I like buying stocks way more than I like shorting anything. I used to be a somewhat active short seller in the early years of my investing journey. Now, I use every opportunity to look for value – even if it means waiting a bit before new opportunities present themselves.

In this article, I will walk you through my thoughts on the housing market. The housing market is rapidly weakening, posing a serious risk for the US economy. While mortgage rates have come down, affordability issues are weighing on sales and homebuilding demand. As a result, prices are falling, transactions are plummeting, and homebuilders are increasingly depressed when it comes to the outlook.

However, instead of shorting anything or panicking, I’m working on a list of stocks I want to buy on weakness. Hence, in addition to giving you my 2023 housing outlook, I will share some housing plays for dividend investors. Stocks that investors will enjoy for wealth generation for hopefully decades to come.

But before we do that, we need to work out way through some pretty bad indicators.

So, let’s get to it!

Housing In 2023 – Buckle Up

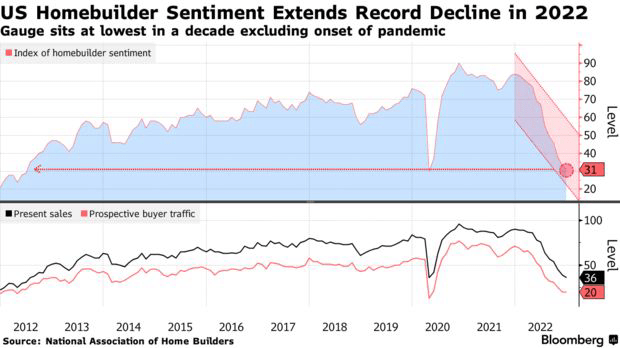

Every month, I check the NAHB (National Association of Home Builders) housing market index. This index is a monthly survey of NAHB members designed to take the pulse of the single-family housing market.

Homebuilding sentiment is now at 31. That’s the lowest number since the pandemic panic. Ignoring that flash crash, sentiment hasn’t been this low since 2012. And 2012 marked the start of the post-recession housing rebound. Now, we’re back after 10 years.

Bloomberg

According to the NAHB, a mix of high mortgage rates, elevated construction costs, and flagging consumer demand have caused the homebuilding index to fall in every single month of 2022.

“Our latest survey shows 62% of builders are using incentives to bolster sales, including providing mortgage rate buy-downs, paying points for buyers and offering price reductions. But with construction costs up more than 30% since inflation began to take off at the beginning of the year, there is little room for builders to cut prices.

The worst part is that these developments aren’t short-term developments. We’re not in a scenario where the Fed hikes for a year and will now return to normal with the surge in rates being a short-term phenomenon.

In a recent article, titled “Buckle Up, It’s A New Investment Era,” I discussed the changing market environment. Even if we’re past peak inflation, we’re unlikely to return to a scenario where inflation is low (normalized), central bank rates are close to zero, and supply chain and other secular headwinds are solved. At least not anytime soon.

In that article, I quoted Howard Marks’ latest memo, which hit the nail on the head when he covered major economic changes that are likely here to stay for a while.

– While some recent inflation readings have been encouraging in this regard, the labor market is still very tight, wages are rising, and the economy is growing strongly.

– Globalization is slowing or reversing. If this trend continues, we will lose its significant deflationary influence. (Importantly, consumer durables prices declined by 40% over the years 1995-2020, no doubt thanks to less-expensive imports. I estimate that this took 0.6% per year off the rate of inflation.)

– Before declaring victory on inflation, the Fed will need to be convinced not only that inflation has settled near the 2% target, but also that inflationary psychology has been extinguished. To accomplish this, the Fed will likely want to see a positive real fed funds rate – at present, it’s minus 2.2%.

– The Fed faces the question of what to do about its balance sheet, which grew from $4 trillion to almost $9 trillion due to its purchases of bonds. Allowing its holdings of bonds to mature and roll off (or, somewhat less likely, make sales) would withdraw significant liquidity from the economy, restricting growth.

These developments are hurting the American housing market.

