akinbostanci

Published on the Value Lab 11/2/22

Tiptree (NASDAQ:TIPT) is really a story about Fortegra, their specialty insurance. Not only was it growing successfully alone at high organic rates, the recent acquisition of 24% in the Fortegra holding within Tiptree also means a partnership that can put its specialty insurance business that has a big focus on executive liability in a good position for further, networked growth. The acquisition by Warburg Pincus also values the company at a substantial premium from today’s prices. While capital market conditions have notably changed, there is certainly a margin of safety in this investment that cannot be denied.

Quick Q2 Look

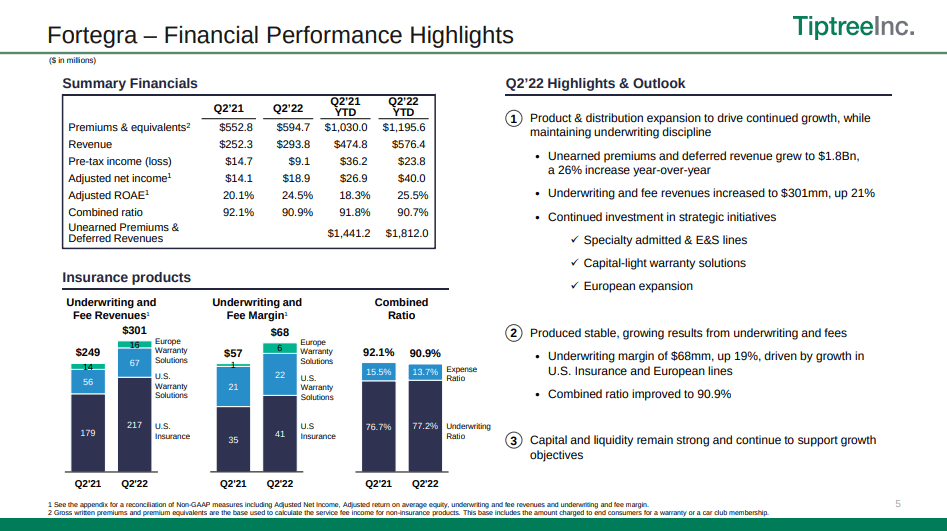

Fortegra performed well YoY in terms of growth at stronger expense ratios thanks to both E&S and specialty strength. About 66% of Fortegra business is in specialty insurance.

Fortegra Performance (Q2 2022 Pres)

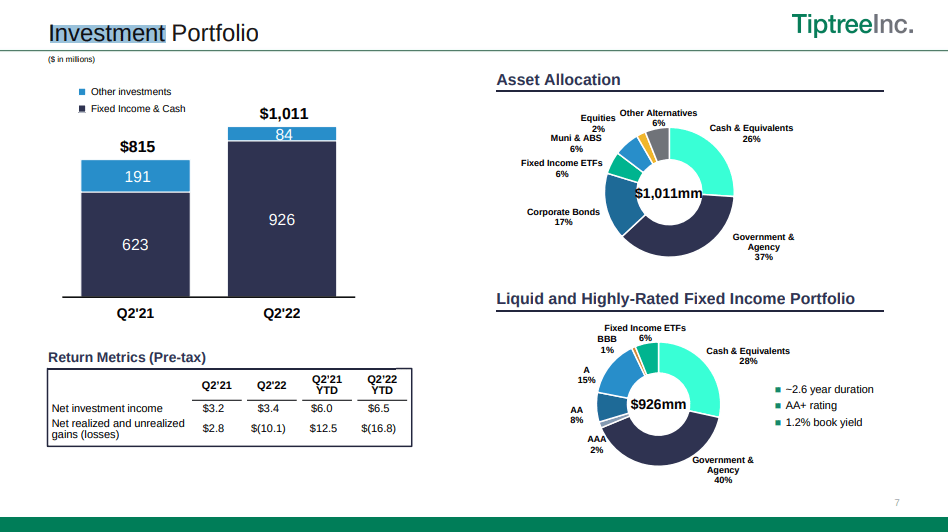

As is typical of insurance businesses right now, they are well positioned with substantial fixed income positions that have rolled over at attractive rates as interest rates rise. Duration is a little on the long side in principle at 2.6 years, but the velocity of rollovers is higher since this is just an average figure, and a decent amount of those securities are likely to be rolling over now with the rest being long enough maturity to see a possible recovery in price once the rate hiking cycle appears to come to an end.

Investment Returns (Q2 2022 Pres)

The Tiptree Capital business, which is the counterpart to the Fortegra exposure, is a mortgage origination business that has seen declines on account of lower mortgages originated right now. The other thing that the company does is own dry bulk tankers. While in Q2 those rates were still rising, they have likely since fallen, especially in dry bulk. Tiptree Capital is only 10% of revenue, and in turn, the maritime business is only half of that, so the effects won’t be too pronounced.

The Warburg Pincus Connection

What accentuates the Tiptree thesis is firstly that it offers the cash flow generative exposure of an insurance company with a model that makes sense at the points in the rate cycle that are dangerous for the rest of the market. Secondly, the Warburg Pincus ownership means that there is a vested interest to get Fortegra into the door with its other portfolio companies. Large executive and director liability packages can be underwritten thanks to Warburg that will actually move the needle due to the company’s still pretty low scale, so there’s an organic growth opportunity there.

The biggest thing to point out regarding the Warburg Pincus acquisition is how it valued the company in October 2021. The implied valuation of TIPT ignoring Tiptree Capital for a moment was about $800 million. Warburg only invested in the Fortegra component, but assuming that it accounts for all the TIPT value, we can say that the implied price for TIPT should be around $22, which is a 70% upside from current levels.

Capital market conditions have changed substantially from when that acquisition was made, and indeed multiple has fallen. Still, comparing TIPT to other specialty insurance companies like RLI Corp. (RLI). The P/Bs are very different despite tackling some of the same markets. RLI is at over 4x while TIPT is at less than 1.5x. The Warburg Pincus acquisition did pop the capitalisation from $169 million in 2020, but it should have anyway gone further than the $15 peak it reached around the time of the acquisition considering the implied value. With earnings growth having proceeded substantially since then, indeed net income is up 12% YoY similar to RLI’s as well, the valuation appears strange. With directional safety as well as a value proposition, we are bullish on the stock.

If you thought our angle on this company was interesting, you may want to check out our idea room, The Value Lab. We focus on long-only value ideas of interest to us, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our gang could help broaden your horizons and give some inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment