David Ramos

IBM (NYSE:IBM) is a legacy technology company which is known for being a pioneer in mainframe computers. This business was of course decimated by the Personal Computer [PC] revolution and Microsoft managed to ride IBM’s coat-tails before leapfrogging them to success. In recent years, IBM has focused on its new “platform” business which focuses on the hybrid cloud and Artificial Intelligence [AI] at its core. Both these are huge growth markets with the Hybrid Cloud forecast to grow at a rapid 21.06% compounded annual growth rate [CAGR] up until 2026. In addition, ~77% of I.T decision makers have announced plans to use a “hybrid cloud” I.T environment, according to an IBM cited study. I also discovered other more independent studies back up this industry trend. AI has been a hot topic recently and the industry is forecast to grow at a rapid 37.3% CAGR, up until 2030. In this post I’m going to break down, IBM’s quarterly financials, its AI/Hybrid cloud tailwinds and its valuation, let’s dive in.

Solid Financials

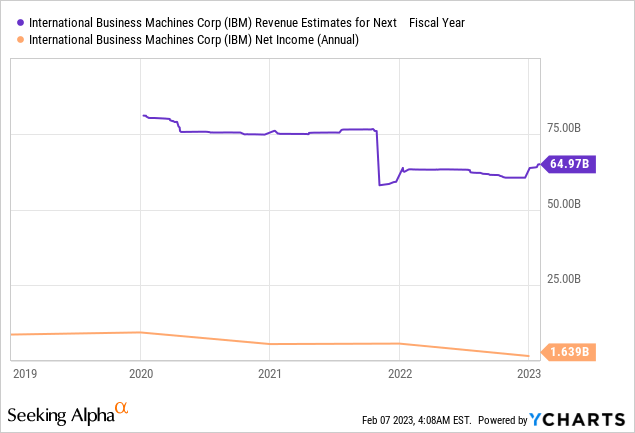

IBM generated solid financial results for the fourth quarter of 2022. Revenue was $16.7 billion, which beat analyst expectations by $313.39 million and was pretty much flat compared with the same quarter last year. This may not seem amazing but let’s keep perspective, on a constant currency basis revenue increased by 6% year over year. For a mature company founded in 1911, this isn’t bad especially as the company has previously reported negative growth rates between -4% in 2013 and -27.56% in 2019. In addition IBM is going through business model transition (which I will discuss in the next segment). On an earnings per share [EPS] basis the company reported $2.96, which increased by over 15% year over year and beat analyst estimates by $0.22 per share.

Hybrid Cloud Tailwinds

The chart below shows IBM has approximately a 3% of the cloud infrastructure market. This may not seem like a massive slice, but the “pie” is forecast to grow at a 19.9% CAGR and is expected to be worth over $1.7 trillion by 2029.

IBM market share (Statista, Synergy Research)

IBM has carved itself out as a niche provider of hybrid cloud infrastructure. A “Hybrid Cloud” basically refers to either the use of multiple cloud providers (AWZ, Microsoft Azure and Google Cloud) or a cloud provider with an on premises I.T system. Organizations are adopting this methodology for a variety of reasons. Firstly, the use of multiple cloud providers mitigates the “lock in” one cloud provider will have over its infrastructure, which has been a worry for many organisations. Secondly, using multiple cloud providers enabled specific benefits to be gained from each. For example, AWS will likely have the most cost effective infrastructure due to its scale. Whereas, Microsoft Azure has fast become a leader in Artificial Intelligence [AI] and plans to build one of the most powerful supercomputers in the world. IBM is also a strong player in this industry also and its Summit Supercomputer was ranked number 5 and number 6, on the list of the top 500 supercomputers. Many organizations are also using a hybrid cloud model due to “data residency” requirements. For example countries such as Germany, Belgium, Turkey, Brazil, China and South Korea, all require data produced on citizens to stay in the country. The U.S is also moving in this direction and has previously slammed social media growth company TikTok with accusations that it is sending U.S citizen data to China. To solve this TikTok has announced a data residency plan with Oracle who also is a hybrid cloud player. Despite Oracle being a competitor to IBM, I don’t deem this to be a negative as I believe it shows the potential of “smaller” cloud providers to fill a gap in the market.

