MagioreStock/iStock Editorial via Getty Images

Today, most of my wealth is invested in REITs (VNQ) that own defensive real assets such as farmland, apartment communities, industrial warehouses, and grocery-anchored strip centers.

In my mind, they offer the best risk-to-reward in today’s environment because rents are today growing the fastest in decades and their valuations are deeply discounted.

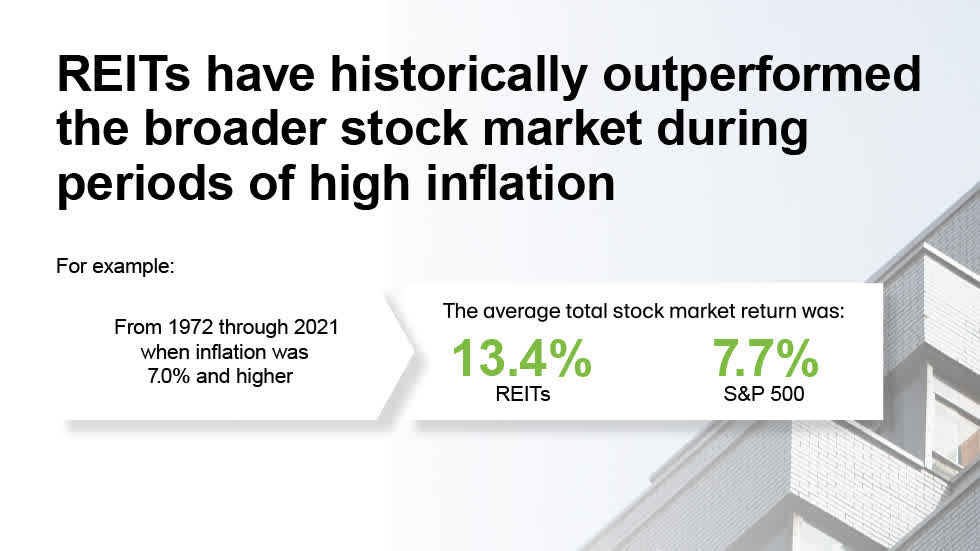

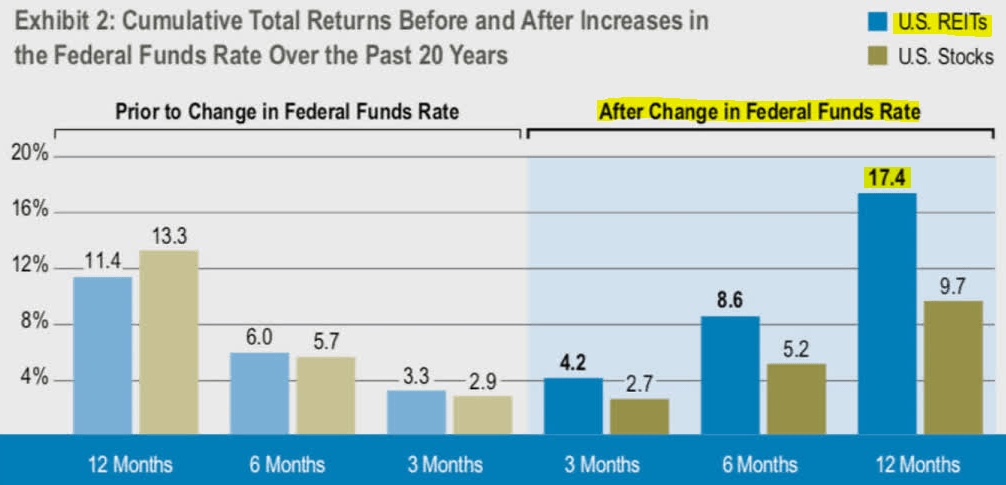

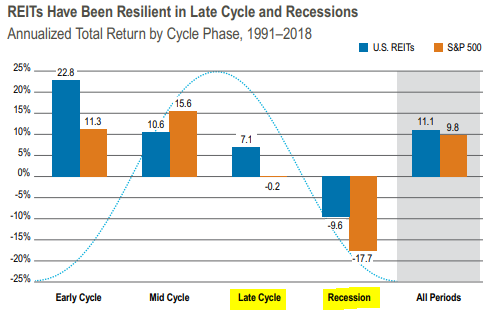

Moreover, REITs have historically performed especially well during time periods of inflation, rising interest rates, and recessions – which is very representative of today’s environment:

REITs outperform inflation is high (NAREIT) REITs outperform during times of rising interest rates (Cohen & Steers) REITs outperform during recessions (Cohen & Steers)

While REITs make up the lion’s share of my portfolio, I have recently begun to accumulate a number of tech stocks (QQQ).

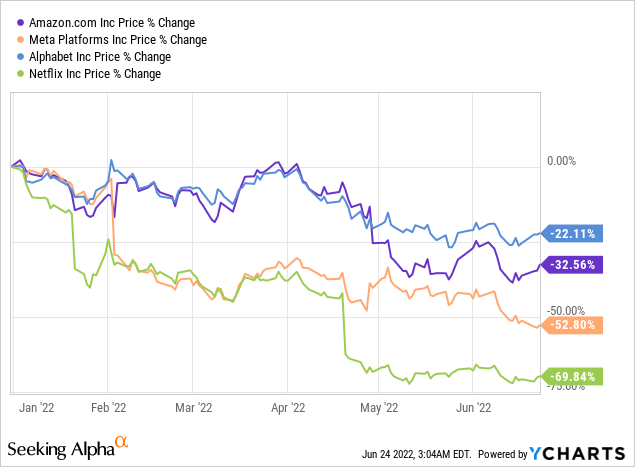

They have dropped so much that they are hard to ignore.

Alphabet (GOOG, GOOGL) is down 22%…

Amazon (AMZN) is down 32%…

Meta Platforms (META) is down 53%…

And Netflix (NFLX) is down as much as 70%!

That’s just this year alone.

And if these large and well-known tech companies are down as much, you can imagine that many of the smaller and lesser-known tech companies are down even more heavily. The drop has been so severe that some call it the dot-com crash 2.0.

What’s causing it?

Valuations were excessive. As we noted in late 2021, trees don’t grow to the sky, and market sentiment is fickle:

One of the main reasons why tech stocks did so well over the past decade is that their valuation multiples expanded drastically. If your valuation goes from 20x earnings to 40x earnings, that’s a 100% gain without even accounting for the growth in earnings. Add to that some earning growth and the returns are exponential.

But the issue here is that multiples cannot expand forever. Could that same stock go from 40x to 50x earnings? Maybe. But it could just as well stagnate at 40x or head back down to 20x if its prospects deteriorate. The higher the multiple, the lower the future upside potential, and the higher the downside risk.”

That’s precisely what happened. Future prospects first began to deteriorate when the world reopened and we slowly moved past the pandemic. Then, things got a lot worse when inflation surged to multi-decade highs and interest rates began to rise.

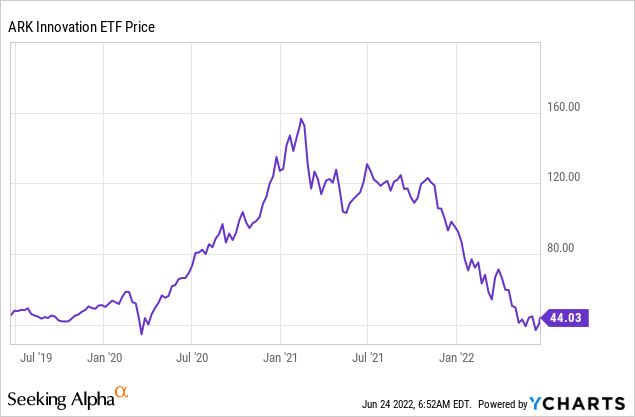

Suddenly, the market couldn’t justify these high multiples anymore, and as they deflated, share prices collapsed. The ARK Innovation ETF (ARKK), which did so well early into the pandemic, is now back to its pre-covid-19 levels:

But as a result of this crash, valuations have again become quite compelling in the tech sector. Earlier, we said that “the higher the multiple, the lower the future upside potential, and the higher the downside risk,” but the opposite is also true.

There are a number of tech stocks that enjoy strong future prospects, irrespective of the pandemic, and they are now priced at very reasonable valuation multiples that could expand once inflationary pressures cool off.

Their risk-to-reward has improved materially, and in what follows, I highlight two tech stocks that I have been accumulating over the past months:

Fintech companies have sold off particularly heavily.

Popular names in this space include PayPal (PYPL) and Block (SQ). They both have over 200,000 followers here on Seeking Alpha.

I personally prefer Wise plc, which is a much smaller peer that’s overlooked by most investors. It only has 2,000 followers on Seeking Alpha.

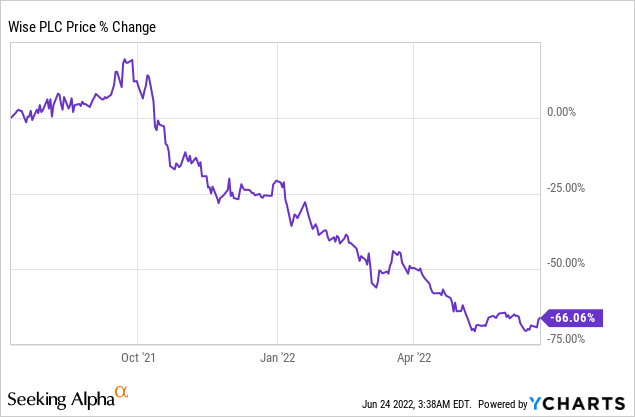

The company recently went public, but I have been a client of them for years prior to that, allowing me to get familiar with their products ahead of their listing. Since then, it has dropped like a rock along with other fintech companies, offering a great entry point for people familiar with the company:

In short, I believe that Wise has the potential to revolutionize international banking. They have created an alternative payment infrastructure that connects local payment systems around the world and allows people and businesses to make international money transfers at a fraction of the cost. I use it all the time for my business and have not been able to find a better alternative.

PayPal promotes itself as a low-cost alternative to banks, but in reality, it is much more expensive than Wise. It is interesting to note that two of PayPal’s co-founders actually invested in Wise. Here’s what Peter Thiel said about it:

“Wise demonstrates true innovation in banking by enabling its users to retain their wealth across borders, instead of paying big fees to big banks.” Peter Thiel, co-founder of PayPal

Wise vs. PayPal (Wise)

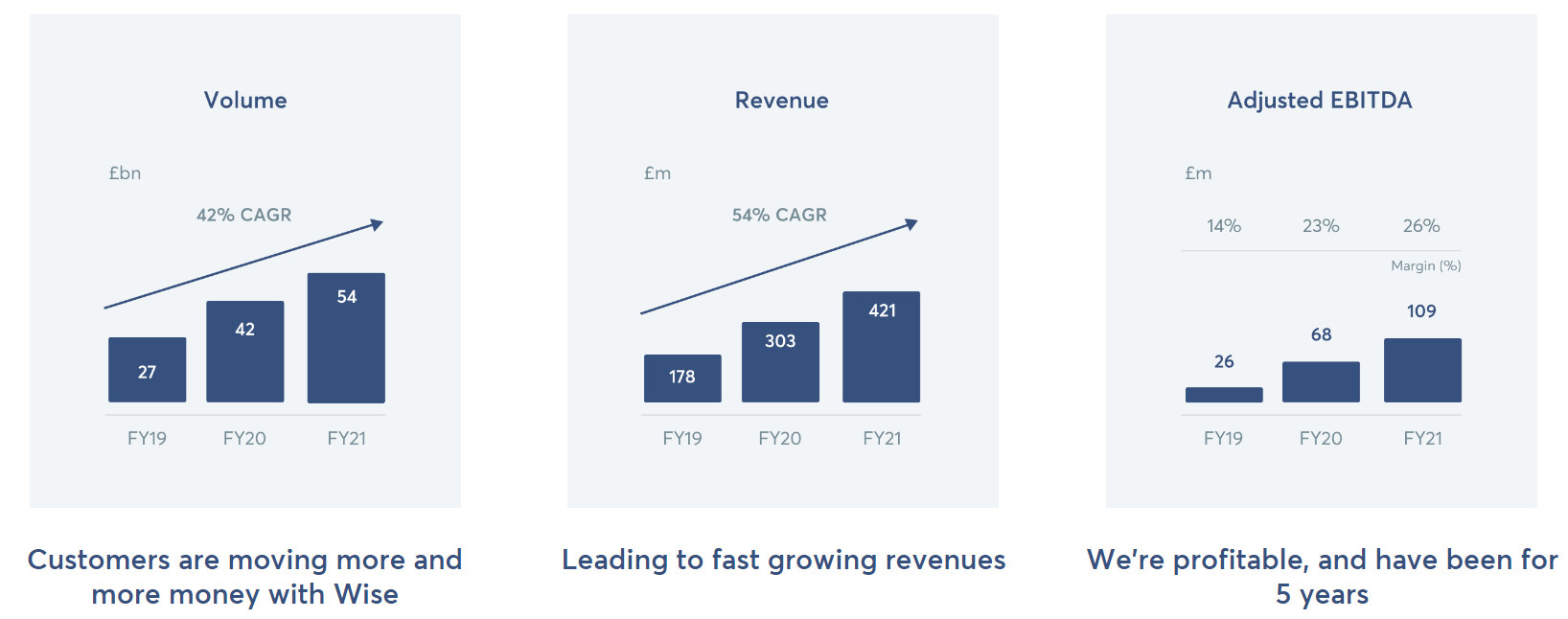

Best of all, the company is already profitable and is growing rapidly, while keeping a focus on profitability. Over the past year, the company grew its volumes by 44% and its free cash flow by 39%:

Wise is profitable and growing rapidly (Wise)

Currently, the company is priced at ~25x its forward free cash flow which is exceptionally cheap for a tech company with such rapid growth prospects.

The reason why it is so cheap is that the company kept on growing even as its share price lost 2/3 of its value.

PAR Technology Corporation (PAR)

Most investors are attracted by exciting tech stories like Zoom (ZM), Peloton (PTON), or even Coinbase (COIN). But excitement is probably what you should run away from when investing.

PAR Technology is a fairly boring tech play in the restaurant industry, but it is very compelling as an investment opportunity.

PAR invented what we call the modern point-of-sale terminal around 40 years ago. This is the big screen where orders are entered at McDonald’s (MCD) restaurants as an example:

PAR point of sale terminal (PAR Technology)

This product was a big hit. Soon after creating it, major restaurant chains began using it and PAR become a major tech hardware business.

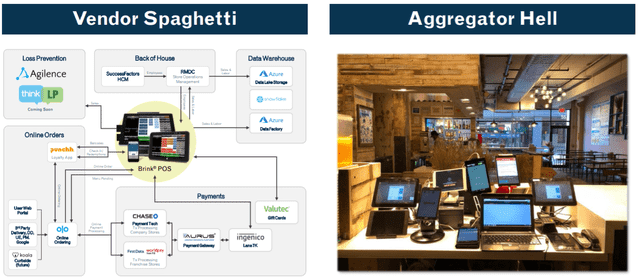

But as tech needs evolved over time, PAR missed the boat, forcing its customers to purchase additional hardware/software from other companies. This led to what they call the “tablet hell”:

Tablet hell (PAR Technology)

For a long time, PAR was a family business, and the management was likely resting on their laurels. But they finally recognized this issue and after changing the management, they began to transform themselves from a boring hardware company into a one-stop shop for all restaurant tech needs.

Their new CEO comes from a SaaS / Tech investment background and he rapidly began to transition PAR into the SaaS model, acquiring important restaurant software and integrating them into the PAR point-of-sale terminal to resolve the “tablet hell.”

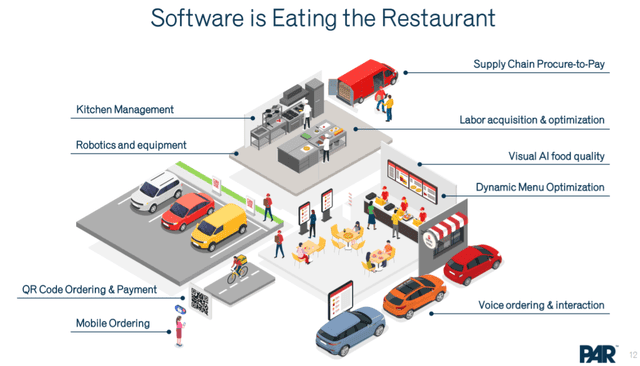

Restaurants love it because it allows them to consolidate all data under one system, which then leads to more efficiencies, cost optimization, and higher margins.

Tech in restaurants (PAR Technology)

The total addressable market (“TAM”) is massive, and PAR has a major competitive advantage. They are the creators of the point-of-sale terminal and have decades-long relationships with most major restaurant chains. Now they are finally adapting it to today’s world and adding clients under subscription payment structures to benefit from their all-in-one products.

And the early results are very impressive.

In just a few years, they went from $14 million to nearly $100 million of annual recurring SaaS revenue:

PAR’s growing ARR (PAR Technology)

They have now essentially proven the concept, but they are still just getting started. Yet, the share price of the company is not reflective of it. They are priced at just 8x their forward ARR and they are still very early in their growth phase.

Panera Bread’s founder and CEO took a major position in the company at $68 per share. He noted that he typically only invests in situations where he has an insider understanding of the product itself and since he has been a major client of PAR for a long time, he really understands the company and where it is likely going.

Right now, you have the chance to invest in the company at a 2x lower valuation than him.

Bottom Line

Most tech companies were overpriced in 2020 and 2021.

Today, some of these companies are becoming increasingly compelling, and I would put Wise and PAR on that list.

Most of my investments remain in REITs and I believe that they offer the best risk-to-reward in today’s world, but I am now also growing my tech portfolio to seek greater diversification.

Be the first to comment