Slavica/E+ via Getty Images

In this article, I will examine Valmont Industries, Inc. (NYSE:NYSE:VMI) and explain why I believe this is a Hold at the present valuations. The firm is in a strong financial position and carefully grows organically and through acquisition in segments with strong future growth prospects. VMI has an illustrious history and now provides engineered products and services. It primarily focuses on infrastructure development and agriculture, where it supplies irrigation equipment and services. Their four main segments are:

- The Engineered Support Structures business, which develops and engineers access systems, highway safety products, and technology-based solutions for smart cities.

- The Utility Support Structures component of the business emphasizes the support for steel and concrete pole structures (utility transmission) as well as a range of distribution and generation platforms and support.

- The Agriculture business has focused on technology, mechanization of irrigation systems, and water management solutions.

- The Coatings business provides services in galvanizing, painting, and anodizing.

When we look at VMI’s business, it has an interesting diversification that comprises traditional manufacturing elements, a strong ESG focus (such as solar), as well as an emerging powerhouse in its technology support systems for clients, driving service growth.

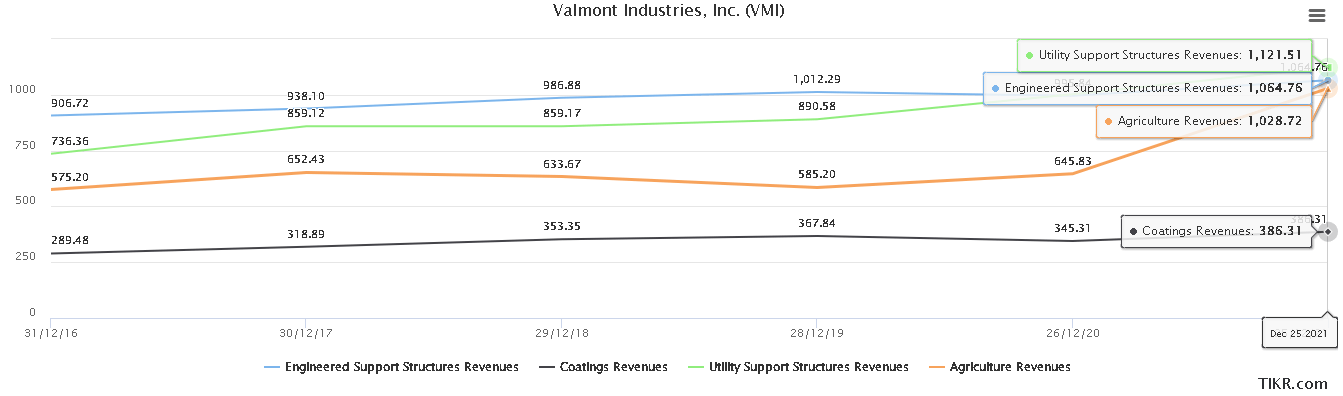

The original core VMI business is more of an ‘old school’ manufacturing with associated services. The coatings, utility support structures, and engineering support structures have maintained relatively steady revenues (Figure 1). The standout in the last year has been the Agricultural segment, with a sharp rise in revenue.

Figure 1. VMI’s four segments by revenue (TIKR terminal)

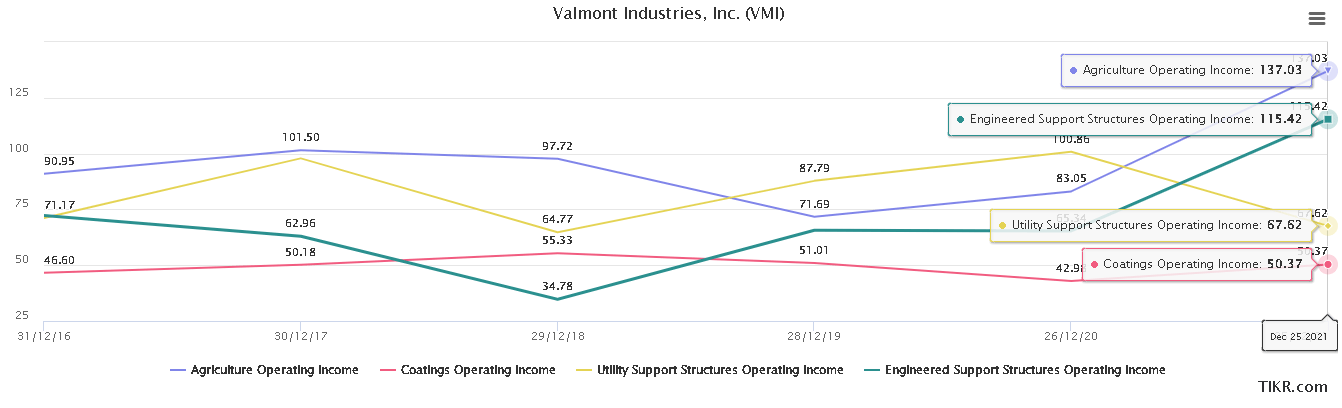

The segments have varying operating income, however, with both Engineering support structures and Agriculture showing increases in operating income in 2021 (Figure 2)

Figure 2. VMI’s four segments by operating income (TIKR Terminal)

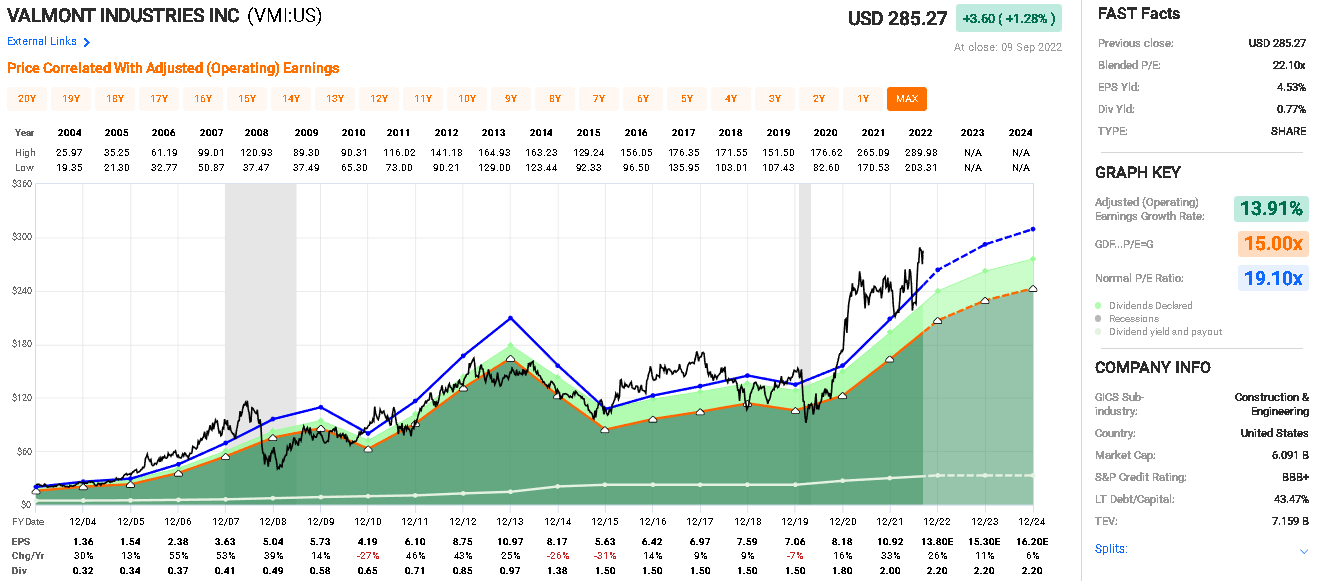

The company has shown periods of strong growth as well as declines in earnings. Figure 3 shows a historical perspective from FAST Graphs, with the orange line representing a 15x P/E ratio of earnings to prices. The blue line shows the normal trading P/E multiple of 19.1x, suggesting the market places a premium on the strength of the company. We can observe declines in earnings (2014 and 2015) and some relatively flat years (2016 to 2019), so I would suggest this is a semi-cyclical behavior resulting in the need to invest at the ‘right price’ to minimize risks and maximize the opportunity to take part in VMI’s growth of future earnings.

Figure 3. VMI’s historic price and earnings performance (FAST Graphs)

The wider environment

During Q2, VMI experienced strong volume growth and relatively consisting pricing, to give improved earnings. Infrastructure revenue was up 24% YoY while Agriculture was up 34% YoY. The additional electrification of power infrastructure over the U.S. is expected to continue, benefiting VMI through their utilities and infrastructure business. The U.S. infrastructural spend is expected to increase. VMI also expects strong growing growth in telecommunications products.

In support of their business in this area, VMI acquired a majority interest in ConcealFab. This provides VMI additional capability to benefit from the 5G roll out with ConcealFab’s 5G infrastructure and passive intermodulation expertise in this area is crucial to the market. The acquisition is a good fit with VMI’s expertise in engineering and manufacturing and expands its capabilities in this area. Finally, Ericsson remains a minority owner in ConcealFab, providing long-term strategic collaboration for VMI. As the CEO notes, ConcealFab has a suite of solutions that synergistically work with VMI’s offerings and the acquisition provides VMI the ability to enhance its international growth (my emphasis in bold):

This exciting transaction aligns well with our strategy to invest in high-growth market sectors and enhances our portfolio of Telecommunication solutions. ConcealFab is a fast-growing industry leader in 5G infrastructure and passive intermodulation, or PIM Mitigation. PIM interference arises when signal at the cell site are mixed which can degrade system performance and lead to unreliable coverage and spotty data speeds. ConcealFab’s portfolio of PIM solutions helps both identify these issues and solve the problem to improve performance.

Joining the Valmont team provides immediate commercial benefits, as we are now able to accelerate expansion in telecom markets in partnership with the industry leader Ericsson who remains a minority owner of the business. This is a tremendous step toward enhancing our access to markets and carriers around the world. With our combined experience in the space and leveraging Valmont’s engineering expertise and global manufacturing footprint, we are positioned to address critical pain points and further accelerate the delivery of 5G technology to the market. We are excited to welcome the ConcealFab team to Valmont.

The power of technology

The emergence of a technology platform has provided a strong opportunity for VMI to extend its revenues. In 2021, VMI started the process to acquire Prospera Technologies, providing access to Prospera’s artificial intelligence and machine learning capabilities. The grower adoption of this platform has expected to show strong growth. The earlier expansion of revenues in the Agricultural segment suggests that this has benefited VMI. Further, the CEO remains very bullish on integrating these types of AI technologies into VMI’s platforms, such as the note in the Q2 earnings call, where he says:

I think the technology definitely enhances the payback story on Pivot. The ability to operate remotely, the ability to get plant insights, particularly around emergence and pest and disease really makes the Pivot a much more valuable tool to the farmer. And so therefore, yes, to answer your question, if the Pivot were static and just all it did was mechanical irrigation, then I think — it doesn’t have the same value proposition. Because most growers’ equipment, other pieces of equipment have advanced in technology as well. And so it’s, I believe, just a simple market expectation. And our solution is pretty unique in the insights area and being able to look at the crop very early on and straight through to the harvest process.

Further acquisitions are likely to be similarly strategically focused on enhancing the core VMI offerings.

Operational matters

There are several things to like about VMI and several things to be cautious about.

In 2014, revenues decreased slightly, and this continued for a couple of years. The business is somewhat cyclical. It has seen good growth since 2017.

They maintain strong levels of assets and cash; the current ratio is 2.22, the quick ratio is 1.3, and the interest coverage is 7.8x (Source: Stock Rover). The operating margins are reasonable compared to the peers (below), at 8.8% compared to the group at 6.9%; however, this also is a decline from 12 to 14% during 2012 and 2013. VMI’s ROIC has been relatively stable and is currently at 10% and has been as low as 4% and as high as 15% over the last decade.

In 2021, they issued about $218 million of long-term debt, an increase of 30%. This is a jump, but overall debt appears to remain at a manageable level.

Finally, they have maintained investment in their operations. This may have been contributing to the increase in assets over the last five years. It is important to their continued competitiveness, as noted in the Q2 call, where the CEO noted that:

the real push is on productivity as a way to gain capacity through the plants. So the capital decisions are more, first and foremost, focused towards automation, improved flow through the facilities, better cutting machines, better welding machines, things that can really help you just move more of the product through your existing footprint. In terms of a big brick-and-mortar, it’s like the last thing that we want to do. And so therefore, we’re going to stay very close to the market. We’ll be very close on lead times.

New plants, such as the concrete manufacturing facility in Indiana, also support long-term ESG efforts with an emphasis on low-carbon transmission poles. Further, the site will be supported by a 500kW solar array installation that should fully power the location.

Peers

Given the diversified nature of VMI, which I consider to be one of the core strengths of the business, selecting appropriate peers is a little challenging. I used some peers from Seeking Alpha in the construction and engineering business, and a couple of others, primarily in the infrastructure business. These are incomplete comparisons, given the more diversified nature of VMI.

- Gibraltar Industries, Inc. (ROCK)

- Ameresco, Inc. (AMRC)

- Fluor Corporation (FLR)

- EMCOR Group, Inc (EME)

- MasTec, Inc. (MTZ)

- Steel Partners Holdings L.P. (SPLP)

- MDU Resources Group, Inc. (MDU) – this is another conglomerate with a similar industrial focus.

Looking through these peers, the more industrial companies have lower valuations, generally. Firms with more diversified operations, such as VMI, tend to have richer valuations at this point in time. While the table lists the firms alphabetically, AMRC (at the start) and VMI (at the end) appear to be trading at the highest multiples with the EV/EBITDA quite elevated for AMRC, with VMI still a reasonable way ahead of the peers. Most of the firms are trading at P/S multiples at or below 1.0, except for AMRC and VMI. The P/B multiples are more variable, but, again, VMI and AMRC are considerably greater than the peers.

From this, we can get a sense that, relative to comparable companies, VMI appears to be moderately overvalued.

| Company | P/E | EV / EBITDA | P/S | P/B |

| Ameresco (AMRC) | 41.5 | 25.6 | 2.3 | 5.1 |

| EMCOR Gr (EME) | 17.2 | 10 | 0.6 | 3.1 |

| Fluor (FLR) | 64.9 | 8.5 | 0.3 | 2.6 |

| MDU Resources (MDU) | 19 | 11.3 | 1 | 1.8 |

| MasTec (MTZ) | 36.4 | 12.1 | 0.7 | 2.5 |

| Gibraltar Industries (ROCK) | 16.8 | 10 | 1 | 1.6 |

| Steel Partners Holdings (SPLP) | 7.1 | 3.3 | 0.7 | 1.3 |

| Valmont Industries (VMI) | 28.3 | 15.9 | 1.6 | 4.1 |

| Summary | 19.3 | 12.1 | 0.8 | 2.3 |

Capital allocation decisions

From the 2021 Annual Report, we can see a clear focus on both share repurchases and dividend payments. The effectiveness of share repurchases appears to have been good since it was announced in 2014. By the close of 2021, approximately $878 million had been used to acquire shares at an average price of about $135. The purchases appear to have been in the earlier years, suggesting sensible capital allocation at those prevailing lower prices.

The other major tranche of capital allocation is their dividends. The current yield is 0.77%, which is low, but Seeking Alpha’s Dividend Grade for safety is a strong “A+”, reflected in the lower payout ratio of 17.40%. The five-year DGR is only 6.96% which is reasonable. Together, however, this suggests that the opportunities at VMI will not excite many dividend growth investors. From 2015 to 2019, the dividend payments were static.

