All financial numbers in this article are in Canadian dollars unless mentioned otherwise.

Introduction

The Canadian Pacific Railway (NYSE:CP) is one of my favorite investments in my dividend (growth) portfolio. The dividend yield isn’t high, nor is dividend growth very consistent. However, the company has an incredible business model, allowing it to become the first railroad to combine Canada, the United States, and Mexico. This opens up near- and re-shoring opportunities on top of its major success in intermodal and grains.

In this article, I will explain how I’m dealing with this stock as it’s an exciting long-term play that incorporates macro and geopolitical issues. It’s far less “boring” (boring isn’t bad) than a well-known dividend stock. But it also comes with more volatility and cyclical risks.

Now, let’s look at the details!

A (Reconfigured) Supply Chains Play

I own Canadian Pacific based on a number of reasons. First of all, I believe that Canadian Pacific has a huge moat as I will show you in this article. It’s soon to be the first railroad combining all three North American countries with huge exposure in agriculture and soon intermodal. Second of all, the company is a dividend growth stock, which makes sense in a dividend growth portfolio.

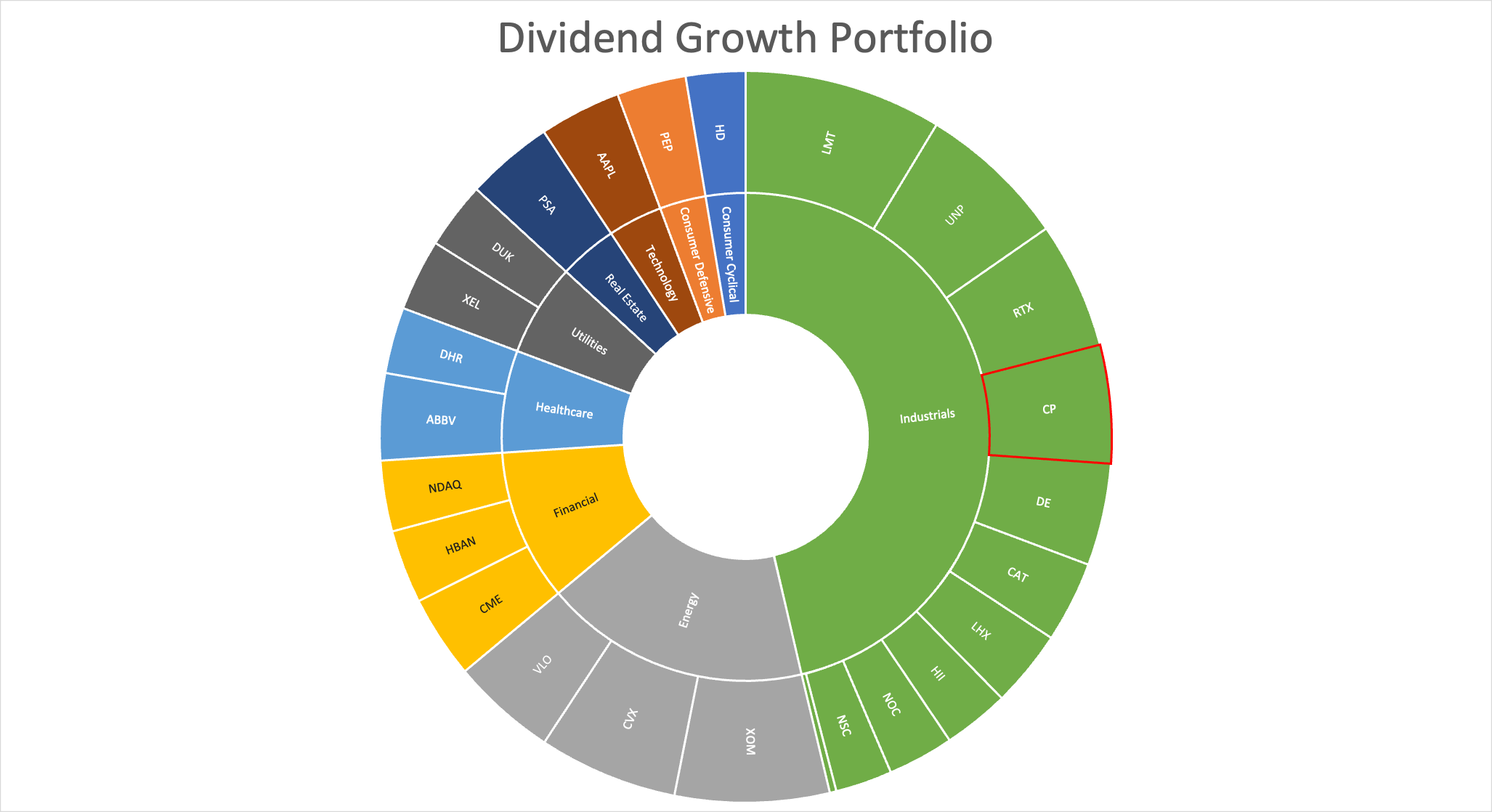

Author Portfolio

The company is now my fourth-largest industrial holding. I bought the biggest chunk in 2021 when the company was in a merger fight, competing with Canadian National (CNI) to buy Kansas City Southern, formerly listed under the “KSU” ticker.

On April 4, I wrote an article titled “Canadian Pacific – My Biggest Supply Chain Bet”.

The merger, which is likely about to be approved in early 2023, connects Canadian Pacific’s rail operations in Canada and parts of the Midwest to KSU’s exposure in the South and Mexico.

From a supply chain point-of-view, it’s a match made in heaven as Canadian Pacific gets to connect its network to Kansas City Southern’s network, creating a network combining Canada, North America, and Mexico. While it does not compete with the big guys in the West and East of the United States, it has access to the US Midwest and all major Mexican industrial, energy, and metropolitan hotspots.