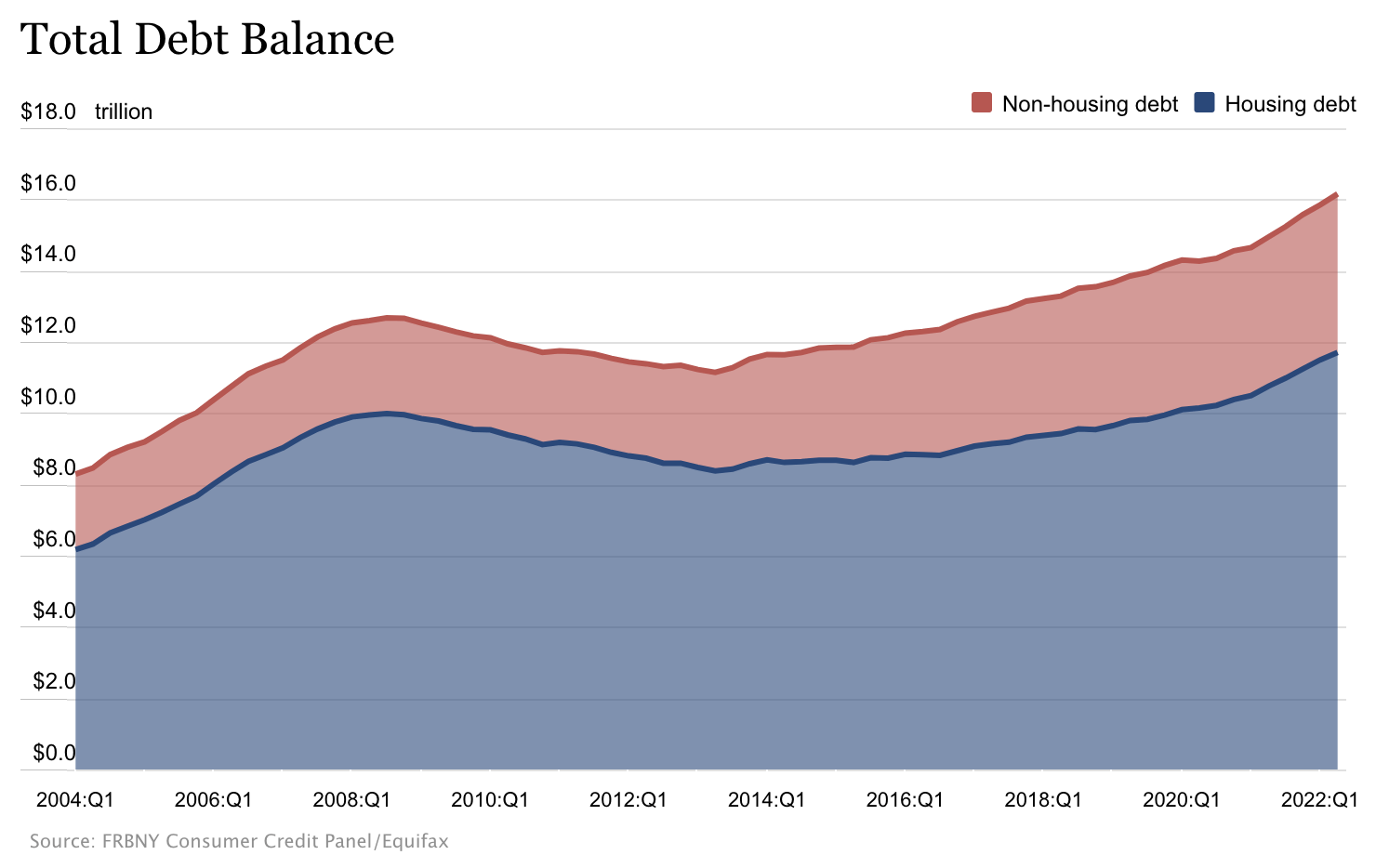

While everyone knows that a weak housing market is a bad thing, it’s worse than some might believe. Protecting the housing market means protecting the quality of debt. After all, almost all deals are debt-financed. As I wrote in September, total housing debt was close to $12 trillion in the first quarter of this year. While that data is a bit old, it is still valid for what I’m trying to achieve here.

Housing debt was 72% of total debt, according to New York Fed data. Protecting the quality of that debt is important. Failing to do so will lead almost certainly to a steep recession with risks of a chain reaction.

Federal Reserve Bank of New York

And it’s not only debt, housing-related economic activities are a massive pillar of GDP.

As of 2020, spending on residential fixed investment was about $885 billion, accounting for about 4.2% of GDP. Second, GDP includes all spending on housing services, which includes renters’ rents and utilities and homeowners’ imputed rent and utility payments. As of 2020, spending on housing services was about $2.8trillion, accounting for 13.3% of GDP. Taken together, spending within the housing market accounted for 17.5% of GDP in 2020.

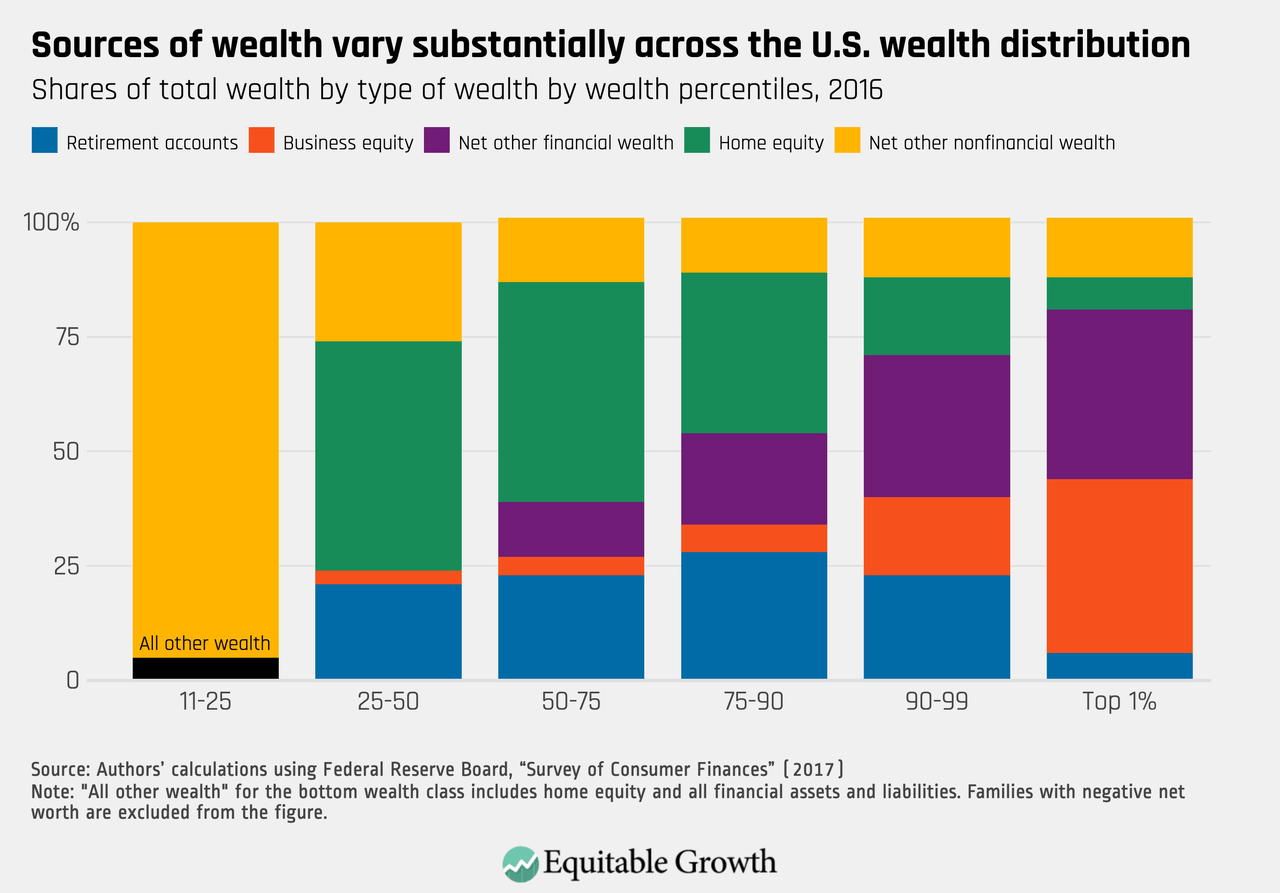

Moreover, a huge part of middle-class wealth is stored in the housing market via home equity. Reducing that will impact consumption and whatnot.

Equitable Growth

In this case, issues are going far beyond housing. For example, almost 30% of auto loans for used vehicles now exceed six years. In 2020, that number was less than 20%.

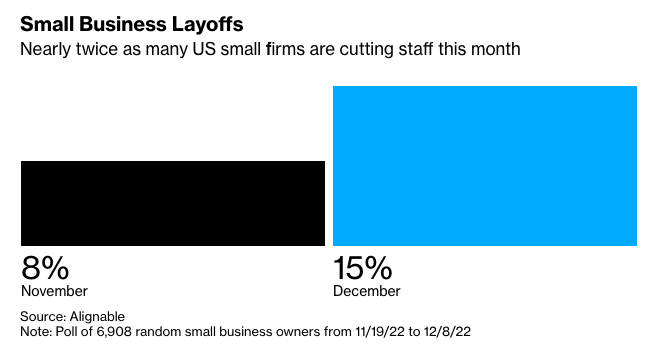

It also does not help that small business layoffs are starting to rise – despite non-farm payrolls painting a somewhat rosy picture. In December, 15% of small firms were cutting staff. That’s up from 8% in November.

Bloomberg

It’s a situation where people with lower and middle-class income (the biggest share of the population) cannot afford homes, while people who own homes are not willing to sell, knowing that great sales prices are likely out of reach.

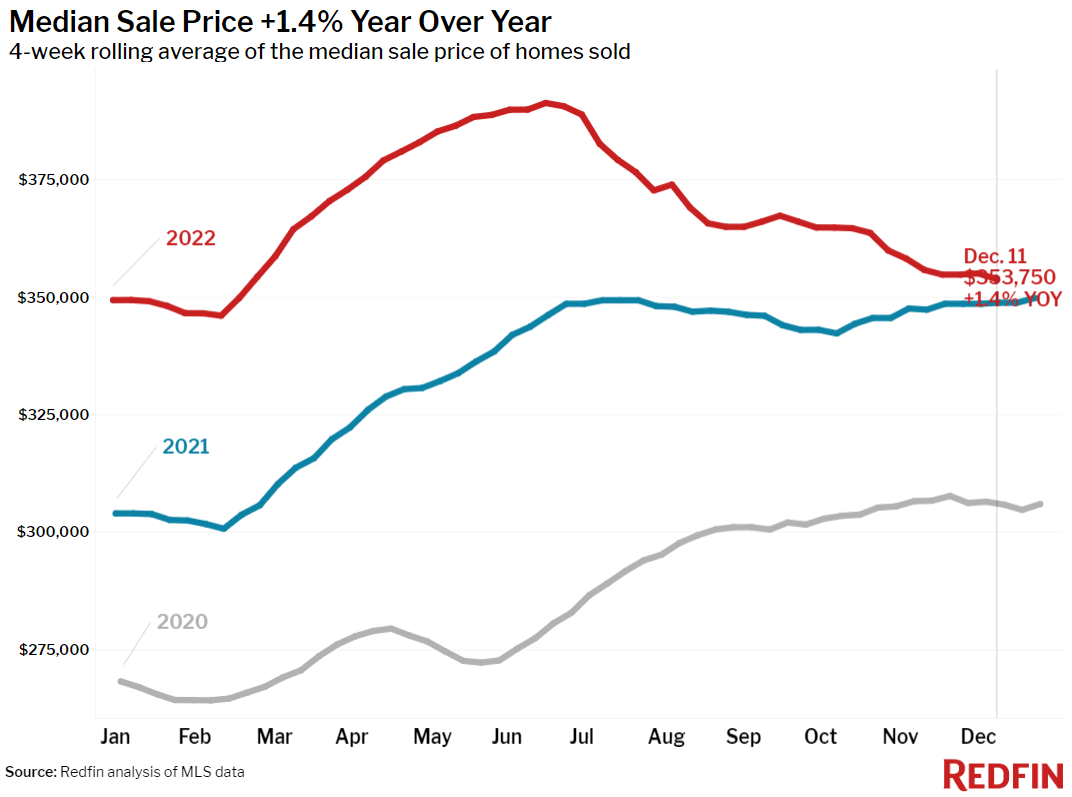

Redfin showed that the median sales price of homes sold is now just 1.4% higher compared to the prior-year period. The mild decline in mortgage rates to 6.3% (as of December 11) was not able to stop the decline in prices.

Redfin

That’s no surprise as affordability is still a mess. Even as mortgage rates have come down a bit, the median monthly mortgage payment is still close to $2,300. In 2020, that number was close to $1,500.

There are more signs of weakness. In December only 24.7% of homes were sold above the list price. That is still elevated. However, it’s down from 40% in December of 2021. The average home sold for 98.3% of the list price.

With all of this said so far, I believe that the first serious cracks in the housing market have appeared. While I’m not trying to predict the next housing crash, it’s something that worries me as it impacts the economy as a whole.

Moreover, one of the reasons why I’m writing this article is to explain why a short-term decline in rates is not the end of these issues.

With mortgage rates retreating from their highest since 2002 and the US housing market cooling, some buyers are expecting to get a deal next year instead of having to contend with sky-high home prices. Unfortunately, that’s just wishful thinking.

After all, prices have risen so much that normalization would require a lot of pain. In order to push mortgage payments back to the historic average of 18% of household income, prices would have to drop 39%. That’s a big number and very bad news for everyone who was “forced” to buy a house during the past two years.

That isn’t going to happen so easily as the housing supply isn’t that high while demand for housing is still high – affordable housing that is.

There are also now more young middle-aged adults (“elder Millennials”) eager to buy. That will help to keep home prices propped up, says Len Kiefer, Freddie Mac’s deputy chief economist. That’s another key difference with the early aughts, when there just weren’t as many homebuying Gen X’ers, the smallest generation.

However, as I already said, cracks are appearing. Right now, every house has 2.4 offers, on average. That’s down from 5.5 offers earlier this year.

If the Fed is serious about fighting inflation (really serious), it will maintain high rates throughout 2023. It would maintain a high level of unaffordability in the housing market and slowly but painfully harm participants with high debt levels (and variable rates). It would eventually hurt demand, causing supply to grow. Prices would fall, hurting overall economic growth and inflation.

Apparently, I’m not the only one with that view. In November, I wrote a housing article, which included the view of large players that had created big funds to buy residential real estate. At this point, a lot of big guys are sitting on the sidelines waiting for the following things to happen:

High rates and economic weakness weaken the housing market.

Eventually, unemployment comes down as these developments hurt the economy as a whole.

The Fed will pivot as the economy has weakened along with inflation.

Large players with cash reserves start buying, outbidding the average private buyer who suffers from a weak economy (high unemployment)

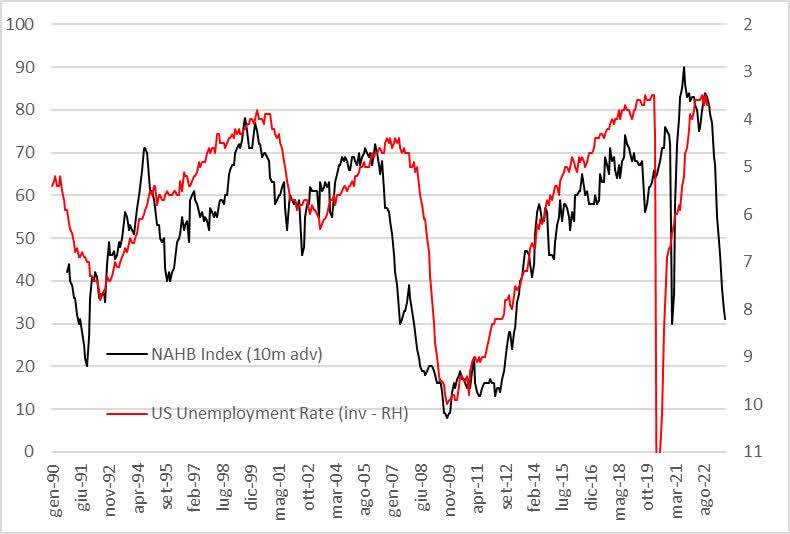

On a side note, this is what the comparison between the aforementioned NHAB housing market index and unemployment looks like.

Bear Traps Report

With that said, let’s quickly summarize this part before we move to the stock selection part of this article.

What To Expect In 2023?

The housing market is showing cracks. I believe we’re in a situation where we see gradual weakness in home prices and related economic indicators like GDP growth and unemployment. My view is that “smart” money is going to be right. We will likely encounter a situation where the Fed will be forced to pivot. That could be in the second half of 2023 if we assume that the Fed will keep hiking unless the economy becomes really weak.

At that point, we’re likely dealing with higher unemployment and lower rates. That’s when buying demand will come back roaring.

While I have consistently added to my housing-related plays, I’m keeping a larger-than-usual cash position to benefit from this situation (if it occurs).

Now, onto the stock selection.

The Stock Selection In This Article

The message of this article is rather bearish. However, none of the picks in this article are short plays. That has two reasons.

I quit covering short ideas many years ago, as I know that it’s simply too risky for a lot of people. It would do more harm than good. There are obviously exceptions, but you get my point.

I’m not a short-seller anymore. I have become somewhat of a long-term value buyer with almost all of my money invested in long-term investments. I buy weakness and undervaluation.

Hence, I covered the strategy of big buyers, who remain on the sidelines until they see prices they like.

That’s what I’m going to do here as well. I will give you three dividend (growth) stocks that – I believe – are great buys on weakness. They’re all on my list, and there’s a big chance I will own at least two of the three at the end of next year.

Please note that there are so many good opportunities. In this article, I went with three picks. All of them are operating in different industries related to the housing market.

Use the comment section if you disagree or agree with me, or if you have picks that you like to share with the crowd.

Now, onto the stocks, before this article gets too long.

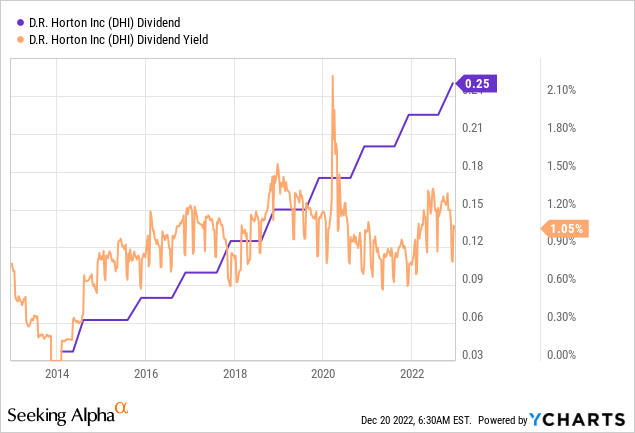

I’m starting this article with the riskiest, low-yielding stock on my list. With a quarterly dividend of $0.25 per share, D. R. Horton yields just 1.1%.

That’s obviously not enough to get anyone excited. Especially not as yields have increased due to the ongoing bear market.

DHI is a recession wild card.

Hence, in November, I wrote an article titled “Keep An Eye On D.R. Horton In 2023.”

D.R. Horton is my favorite homebuilder stock based on a number of qualities.

For starters, it dominates a number of key markets like Dallas Fort-Worth, Houston, Atlanta, Phoenix, and Austin.

D.R. Horton

D.R. Horton has a 12% market share in the single-family homebuilding industry. This market share has consistently grown through many cycles.

D.R. Horton

That’s no surprise. The company is the largest homebuilder in key markets in the Sun Belt. These areas have enjoyed more growth than some of the large markets on the West Coast and Northeast.

Moreover, D.R. Horton focuses on affordable housing. Even in 2022, more than 67% of homes were closed with a price tag of less than $400,000. Less than 13% of homes sold at a price of more than $500,000.

Hence, the company was able to outperform its peers by a wide margin over the past ten years – and prior to that.

Needless to say, a company this size is unable to escape market weakness. This is what the company said in its recent earnings call.

[…] we began to see a moderation in housing demand that has continued and accelerated through today. The rapid rise in mortgage rates, coupled with high inflation and general economic uncertainty, have made many buyers pause in their home-buying decision or choose to not move forward with their home purchase. However, the supply of both new and resell homes at affordable price points remains limited and the demographics supporting housing demand remained favorable.

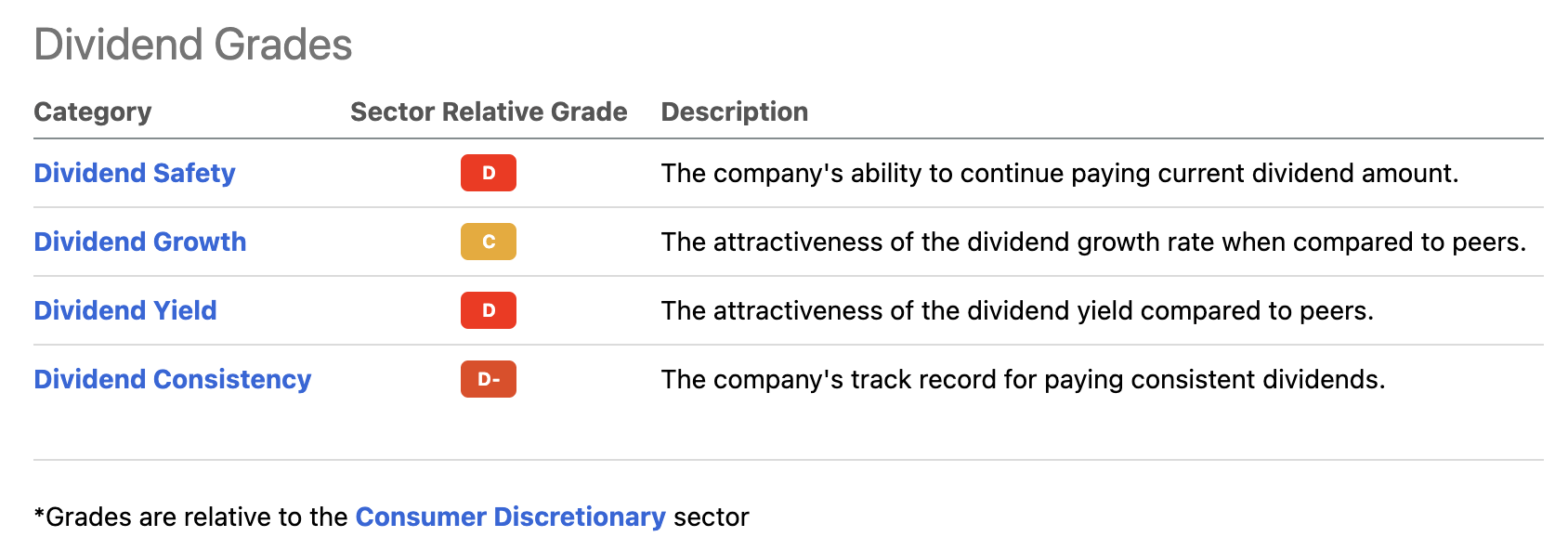

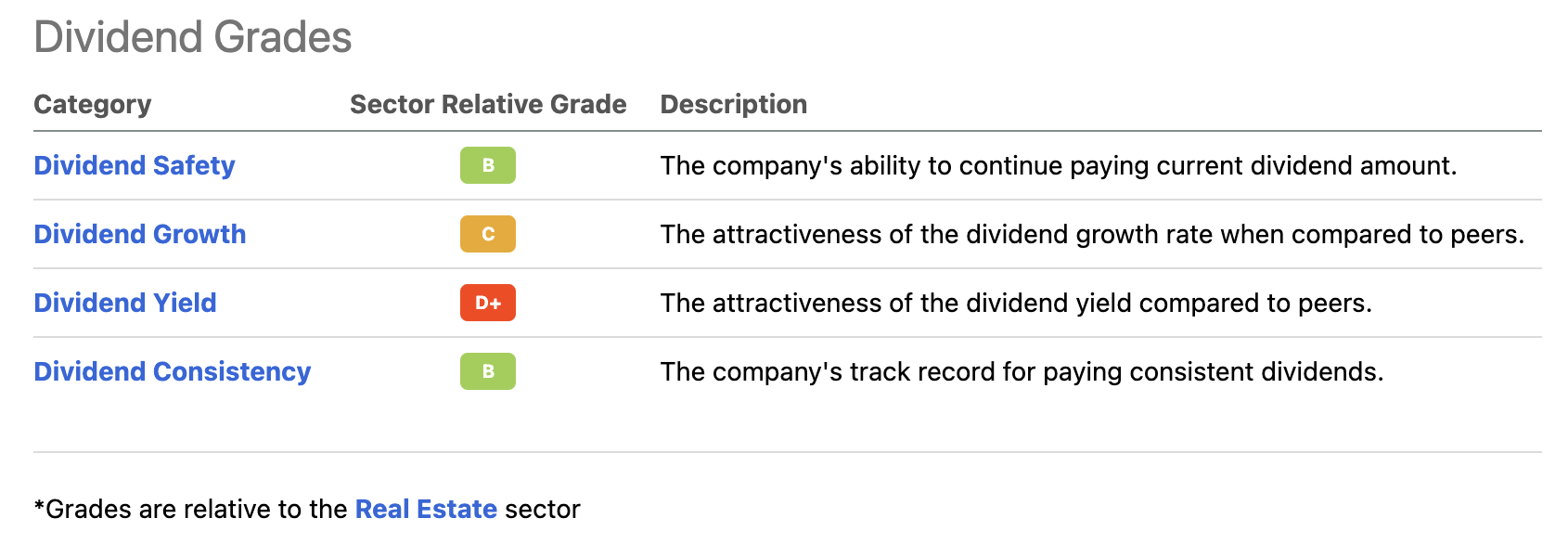

With that said, the company’s Seeking Alpha dividend scorecard is a mess. The company scores low on everything.

Seeking Alpha

However, it’s less bad than one might think. The 10-year average dividend growth rate is 20.0%. The payout ratio is just 5.6%. That’s actually very good.

The most recent dividend hike was announced on Nov. 9, when the company hiked by 11.1%. These are the most recent hikes prior to that:

November 2021: +12.5%

November 2020: +14.3%

November 2019: +16.7%

I think D.R. Horton is a good wild card. If the housing bear case does unfold as expected, I think we might be able to pick up some shares below $60. If the Fed is indeed forced to pivot, I wouldn’t bet against prices lower than that.

AvalonBay is featured in this article for a number of reasons. One of them is that I finally have a good reason to cover a stock I’ve never discussed before.

Generally speaking, AvalonBay is a bit of a boring stock (that’s a compliment in a lot of cases). With a market cap of more than $20 billion, AVB is one of the world’s largest owners of residential real estate.

FINIVZ

Prior to the current sell-off, the stock was a somewhat low-yielding REIT with a boring and underwhelming stock price performance.

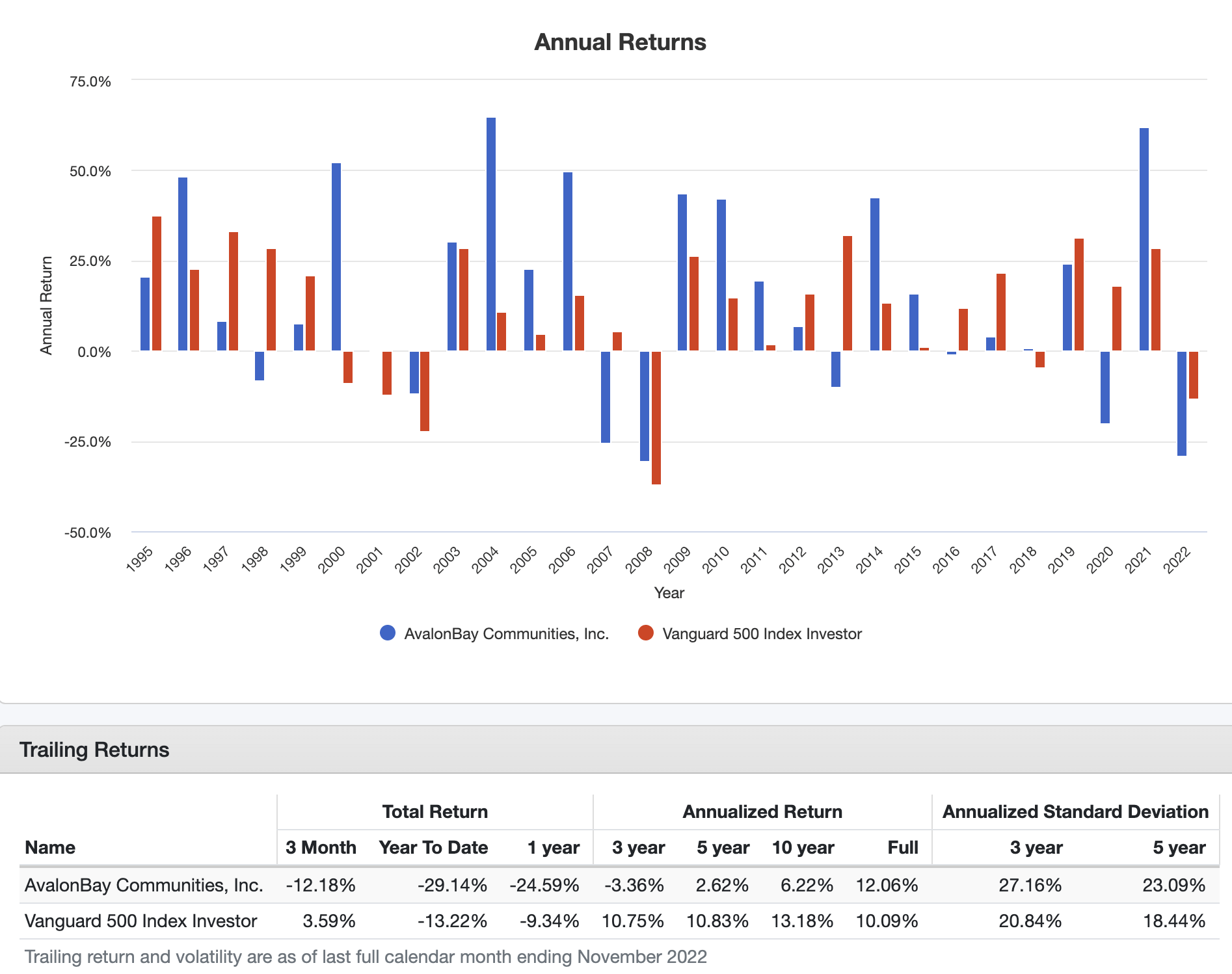

Using the data below, we see that the company has returned 12.1% per year since 1995. That beats the S&P 500 by 200 basis points. Moreover, the standard deviation is subdued. Unfortunately, in the past three, five, and 10 years, the stock had underwhelming returns, which is why I didn’t bother covering AVB. I was (and still am) focused on self-storage, manufactured housing, and fast-growing industrial real estate.

Portfolio Visualizer

However, things have changed. AVB is getting attractive.

AvalonBay is a REIT, which focuses on the development and acquisition of multi-family apartment communities in New England, New York/New Jersey, the Mid-Atlantic, the Pacific Northwest, and Northern and Southern California, as well as Raleigh-Durham and Charlotte, North Carolina, Southeast Florida, Dallas, Austin, and Denver.

Going into this year, the company owned 278 communities, covering 81,800 homes in 12 states and the District of Columbia.

Seeking Alpha

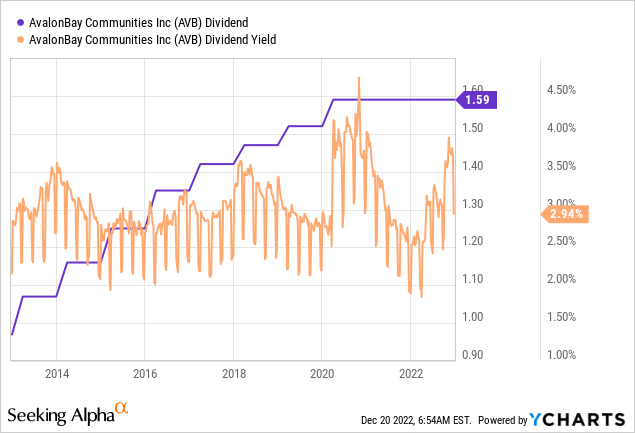

The reason why I put AVB on my watchlist is the fact that higher rates are pressuring the stock price. The company is now yielding close to 4.0%.

The 10-year average dividend growth rate is 5.3%. The five-year average is 2.5%.

The most recent hike was announced in February 2020 when the company hiked by 4.6%.

The adjusted FFO payout ratio is 72%, which is in line with the sector median.

Please note that the company did NOT cut its dividend during the Great Financial Crisis. The company has a stellar balance sheet, an occupancy rate in the high 90% range, and a very anti-cyclical business model – at least when it comes to its cash flow from rents.

The company has a net debt ratio of 4.6x, its average weighted time to maturity is 8.1 years, and the company has $1.9 billion in excess liquidity.

Not only does the company has no major debt maturities over the next few years, but $7.2 billion of its $8.1 billion gross debt load has fixed rates.

This protects the company against high rates for years to come.

It does not mean that AVB won’t sell off along with the market (even below current levels). However, it means that I’m looking to buy some close to $140 for either my own portfolio or portfolios from family members that I advise.

It’s a great stock for income and safety.

Now, onto number three.

3. The Home Depot (HD) – Consumer Retail – 2.4% Yield

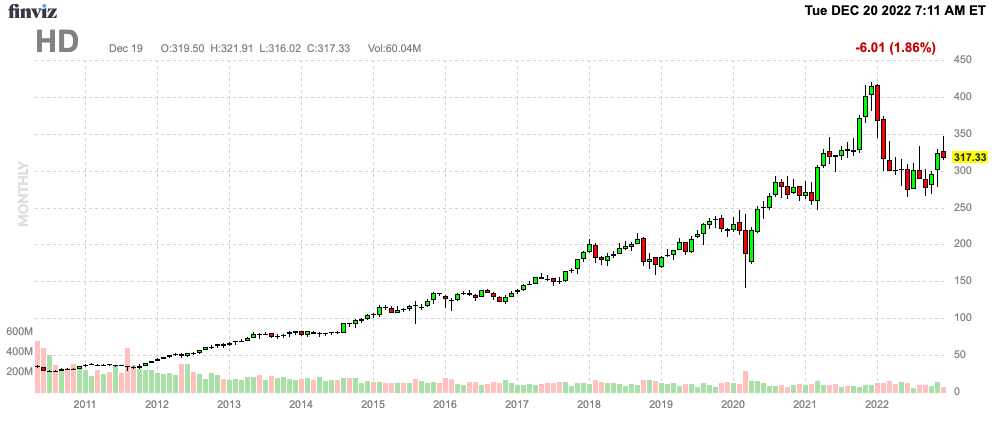

I have covered Home Depot a few times in 2022, but I had to include it again. Home Depot is a stock I have aggressively added to at the 2022 lows this summer.

FINVIZ

The reason I’m watching HD as a hawk is because it has everything I’m looking for in a dividend stock. It’s also tied to the housing market, which could (likely) provide more weakness in 2023. After all, HD does well when consumers are working on projects at home or when pro customers buy supplies for major projects.

This is what the comparison between the HD stock price and building permits looks like:

TradingView (Building Permits vs. Home Depot)

Now, buying HD on weakness is a solid strategy for many reasons. One of them is its ability to create value through consumer products.

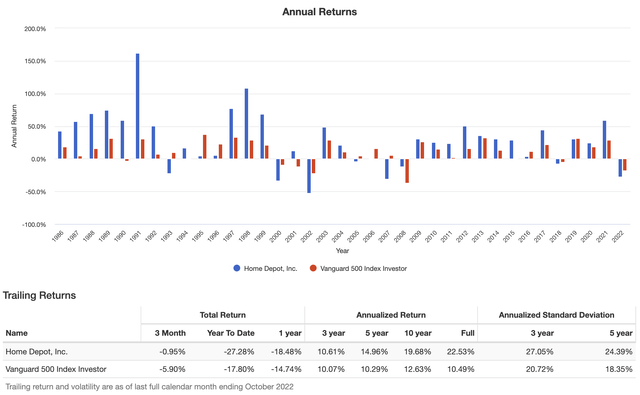

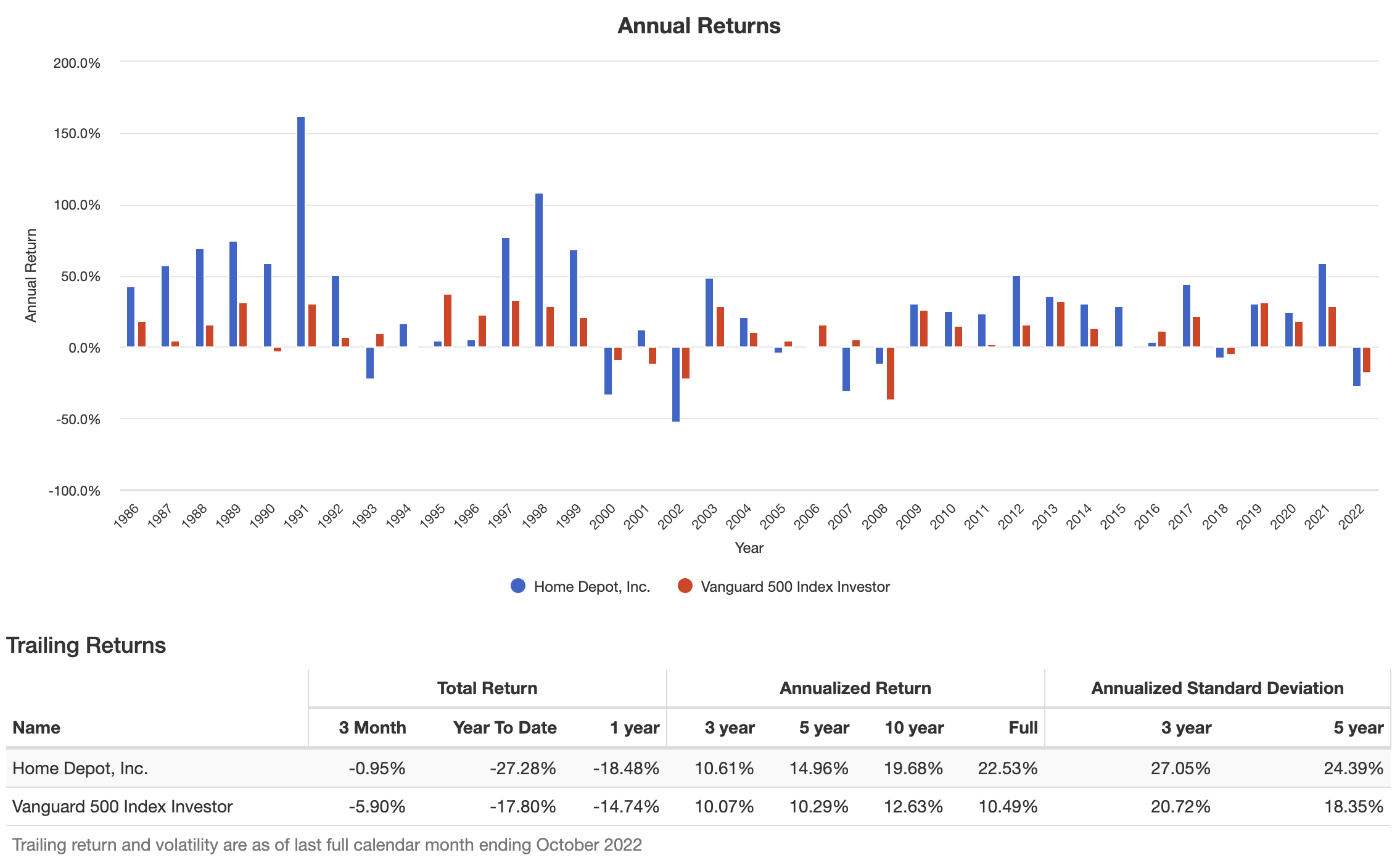

Home Depot is a superstar when it comes to generating shareholder value. The company has returned 22.5% per year since 1986. However, that’s not the main takeaway. The company has consistently outperformed the S&P 500, as the chart below shows. Over the past five years, the stock has still returned 15.0% per year, beating the S&P 500 by almost 500 basis points. Even better, all of this happened with subdued volatility. The standard deviation is just 600 basis points higher compared to the S&P 500. That’s a stellar number, given that the S&P 500 is a huge diversified basket of stocks.

Portfolio Visualizer

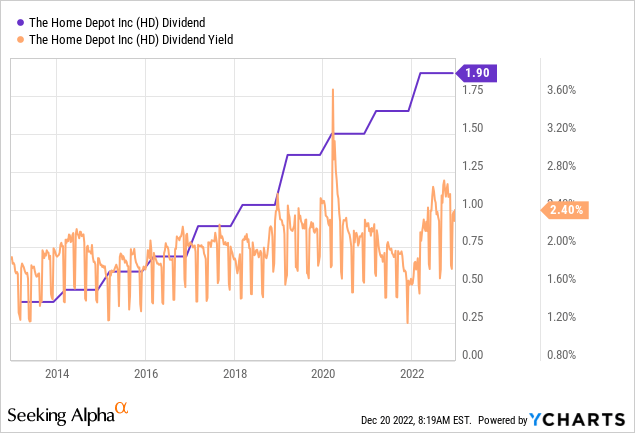

Currently, the stock pays a $1.9 dividend per quarter. This translates to a 2.4% yield.

One might argue that this is not a lot. 2.4% is not a high yield. However, the company has a lot of dividend growth power – especially in times of housing strength.

Over the past ten years, the average annual dividend growth rate was 20.2%, which is a stunning number. Over the past five years, that number is still 17.0%.

In 2023, I’m looking to buy much more HD exposure as close to $250 as possible as I need this high-quality combination of a decent yield and high (potential) dividend growth.

Takeaway

In this article, we discussed my housing outlook for 2023. I expect that we’ll see a situation where housing demand won’t rebound until inflation is elevated. In such a scenario, we are more than likely dealing with a worse-than-average recession, which will likely trigger the Fed to pivot.

Hence, I presented three dividend (growth) ideas that I am watching like a hawk. D.R. Horton is a homebuilder wild card, which could present tremendous value “if” panic selling hits the market. AvalonBay is different. This REIT has a healthy balance sheet, a strong stream of rental income, a high yield, and a very low probability of dividend cuts.

Home Depot has a decent yield, high expected dividend growth, and a business that offers tremendous outperformance in housing bull markets.

Needless to say, there’s a lot of uncertainty. I might be wrong when it comes to housing (I hope I’m wrong for the sake of the economy). However, my downside risk is limited. If I’m wrong, the biggest downside is that I do not buy a lot more quality housing exposure going into the next bull market.

However, given my view, I’m willing to take that risk.

Do you agree with my assessment? Feel free to share your opinion in the comment section. The same goes for the stock selection. Am I missing something? What are you buying?

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment