Steve Pope

In this article, we will look at the outlook for the S&P 500 (NYSEARCA:SPY) against what Berkshire Hathaway’s (BRK.A)(BRK.B) Warren Buffett once described as “the best single measure of where valuations stand at any given moment.” We will also consider some potential bullish and bearish catalysts that could change the calculus for SPY and then we will conclude by discussing our approach in the current environment as we head into 2023.

The Buffett Indicator’s Implications For SPY:

The aforementioned Buffett-endorsed valuation metric for the stock market is known as “The Buffett Indicator” and is defined as the ratio of total US stock market valuation to US GDP.

While Mr. Buffett has since clarified that there are many factors that go into evaluating markets and that it is often a fool’s errand to try to time the markets, the fact remains that it has proven to be a useful model for assessing the forward outlook for stock markets and Buffett himself has said that it has some value for this very purpose.

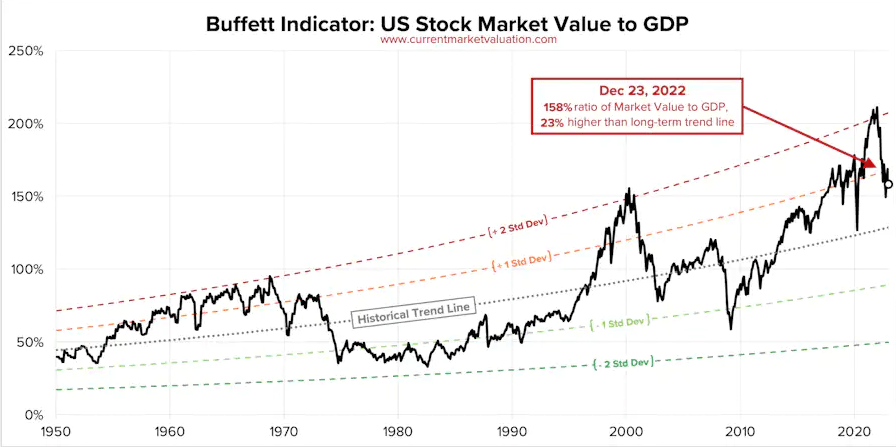

Based on the historical data, the Buffett Indicator looks to be a bit on the high side at the moment, with the total market value to GDP ratio at ~158%. While this is down significantly from the bloated levels seen a year ago, it remains elevated relative to historical norms. It is in fact 23% – or nearly 1.5 standard deviations – above than the long-term trendline as illustrated in the chart below:

Buffett Indicator (current market valuation)

This indicates that SPY is likely to underperform its historical average of ~10% annual returns moving forward. Other valuation models also indicate this, including the Yield Curve Model whose recent inversion signals trouble is ahead for the economy, the Price/Earnings Model that shows the US cyclically adjusted price to earnings ratio is ~1 standard deviation its historic average, and the S&P 500 Mean Reversion Model that shows that SPY is currently trading at 27% – or ~0.8 standard deviations – above its modern-era historical average.

Potential 2023 Bullish & Bearish SPY Catalysts

When you add on to these risks of the continued high inflation (though this appears to be waning), a widely expected recession in 2023, the Fed’s sustained hawkish language, and the soaring geopolitical risks facing us today, the outlook for SPY is far from rosy. While the bear case is certainly compelling, there is a very real bullish case as well.

Perhaps the biggest potential bullish tailwind is that there is no guarantee that there will in fact be a recession in 2023. While many have voiced concern that the Fed’s aggressive pace of rate hikes this year will break the back of the economy and plunge it into recession in 2023 and potentially beyond, this has yet to materialize and – until it does – it is very possible that the Fed will be able to achieve a soft landing for the economy after all, where inflation comes down and the economy manages to skirt a recession entirely. We do not think this is likely and fully expect a recession to hit in 2023, but prominent economists such as those at Goldman Sachs (GS) apparently do think we will achieve a soft landing to inflation. If we do see the economy avoid a recession next year and inflation continues to come down, SPY will likely see solid performance as some of its largest components like Tesla (TSLA) will undoubtedly see their share prices recover strongly if demand is sustained and inflationary concerns also begin to subside simultaneously.

Another big potential bullish tailwind is if the Federal Reserve pivots away from rate hikes in 2023 and even goes to rate cuts. Fed officials are forecasting a 3.1% inflation rate in 2023, which – while not quite at their long-term target rate – would mark significant year-over-year deceleration and certainly make the case that further rate hikes are not needed if it materializes. According to CME Group’s FedWatch, the majority of investors currently project that interest rates will peak at 4.75-5% next year and that by year-end the Federal Reserve will have begun cutting interest rates and reduced the Federal Funds rate to 4.25-4.5%

A final bullish tailwind – though this may not fully manifest itself for a few more years – is the rapid deflationary impact of technological innovation. In particular, the advances of robotics and artificial intelligence technologies are removing the need for labor to perform many repetitive tasks and will likely eventually eliminate the labor shortage that is one of the primary current drivers of inflation (and by extension higher interest rates). On top of that, these technologies are also expected to create trillions of dollars in wealth in the coming years. To the degree that these innovative forces manifest themselves in 2023, they will undoubtedly be a bullish tailwind for SPY.

Investor Takeaway: Our Approach

While we obviously do not know for sure what 2023 has in store for the economy or SPY, we are somewhat concerned about the medium-term total return potential being offered by SPY at current prices. At a minimum, we believe that the risk-reward is less attractive than average. Between the elevated Buffett Indicator and other valuation models and the significant potential bearish catalysts, investors who have a low risk tolerance and/or do not think they can handle volatility in their net worth should probably keep their exposure to SPY and markets on the whole to a small level.

That said, we believe in what the data has borne out: time in the market is almost always more important to long-term wealth compounding than timing the market. Markets can behave irrationally for a long time and there is no guarantee that SPY will crash at all in the future. Instead, it may simply generate 6-8% annualized returns over a long period of time and gradually grow its earnings power into its valuation. Investors who sit in cash waiting for a crash that never materializes will get burned in such a scenario.

Furthermore, if the Federal Reserve does bias itself towards supporting markets with a more dovish approach to interest rates (as investing legend Howard Marks seems to think will happen), it is very possible that the markets will experience a sharp recovery at least in the short term.

Last, but not least, technological innovation may very well take the baton from the Federal Reserve’s easing in 2023 and ignite strong economic growth and deflationary pressure that enable the Federal Reserve to keep interest rates historically low for a long time to come. Such a scenario could very easily lead to continued impressive gains for SPY for the foreseeable future.

At High Yield Investor, we remain invested across a diversified range of sectors, reflecting our uncertainty at which scenario will play out. Furthermore, our focus on value and income gives us some margin of safety in either case. However, our weighting at present reflects our expectation that a recession is likely in 2023 and that interest rates will peak in early 2023 and quite possibly be cut by year-end. As a result, we are weighted more heavily towards defensive business models – like utilities (XLU), defensive REITs (VNQ), and conservatively positioned and underwritten secured lenders – whose stock prices have been beaten down in 2022 due to rising interest rates but will likely outperform in a recession. We are also on guard against soaring geopolitical volatility by investing pretty heavily in gold miners (GDX) and other businesses that benefit from high market volatility.

Be the first to comment