Veni vidi…shoot/iStock Editorial via Getty Images

Nvidia’s (NASDAQ:NVDA) stock has weathered one of the worst tech storms, declining by more than 55% since the epic tech drop began. While Nvidia’s stock was significantly overbought at around $350 in November 2021, it’s only trading around $150 now. The company’s P/E ratio has come down substantially, and Nvidia is trading below 30 times this year’s consensus EPS estimates. Moreover, Nvidia has substantial growth prospects and tremendous profitability potential.

Nvidia is much more than just a graphics card company. Nvidia makes some of the best GPUs for gaming, digital asset mining, deep learning, and more. Furthermore, the company is helping to change the world with its AI and data science initiatives, businesses that should provide significant revenue and EPS growth in future years. While there may be some more transitory volatility for Nvidia shares in the near term, Nvidia’s stock is relatively inexpensive now, should appreciate considerably in the coming years, and is a strong buy intermediate and longer term.

Nvidia – On Sale Now

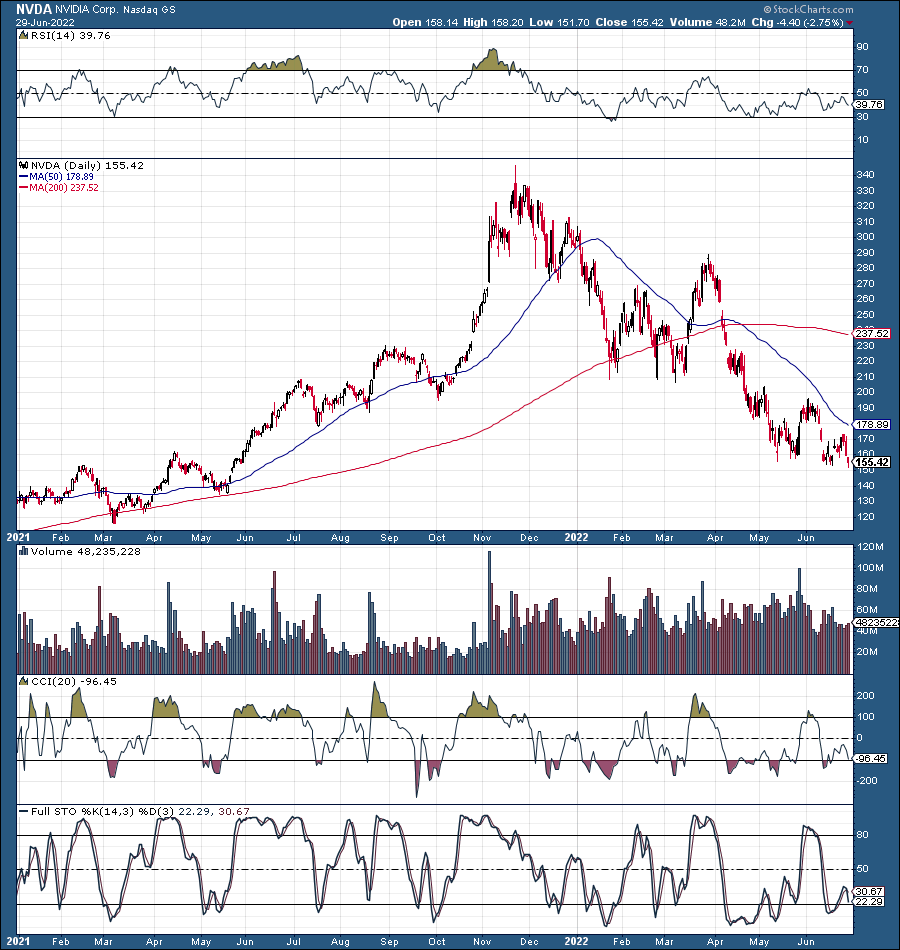

NVDA (StockCharts.com)

Nvidia’s fall has been epic, as its share price declined by approximately 55% from its all-time high. We see Nvidia trading around a 52-week low now, levels not seen since early 2021. I understand that Nvidia is not down to levels from 2020 or earlier, but everything moves quickly in the computer industry, and significantly lower prices may be unrealistic to expect. In fiscal 2020, Nvidia had $10.9 billion in revenues; in fiscal 2022, the company had $26.9 billion. Next year, in fiscal 2024, consensus figures are for around $40 billion in revenues. Also, Nvidia was trading at roughly 75 forward earnings around its highs and is only trading at approximately 23 times forward earnings now (consensus fiscal 2024). Nvidia’s growth is spectacular, and the company has excellent profitability prospects. Therefore, the stock has a high probability of going much higher long-term.

Nvidia Tops The Gaming GPU Market

In 2020, the gaming industry generated $150 billion in revenue, and analysts predict that by 2025 the gaming industry will generate $260 billion in revenue. Three companies dominate the GPU market, Intel (INTC), AMD (AMD), and Nvidia (NVDA). While Intel leads in the integrated graphics market, Nvidia makes the best discrete graphics cards.

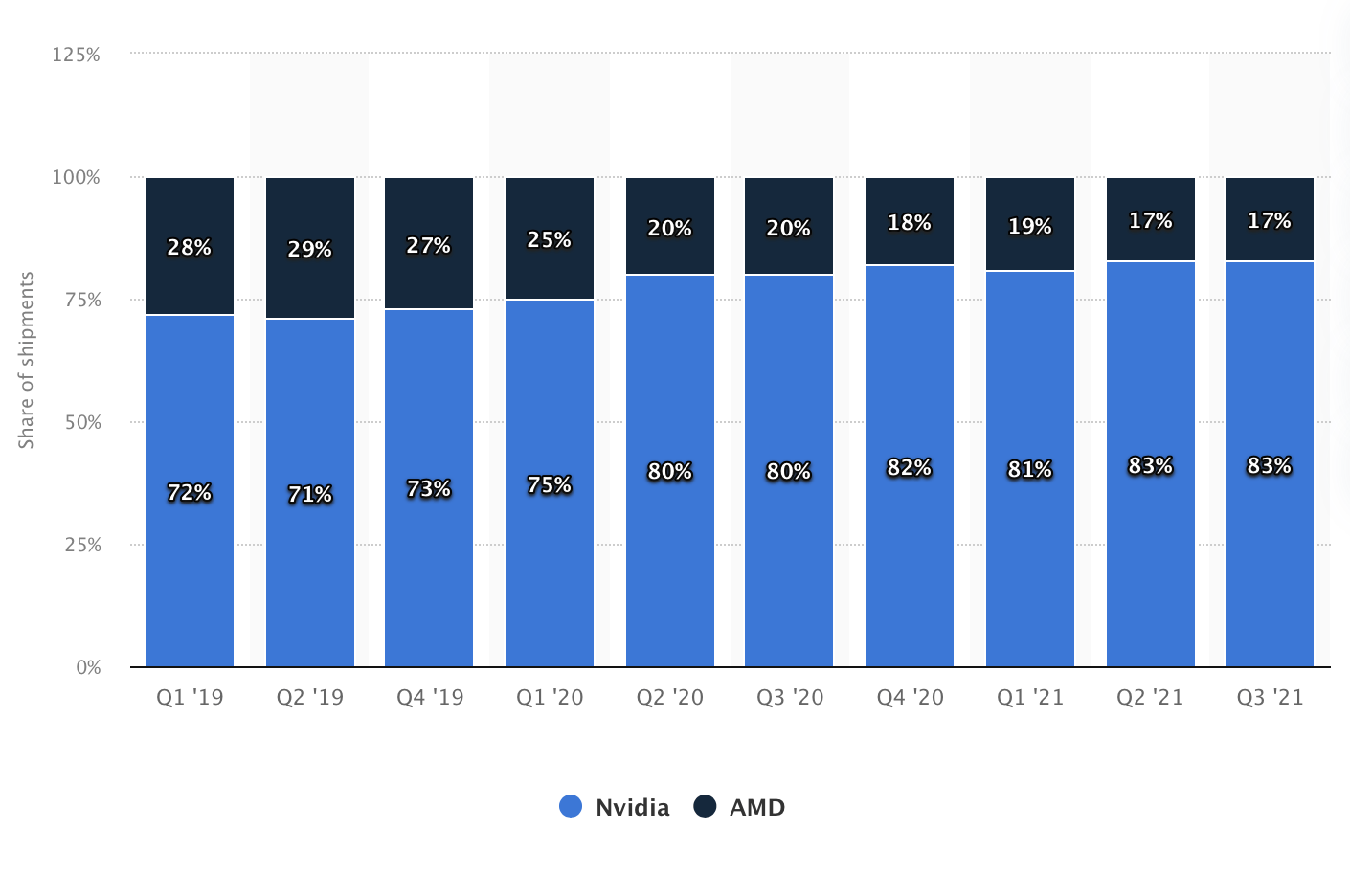

PC Discrete GPU Market

dGPU (Statista.com )

The lucrative PC discrete GPU market is dominated by two companies, Nvidia and AMD. However, we see that Nvidia has the edge in this market and has been gaining share over AMD in recent years. Nvidia’s market share has climbed significantly, from around 72% to 83% over the last three years. Additionally, if we look at the best-rated graphics cards, Nvidia has six out of the top eight, including the number one spot (according to PCGamer.com). Therefore, Nvidia should continue dominating the dGPU market, leading to significant revenues and net income increases as the company advances.

Nvidia Mining Cryptocurrencies

Nvidia’s dedicated GPUs are also used to mine Bitcoin, Ethereum, and other digital currencies. The cryptocurrency industry is another lucrative space where Nvidia has been able to establish a strong foothold in. While the cryptocurrency industry remains volatile and is in a downturn, future bull markets should spark increased demand for Nvidia’s mining-related GPUs and other products. Again, if we look at the best graphic cards for mining, the list is dominated by Nvidia. The top ten GPUs for cryptocurrency mining include seven Nvidia GPUs and three AMD GPUs, with the top spot going to Nvidia’s GeForce RTX 3060 Ti, according to Windowscentral.com.

Nvidia’s Massive AI Potential

Did you know that Nvidia has over 370 partnerships centered around self-driving alone? Nvidia’s goal is to increase the efficiency and safety of self-driving cars through its AI solutions. Therefore, Nvidia is working with major automakers and other participants in the self-driving industry to achieve its objectives. The self-driving market could grow exponentially in the coming years, delivering significant revenues and earnings to Nvidia and other early leaders in this space.

In addition, Nvidia excels in high-performance data analytics, accelerated machine learning, deep learning training, deep learning platforms, conversational AI, and prediction and forecasting. The company also offers a wide range of software supporting its AI-related services. In general, Nvidia is one of the best set-up companies to take advantage of the AI revolution that could be the next massive booming marketplace in the next decade. Therefore, Nvidia is set up exceptionally well to outperform in the future, and its stock should appreciate considerably as the company advances.

Cheap Valuation And A Massive Growth Story Ahead

I was very straightforward about Nvidia being massively overbought last fall, and it was one of the top names I called out continuously around the tech top in November. However, that was when the stock was above $300, and now Nvidia is around $150. The stock price has been sliced in half, yet the company’s prospects are as bright as ever. Therefore, I am pounding the table on Nvidia now, as the stock is cheap relative to the company’s growth prospects. Don’t get me wrong. There is a chance we can move lower in the near term as this bear market progresses. But the downturn won’t last forever, and Nvidia is a strong buy long-term.

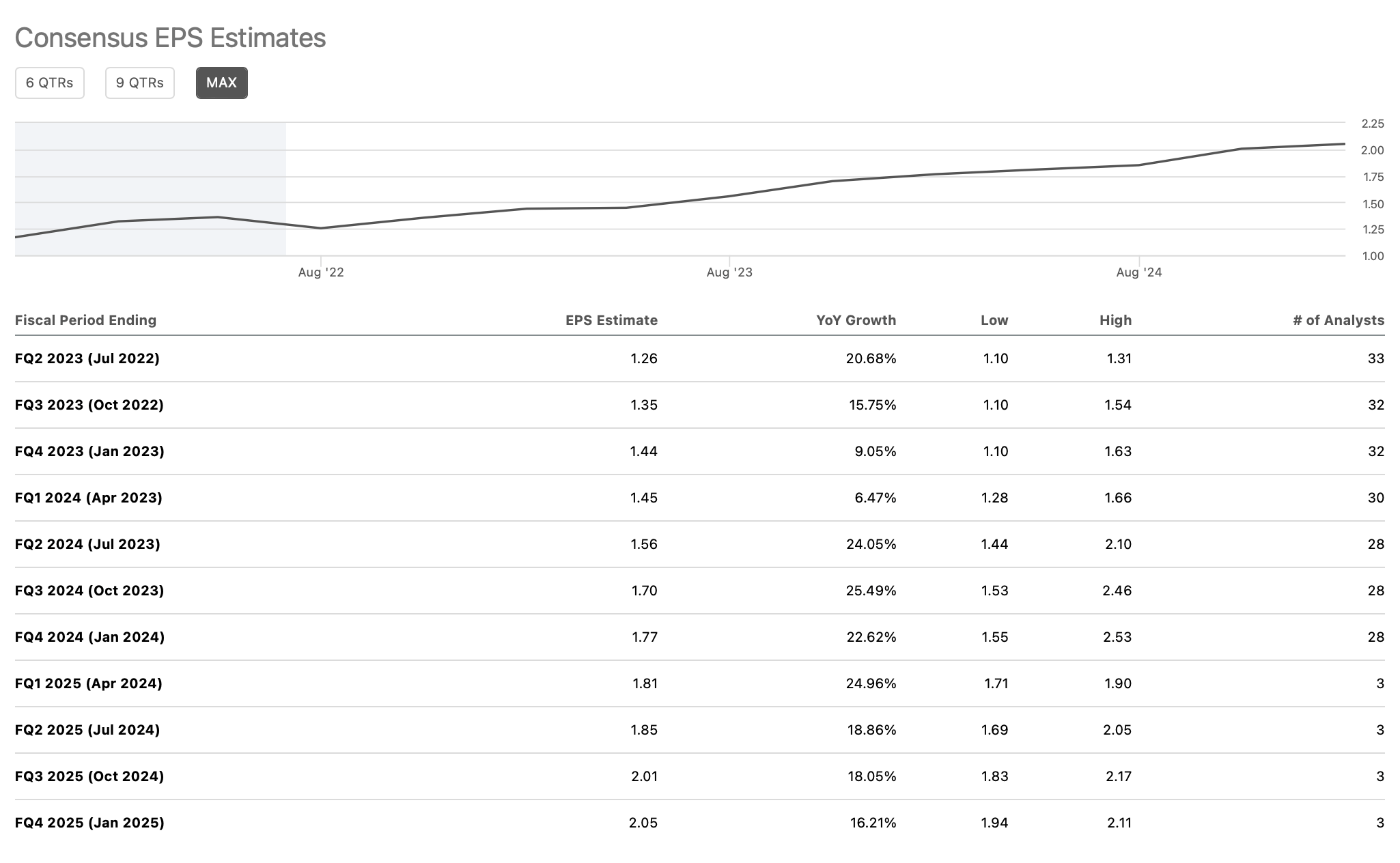

EPS Estimates

EPS estimates (SeekingAlpha.com)

If we look at next year’s (fiscal 2024) EPS estimates, Nvidia should deliver around $6.48 in EPS (consensus estimates). This estimate represents a 20% YoY increase over this year’s $5.41 forecast. However, Nvidia has shown a distinct tenacity for surpassing consensus analysts’ EPS forecasts.

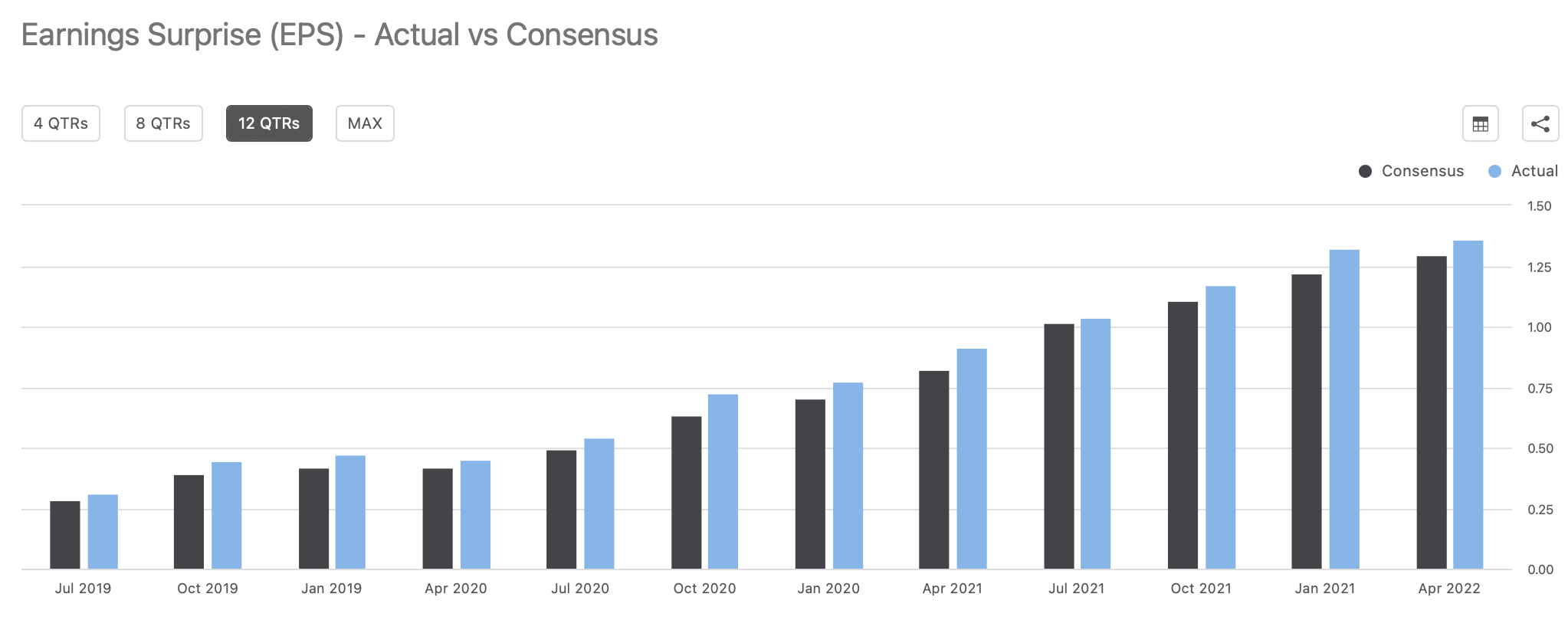

Earnings Surprise

Earnings surprise (SeekingAlpha.com)

Nvidia has surpassed consensus EPS estimates in twelve of the last twelve quarters. The company’s beat rate has recently been around 5-10%. Therefore, we can anticipate the company to continue surpassing estimates by a modest margin. If we apply a 5% beat rate to this year’s EPS forecast, we arrive at around $5.68 in EPS for fiscal 2023, and if we use the same beat percentage for next year’s estimate, we arrive at $6.80 in EPS for fiscal 2024. Now, Nvidia’s stock is only trading at around $150 today, illustrating that the company’s forward P/E ratio is only about 22. When was the last time we saw Nvidia trading at a forward P/E ratio of just 22? Provided the company’s relatively high revenue growth rate (26% this year’s estimate and 18% next year) and bullish setup for future expansion, 22 times forward earnings is a cheap valuation. Therefore, while transitory downside risk exists, anything below $150 should be considered a buying opportunity for Nvidia.

Yes: Nvidia Is A Strong Buy Again

What Nvidia’s financials could look like in future years:

| Year (fiscal) | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 |

| Revenue Bs | $34 | $40 | $47 | $55 | $64 | $74 |

| Revenue growth | 26% | 18% | 17% | 17% | 16% | 16% |

| EPS | $5.68 | $6.80 | $8.10 | $9.55 | $11.28 | $13.50 |

| Forward P/E ratio | 22 | 25 | 27 | 28 | 28 | 29 |

| Price | $150 | $203 | $258 | $316 | $378 | $470 |

Source: The Author

Nvidia’s forward P/E ratio of just 22 seems very low now, and it is not likely that it will remain low for long. Yes, we may see some temporary weakness while the bear market persists, but multiple expansion seems highly likely when conditions normalize. Therefore, we will probably see Nvidia’s forward P/E multiple expand to 25-30 (or higher) in the coming years. Of course, there is a possibility that the multiple could go much higher (40-80), as we saw in the previous cycle, but I’m keeping estimates modest to remain conservative in my estimations. I also think the revenue growth rate is fair, as Nvidia could see a surge in revenues due to increased crypto mining, self-driving, AI initiatives, and other business.

Nevertheless, even with conservative revenue estimates, Nvidia’s EPS should rise notably in the coming years. As we apply our relatively conservative P/E multiples to our EPS calculations, we see a high probability of a significantly higher stock price as we advance. Therefore, Nvidia is a strong buy here with a $300-500 target price range by 2025.

Risks to Nvidia

While I am bullish on Nvidia in the intermediate and longer-term, technically, we are still in a bear market. Therefore, we may see the stock bottom out at a lower level. In a bearish-case scenario, Nvidia may find its base around the $120 level. However, near-term declines should be transitory and not affect my intermediate/long-term price target on the stock. Additionally, Nvidia could face increased competition in the GPU sector and other areas the company operates in.

Moreover, the company could face margin pressure due to higher costs associated with inflation, leading to decreased profitability. Ultimately, the company could deliver less growth and worse EPS than my estimated forecast. Investors should examine these and other risks carefully before committing any capital to an investment in Nvidia shares.

Be the first to comment