SHansche/iStock via Getty Images

Co-produced with Hidden Opportunities.

Traditional retirement planning requires you to work hard, save diligently, and live off your savings. How much do you need to save to retire comfortably? It is a simple question, but the answer is complicated, and you will always hear, “it depends,” and there will be several follow-up questions including but not limited to:

-

At what age do you plan to retire?

-

Where do you plan to live after your retirement?

-

When will you claim Social Security?

-

Will your spouse be working?

-

Do you plan to work part-time?

Almost every strategy will involve the steady depletion of your savings, with inflation and life expectancy being a constant worry factor, not to mention bear markets that shave off a significant chunk of your hard-earned capital. But my biggest complaint with this approach is that life is never as fixed as that.

We all make modifications based on changes in our personal life – you may want to stay closer to your children, you may want to retire early to help raise your grandkids, or you may be facing unexpected home repair expenses a few years into your retirement. Your retirement strategy must handle the unknown and the unplanned without compromising your quality of life. Most importantly, your strategy must not come at the expense of your mental health and well-being.

I believe in the income method of investing, where my savings are invested in a large basket of securities, and I live off the dividends. It doesn’t matter if you want to retire in your 60s, 50s, or 40s – this technique will ensure your income keeps flowing in to support your needs. Two picks with up to 11% yields to get your passive income started.

Pick #1: UTG – Yield 8%

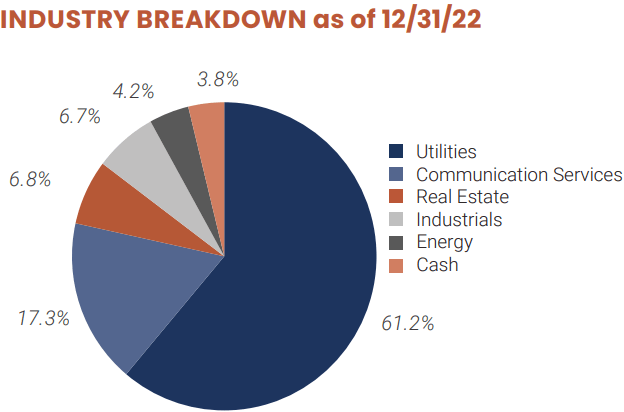

Reaves Utility Income Fund (UTG) is a Closed-End Fund (‘CEF’) that primarily invests in utilities and communication infrastructure. Source

UTG Fact Card

These are conservative sectors that tend to have large established businesses that enjoy deep moats and very high barriers of entry for any potential competition. These businesses have very “inelastic” demand meaning that the demand for their products does not vary significantly with economic conditions. You need electricity and communication, and these will be priorities for your budget.

On the other hand, these businesses tend to deal with more government regulation than other sectors. This is a benefit in that it limits competition, but it can also be a challenge if regulators and companies don’t see eye to eye. For example, with inflation, many utility companies have found themselves in conflict with regulators in determining a fair amount to increase prices.

As a result, over the past couple of years, utilities have seen their expenses go up immediately with inflation, while the red tape required to get a corresponding price increase takes time. Expenses go up, but revenue doesn’t go up right away. This will change as utilities go through the process of demonstrating that a price increase is necessary and getting the approvals.

With the prospect of a recession on the horizon, we want to make sure we have a healthy allocation to investments that will provide us with a healthy cash flow in any environment.

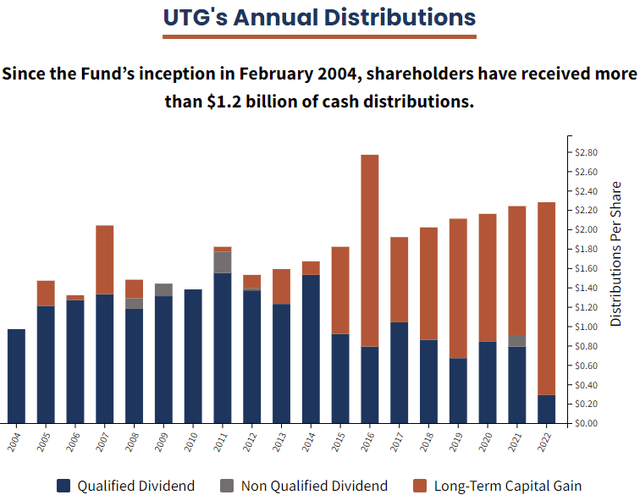

Since 2004, UTG has provided shareholders with generous distributions that have generally grown over time, along with a few years where there were sizable special distributions. Source

UTG Fact Card

UTG’s regular monthly distribution has climbed from $0.0967/month to $0.19/month, while special distributions have added some year-to-year variability.

We expect utilities to benefit as price hikes are passed along to consumers. If there is a recession, which is looking increasingly likely, then utilities are a great stable investment for income investors to hold. UTG is a fantastic way to gain exposure to this sector from a manager with an excellent track record of providing growing income.

Pick #2: PTY – Yield 11.2%

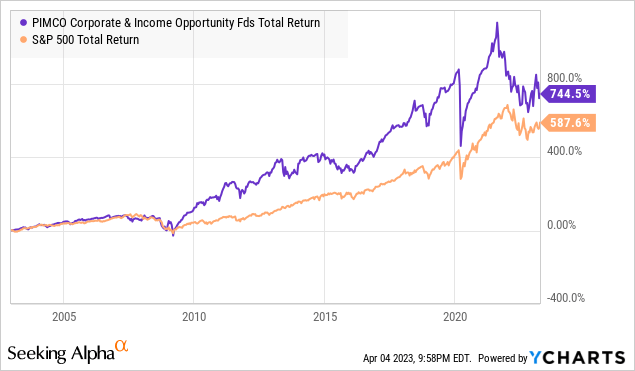

It is no secret that I am a big fan of PIMCO funds, and PIMCO Corporate & Income Opportunity Fund (PTY) is the “OG.” For over 20 years, PTY has been providing investors with exposure to the bond markets, and its track record is nothing short of amazing.

As a bond fund, PTY has managed to produce higher total returns than the S&P 500!

Remember, this was during 20 years when equities had very good returns. How does PIMCO do it? Is it magic? Are they doing something funny? Are they taking on too much risk?

I’ve been investing in PTY for decades, and it amuses me how much angst many have over it. PTY has gone through periods of declining interest rates, periods of rising interest rates, a financial crisis, COVID, and now the worst year for bonds in the history of bonds.

Has PTY beaten the market every single year? Absolutely not. In fact, PTY has underperformed the market in 2020, 2021, and 2022. When others point at that and exclaim, “See, PTY is a BAD investment!” I chuckle and buy more. This kind of short-term thinking causes many investors to chase their tails. They are constantly jumping from the frying pan and into the fire, trying to predict the future. I just keep adding while it is cheap.

At one point, PTY was down 36% from its peak, the largest drawdown it has seen since the Great Financial Crisis. For that I would just say, thank you for the discount.

You see, it is no secret why PTY was down so much last year. It was down for the same reason that every bond investment in the world was down – interest rates were going higher. In other words, the price that investors were willing to pay for debt investments was lower at the end of 2022 than they were at the beginning, while sellers were also willing to sell at lower prices.

I have a news flash – interest rates aren’t going to go up forever. I can’t say for certain exactly how much they will go up, and neither can anyone else. What I can be confident about is that interest rates will be cut eventually. Those who gamble on such things are betting that rates will start being cut by July. If those gamblers are right, then PTY will see its net asset value start to climb as bond prices go up.

If they are wrong, well, then I’ll just keep buying more PTY while it is cheap. I don’t have to bet on when the Fed will pivot. All I need to know is that the Fed will eventually pivot. Time is on my side because I’m getting paid every month to wait.

But what about the losses?!? By now, you have likely seen the breathless headlines about PIMCO losing $340 million from the “AT1” bonds to Credit Suisse that were written off as part of the UBS acquisition. What is less widely reported is that PIMCO also had approximately $3 billion in senior bonds that went up in price by about 25% after the acquisition.

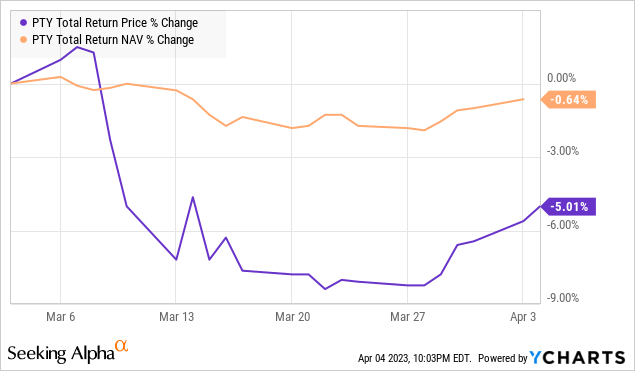

We can see a radical difference in how the market price of PTY responds compared to the change in NAV:

PIMCO updates NAV daily, so the write-off of any Credit Suisse bonds is incorporated in the small 0.56% decline over the past month. PIMCO is highly diversified, and when you see these reports about them losing $X on this investment or that investment, it includes PIMCO’s entire exposure across all of the assets it manages. PIMCO manages somewhere around $1.7 trillion in assets. So $340 million, compared to $1.7 trillion, suddenly isn’t such a scary number.

I’ll be clear, PTY is not a fund that is investing in super-safe bonds. If you are looking for something like that, consider a municipal bond fund like BNY Mellon Municipal Bond Infrastructure Fund (DMB). PIMCO has built its success on the reality that the fear the market has is often greater than the real risk. It is usually stepping in and buying when other bond investors run away in terror. Sometimes, that strategy works to produce huge gains. For example, PIMCO has made huge gains on pre-2009 mortgages that it bought hand over fist during the mortgage crisis. Other times, it results in a total loss, like the Credit Suisse AT1 bonds. Historically, the size and frequency of gains have greatly exceeded the losses.

Evaluating “special situations” is one of PIMCO’s greatest strengths. Being able to determine when a bond that the market is running away from could have a much larger recovery than the market is pricing in is one of the strengths of the PIMCO team.

PTY has had the ability to take advantage of turmoil and uncertainty in the bond market. Following the Great Financial Crisis, PTY paid out oversized special dividends every year from 2009 through 2014.

I’ll let others panic over whether the Fed will pivot in May, June, July or surprise the market and hike all three months. In the meantime, I’ll collect my dividends and let PIMCO do what it does best – turn my capital into dividends!

Conclusion

Dividend investing is not a get-rich-quick scheme but a time-tested method of slowly but surely producing dependable cash flow. Dividends have the power to sustain your cash flow needs for a lifetime.

At HDO, we maintain a portfolio of 45+ opportunistically identified equities with an average yield of +9%. With such a portfolio yield, you can live off dividends and not worry about outliving your savings.

The rising cost of living has retirees cutting back on leisure activities like eating out and modifying their vacation preferences. Your retirement timeline and lifestyle choices can fully be in your control, and dividends are here to meet your cash flow needs and support the flexibility you need. After all, we are human beings, not robots; we have our preferences and are allowed to change our minds. Two picks with up to 11% yields for the retirement you deserve, not the one you are stuck with.

Be the first to comment