 10-K

2023 appears to be the grand finale where CGC incinerated more than the last 3 years combined. This Drogon Vs Lannisters clip does better justice than anything we can say.

Restructuring

Obviously, Canopy Growth Corporation is also aware of this, and we saw it take yet another restructuring initiative. This restructuring will involve 5 steps.

1) Canopy Growth Corporation will move to a third-party sourcing model for cannabis beverages, edibles, vapes, and extracts.

2) It will close its Ontario Research Facility and its Hershey Drive facility, alongside reduction of headcounts by 60%.

3) The target is to reduce costs by close to $300 million within a year.

4) The company plans to maintain its dual listing status and pursue its US growth plans.

5) It expects to reach a positive EBITDA run rate in 1 year, surprisingly, with the exception of BioSteel.

Outlook

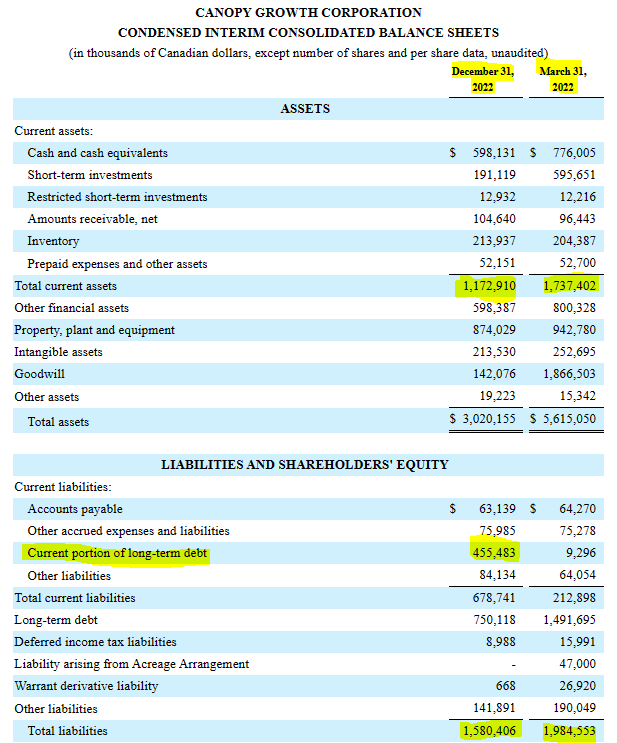

Canopy Growth Corporation’s cash burn continues unabated. In the last 9 months, current assets have fallen by about $565 million (8-K Link). Keep in mind that $213 million of total current assets is in inventories.

CGC 8-k

CGC’s debt exchange maneuver has prevented this cash drop from becoming catastrophic. But the rest of those bonds are still coming due in 6 months. Assuming that $455 million is paid off – and the bonds certainly believe this will happen – we will be down to $333 million of cash and short term investments. CGC burns through $100 million in a run of the mill quarter, although the announced restructurings will make this a more volatile number. Nonetheless, we think this is coming to a climax soon. That is because there are other hurdles for Canopy Growth Corporation to make it over the next year.

CGC’s credit facility is based on LIBOR plus 8.5%. So it will be paying a 13.5% interest pretty soon. Additionally, the credit facility requires a minimum of $200 million of liquidity at all times.

The Credit Agreement contains representations and warranties, and affirmative and negative covenants, including a financial covenant requiring minimum liquidity of US$200,000 at the end of each fiscal quarter.

Source: CGC 10-K.

Oops. Our bad. That is $200 million USD, so about $270 million in Loonie bucks. So you can see how a $100 million quarterly cash flow deficit coupled with paying off those notes means there will be a showdown in 6 months.

Verdict

We are downgrading Canopy Growth Corporation to a Strong Sell as there are only two paths left for the company. One is that banks takeover in 6 months. If paying off those notes results in a credit agreement violation the equity is worth zero. An alternate is another round of extreme dilution. This could happen by paying off the 2023 notes in shares. This would take some extreme negotiating and likely create volatility in the stock. Assuming the better outcome happens, we would expect share count to at least double from here. This comes from our assumption that the share price would have to be at a huge discount (< $1.00) to get the bond holders on board.

CGC also has some investments in other companies (see other financial assets above). These are likely extremely illiquid but represent an outside possibility of extending this drama. We recommend investors who missed the writing on the wall for the last 3 years by chasing “growth,” take this “better late than never” opportunity, to exit.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment