AnnaStills/iStock via Getty Images

Investment Thesis

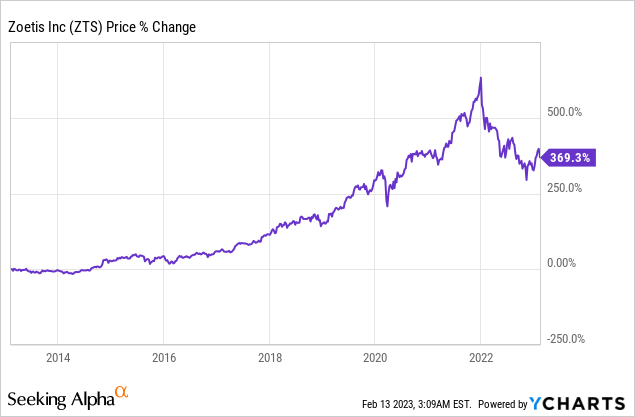

Zoetis (NYSE:ZTS) has been a wonderful compounder in the past decade, with shares up over 360% during the period, comfortably outpacing the broader indexes. Due to rising rates and inflation headwinds, its share price has pulled back significantly and is now trading 35% below its all-time high.

Zoetis has strong fundamentals and the animal healthcare market is also huge and continuing to grow. This should set up the company for long-term durable growth rates. However, despite the pullback, the current valuation is still elevated. Its Q4 earnings results are solid but not enough to support the valuation in my opinion. I don’t see much upside potential from the current price levels therefore I rate ZTS stock as a hold and will wait for a better entry point.

Strong Fundamentals

Zoetis is a US-based animal healthcare company. The company was spun off from Pfizer (PFE) back in 2013 and later went public. It provides medicines, vaccines, diagnostic, and technology products for livestock and companion animals. The company is currently the global market leader for animal health with over 300 product lines across 8 species. It has a strong moat as most of its products are patented with a 30-year average market life for key brands. It also has multiple manufacturing sites across the globe from Norway to New Zealand, which provides reliable supply channels and strong operation efficiencies.

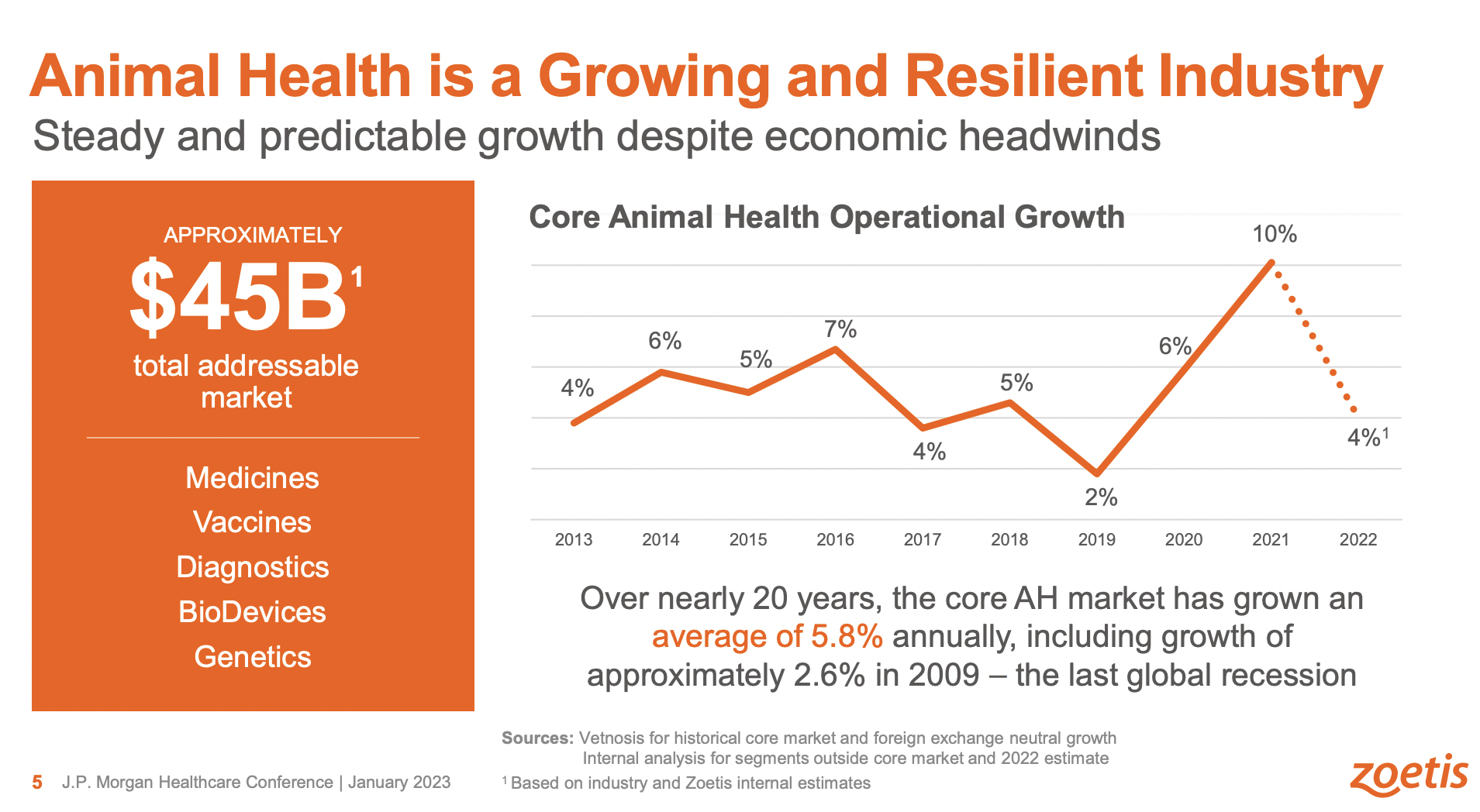

The TAM (total addressable market) for animal health is huge and continues to grow steadily. According to Grand View Research, the TAM is forecasted to grow from $43.3 billion in 2022 to $92.8 billion in 2030, representing a solid CAGR (compounded annual growth rate) of 10%. The market is also very resilient as it managed to grow by 2.3% in 2009 despite facing a severe recession. Zoetis currently estimates its TAM to be approximately $45 billion.

For the livestock segment, the growth is driven by increasing demand for animal protein (e.g. fish and milk) as the global population continues to grow. The animal protein market is expected to grow at a CAGR of 5.7% from 2021 to 2030. Meanwhile, the companion animal segment is benefiting from an increasing number of pets. According to Idexx Laboratories, the US pet population increased by 5% in 2020 and 2021 compared to 1% from 2010 to 2019. The acceleration should continue as Gen-Z and millennials are driving pet ownership.

Zoetis

Q4 Earnings

Zoetis just reported its fourth-quarter earnings and the results are solid, especially the bottom line which reported double digits growth. The company reported revenue of $2.04 billion, up 4% YoY (year over year) compared to $1.97 billion. The growth is mostly driven by companion animals as demand for small animal parasiticides remains strong. Revenue for the segment increased 10% YoY from $1.18 billion to $1.3 billion. The growth is offset by the decline in livestock revenue which dropped 7% YoY from $760 million to $710 million. Due to inflationary pressure, costs of sales increased by 9% YoY to $653 million and gross profit was flat. The gross margins dipped 150 basis points from 69.5% to 68%.

The bottom line was impressive as the company managed to slash its expenses. Operating expenses were $662 million compared to $731 million, down 10.4% YoY. SG&A (selling, general and administrative) expenses decreased by 13% from $593 million to $514 million as the company reduced marketing efforts. This is partially offset by R&D (research and development) expenses which increased by 7% from $138 million. to $148 million. This resulted in operating income increasing from $596 million to $690 million, up 15.8% YoY. The operating margin widened significantly from 30.3% to 33.8%.EPS was $0.99 compared to $0.87, representing an increase of 14% YoY. The company also initiated upbeat guidance for FY23 with revenue growth of 6% to 8% and net income growth of 7% to 9%.

Overall, the quarter was solid. Top-line growth was soft but this is much expected as the economy weakened. Through disciplined cost-cutting, expenses dropped substantially which resulted in operating income growing by double digits. The guidance was also decent as it indicates a rebound in revenue growth, although net income growth does look a bit conservative. On a side note, Zoetis recently raised its quarterly dividend by 15.4% from $0.325 to $0.375 and the fwd yield is now 0.95%. While the yield is still low, the dividend has been growing at a CAGR of 25.1% in the past 5 years.

Investors Takeaway

Zoetis is a great company with strong fundamentals. The company has broad patented product lines with a long market lifespan. It also operates in a large, expanding, and resilient market that should drive durable growth in the long run. However, valuation is a big problem. Even after the pullback, the company is still currently trading at a PE ratio of 39.37x, which is quite expensive. This is meaningfully above large-cap healthcare peers such as Thermo Fisher (TMO) and Danaher (DHR) which are trading at a PE ratio of 32.3x and 26.6x respectively. The latest earnings result is decent but a low double-digit EPS growth is not enough to support such elevated valuation in my opinion. On a historical basis, the current multiple also seems fully valued as its 5-year average PE ratio was 41.99. The company is priced to perfection and I just don’t see much upside potential. Therefore I rate the company as a hold.

Be the first to comment