As the overview below shows, the company can ship bulk from Canada straight to Mexico and connect the Mexican automotive industry to customers in North America. In this case without the need for additional companies, which was the case prior to the (pending) merger. This is a cheaper alternative for customers.

Canadian Pacific

Canadian Pacific currently generates 43% of its money in the bulk business. A big part of this is agriculture. In 2020, a quarter of total revenue came from grains. Fertilizers accounted for 11%. Basically, the company’s bulk is grains, fertilizers, and coal.

36% of sales are generated in merchandise segments. 21% of revenue comes from intermodal. After the merger, the new CPKC company will boost total merchandise to 46% while maintaining 36% bulk exposure. The company will remain Canada-focused with 53% of expected CPKC sales coming from the US’ northern neighbor.

I’m extremely excited about the company’s business in grains as I mentioned a few times. The company can combine Canadian, US, and Mexican ports, benefiting from the fact that North America is one of the most important sources of export grains and fertilizers in the world.

Especially because of the war, the focus on US exports is greater than “ever”. Russia and Ukraine export 30% of global wheat exports. Add Ukraine’s exposure to vegetable oils and the fact that the war is ruining exports, and we get a situation that is beneficial for North America.

In a recent Q&A, the company said that it had invested $500 million in new hopper cars, giving the company the most modern and largest fleet in the industry. Moreover, Canada is expanding its export capabilities, adding massive grain elevators. The country has now 43 8,500-foot elevators.

Overall, the company sees a lot of benefits as it can move freight in a shorter amount of time. Especially when it comes to grains and fertilizers. In general, combining all North American countries with a single railroad services customers as it erases the need to use other railroads – not in all cases, but in some.

When it comes to so-called re-shoring or near-shoring, The Guardian reports that the global supply chain crisis is pushing companies to reconfigure supply chains. I’ve highlighted this in multiple articles for the sole reason that Canadian Pacific combines three countries if the STB approves the deal.

Supply chain reconfiguration is both voluntary, as companies have learned their lessons during the pandemic, and forced by governments. As the Guardian writes:

US president Joe Biden said at the opening of the summit of the Americas on Wednesday night that the region had to invest in ensuring that supply chains were more secure and more resilient.

His administration has already legislated for a $250bn fund to boost US manufacture of computer chips, the shortage of which was one of the first visible signs of problems in the wake of the pandemic shutdowns of factories in the far east. Samsung has acted as well by announcing a $17bn chip factory to be built in Texas as the company aims to ease the problem of supplying US customers from its east Asian manufacturing bases.

The hearings in Washington will seek to push the urgency of the situation, especially in relation to the defence industry, and will take evidence from management experts from Harvard, champions of reshoring (AKA bringing manufacturing back to the US or Mexico from Asia) and Biden administration officials such as Deborah Rosenblum tasked with securing the “industrial base”.

With that said, the stock is starting to trade at attractive levels.

The Dividend And Valuation

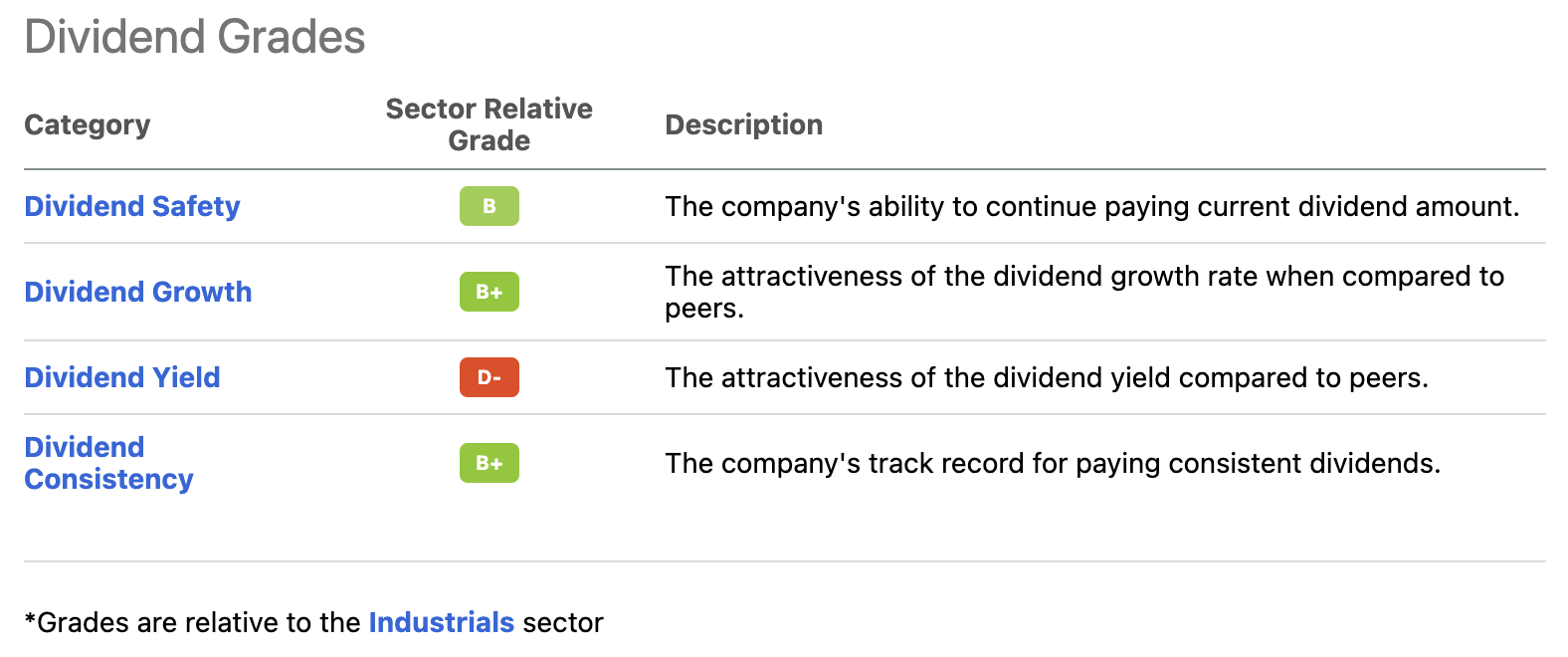

Canadian Pacific has a more than decent dividend scorecard. Provided by Seeking Alpha, these grades show relative scores versus (in this case) industrial peers. The company only scores low on its yield.

Seeking Alpha

Bear in mind that the company’s dividend policy is in Canadian dollars. Currently, the company pays a $0.19 per quarter per share dividend. That’s $0.76 per year or 0.85% of the company’s $90 stock price. I’m using Toronto-listed shares, in this case.

0.85% isn’t worth mentioning to most dividend investors. However, I care about the bigger picture.

In a recent article, I explained that dividend growth stocks (even if the yield is very low) are able to deliver outperforming total returns.

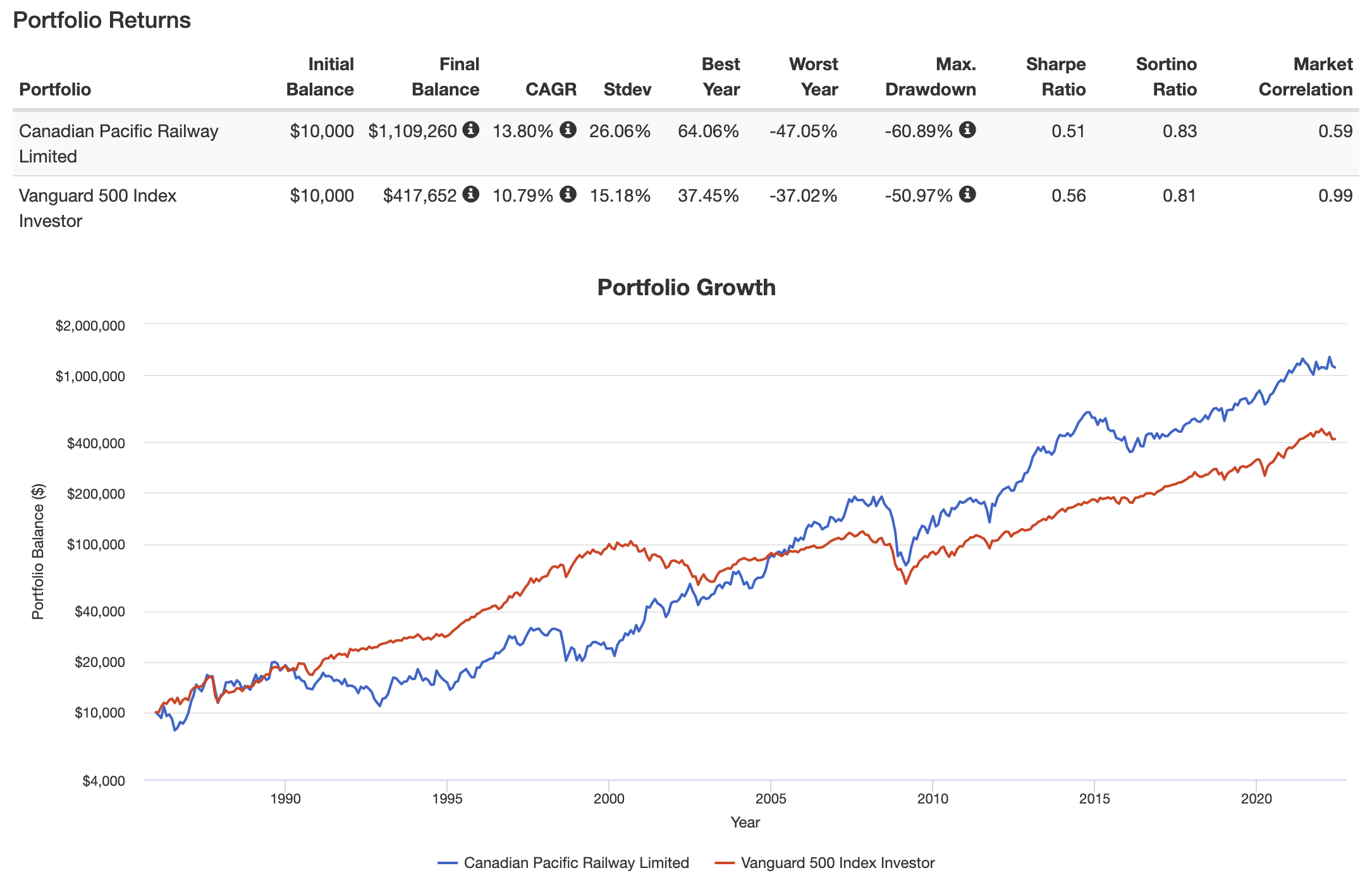

This applies to CP. Its New-York listed shares have added 13.8% per year since 1985. The S&P 500 returned 10.8%, which isn’t bad either. The only issue that some investors see is that the standard deviation of Canadian Pacific is