Natali_Mis

Over the past two years, the value of the U.S. dollar has generally risen.

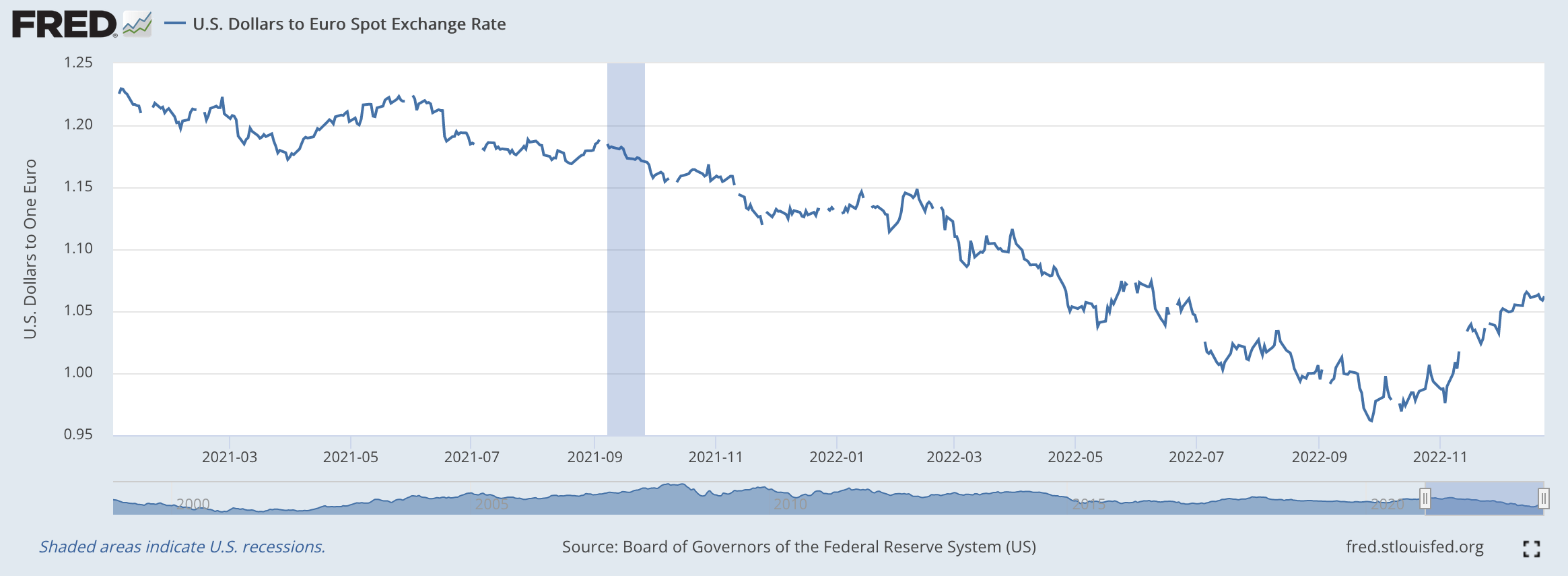

Here is the value of the U.S. dollar in terms of the euro.

On December 30, 2020, it cost $1.2300 to purchase one euro.

On September 27, 2022, the Euro cost only $0.9616.

During this time period, the value of the U.S. dollar rose almost constantly.

What was going on?

Well, the Federal Reserve was always moving its monetary policy in a “tighter” way than were other central banks. It was a relative thing!

During this time period, the U.S. central bank was always coming up on the “tighter” side of where other central banks were moving.

This was true of the Federal Reserve versus the Bank of England, against the European Central Bank, and against the Bank of Canada.

Since this past fall, the dollar price of one euro rose to $1.0621 as these other central banks got more with the “fighting inflation” focus, and again, their actions tended to be “relatively” more stringent than that of the Federal Reserve System.

The movements, in both cases, were all in the same direction, it was just a question of who seemed to be making the “similar” moves.

Between December 30, 2020, and September 27, 2022, the Federal Reserve seemed to be making the more stringent moves. Since September 27, 2022, the others seemed to be making the “relatively” more stringent moves.

As a result, you got charts of all of these currencies relative to the U.S. dollar that were very similar to this one, showing the price of one euro in terms of the U.S. dollar.

Price of Euro in terms of U.S. Dollar (Federal Reserve)

There is no question that in this round of monetary policy the Federal Reserve System started moving before these other central banks started to move, and, in essence, led the other central banks through until the fall months of 2022.

Then the other major central banks began to move in an attempt to catch up somewhat with the Federal Reserve.

The story became one where all the major central banks listed here took up the fight against inflation.

The question now becomes, what happens next?

The Federal Reserve System

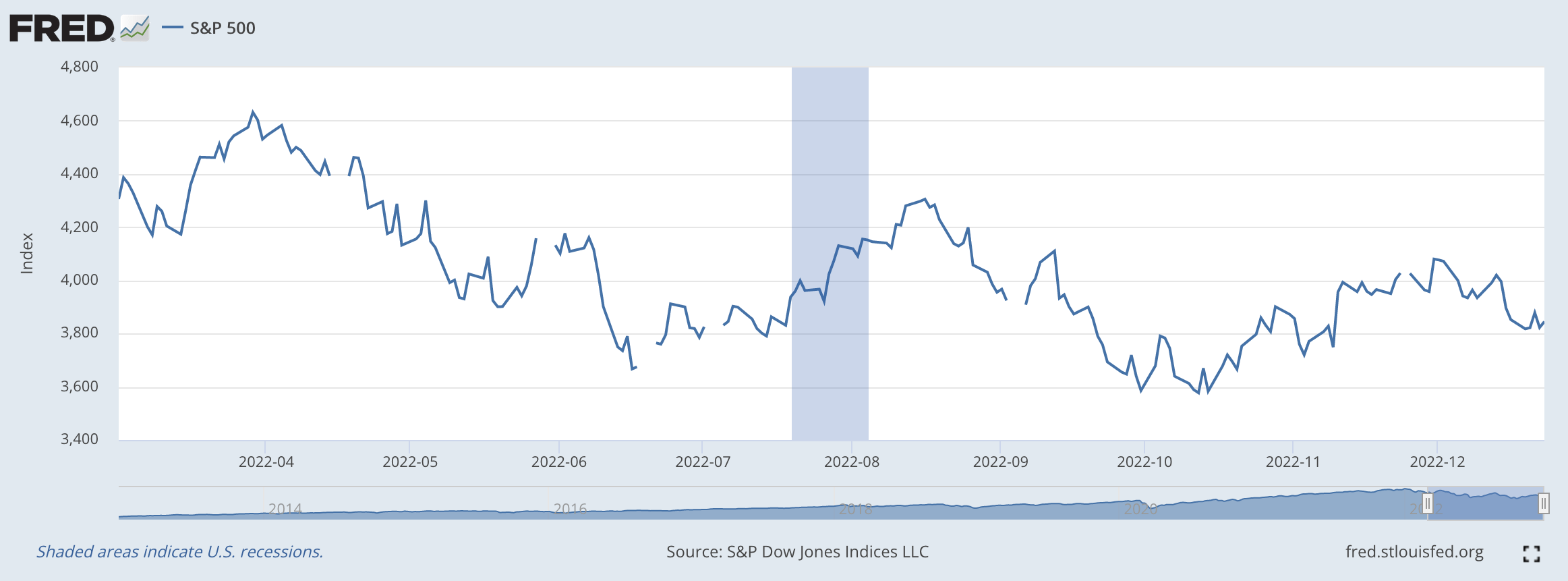

One of the stories following the Federal Reserve’s efforts through the summer months has been the story about how soon investors believe that the Fed will “pivot” from its “tight money” stance into something more accommodating.

This story has been going around all summer and through the fall.

Chairman Jerome Powell just does not seem to have the confidence of the investment community that he…and the Fed…will keep their “foot on the break” for an extended period of time.

Seven times over the past six months, investors have believed that Mr. Powell and the Fed are ready to “back off” of the tight money in order to avoid any kind of a downside surprise.

Mr. Powell has constantly come back and stood up for his efforts to fight inflation and, therefore, to keep his “foot on the brake.”

These battles between Mr. Powell and the investment community can be captured in the swings that have taken place in stock prices over the past six months or so.

Here is a picture of how volatile the S&P 500 Stock Index (SP500) has been since the middle of March, when the Federal Reserve really sprang into action.

S&P 500 Stock Index (Federal Reserve)

Investors just keep thinking that Mr. Powell cannot accept the possibility that the Fed might be connected, at some time, with dramatically falling stock prices. These investors are constantly looking for the Fed to “pivot.”

I don’t think Mr. Powell is going to back down right away, but, he certainly does not have the full confidence of the investment community.

The Dollar

It is my belief that the Federal Reserve wants to achieve a strong U.S. dollar.

And, I don’t think that this is a recent desire. I have written about this quite a few times in the past year or so.

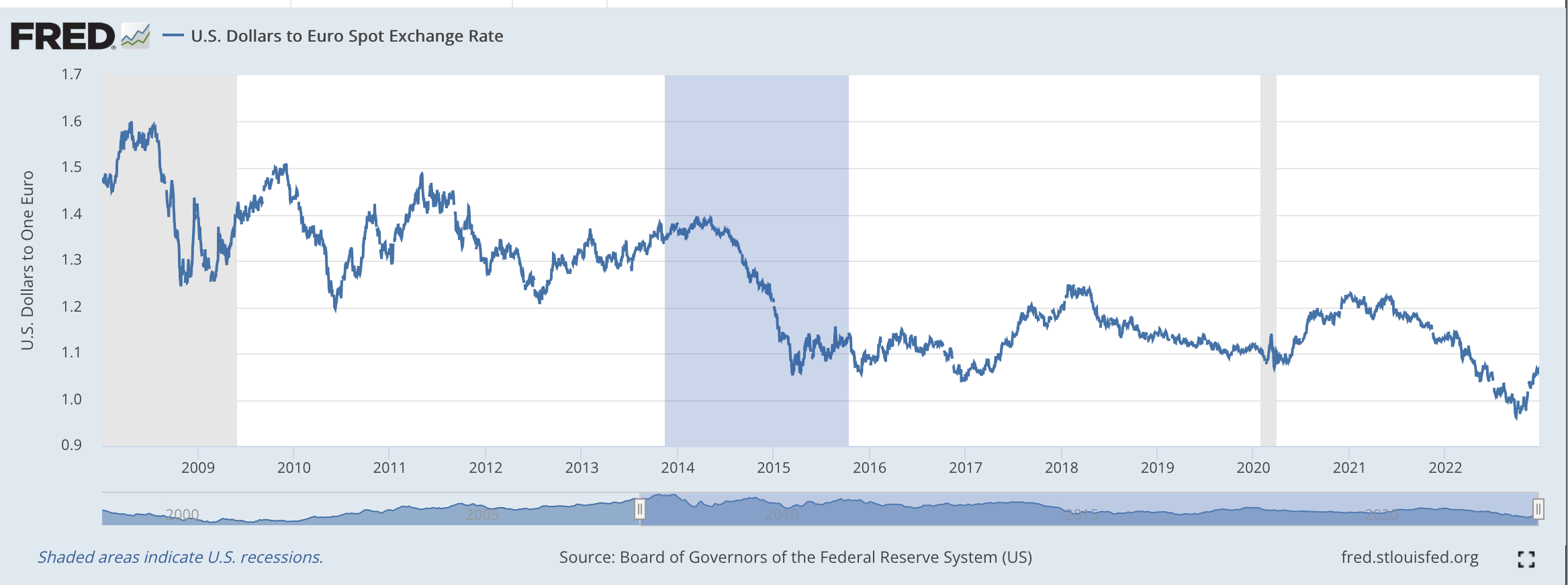

Look at this chart. The value of the U.S. dollar against the Euro has been getting stronger since 2008.

U.S., Dollar Price of One Euro (Federal Reserve System)

Look, in 2008, the cost of one Euro was close to $1.6000.

The trend has been downward ever since…of course with some short-run swings.

The driving force here was the fact that the rate of inflation, from around 2010 to 2020 was a compound rate of about 2.3 percent per year.

This was lower than any other nation during that time period.

The U.S. dollar grew stronger as the rate of consumer inflation remained down around 2.0 percent, the Fed’s target rate.

As a consequence, the value of the U.S. dollar got stronger and stronger and stronger.

Ben Bernanke, Chairman of the Board of Governors of the Federal Reserve System, was well aware of what a modest rate of inflation would do for the dollar.

Mr. Bernanke, in my mind, wanted a strong U.S. dollar.

And, he got it.

I firmly believe that the Federal Reserve, following the appearance of the Covod-19 pandemic, strongly supported the continued increase in the strength of the U.S. dollar.

A strong dollar supported the strengthening of the supply side of the economy. I have also written about this many times. To be more and more competitive in international markets, an economy needs a strong currency because a strong currency creates the environment for improving labor productivity and for encouraging lots and lots of innovation.

Mr. Bernanke saw this and wanted to create the atmosphere where it would happen.

And, he succeeded.

Although the Fed does not talk about it, a strong currency policy helps to build and strengthen an economy over time.

The Federal Reserve, in my mind, has continued this program.

And, will continue the program in the future.

I still believe that the Fed would like to have the U.S. dollar slightly under parity with the Euro.

A good range would be $0.9500 to $0.9900 for one Euro.

This would be consistent with the U.S. having an inflation rate of around 2.0 percent, right on the Fed’s goal.

But, it can back off for a while as the rest of the world adjusts to the current conditions.

Once things smooth out, however, watch for the price of the Euro to fall into the range just mentioned above.

I believe this would be a firm foundation for the future “world-class” performance of the U.S. economy.

Be the first to comment