Kelvin Murray

Author’s note: This article was released to CEF/ETF Income Laboratory members on August 23rd, 2022. Please check latest data before investing.

Virtus

ZTR rights offering

The rights offering for Virtus Total Return Fund Inc. (ZTR) is now live. From the press release:

Virtus Total Return Fund Inc. Rights Offering Declared Effective. HARTFORD, Conn., Aug. 1, 2022 /PRNewswire/ — Virtus Total Return Fund Inc. (NYSE: ZTR) announced today that the registration statement for its rights offering has been declared effective by the U.S. Securities and Exchange Commission. The Fund will issue to shareholders non-transferable rights entitling them to acquire one share of common stock for each three shares held, up to an aggregate of 16,500,000 shares of common stock of the Fund. The Fund may increase the number of shares of common stock subject to subscription by up to 25% of the shares, or up to an additional 4,125,000 shares of common stock, for an aggregate total of 20,625,000 shares. Shareholders of record will receive one right for each outstanding share owned on the record date, August 9, 2022. If a record date shareholder’s total ownership is fewer than three shares, such shareholder will receive three rights so that the shareholder may subscribe for one share. The subscription period will be from August 10, 2022 to 5:00 p.m., New York City time, on September 16, 2022, unless extended until 5:00 p.m., New York City time, to a date not later than October 16, 2022. (Brokers may apply an earlier cutoff time, so shareholders that hold their shares through brokers should contact their brokers about the applicable end of the offering period). The subscription price per share will be equal to 95% of the lower of [i] the net asset value per share of the Fund’s common stock at the close of business on September 16, 2022 (the expiration date of the subscription period, unless extended), or [ii] the average of the last reported sales price of a share of the Fund’s common stock on the New York Stock Exchange on such date and the four preceding business days.

In summary, this is a non-transferable one-for-three offering for new shares, with an optional 25% oversubscription quota. Hence, the fund will be able to grow its AUM by +33.3% (+16.5m shares) assuming full subscription, and up to +41.7% (+20.6m shares) with the oversubscription fully allocated. The ex-rights date was August 8, 2022, and the offer will expire on September 16, 2022.

ZTR is a $400m hybrid equity/fixed income fund focused on the utilities/infrastructure sector. It isn’t a portfolio position, but Nick last covered ZTR for our members here: ZTR: Utilities To The Rescue (public link). In that April article, Nick noted that ZTR’s premium remained stubbornly high despite market weakness. The high premium is probably what compelled the managers of ZTR to pull the trigger on the rights offering in order to grow AUM. Which of course caused the premium to tank, but much better to do it from a high point than when the discount is already depressed.

The subscription price will be equal to the lower of 95% of the NAV on the expiry date, or 95% of the average closing market price on the final five days of the offering. The lack of a “floor” for the subscription price means that the offering is more likely to be dilutive to the NAV/share of the fund; in fact, the minimum NAV hit would be -1.47% according to the subscription formula assuming full subscription including the oversubscription allotment.

For some inexplicable (to me) reason, ZTR’s premium actually rose after the rights offering announcement. Were some investors so enthused by the prospects of taking part in the rights offering that they bid up the fund? Remember, this is a non-transferable rights offering so only investors who owned the fund before the ex-rights date could take part.

We generally suggest investors sell a fund which is undergoing a rights offering, particularly before the ex-rights date. This is because the price of the CEF often drops by much more than what the intrinsic value of the rights are worth on ex-rights date, not to mention the generally negative price pressure on the CEF throughout the entire rights offering period. Hence, we also recommended our investors to sell ZTR before its ex-right date.

Income Lab

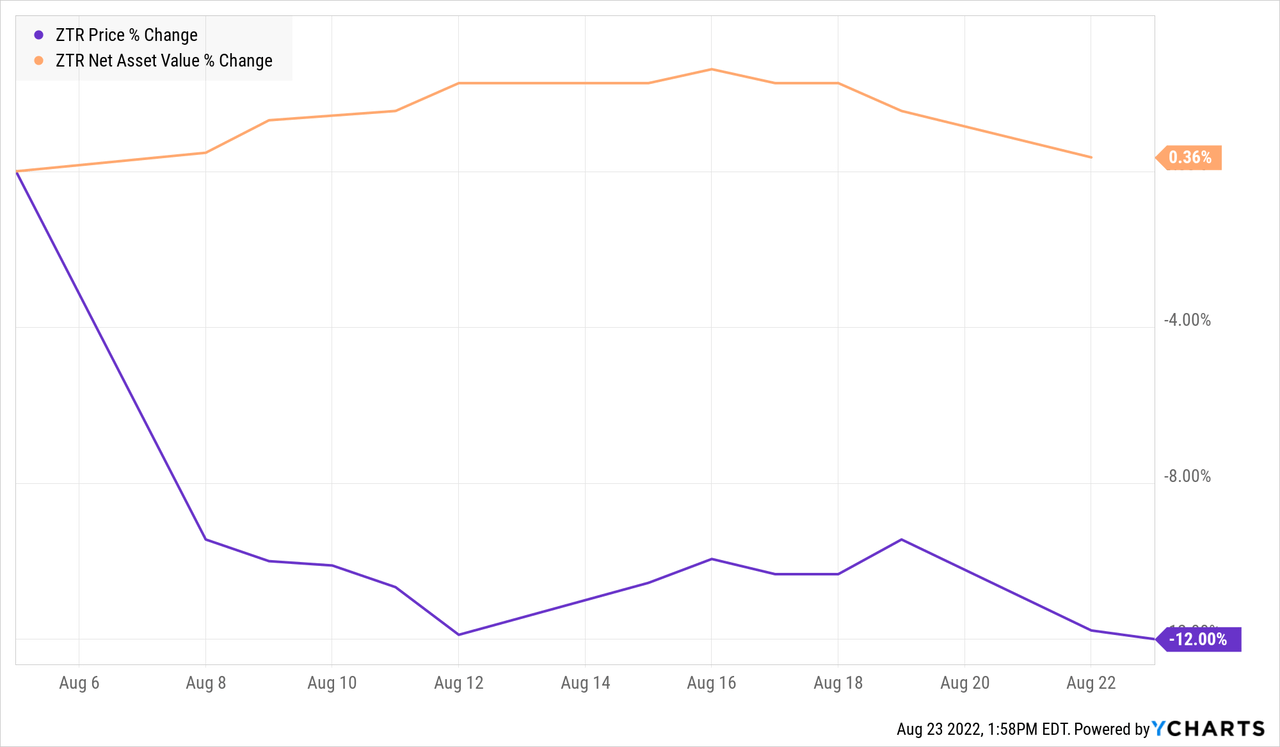

And indeed, our prediction proved to be correct as ZTR has declined significantly in price after its ex-right date even while the NAV of the fund has stayed relatively constant. While an investor who sold out of ZTR would no longer be able to take part in the rights offering, buying back a greater number of shares with the same amount of capital (i.e. “free shares”) using the sell-and-rebuy strategy is more beneficial than subscribing (i.e. paying for) slightly discounted shares in the rights offering process.

YCharts

I am glad that at least one member was able to gain free shares of ZTR using this strategy!

Income Lab

Subscription strategy

With regards to the offering itself, because there is no floor to the subscription price, it will always be more beneficial to subscribe rather than not subscribe. Moreover, since the rights are non-transferable, there’s also no ability to sell the rights on the open market to compensate for the impending dilution. Hence, I would recommend an investor holding ZTR rights to subscribe for the maximum number of shares, rather than letting the rights expire worthless.

Interestingly, with these kinds of dilutive offerings there’s a bit of a prisoner’s dilemma situation going on. The more investors subscribe, the more AUM the fund gains but also the more dilution there will be at the NAV/share level since this is a dilutive offering. At current discount, the NAV/share hit is estimated to be -3.09% assuming maximum subscription including the oversubscription allotment. However, if all investors coordinated with each other for their collective long-term benefit, none of them should subscribe as this would eliminate the NAV/share dilution effect. However, since each individual investor will always benefit more from subscribing rather than not subscribing (regardless of what anyone else is doing), the end result is that there will be a high level of subscription and dilution. This is one of the main consequences of the prisoner’s dilemma: decisions made under collective rationality may not necessarily be the same as that made under individual rationality.

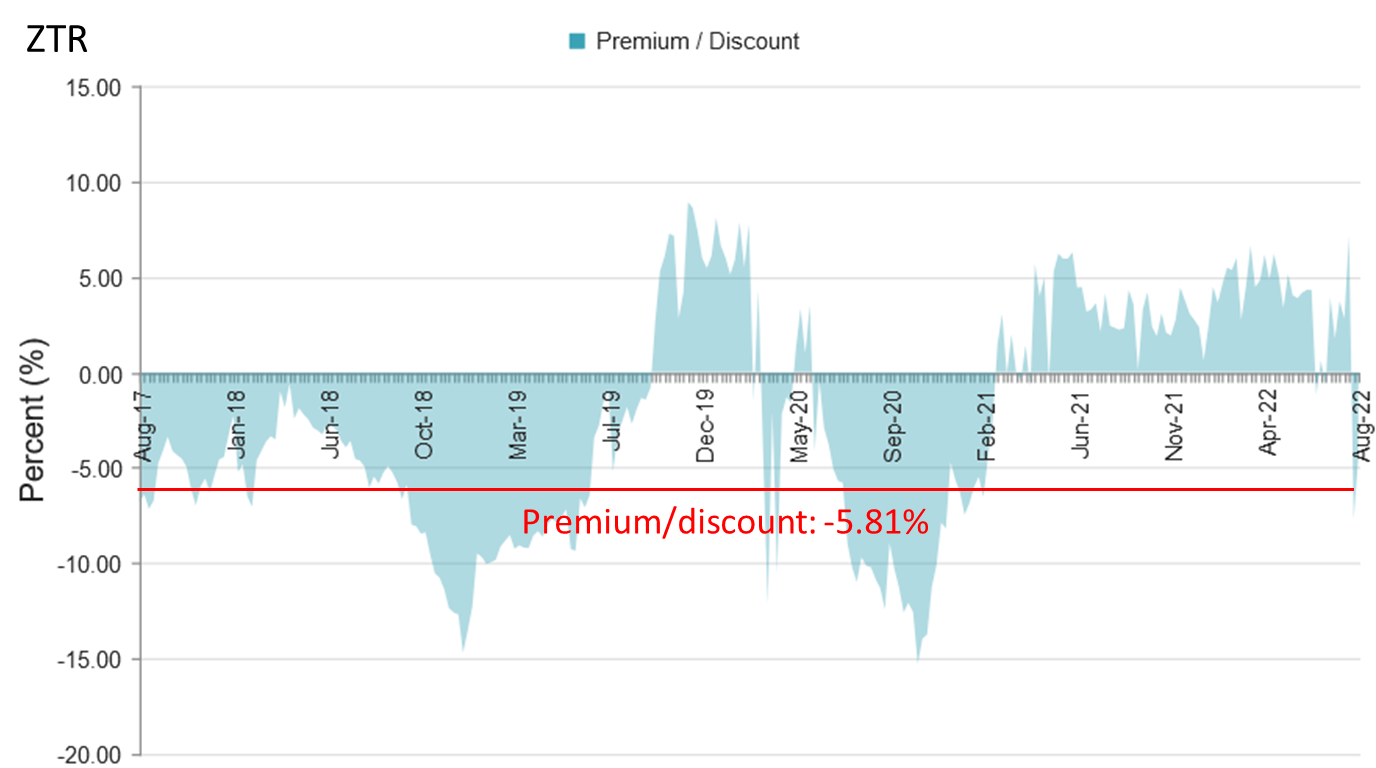

Right now, ZTR’s -5.81% discount makes it relatively underpriced compared to its 1, 3 and 5-year average premium/discounts of +3.21%, +0.21% and -2.36% respectively, and the 1-year z-score is -3.6. For investors looking to get into ZTR, I would still generally wait for the rights offering to expire and the new shares to be issued before buying, as this is where the selling pressure should theoretically ease.

CEFConnect

Strategy statement

Our goal at the CEF/ETF Income Laboratory is to provide consistent income with enhanced total returns. We achieve this by:

- (1) Identifying the most profitable CEF and ETF opportunities.

- (2) Avoiding mismanaged or overpriced funds that can sink your portfolio.

- (3) Employing our unique CEF rotation strategy to “double compound“ your income.

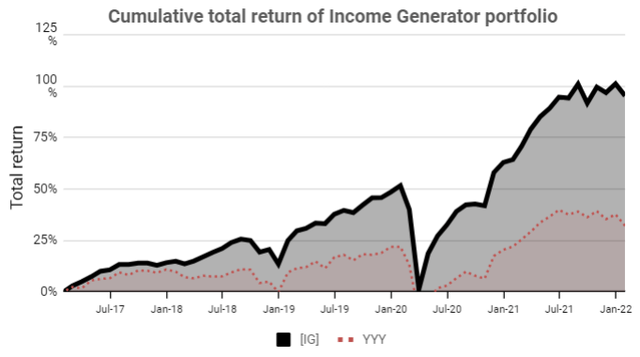

It’s the combination of these factors that has allowed our Income Generator portfolio to massively outperform our fund-of-CEFs benchmark ETF (YYY) whilst providing growing income, too (approx. 10% CAGR).

Income Lab

Remember, it’s really easy to put together a high-yielding CEF portfolio, but to do so profitably is another matter!

Be the first to comment