Valuation and opportunity

When looking at an investment opportunity, I like to consider both historic performances as well as the likely future performance. Historically, as I noted, the firm has performed strongly but has elements of a semi-cyclical company with inconsistent revenue and earnings growth. It has had periods of strong performance punctuated by declines (Figure 3).

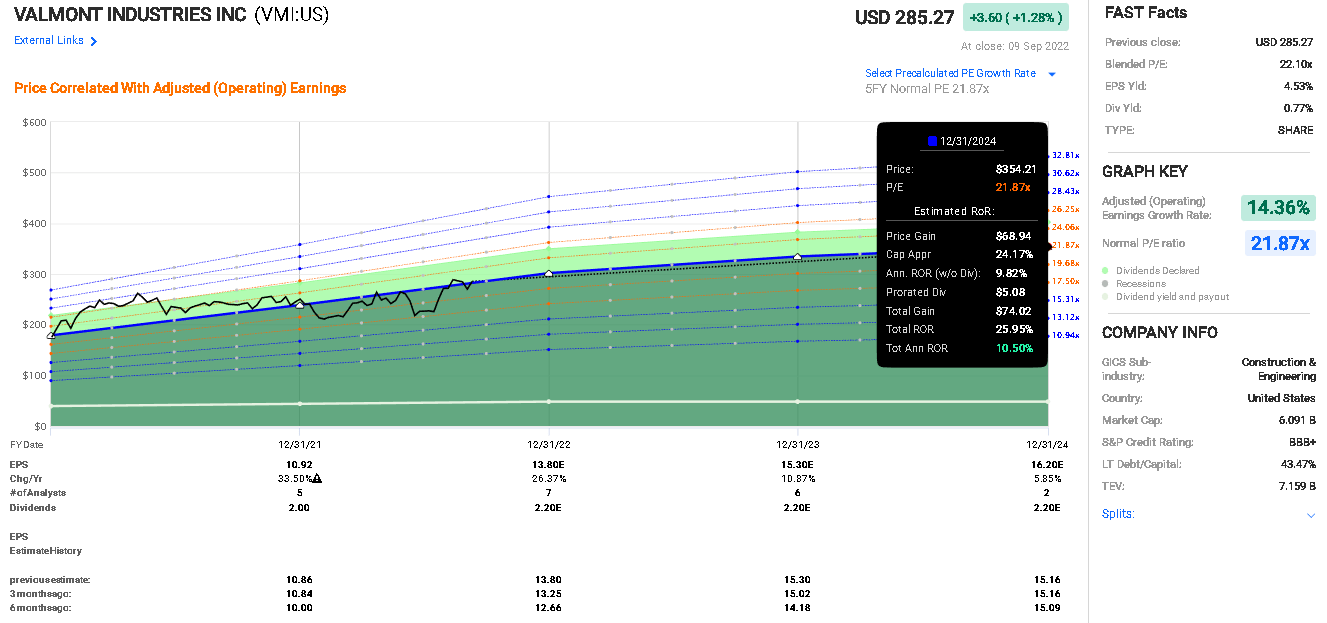

Using FAST Graphs, I can rapidly assess future earnings (using analysts’ estimates) and likely returns if prices maintain particular P/E ratios compared to the estimated earnings. For example, if we look at Figure 4, we can see the blue line shows a historically normalized P/E ratio of over 21x. This is moderately high (see the peer comparison above), but it represents the strength and growth of the company in recent years.

If prices maintained this normalized P/E ratio, by 2024, we may expect approximately a 26% total rate of return (Figure 4). We should interpret this with some caution as it requires both prices to remain at this multiple and the earnings estimates to be met. Fortunately, FAST Graph’s analyst scorecard gives a 77% hit or beat over the two-year forward estimates (with a 20% margin of error), suggesting these are reasonable estimates. Further, the data at the bottom of Figure 4 shows that the analyst estimates remain relatively static over the last 6 months with slightly upward revisions of earnings estimates.

Figure 4. VMI’s potential return if prices adjust to the normalized P/E based on analysts’ expectations (FAST Graphs)

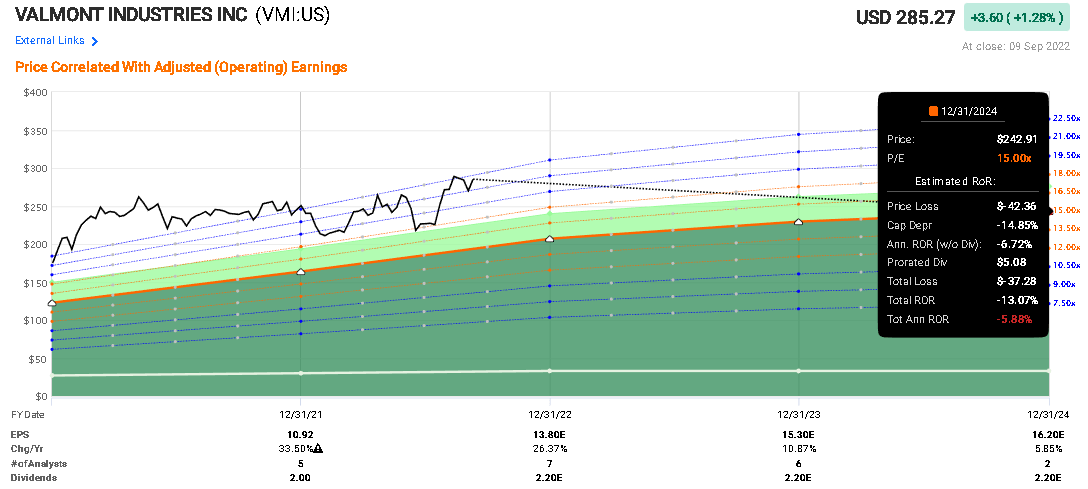

If you are more risk averse, like me, you may be concerned about what would happen if prices took a tumble. To illustrate the risks of the current valuation, I use turned to FAST Graphs and inputted a 15x P/E at 2024. From Figure 5, we see that this would generate a -13% total rate of return; the decline in prices not being substantially offset by VMI’s small dividend yield.

Figure 5. VMI’s potential return if prices adjust to the normalized P/E based on analysts’ expectations (FAST Graphs)

At what point would I consider VMI a compelling buy? I would suggest that at about $220 (as they were a few months earlier in July) the expectation at a 15x P/E by 2024 would be a 13% total rate of return, while at a normalized 21x P/E it would be around 112% total rate of return. In my mind, that would present a more reasonable balance of risk and reward for new investors, where the entry price would enable an investment to fully benefit from the growth in VMI’s earnings.

While I think the strength of VMI warrants a greater than a 15x P/E multiple, my concern is that the maintenance of the current multiple would be challenging and there is room to fall from the present, somewhat elevated, levels.

Analysts’ reports on Stock Rover have this as a ‘Strong Buy’ (4x) and ‘Hold’ (1x) and Yahoo Finance suggests there is a 10% long-term (5 years) per annum growth rate expected. While I broadly agree with these expected earnings, I remain concerned about the present valuation of VMI and will be waiting for a better entry price.

Thesis

This is a strong and well-established conglomerate with a long history. There are expectations of strong future growth in earnings and revenue. The firm undertakes carefully researched and synergistic acquisitions that benefit its product and service offerings. The business remains strong and has attractive future growth prospects in all of its markets with new growth opportunities through acquisitions.

The current market price and valuation appear slightly elevated relative to both VMI’s peers and the analysts’ expectations of earnings at this time. If the prices maintained the current P/E ratio, this would be reasonable, but there is also the risk of a decline in the P/E that could cause small capital losses for new investors.

Given the strength of VMI’s business and their long-term success, at the current valuation, I rate this as a Hold and will watch carefully for further buying opportunities at levels closer to $220, such as they were in July 2022. Add VMI to your watchlist!

Be the first to comment