Another popular Hybrid cloud application is in retail, which aims to use a hybrid cloud model to seamlessly converge and scale both online and offline activities.

IBM has made a huge number of acquisitions to bolster its hybrid cloud capabilities. In 2016 the company acquired Sanovi Technologies to enhance its hybrid cloud capabilities in areas such as cloud migration and recovery. Then in 2019, IBM acquired Red Hat for a staggering $34 billion in 2019, which is a hybrid cloud platform. This was a great strategic acquisition in my eyes as it enables its customers to build customised applications for a hybrid cloud environment. A prime example, would be a data residency setup (as mentioned with the TikTok deal). I forecast many other organizations (especially those in social media or finance) to follow a similar path, to keeping U.S resident data in the U.S. A recent customer win in the finance space was the Canadian Imperial Bank of Commerce [CIBC], which leveraged IBM cloud for its hybrid cloud offering. I believe banks will be a huge lucrative market, as financial companies have much stricter requirements regarding data privacy and are often cautious about sending financial data to the “cloud”. I have first hand experience of this working with banks in areas such as digital transformation, the fear of the “cloud” is deeply embedded, but hybrid cloud offers the best of both worlds. Given there is around 44,000 banks across the world, IBM has a huge opportunity in this space. Airlines is also another great area where security is of the upmost importance. For example, the largest airline in the world Delta, has a multi year agreement with IBM to move its system to a hybrid cloud to help “modernize” and automate operations.

In 2022, IBM launched its Red Hat Device Edge, which is a low friction solution for deploying “containerized” workloads onto small internet connected devices from robots to point of sale terminals. This may seem like a small feature but offers huge potential. Without going into too many technical details “containers” are the future of I.T application deployment, as they are basically packages which contain all the code required for an application to run. Thus it is no surprise that global application deployment market is forecast to grow at a rapid 33.1% compounded annual growth rate.

