Melpomenem/iStock via Getty Images

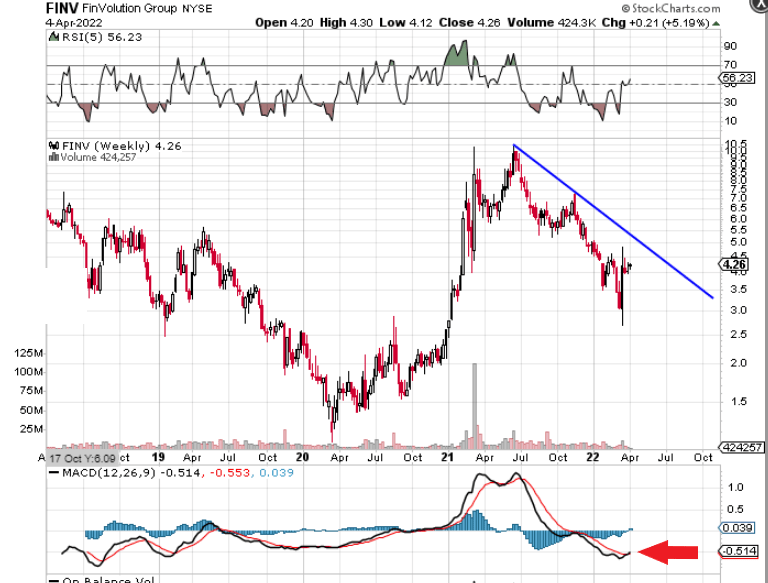

If we look at a technical chart of FinVolution Group (NYSE:FINV), we can see that shares seem to be in the process of giving a buy signal by means of the popular MACD indicator. We believe this indicator is especially noteworthy on long-term charts due to the duality of the signal (Momentum & Trend) and the amount of information studied. To ensure though that this buy signal does not end up being a false dawn for the company, we still would need to see shares break above that downcycle monthly trend line before we could categorically state that a new bullish trend has begun in FinVolution.

Technical chart of FinVolution (Stockcharts.com)

We wrote about FinVolution prior to the announcement of its fourth-quarter earnings report when we stated that the sustained shift to better quality borrowers would eventually bear fruit. Given the record numbers we witnessed once more in Q4, it is evident that the company’s technology concerning borrowers continues to separate the wheat from the chaff. For example, transaction volume increased by 81%, and the loan book increased by 88% in Q4 over the same period of 12 months prior with risk management remaining paramount. This means the company acquired well over 4 million new borrowers in fiscal 2021 which is a feat in itself.

Suffice it to say, the main attraction in FinVolution from a long-term investor’s standpoint should be the stock’s valuation as well as the generous dividend on offer. Shares currently trade with a trailing GAAP earnings multiple of 3.2, a trailing book multiple of 0.73, and a trailing sales multiple of 0.81. The dividend almost tops 5% as the stock goes ex-dividend next week with the latest $0.205 per share annual amount. The fact that FinVolution’s valuation multiples remain well below the averages in this sector and top-line growth is expected to once more exceed 10% this year should demonstrate the potential that exists in FINV. Throw the sustained buybacks into the mix here and it quickly becomes evident that earnings should enjoy a strong tailwind going forward.

In saying this, management was cautious with respect to fiscal 2022 guidance on the most recent Q4 earnings call due to ongoing COVID outbreaks in China and this was masked somewhat by the announcement that Beijing was pledging to support equity markets. Suffice it to say, this is where the uncertainty lies with FINV at present. Can earnings continue to grow which will fuel strong growth in that annual dividend? It is a valid question and especially pertinent in the current environment. Why? Because as inflation runs rampant in western countries, international investors especially will be looking to keep their purchasing power intact. The latest annual increase in FinVolution’s dividend surpassed 20% and remains well above current inflation rates in the west. Even if management cannot keep up this growth rate, here are some reasons why we believe FinVolution’s dividend growth rate will remain elevated.

- On the latest earnings call, management pledged to keep distributing an annual cash dividend which will be at least 10% of the firm’s annual net profit after tax. This is only the baseline number though as 15% of net profit will be paid to investors next month for fiscal 2021.

- We believe the market is underestimating the scope with respect to the company’s international operations. Transaction volume of RMB3.7 million was a 270% gain over fiscal 2020 and this number included another covid outbreak in Southeast Asia. 32% of all new borrowers in fiscal 2021 came from international markets.

- FinVolution’s economies of scale over time will increase earnings for the following reason. Essentially it is all about the numbers and current trends are pointing to growing profitability in the long run. As better quality borrowers continue to increase in number and improvements are made in the firm’s risk modeling practices, risk will subside as we can see in recent declining delinquency rates.

Therefore, to sum up, we maintain that FinVolution remains a compelling long-term Fintech investment because of its growth profile, valuation, and high dividend yield. Furthermore, with management pledging to pay at least 10% of annual net profit towards the dividend, growth should continue here for some time to come. Let’s see if that monthly downcycle trend-line can be taken out shortly. We look forward to continued coverage.

Be the first to comment