rather high. It’s 26.1% during this period. So please, keep that in mind before trading or investing in CP.

Portfolio Visualizer

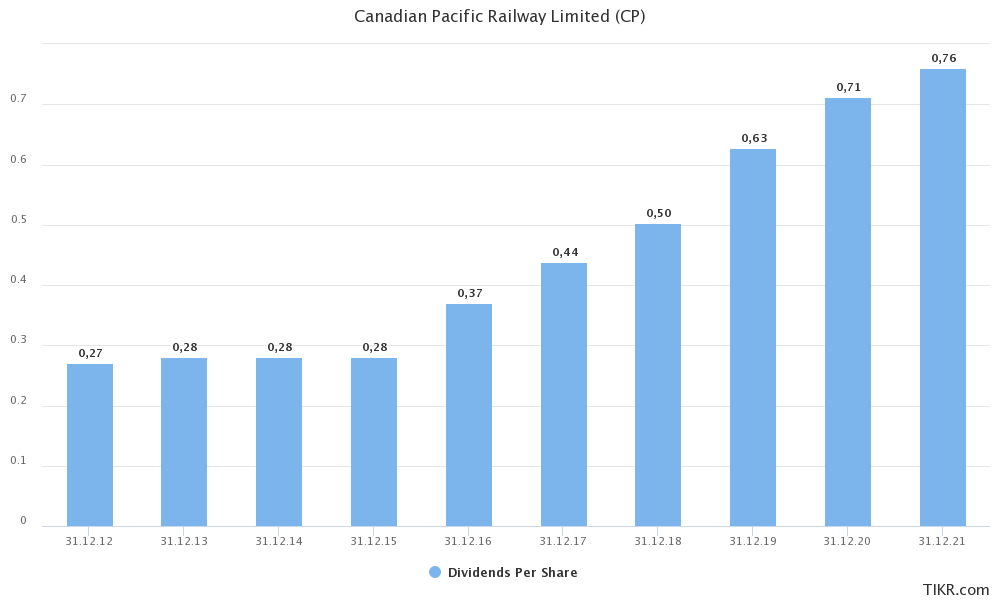

The good news is that dividend growth is high, although somewhat inconsistent on a long-term basis.

These are the most “recent” dividend hikes:

July 2020: 14.5%

May 2019: 27.7%

May 2018: 15.6%

TIKR.com

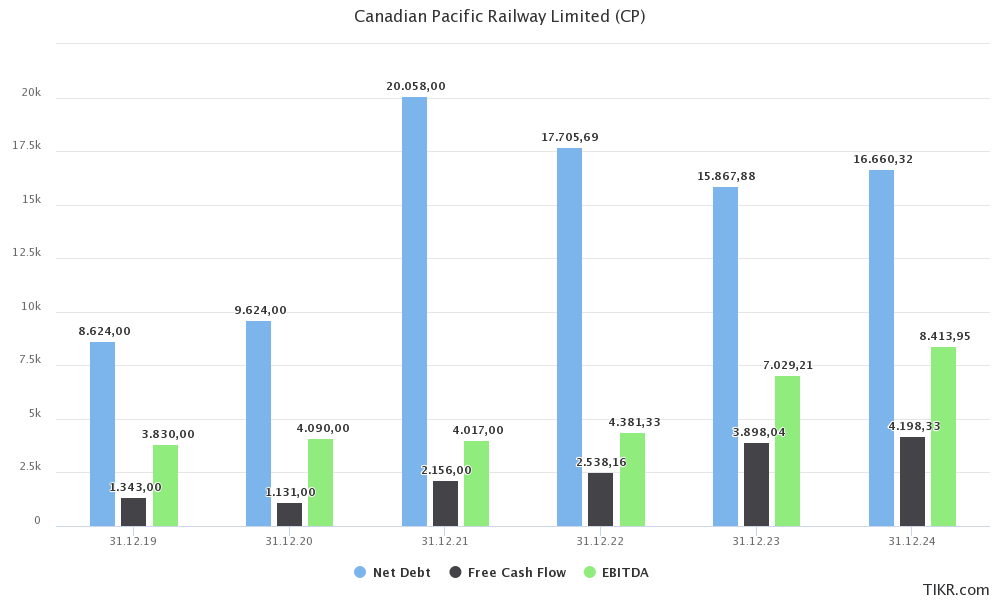

I expect dividend growth to accelerate once the company lowers its post-merger debt again.

Next year, the company’s synergies are expected to pick up, resulting in roughly $3.9 billion in expected free cash flow and more than $7.0 billion in EBITDA. This allows the company to lower net debt to less than $16.0 billion again. That’s roughly 2.3x EBITDA, a healthy number supporting high cash distributions.

TIKR.com

Based on the company’s $82.5 billion market cap, $700 million in pension-related liabilities, and the following estimates:

2023: $7,000 million EBITDA, $15,900 million net debt

2024: $8,400 million EBITDA, $16,700 million net debt

We get EV/EBITDA multiples of 14.2x, and 11.9x, respectively.

Moreover, the implied free cash flow yield in 2024 is expected to reach 5.1% based on the current market cap. Historically speaking, CP has traded at a 3% yield.

Takeaway

Canadian Pacific is a somewhat uncommon dividend stock. Its yield is low, and dividend growth is high, on average, but not as consistent as some of the dividend stocks you may be used to.

However, to me, it’s more than a dividend stock. While I believe that dividend growth will remain very high on a long-term basis, I like the stock because of its transformation. Canadian Pacific is quickly becoming one of the most important transportation companies in North America.

Not only will it dominate agriculture transportation in a world where US exports are more important than “ever”, but it will be one of the biggest beneficiaries of long-term near- and re-shoring.

Global supply chains are shifting, benefiting the US, Mexico, and Canada, thanks to reliable energy supply, and (in some areas) affordable labor.

I expect to hold CP for decades and expect the stock to keep outperforming the S&P 500.

The current valuation isn’t very cheap, but it starts to make sense when incorporating synergies after 2023.

However, if you decide that CP is the right stock for you, please be aware that the stock is rather volatile and cyclical. Moreover, it’s hard to say how far the ongoing stock market downtrend will go.

The best way to play this is by starting a small position. For example, buying 25% now and adding over time allows investors to average down if the market keeps falling. If the stock suddenly takes off, investors have a foot in the door.

This is how I’m dealing with all of my investments at the moment.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment