tattywelshie/E+ via Getty Images

In this article I will provide a preview of the Employment Situation Report to be released Friday, April 7, 2023, at 8:30AM EST. In connection with this preview, I will provide summary analysis of the current US economic outlook heading into this report. Additionally, potential consequences for US bond and equity markets will be discussed in detail. The article will be organized as follows:

- Summary data for prior month and expectations for current month.

- Review of key forecast factors.

- Significance for US economy.

- Potential implications for US bonds and US equity markets.

- Pre-report technical condition of US equity market.

Summary Preview

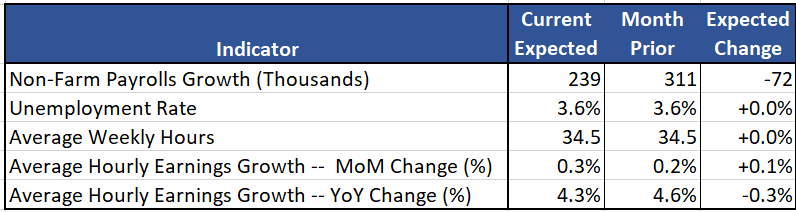

In the table below we highlight the median forecasts of surveyed economists for several important figures to be released in the Employment Situation Report

Figure 1: Summary Preview of Expectations vs Prior Month

Current Expectations vs Prior Month (Investing.com)

According to Investing.com, the median forecast of surveyed economists is expecting a month-on-month – MOM – increase in non-farm payrolls of approximately 239,000. This would represent a significant deceleration in MoM job growth compared to the March figure of 311,00.

The median forecast expects the unemployment rate to remain unchanged at 3.6%.

The median forecast expects weekly hours to remain unchanged at 34.5 hours.

The median forecast expects average hourly earnings to accelerate by 0.1% from a growth rate of 0.2% last month to growth of 0.3% this month. If the median forecast is correct, average hourly earnings will have accelerated from 4.3% to 4.6% on a year-on-year basis.

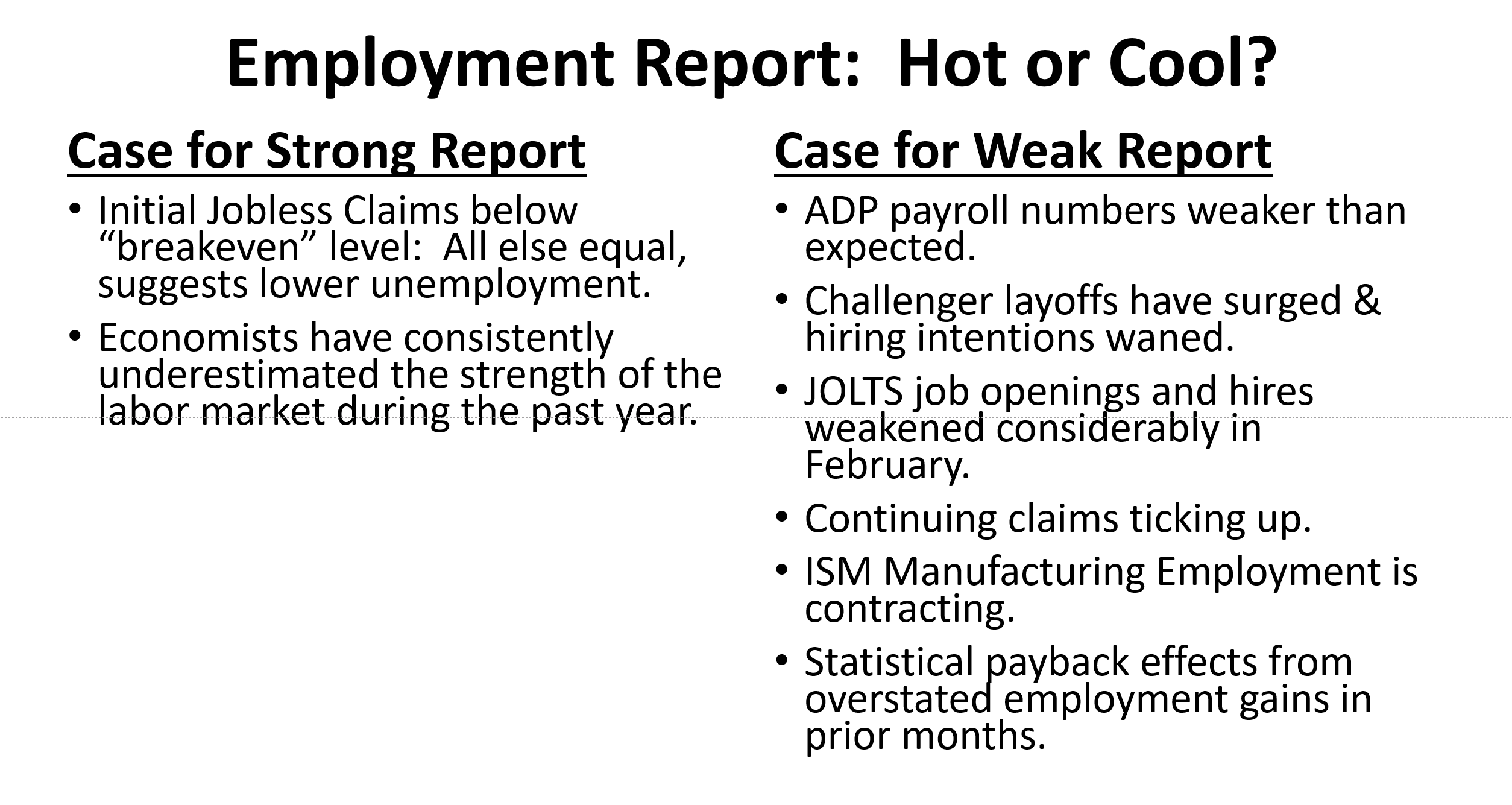

Hot or Cool: A Review of Key Forecast Factors

Will the employment numbers be hot or cool? The following table reviews some key factors that have influenced the forecasts this month, highlighting contrasting arguments supporting both sides of the debate.

Review of Forecast Factors (Investor Acumen)

My own view regarding the likely outcome is neutral. For the BLS itself, the margin of error in their own official estimates is very high and this margin has been rising in recent months. Forecasters trying to estimate the BLS’s figures are not only challenged to estimate the actual numbers, they also must estimate the errors in the BLS’s estimation of the numbers. The BLS reports that revisions are made more than 90% of the time. For example, the estimated margin of error (confidence interval 90%) in its non-farm payroll estimates is roughly 130,000 while the margin of error in the estimate of the unemployment rate is roughly 0.20%. The potential for errors has been compounded in recent months due to the distorting effects that data during COVID pandemic period had on seasonal adjustment factors.

The available evidence clearly does suggest weaker labor market conditions in March compared to February. This already is at least somewhat reflected in the median forecast which anticipates a significant slowing in the growth of non-farm payrolls. However, if forced to take one position or the other (which I am not), my impression is that the median forecast may be anticipating slightly firmer conditions than I think the balance of forecast factors probably warrants.

Significance for the US Economy

The US economy is currently at a crossroads. In the wake of recent turmoil in the US banking sector, there are unmistakable signs that the US economy has been slowing. The extent to which banking sector problems are sufficiently severe to push the US economy into a recession is as of yet uncertain.

There will be no recession in the economy unless payrolls actually contract and unemployment rises significantly. In this regard, it’s important to note that US employment data have consistently been stronger than analysts’ expectations during the past year. The latest Employment Situation Report will be an opportunity to see if this pattern of surprising resiliency continues.

The US Federal Reserve will be watching these numbers carefully as one of the key drivers of their monetary policy is the strength of the US labor market. The Fed has indicated very clearly that the extraordinary strength and tightness of the US labor market that has been exhibited for the past year is, in the long run, incompatible with stable inflation at the Fed’s targeted rate of 2.0%. The Fed, therefore would like to see evidence of a substantial weakening in labor market conditions prior to implementing a “pause” in their increases of the Federal Funds Rate.

In particular, the Fed has forecast a trough-to-peak increase in the US unemployment rate of roughly 1.0% in 2023. So far, virtually none of the softening in the labor market that the Fed has hoped to see has actually occurred thus far.

Unless the numbers in the March report show substantial weakness, the Fed will remain under considerable pressure to continue raising the Federal Funds interest rate.

Implications for US Bonds and US Equities

Ever since the US banking sector turmoil started about one month ago, yields on US government securities have plunged dramatically. This reflects fears of recession as well as increased expectations that the Fed is likely to soon pause its interest rate hikes. Indeed, bond yields imply that the that bond markets are expecting the Fed to cut interest rates later this year.

Expectations and hopes of a Fed “pivot” are likely to be frustrated unless there’s evidence that US labor market conditions have started to soften significantly. In this context, a “hot” employment report could trigger a sell-off in the bond and equity markets. By contrast, an extraordinarily soft labor market report could ramp up recession fears, which would likely cause US bonds to rally. The attitude of the US equity market toward a soft Employment report would be somewhat ambivalent. US equity market participants would welcome a Fed “pause.” However, US equities will likely perform poorly if expectations regarding the probability and/or severity of recession were to surge higher.

There’s a rather marked divergence between recent action in the US bond market and the US equity market. US bonds are signaling significantly increased fear of recession. By contrast, US equities appear to be pricing in a rather idyllic “soft landing” scenario, in which the US economy merely cools off “by the right amount” but does not lapse into a recession. The March employment report could trigger a resolution of this rather extraordinary divergence – in one direction or the other.

Pivotal Moment in Economy Reflected in Technical Conditions

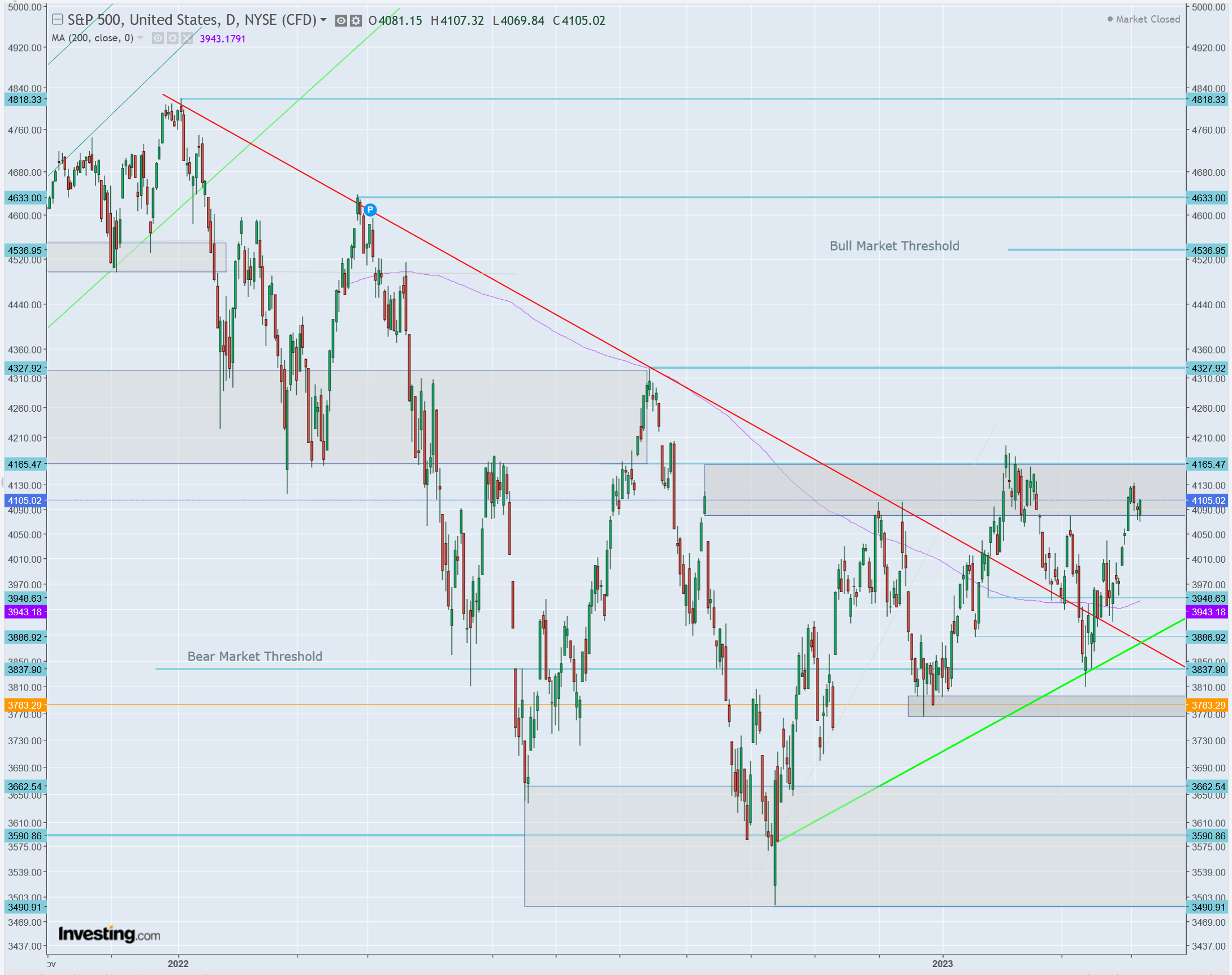

As can be seen in the graph of the S&P 500 index below, the US equity market is literally at a crossroads, represented by the red downward trend line (old bear market) and the green upward trend-line (potential bull market). Furthermore, the S&P 500 is near the 200-day moving average and is at an important resistance level (grey shaded area).

Technical Analysis as of March 6, 2023 (Investor Acumen, Investing.com)

If the S&P falls back down below the bear market down-trend line (red) and breaks down below the up-trend that has been in place since December (green), the technical chart pattern would turn decidedly bearish. However, the S&P 500 has recently held extremely important support levels and has rallied back to an important area of resistance just below 4200.

On a multi-week timeframe, the S&P 500 looks to be in fairly solid shape as the market has rallied off of key supports. The multi-week outlook is currently neutral as the market is between resistance just below 4200 and support just above 3800.

On a multi-month basis, the current uptrend, in place since December 2022 would be broken if the SPX fell below the 3760 level. Indeed, this would set up a potential test of the October 2022 lows. On the other hand, a bull market would be confirmed if SPX managed to rise above the recent high of around 4200 and then above final key resistance at 4330. Unless and until the market breaks above or below the afore-mentioned levels, the technical outlook of the market, on a multi-month basis is relatively neutral.

A very large surprise in the Employment Situation Report would be exactly the sort of catalyst that could cause the market to break out of the aforementioned critical multi-week and multi-month ranges. While I’m not expecting such a major surprise, I do think that it would likely require major fundamental developments such as this to enable the market to break out of these aforementioned ranges.

Conclusion

Fundamentally, the US equity and bond markets are at a potential inflection point. The employment situation report could provide critical evidence regarding the likely path that the US economy is likely to take in the next few months.

From a technical analysis perspective, the US equity market is at a crossroads between resumption of the old bear market trend (January to October 2022) or confirmation of a new bullish trend that has been in place since October 2022. In this regard, Friday’s Employment Situation Report could potentially trigger the unfolding of decisive price action that clarifies the likely direction of the primary trend in the US equity market for most or all of the rest of 2023.

Be the first to comment