Platform Strategy

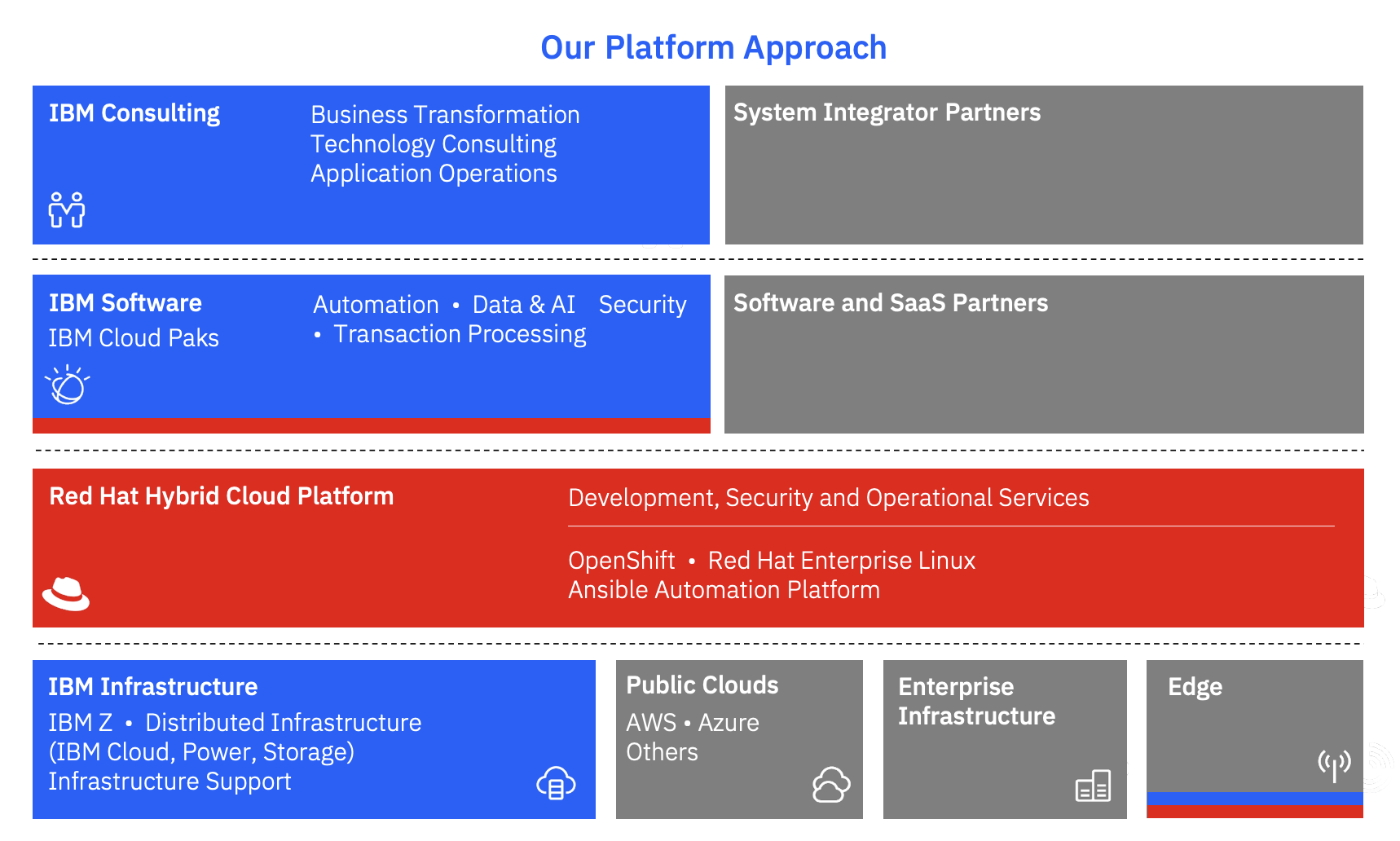

On the below graphic you can see IBM’s entire “platform approach”, which includes the Red Hat Hybrid cloud platform. This platform centric approach basically means as the company signs up a customer for its applications, IBM achieves a multiplier effect on its revenue from infrastructure and any consulting work required (I will discuss more on this later). Thus the company doesn’t need to become an infrastructure leader like AWS, as its strategy is different.

RedHat Hybrid Cloud Platform (IBM)

In fact, IBM has built out a vast partner ecosystem and scaled its presence on marketplaces by cloud infrastructure giants like AWS and Azure. This is no small section of the company and SAP, Microsoft and AWS partner revenue contributed over $1 billion in the full year of 2022. IBM also has strategic partnerships and integrations with both Adobe and Salesforce two major players in the software industry with a vast range of enterprise customers. More recently (in 2023), the company launched its “Partner Plus” program which aims to increase its scale through new and existing IBM partners.

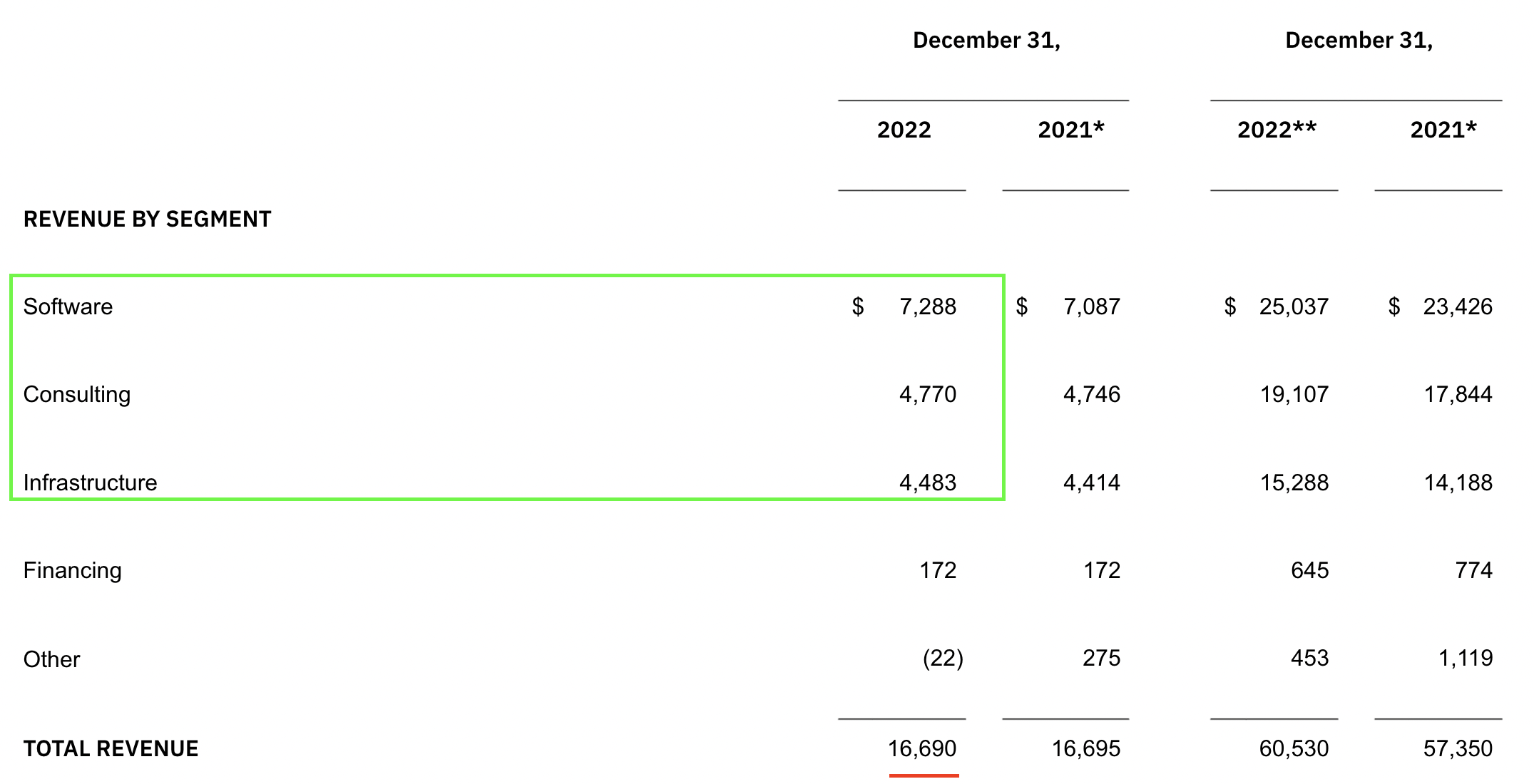

Breaking revenue down by segment, IBM reported Hybrid Cloud revenue of $22.4 billion for 2022, which increased by a solid 11% year over year or a rapid 17% on a constant currency basis. This segment now contributes ~37% of total revenue and I expect this to expand moving forward, which should drive up IBM’s overall growth rate. For the fourth quarter of 2022, its software revenue was $7.288 billion, which increased by 3% year over year or a solid 8% on a constant currency basis.

Splitting revenue down by subsections of the software segment, IBM reported strong growth in its Red Hat platform which increased sales by 10% year over year or 15% on a constant currency basis. This was driven by the aforementioned tailwinds in the hybrid cloud industry. Its other software segments, Automation, Data & AI and security also increased by 4% year over year and more than double this metric on a constant currency basis.

Revenue by segment (IBM)

As discussed above its “consulting” segment benefits from the multiplier effect of platform signups. According to one study, 70% of I.T decision makers believe they do not have employees with the right skills to help with a cloud transition. Thus IBM is leveraging its strong brand and technology expertise to help assist companies in their digital transformation journey. In Q4,22, IBM consulting reported $4.77 billion in revenue, which increased by 0.5% year over year or a solid 9.3% on a constant currency [CC] basis. This was driven by business transformation consulting (up 7% on a CC basis), technology consulting (up 10% on a CC basis) and Application Operations (up 12% on a CC basis). In the trailing 12 months, IBM consulting reported a solid $19.1 billion in revenue, which increased by 7% year over year and contributed to over one quarter of total revenue.

For finality, IBM also reported infrastructure revenue of $4.48 billion which increased by ~1.56% year over year or 7% on a constant currency basis.

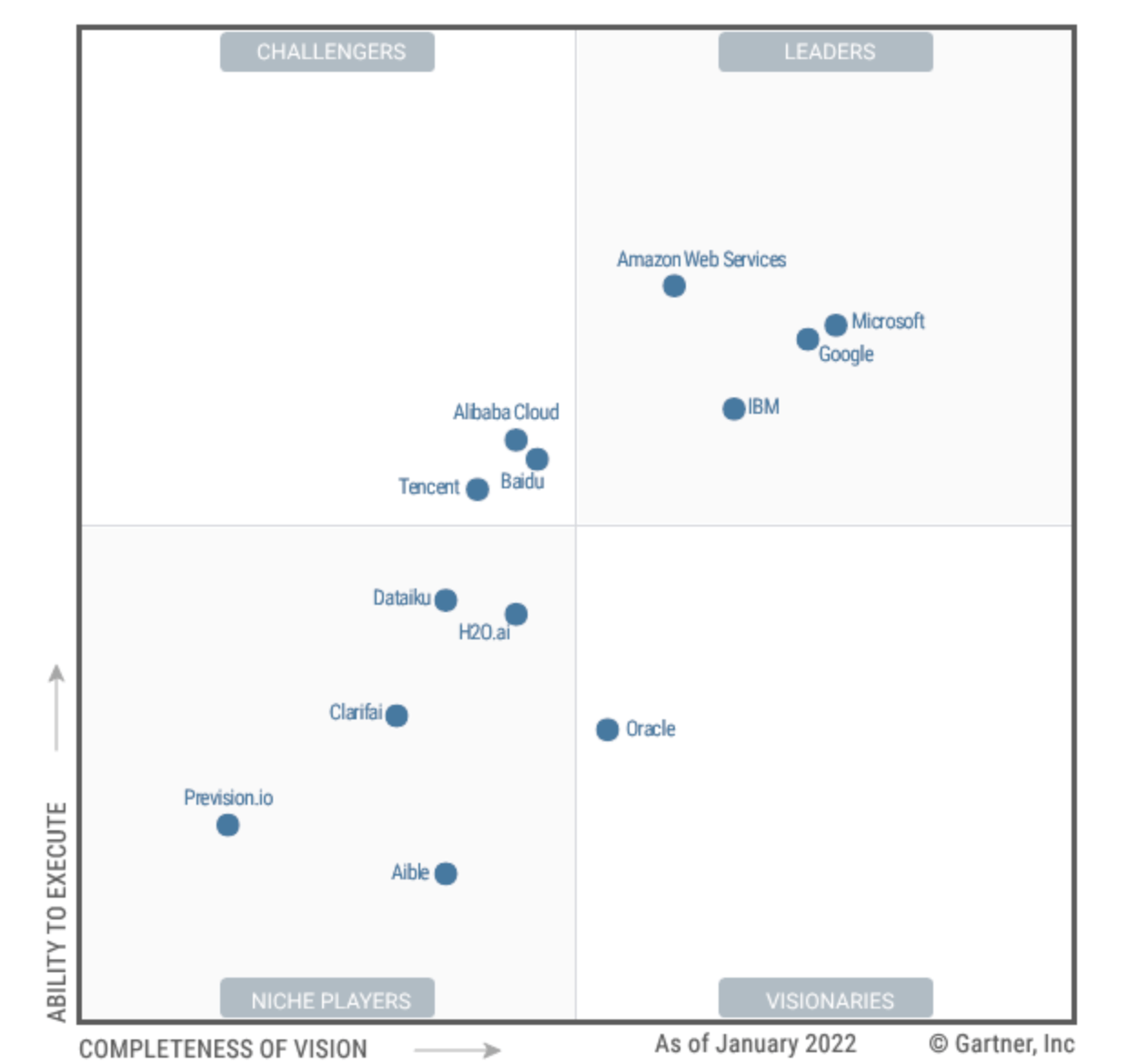

The AI Opportunity

“Big Data” and “AI” are huge growing markets I forecast IBM to benefit from. Many large organizations often have tonnes of data in “silos” but through the use of the cloud, IBM can help to bring this data together and then run AI and machine learning on it to unlock new insights. The company has been a leader in the industry for many years and is has over 2,300 AI related patents. In addition, the company is a Gartner Magic Quadrant leader in AI developer services.

Cloud AI developer services (Gartner)

IBM’s strategy is to focus on the productivity enhancements offered by AI and believed it can help enterprises to execute AI at scale. Example applications, include automated the rollout of CV19 vaccines and using AI chatbots to reduce contact phone center resources.

The BBC is now using our AIOps software to automate the management of its IT infrastructure. For businesses, deploying AI can be challenging because it takes time to train each model. But by using large language models, companies can now create multiple models using the same data set. This means businesses can deploy AI with a fraction of the time and resources. That is why we are investing in large language, our foundation models for our clients and have infused these capabilities across our AI portfolio. Another more complicated example, is the usage of “AIOps” to automate I.T operations are major television broadcasters such as the BBC.

Given the AI industry is forecast to be worth over $1.3 trillion by 2029, IBM has a huge opportunity to ride this trend.

Valuation and Forecasts

In order to value IBM I have plugged its latest financial data into my discounted cash flow valuation model. I have forecast 6.5% revenue growth for “next year” or the full year of 2023. This is based upon Yahoo finance analyst estimates and strong growth in its Hybrid cloud segment which grew revenue by ~11% year over year (or 17% on an FX neutral basis). In years 2 to 5, I have forecast even more optimistic growth rates of 12% per year. This is based upon a few factors. Firstly, I forecast a rebound from the “recessionary environment” (post 2023), as historically the economic cycles have been cyclical by nature. Foreign exchange rates are also likely to adjust and we have already seen signs of the U.S dollar finally weakening against the Euro, after a major strengthening, which has impacted IBM’s international revenue. A catalyst such as an end of the war in Ukraine could also present favorable tailwinds for IBM’s international segments and the currency rates.

In addition, I have based this growth rate on the rapid industry growth forecasted in areas such as AI, Hybrid Cloud etc (I have previously cited analyst reports above). IBM’s partner strategy will continue to grow as this should further help to accelerate revenue.

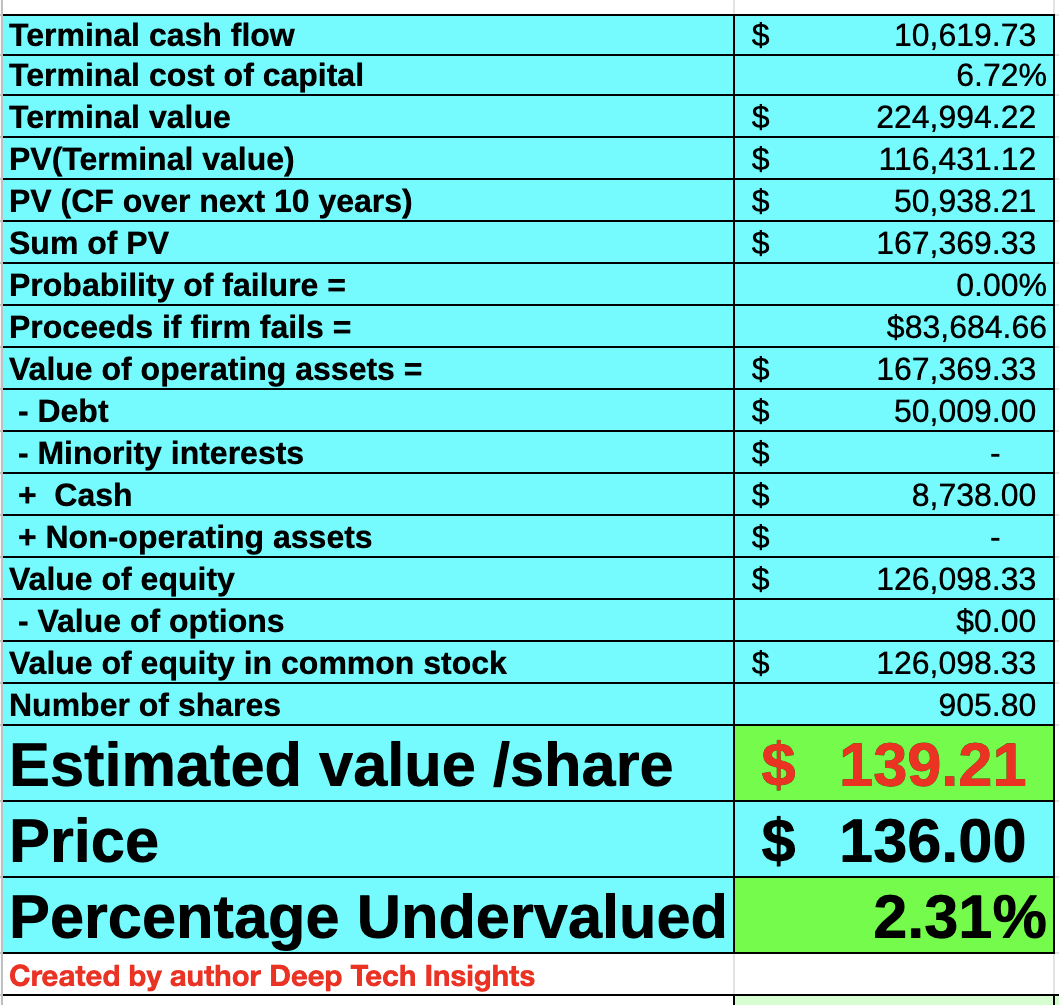

IBM stock valuation 1 (created by author Deep Tech Insights)

To increase the accuracy of the valuation model I have capitalized the company’s R&D expenses, which has boosted net income slightly. Over the next 5 years I have forecast a 20% operating margin. This is optimistic but not unachievable. In the most recent quarter (Q4,22) the company reported a pre tax operating margin of 19.8%. In addition, in Q4,20 its operating margin was over 32.4%. However, it has varied over the past few quarters. Long term as the company continued to grow its software business, this should result in higher margins for the company overall.

In my model, I have also taken into account IBM’s cash and marketable securities of ~$8.8 billion. In addition, to the company’s $50.9 billion of debt, which is extremely high but down $0.8 billion since the end of 2021. Another positive is the majority of its debt ($46.189 billion) is “long term debt” and thus manageable (data from IBM balance sheet).

IBM stock valuation 2 (created by author Deep Tech Insights)

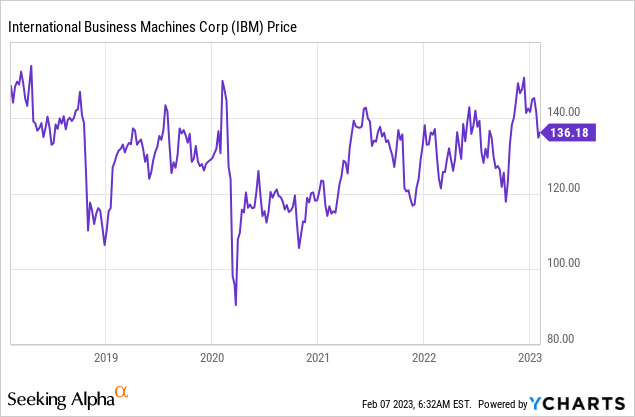

Given these forecasts and financials, I achieve an intrinsic value of IBM stock of ~$139 per share. Its stock is currently trading at ~$136/share at the time of writing and thus is 2.31% undervalued. My investment strategy focuses on investing into stocks which trade at least 20% below its intrinsic value, in order to give a margin of safety (Warren Buffett and Benjamin Graham) also use a similar method. Thus in this case, as IBM is only slightly undervalued I will label the stock as a “hold”.

As an extra datapoint its non GAAP P/E ratio = 14.35x, which is 21.56% higher than its 5 year average. However, relative to other hybrid cloud providers such as Oracle and technology companies such as SAP and Microsoft, IBM is trading the cheapest on a P/E ratio basis.

Risks

Recession/Russia Exit

Many analysts have forecast a recession in 2023. This may impact the number of customers moving to the cloud as they aim to delay spending cycles. A positive is we are not seeing major signs of this yet. IBM’s high debt could also be a risk as even though the majority is long term, if interest rates do not fall back to “normal” low levels, this could mean a high debt servicing cost for the business.

IBM is also facing headwinds from its exit from Russia, which has already cost the company ~$600 million in profit and cash lost. However, if/when the Ukraine-Russia war finishes and perhaps a regime change occurs, Russia could open up long term (5 year to 10 year period). This seems unlikely currently but remember even Germany reopened for business after it was involved in world wars.

Final Thoughts

IBM has a strong brand, over 40,000 patents and huge foundation of state of the art technology. The company’s hybrid cloud and AI focused strategy has major potential given the growth in the market and IBM’s solid leadership position. The business is currently facing a series of headwinds from a tough foreign exchange rate market, but I do not believe this will result in a negative impact long term. Its stock is trading close to my intrinsic “fair value” calculation, but I would personally like to see a pullback before entering.

Be the first to comment