segray/iStock Unreleased via Getty Images

Investment Thesis

Starbucks is a leading brand with a wide moat. The company has sufficient ability to pass on cost increases to customers. It is facing some key challenges — COVID-related restrictions in China, unionization efforts, CEO transition — but the company can maneuver past these. It is these challenges that explain the stock’s steeper fall than the market in this year. So, the stock has fallen to attractive levels and, of course, there are reasons for the fall.

I believe that the stock should bounce back once the issues are resolved.

An overview of operations

Starbucks Corporation (NASDAQ:SBUX) is a premier roaster, marketer, and retailer of specialty coffee, operating in 84 markets. Revenue from company-operated stores accounted for 85% and licensed stores accounted for 9% of total net revenues in fiscal 2021. Under licensing arrangement, Starbucks receives a margin on branded products and supplies sold to the licensed store operator along with a royalty on retail sales. Licensees are responsible for operating costs and capital investments.

Starbucks

In North America, Starbucks has more company-operated stores than licensed ones, whereas more of its stores are licensed in international markets. The company expects 75% of the net new stores of fiscal 2022 to be outside the U.S.

Coffee consumption soars in the U.S.

The trends in the coffee consumption in the U.S. are supportive to companies like Starbucks. According to a March 2022 report by National Coffee Association USA, coffee consumption has soared to a two-decade high in the U.S. The report further states that specialty coffee consumption hit a five-year high in March.

Coffee, being an integral part of the morning routine, will see healthy growth in the coming years with more people returning to work and thereby having their coffee outside home at places such as Starbucks.

China presents a huge opportunity

Outside the U.S., China presents a huge opportunity for Starbucks’ growth. According to Statista, the out-of-home coffee consumption value in China is estimated to grow from 49 billion yuan in 2020 to 160 billion yuan in 2024, growing at a CAGR of 34.4%. Starbucks is well poised to benefit from this growth, as China is the company’s second-largest market.

Additionally, in 2021, roasted coffee generated the most revenue, roughly $9.4 billion, in the coffee market in China. According to estimates of the Statista Market Outlook, this is expected to rise to around $13.25 billion in 2025.

Financials

During the period 2017-2021, Starbucks has shown decent growth. Company-operated stores’ revenue increased at a CAGR of 8.7%, whereas licensed store revenue increased at a CAGR of 3.3%. Total revenue grew 6.7% CAGR.

Total operating expenses in this period saw a CAGR growth of 7.1%. Operating income in this period saw a CAGR growth of 4.2%. Net income too witnessed a healthy CAGR growth of 9.8%.

In the second quarter of fiscal 2022, total net revenues increased 14.5%, primarily due to higher revenues from company operated stores. The company-operated stores revenue growth was driven by an increase in average ticket as well as an increase in comparable transactions.

However, inflationary pressure resulted in product and distribution costs as a percentage of total revenue to increase 110 basis points for the quarter. At the same time, store operating expenses as a percent of total net revenue also increased 110 basis points. As a result, operating income for the quarter fell to $948.9 million as against $987.6 million in the comparable quarter last year, showing a decrease of 3.9%.

Talking about the fall, Howard Schultz, Starbucks’ CEO noted that:

“Even so, inflationary pressures have outpaced our price increases, resulting in several points of margin compression in the short term and costing us over 200 basis points in the first half of the fiscal year. In Q2, we were able to absorb the incremental cost while still delivering on our EPS expectations.”

Schultz also noted that “well over $1 billion is loaded on Starbucks Cards waiting to be spent” in the company’s stores. The company will recognize this revenue when the customers redeem it. This highlights customers’ loyalty for Starbucks.

Risks

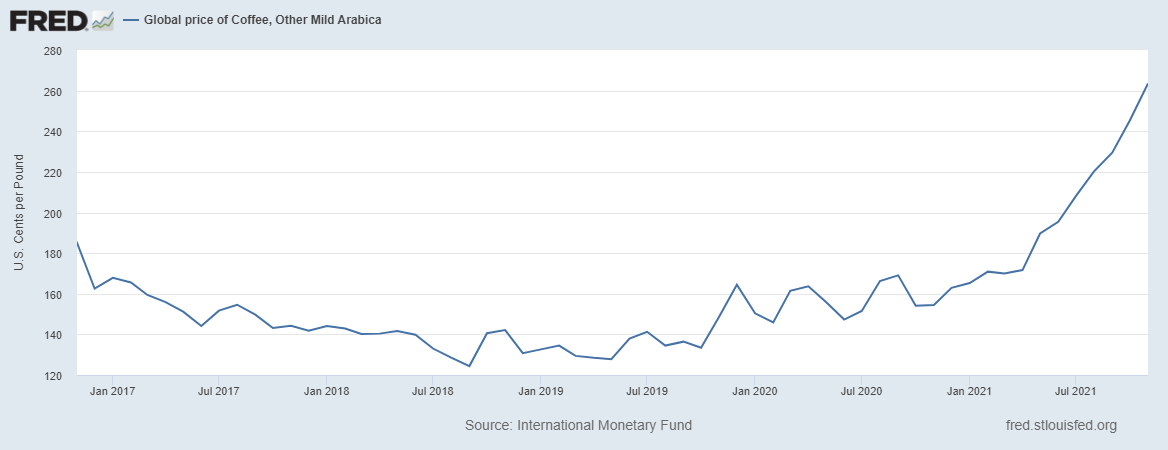

- Increases in the cost of high-quality arabica coffee beans can impact the company’s financials. High quality arabica coffee generally trades at a premium to the “C” coffee price. Global coffee prices have seen a rise in the past 5 years as can be seen from the graph below.

St. Louis Fed

If this trend continues, Starbucks cost of sales will increase, thereby hurting profitability. According to Statista, Arabica coffee was selling for $2.93/ kg in 2018, and is projected to increase in price to $4.28/ kg in 2025.

However, Starbucks management boasts of demand inelasticity for their products. The company has over $1 billion in Starbucks cards, which indicates customers’ commitment to the brand. Over the last year, company faced inflationary pressures and increased the prices several times. Yet, the company experienced negligible customer attrition.

- China is the fastest growing market for Starbucks. It is also the second largest market for the company. Recently, major cities in China experienced new COVID-19 outbreaks. The Chinese government had been imposing restrictions to control the outbreak. Starbucks management stated that it has no ability to predict the company’s performance in China in the back half of the year. Due to the uncertainty in China, accelerating inflation and significant investments the company is planning, management suspended the guidance for Q3 and Q4.

- Starbucks is one of the major companies seeing unionization drive in the U.S. Unionization might result in increased costs for the company. This is because companies often try to discourage unionization efforts by spending more on job benefits.

- It is feared that Schultz has been called back as Starbucks is finding it difficult to find a suitable replacement for Kevin Johnson. How the new CEO performs, once appointed, remains to be seen.

Notably, Schultz had been called back in times of crisis earlier as well, such as in 2008. The current unionization pressures along with COVID situation in China signal difficult times for Starbucks in the short-term. Perhaps this has prompted the management to have Schultz back in the driver’s seat. He has experience in handling employee unrests in the past and he was the one who started the company’s China operations. His appointment should help speedy resolution of some of the company’s pressing issues.

Valuation

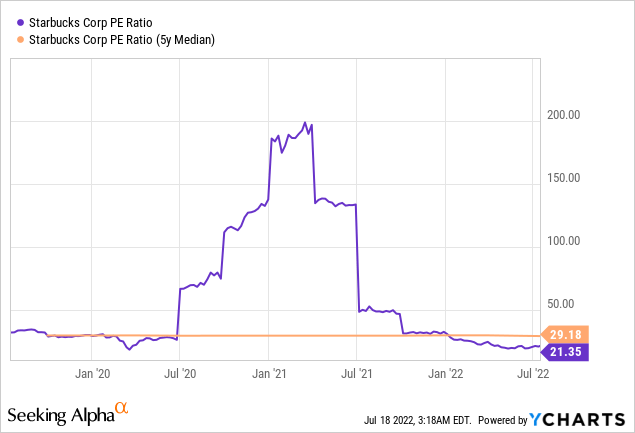

The stock is trading at a discount to its 5-year median P/E ratio. Its current P/E ratio of around 21 looks reasonable.

Seeking Alpha’s proprietary Quant Ratings rate Starbucks as “hold.” The stock is rated low on valuation and earnings revisions and high on profitability.

Conclusion

The Coffee market is poised to grow in the coming years. Starbucks being in the premium category will benefit from the increase in the coffee-drinkers market along with a general rise in per capita disposable income. The stock is trading at a decent valuation compared to its 5-year median.

China, Starbuck’s second largest market, even though under pandemic lockdowns recently, has a strong growth potential in the coming years. Even though the company is facing some issues with the unionization drive at the stores, such issues should not affect the company’s financials and stock performance over the long run, provided the business fundamentals remain strong. Overall, Starbucks stock seems to be a good buy at current price levels.

Be the first to comment