Leonid Sorokin

Billionaire investor Charlie Munger – Warren Buffett’s partner at Berkshire Hathaway (BRK.A, BRK.B) – recently opined that “considerable trouble” was coming for markets at the Daily Journal’s (DJCO) annual meeting earlier this year, stating:

What we’re getting is wretched excess and danger for the country. Everybody loves it because it’s like a bunch of people getting drunk at a party; they’re having so much fun getting drunk that they don’t think about the consequences. Eventually, there will be considerable trouble because of the wretched excess, that’s the way it’s usually worked in the past.

He went on define what he meant by wretched excess:

Certainly, the great short squeeze in GameStop (GME) was wretched excess. Certainly, the bitcoin (BTC-USD) thing is wretched excess. I would argue venture capital is throwing too much money too fast, and there’s a considerable wretched excess in venture capital and other forms of private equity…There’s never been anything quite like what we’re doing now. We do know from what’s happened in other nations, if you try and print too much money it eventually causes terrible trouble. We’re closer to terrible trouble than we’ve been in the past, but it may still be a long way off.”

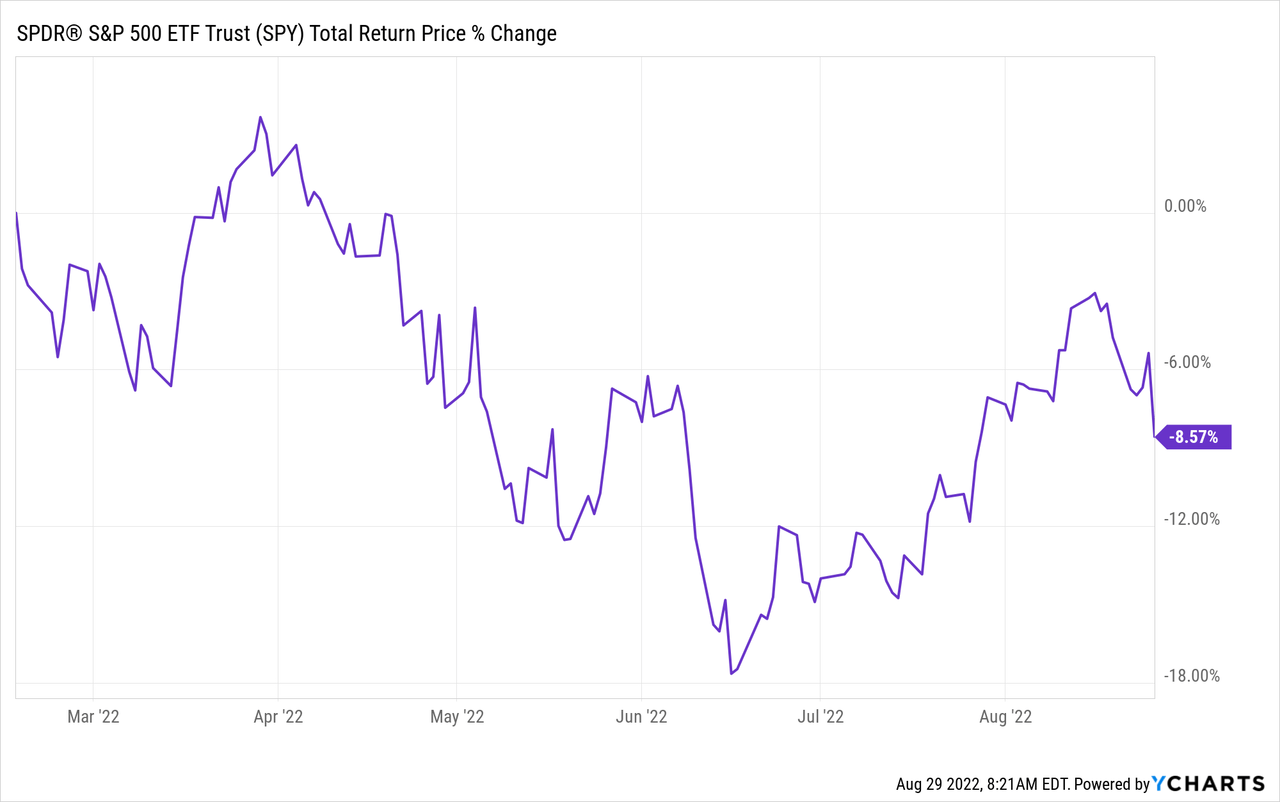

While the SPDR S&P 500 Trust ETF (NYSEARCA:SPY) has delivered -8.57% returns since that meeting, it has not yet experienced the “considerable trouble” of which Mr. Munger spoke:

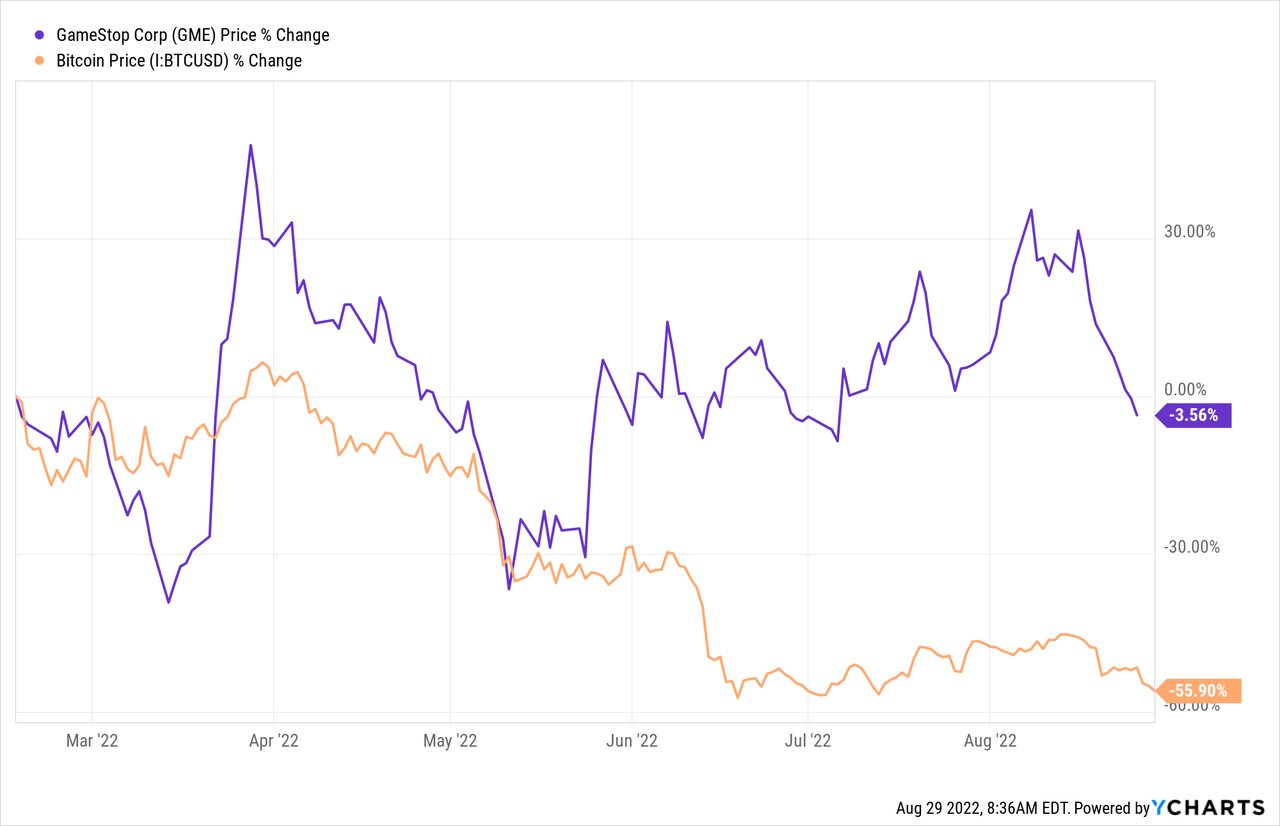

However, we can certainly see that the wretched excess has continued in the months since and the symptoms of it have also increased. While the crypto bubble has continued to burst, with bitcoin down an addition 56% since Mr. Munger’s remarks, GME continues to enjoy an elevated valuation:

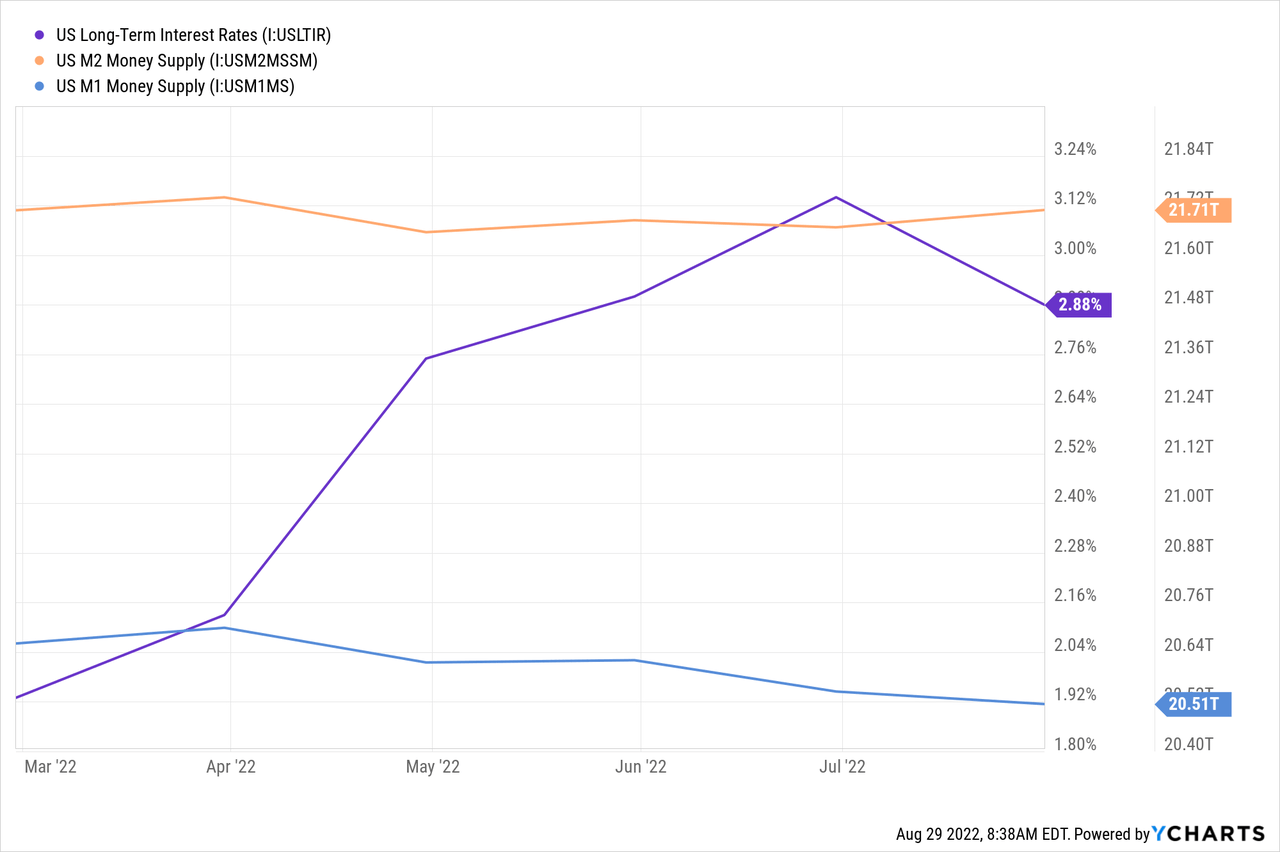

We can also see that interest rates remain near historic lows – despite rising considerably in recent months – and the highly inflated money supply has remained relatively flat since Mr. Munger made his remarks:

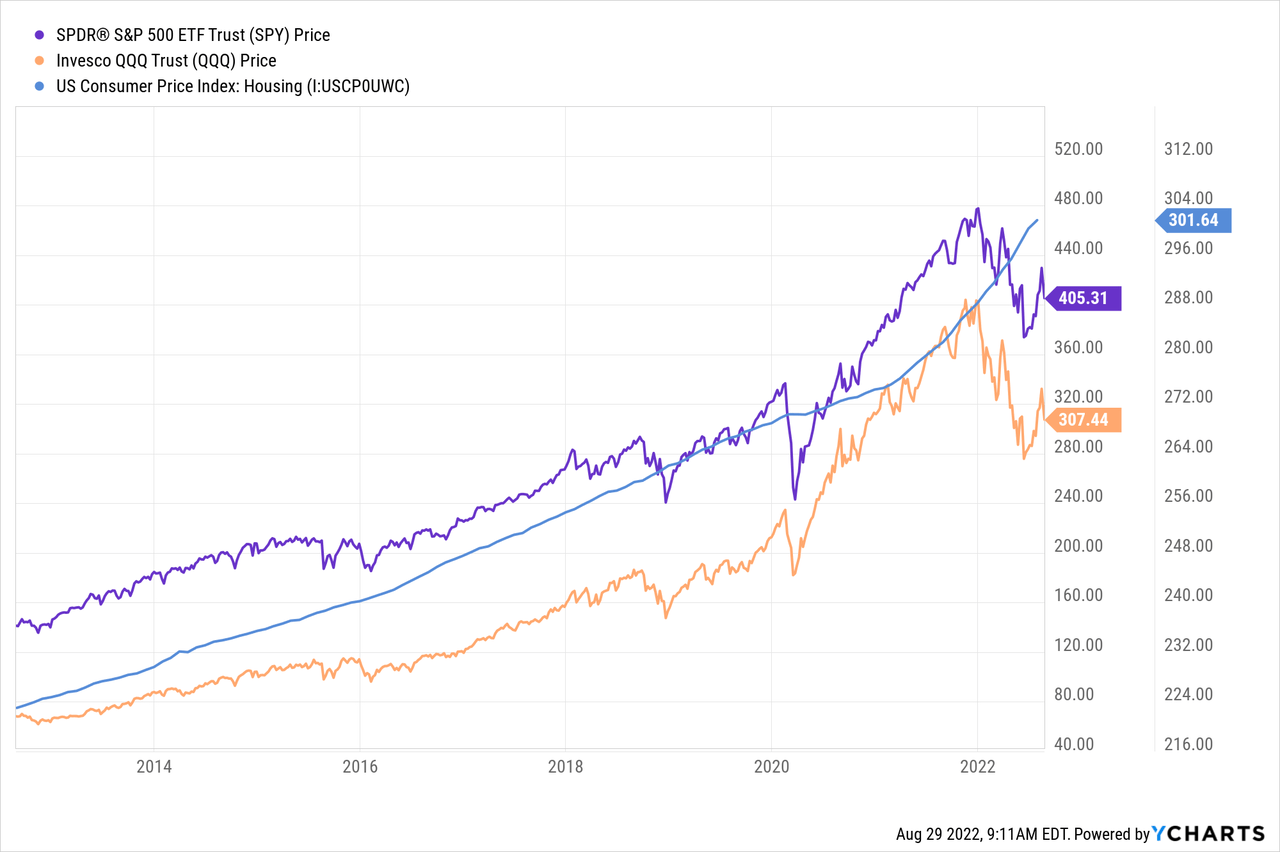

We can also see that market indexes and especially housing prices remain elevated:

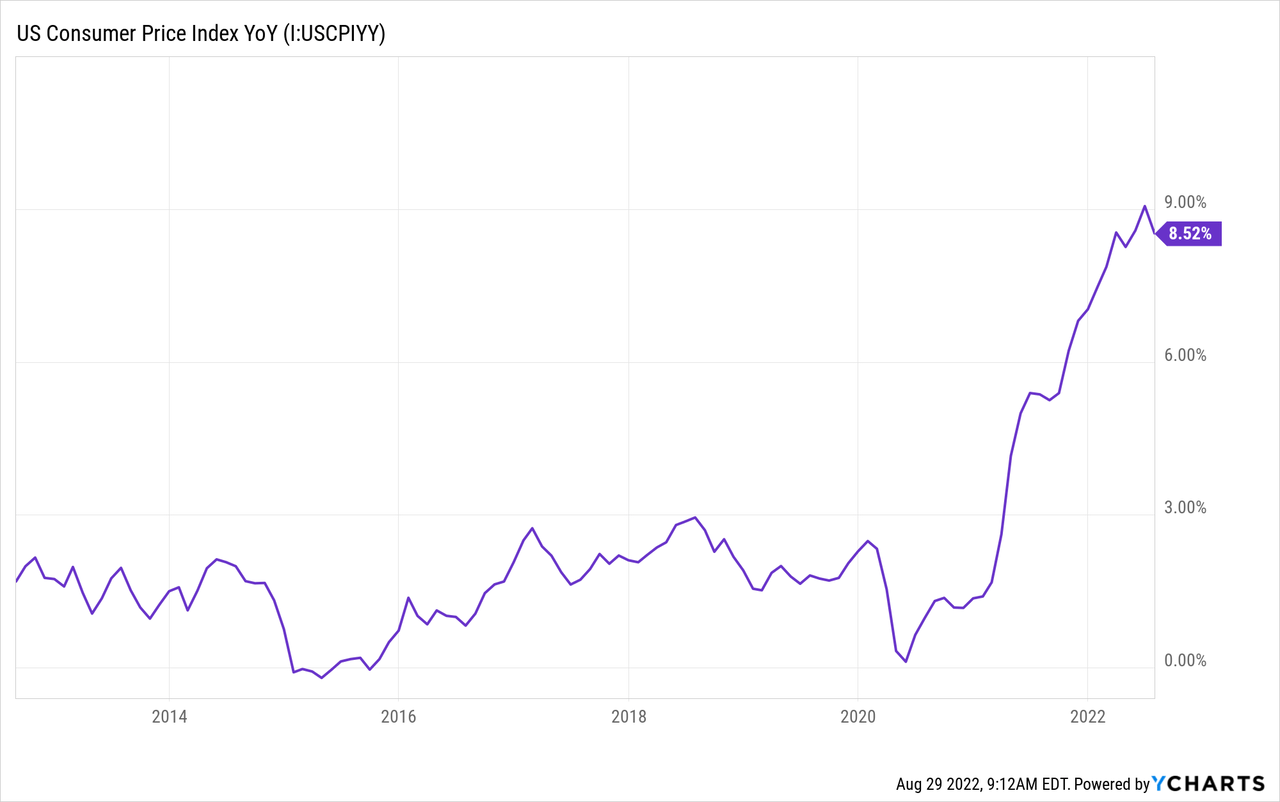

However, the consequences of all this excess and bubble-like behavior are beginning to be felt, with GDP declining for two quarters in a row and inflation soaring to four-decade highs in recent months:

In this article, we will discuss the implications that this has for the SPY as well as our investing approach in the current environment.

Implication #1: Forward Returns Are Likely To Be Lackluster

The biggest takeaway from Mr. Munger’s remarks in light of current macroeconomic and market conditions is that forward returns for the SPY are likely to be lackluster. The reasons for this are pretty straightforward:

1. The economic growth outlook is weak, if not negative for the foreseeable future. Without strong economic growth, earnings growth is bound to be weak as well.

2. Valuation multiples are elevated relative to historical averages. According to data compiled by Current Market Valuation based on an equally weighted average of the Yield Curve, Buffett indicator, P/E Ratio, Interest Rate, Margin Debt, and S&P 500 Mean Reversion models based on historical data, the market is currently towards the upper end of the fairly valued range. This means that it is almost overvalued, implying that the market is likely to experience lackluster, if not poor, returns for the foreseeable future. The SPY is overvalued according to the Yield Curve, Buffett Indicator, P/E Ratio, and S&P 500 Mean Reversion models, is slightly above fair value according to the Interest Rate model, and slightly below fair value according to the Margin Debt model.

3. Interest rates are likely to rise further, based on persistently high inflation and the Federal Reserve’s latest comments. Higher interest rates in the near future will make the market seem overvalued at present according to the Interest Rate model, adding further weight to the argument that the market is overvalued at the moment. Higher interest rates will also act like gravity on asset valuations, driving them lower.

When you combine weak growth with a lack of multiple expansion (and in fact likely multiple compression), very low dividend yields, and likely interest rate increases, there are no real catalysts to drive stock market returns.

Implication #2: Volatility Will Likely Be Elevated For The Foreseeable Future

That said, interest rates do remain historically cheap and there is still a lot of excess capital sloshing around in the global markets. As a result, there will still likely be plenty of dip buying, especially on any hints of inflation declining, the economy weathering the current headwinds better than expected, and/or the Federal Reserve beginning to change its hawkish stance. As the bulls and bears continue to duke it out in aggressive fashion, with bulls aggressively buying dips and bears aggressively selling rips on renewed fears of a recession and/or further interest rate hikes, volatility will likely remain elevated.

On top of that, with geopolitical risks mounting in East Asia, the Middle East, and Eastern Europe, there are plenty of potential further catalysts for sending stocks plunging lower at a minute’s notice.

Implication #3: A Market Crash Is Very Possible

As already indicated in implication #2, a market crash is also very possible at the moment. The reasons for it are simple:

1. As already highlighted, valuations are already bloated, so a crash would not require a stark departure from historical valuation levels. In fact, a crash might be necessary to fully correct financial markets from all of the artificial stimulus from central bankers over the past decade.

2. There are numerous catalysts which could spark a market crash, and they seem more likely at the moment than at any time in recent memory: any number of geopolitical crises, ranging from a Chinese invasion of Taiwan, to the war in Europe going nuclear, to a major energy crisis if a war begins between Iran and Saudi Arabia, a massive cyber-attack that significantly disrupts the global economy, a major new pandemic or variant of COVID-19 emerging, or even possibly a major global recession.

Investor Takeaway

While these are certainly complicated, if not extremely challenging, times for investors trying to navigate the markets, we are remaining fully invested. However, we are keeping the following principles in mind to guide us with greater prudence during this period:

1. We are being highly selective by only investing in securities that appear to have a clear margin of safety, while keeping a small weighting in our most cyclical positions and overweighting our most defensive positions.

2. We are avoiding taking on any personal leverage through this period in order to minimize our risk of outsized losses in the event of a market crash and to give us the capacity to potentially create some dry powder to capitalize on a market crash.

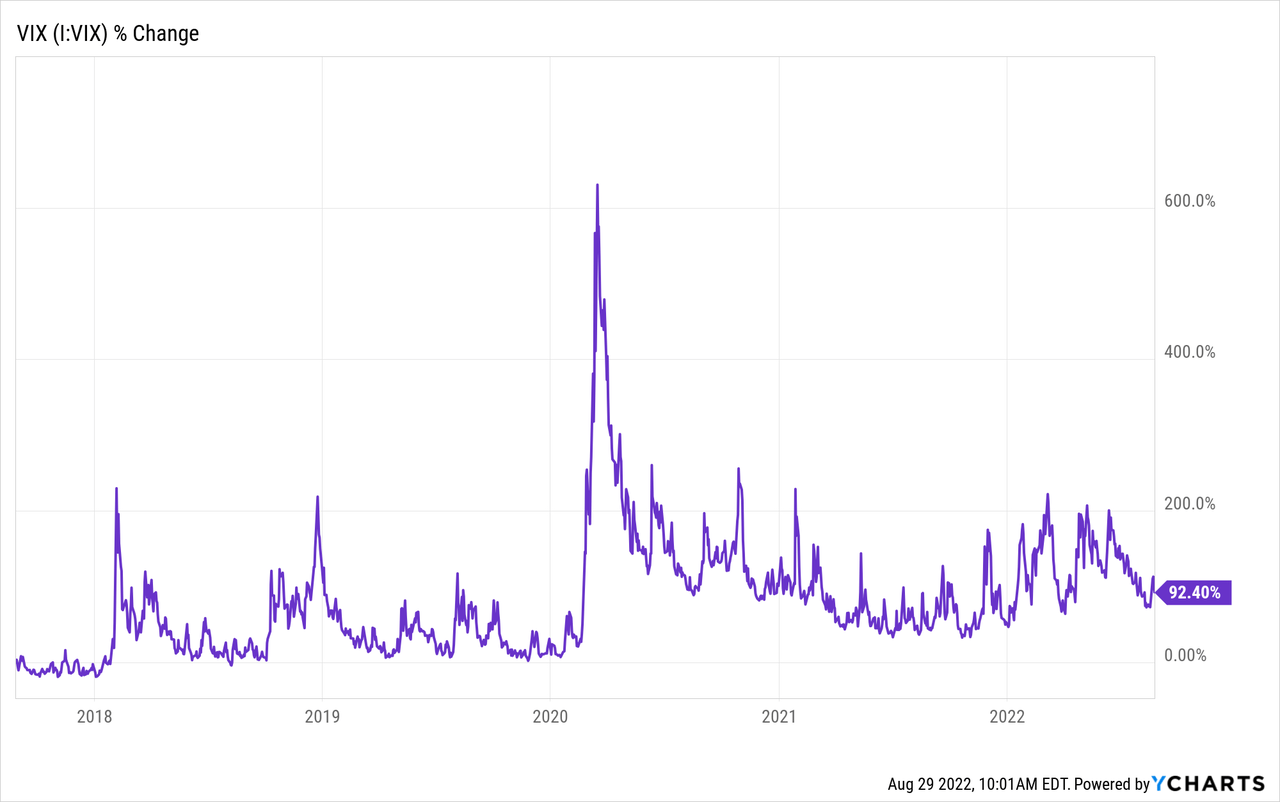

3. We are also investing in securities that profit from elevated volatility as we believe that – even in a scenario where the markets do not experience a full-fledged crash – volatility levels will likely be above average for the foreseeable future due to the geopolitical and macroeconomic jitters that are gripping the markets with increasing frequency. As the chart below indicates, volatility as depicted by the VIX is up significantly from where it was before COVID-19 and is even up in 2022 relative to the second half of 2021.

For those who choose to continue investing in low-cost index funds like SPY, we are not bullish in the short-term, as – for the reasons outlined in this article – we expect lackluster economic growth, elevated valuations, rising interest rates, and the rising risks of a black swan event to suppress broad market total returns for the foreseeable future. As a result, we encourage investors to be more selective in the current environment than to blindly buy the broader market. At the same time, for those committed to passive investing over the long term, remaining fully invested with a practice of consistent long-term dollar cost averaging and prudent personal financial management is unlikely to deliver disappointing results over the course of decades. For that reason, we give the SPY a Hold rating right now.

Be the first to comment